Sample Category Title

Market Morning Briefing: Euro Might Drop Lower To Test Support

STOCKS

Dow (24103.11, +1.07%) has risen a bit. Overall trade within 23500-24500 is likely to continue in the near to medium term. The index could face some rejection from 24500 levels which could push it down to 24000 or lower.

Dax (12096.73, +1.31%) is trading within the channel region of 12300-11700 just now. A rise towards 12200-12300 is possible in the next couple of sessions followed by a fall towards 12000 or lower.

Nikkei (21555.64, +0.47%) is trading above immediate resistance near 21400 and while that sustains, the index could move up towards 21800-22000 levels in the near term. Else a fall back towards 20800-20600 could be seen in the coming sessions.

Shanghai (3183.22, +0.45%) is holding well above support at 3100. A break above 3200 is needed to take it higher to 3250; else the index could be stuck in the 3200-3100 region for some more sessions, trading sideways.

Nifty (10113.70, -0.69%) may come down to 10020 while below interim resistance near 10200. Near term downward channel as shown on the daily candles may hold for now.

Sensex (32968.68, -0.62%) is also likely to come off towards 32500 while below 33250. Near term looks bearish.

COMMODITIES

Brent (69.74) and Nymex WTI (65.20) could re-attempt a rise in the near term towards 71.50 and 67 respectively. The bnext few sessions could be ranged with a possibility of rising in the medium term.

Gold (1333.40) could get some support near 1320 which could attempt to push the prices to higher levels of 1340 again. Note that 1320-1315 could give some immediate support just now. A break below 1315, if seen could again take it down towards 1300.

Copper (3.0455) got some support near 2.90 from where the price has come up to trade above 3.04 again. While the rise sustains, there could be scope of further rise towards 3.10-3.12 in the near term.

FOREX

A downward channel on daily candles for the Dollar index (89.96) could get confirmed if it dips from current levels. Some resistance could be provided by the 13 weeks moving average on the weekly line chart, but a breach of that would mean a test of higher resistance (on weekly line chart and 3 day candles) near 91 and a dip thereafter. A test of 91 is slightly more preferred this week.

Euro (1.2321) might drop lower to test support on 3 day candles and daily line chart near 1.225 this week. However, that would imply a break of immediate support on daily candles near 1.23, which could happen simultaneously with the Dollar Index breaching the 13 weeks moving average.

Dollar Yen (106.34) is moving in a slightly downward channel on daily candles and has dipped after testing resistance near 106.93. It could dip lower this week back towards levels near 106.0-105.5.

Euro Yen (131.02) after testing resistance near 131.5-132.0 on daily candles last week, might see a dip towards support on 3 day candles near 130 this week.

Pound (1.4045) unexpectedly broke support on the upward channel on daily candles last week and should now find support near 1.395-1.390 this week, from where it could then bounce.

Dollar Rupee (65.175) - Resistance at 65.25 has held. See 65.00 and 64.85 this week.

INTEREST RATES

US long term yields have continued falling as investors seem to be shifting away from volatile equity markets into safer debt. This is in line with our earlier expectation of a slow decline in yields, which might continue through Apr-May.

US 10 Yr Yield (2.7625%), 30 Yr (2.9927%), 5 Yr (2.589%), 2 Yr (2.28%) :

The 10 Year yield as per our expectation has touched 2.75% and might now find support near current levels on the medium term chart.

The 30 yr yield is moving in a downward channel on the short term chart and might see a bounce from support near current levels in this week.

China starts tariffs on 128 US products, in response to 232 steel tariffs

China formally starts the tariffs on 7 types, 128 products from the US today, according to a statement (link in simplified Chinese) by the Ministry of Finance. This is part of the packaged announced last month which targets up to USD 3b in imports. And it's a counter measure to the 232 steel and aluminum tariffs of the US that's non-geo-targeted.

China's response is seen by many as symbolic so far, and refrained. And the impact should be negligible comparing to the size of the bilateral trading relationship between the countries. Also, it's reported that the US is already in negotiation with China regarding a trade deal. However, for now, China is still holding the cards regarding the Section 301 tariffs, which are targeted on Chinese goods that adds up to USD 50-60b of value.

Talking about the Section 301 tariffs, Trump administration is expected to announce the list of products to be affected. It's believed that the list will concentrate on those affected by intellectual property theft only. And a major portion would be cutting-edge technology products.

EUR/USD Holding Crucial Support Near 1.2280

Key Highlights

- The Euro traded lower recently towards an important support at 1.2280 against the US Dollar.

- There is a major bullish trend line forming with support at 1.2285 on the 4-hours chart of EUR/USD.

- The pair must hold the stated 1.2280 support to start a fresh upward wave.

- Today, the US Manufacturing PMI for March 2018 will be released, which is forecasted to decline from 55.7 to 55.6.

EURUSD Technical Analysis

There was a downside reaction from the 1.2475 level in the Euro against the US Dollar. The EUR/USD pair declined and it is currently trading near a major support above 1.2280.

Looking at the 4-hours chart, there is a decent support base forming above the 1.2280 level. There is also a major bullish trend line forming with support at 1.2285 on the same chart.

However, the pair is trading well below the 100 (red) and 200 (green) simple moving averages (4-hours). At the moment, the pair is testing the 23.6% Fib retracement level of the last decline from the 1.2476 high to 1.2283 low.

The pair has to move above 1.2330 and the 100 (red) and 200 (green) simple moving averages (4-hours) to start a fresh upward wave. The next hurdle on the upside could be the 50% Fib retracement level of the last decline from the 1.2476 high to 1.2283 low at 1.2380.

On the downside, the trend line support near 1.2285-90 and the 1.2283 low holds a lot of importance. A break and close below the stated supports could ignite further declines towards the 1.2200 and 1.2180 support levels in the near term.

China Caixin PMI manufacturing showed “marginal weakening” in March

China Caixin PMI manufacturing dropped to 51.0 in March, down from 51.6 and missed expectation of 51.7. That's also the lowest level in four months.

Quotes from the release by Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group:

Quotes from the release by Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group:

- "The Caixin China General Manufacturing PMI fell to 51.0 in March. The sub-indices of output and employment both fell from the previous month, while new orders increased at a slightly slower rate, highlighting that the deceleration in the manufacturing sector was mainly driven by the supply side and that demand has remained relatively stable.

- "Output prices rose at a faster pace in March than in the previous month while the increase in input costs weakened markedly, which will help shore up manufacturers' profits.

- "The willingness of companies to restock waned as, apart from a slower expansion in output, the growth rates in stocks of finished goods and stocks of purchases also declined in March.

- "Overall, the manufacturing PMI reading in March showed that demand was not as strong as expected, leading to lower willingness of manufacturers to produce and restock. However, the ability of manufacturers to make a profit was beefed up by the stable increase in new orders and the much slower jump in input costs.

- "The growth momentum of the Chinese manufacturing economy may have weakened in March, but at a marginal pace."

Released over the weekend, however, the official China PMI manufacturing rose to 51.5, up from 50.3. Official PMI manufacturing rose to 54.6, up from 54.4.

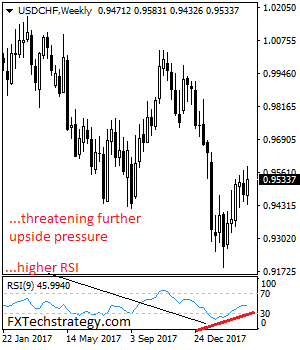

USDCHF – Takes Back Previous Week Losses

USDCHF - With the pair closing higher to reverse its previous week losses the past week, more strength is envisaged. On the downside, support lies at the 0.9500 level. A turn below here will open the door for more weakness towards the 0.9400 level and then the 0.9350 level. On the upside, resistance resides at the 0.9600 level where a break will clear the way for more strength to occur towards the 0.9650 level. Further out, resistance comes in at the 0.9700 level. Above here if seen will turn attention to 0.9750. All in all, USDCHF faces further upside pressure.

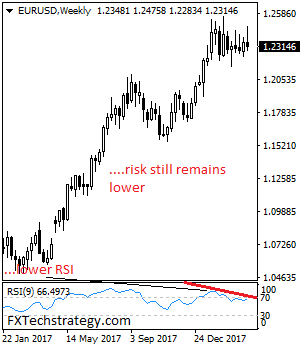

EURUSD – Continues To Retain Downside Pressure

EURUSD - The pair continues to hold on to its downside as it looks to extend its correction. On the upside, resistance comes in at 1.2350 level with a cut through here opening the door for more upside towards the 1.2400 level. Further up, resistance lies at the 1.2450 level where a break will expose the 1.2500 level. Conversely, support lies at the 1.2250 level where a violation will aim at the 1.2200 level. A break of here will aim at the 1.2150 level. Below here will open the door for more weakness towards the 1.2100. All in all, EURUSD faces further downside threats.

Japan Tankan shows slight deterioration in large manufacturer sentiment

Japan Q1: Tankan survey results:

- Tankan Large Manufacturing Index Q1: 24 vs exp 25 vs prior 26

- Tankan Large Manufacturers Outlook Q1: 20 vs exp 22 vs prior 21

- Tankan Large Non-Manufacturing Index Q1: 23 vs exp 24 vs prior 25

- Tankan Non-Manufacturing Outlook Q1: 20 vs exp 21 vs prior 20

- Tankan Small Manufacturing Index Q1: 15 vs exp 14 vs prior 15

- Tankan Small Manufacturing Outlook Q1: 12 vs exp 10 vs prior 11

- Tankan Small Non-Manufacturing Index Q1: 10 vs exp 8 vs prior 9

- Tankan Small Non-Manufacturing Outlook Q1: 5 vs exp 5 vs prior 5

- Tankan Large All Industry Capex Q1: 2.3% vs exp 1.0% vs prior 6.4%

There were slight deterioration in large manufacturing index from 26 to 24 and missed expectation of 25, and large manufactorers outlook from 21 to 20, missing expectation of 22. Over business confidence were firm though. The fall in confidence and outlook is likely more due to Yen's recent appreciation. And so far, the fear of a global trade war had limit impact on sentiments.

The indices were calculated, like many other similar series in the world, by subtracting the number of respondents saying conditions are poor from those responding conditions are good.

Also released from Japan, PMI manufacturing was finalized at 53.1 in March, revised down from 53.2.

Spring Has Sprung And Hope ‘Springs’ Eternal

Spring has Sprung and Hope 'Springs' eternal

Off to a slow start, as market participants slowly filter back after the holy junction of Easter and Passover.

Spring has sprung, and so have green shoot progress on the US/China trade front, but investors continue to struggle with the new normal of higher market volatility, and lower returns after the S&P 500 recorded its first quarterly losses since 2015. The debate over global trade continues to simmer, and the regulation of technology sectors amidst the Facebook security breach has steadily eroded investor sentiments.

The market's biggest fears about escalating trade war and higher US interest rates have tentatively blown over suggesting investors will shift into bargain-hunting mode. However, unlike the start of the year, investors appear less concerned about fear of missing out and continue to be more worried about the fear of getting out. Investors have been riding overweight tech sector positions for just about ever, but tighter regulation in the tech sector suggests the so-called FAANG group of stock (Facebook, Apple, Amazon, Netflix and Google) are at a significant inflexion point. And while hope springs eternal for much of the tech sector in general, the industry behemoths could continue to be investors punching bags while libraries worth of regulatory oversight get ironed out.

The USD remains surprisingly unshakable despite the ongoing Muller investigation, a dovish start to Jay Powell tenure at the Fed, the revolving door at the Whitehouse and mushy wages. While the USD sell signals are less precise than traders idle banter suggests, none the less there could be an early bias to re-engage USD shorts this week, as causality would indicate that the US dollar, in the absence of quarter end flow, would fall prey to exigent themes. Or at least until trader talk is walked. But getting less attention than it really should is the PCE price index, which showed a year-on-year uptick of 1.6 percent in February from 1.5 percent in January which suggests the markets current three rate hike scenarios for this year could be looking a tad dovish on flickering inflation embers.

The IMF reported the US dollar share of global currency reserves has fallen to the lowest in 3 years. Not overly surprising given the strength in the JPY this year has attracted a lot of attention from reserve managers. Not to unsurprising that traders are not alone in their longer-term view of the greenback. No one is especially eager to buy $ these days, including centeral banks.

Asian risk premiums continue to swing on the macrame of trade wars, tech losses and the Korean summits. But the inclusion of Chinese government bonds in the Bloomberg Barclays Global Aggregate Index is a significant coup. And with two more indexes inclusions expected this year, this will be a massive boost for capital inflows and provide anchors for the domestic market structure. Also, it will give a positive knock-on effect on regional sentiment as the RMB complex continues to steady the local ship.

While three month LIBOR continues its assent passing through higher funding costs as institutional market participants borrow through a LIBOR facility. On Monday, the Federal Reserve Bank of New York begins publishing the SOFR. The Secured Overnight Financing Rate aims to be more reliable and less artificial. But keep in mind the new SOFR rate will only be applied to overnight funding transactions.

Oil Markets

The market will continue to digest signals from whether or not the US administration will scrap or maintain the fragile nuclear deal with Iran. So political headlines will remain essential in the absence of any market report from OPEC or IEA. The possible return or Iranian oil sanction will continue to drive near-term sentiment. Although US shale producers continue pumping out an and eye-catching estimated 10.4 million barrels per day, the US massive export market that has grown from a small number of tankers to a burgeoning 7.7 million barrels of crude per day will continue to dry up inventories. So much so that even trader disappointment over US inventory builds and the new high in estimated crude production remains short-lived. As downward pressure remains on US inventories, Oil prices will continue to stay hypersensitive to global supply disruptions.

Adding to the positive vibe, Baker Hughes reported its first fall in weekly rig count in three weeks.

Gold Markets

Gold traders will continue to take their cues from broader USD sentiment. Geopolitical risk premiums are slipping with Korea back in the headlines for all the right reasons: North and South Korea will host a historic summit on April 27, with both countries' leaders meeting face-to-face and Besides with the fear of full-blown global trade war receding bullish geopolitical cues remain subtle. And while the frightening thoughts of an escalation of West -Russia tensions remained real but given the tit for tat response from Russia so far, Gold will be at the mercy of an oscillating dollar to start the week. Over the longer term, however, the burgeoning US debt will be met with fewer and fewer buyers as we slide closer towards an inflationary storm. So with investors trepidation likely to continue overwhelming markets, gold should remain in favour.

G-10 Currency Markets

We're at curious crossroads in currency markets, and last weeks USD dollar demand will be of particular discussion as traders turn on their terminal to start the week. Prattle at the top of the cue is last weeks merciless position squeeze on USDJPY, risk off trade, Fed gradualism, surging LIBOR and flickering optimism on the inflation front after a sturdy PCE print. And while trade concerns loom, traders will be particularly happy for a return to basics as the diary is chalk full of tier one economic data to play off. But G-10 traders remain in desperate need of a wild card to put in play and perhaps this week AHE report will see those cards pressed into duty. But bearish dollar views need to pay very close attention to the data front as Q2 could be pivotal in both US economic and Fed policy terms. And while it's unlikely the US dollar underwent something of a Damascene conversion last week, don't write off dollar just yet – last week was a surprisingly good one for the Greenback.

Japanese Yen

How much of this squeeze has to do with quarter end/Japanese fiscal year-end flows remains to be seen. But the market has taken out some significant levels on its way the way to the most extended USDJPY rally of the year. Of course with' risk off 'abound the temptation is to fade the extremes with 108 widely subscribed as the long-term short dollar KO zone.

The Euro

The EURO remains sidelined at the moment, at the mercy of broader USD moves. And while an April ECB policy shift is far too early even to consider, traders continue to view the June meeting as the big shifter. In the meantime, markets remain guardedly long EUR given the skewed propensity for a negative tail risk surprise from both US economic data and US politics. But that could change swiftly

The Australian Dollar

The Aussie will get absolutely no help from the RBA meeting where no change is s widely expected and for the RBA to maintain its neutral bias. RBA guidance remains exceptionally consistent; the economy is doing well they need to stay patient for wage growth to kick in before shifting policy rates.

$Asian X Japan Currency Markets

Investors' are realizing that regional currencies could experience a hawkish shift as the North Korean political olive branch continue to suggest an easing of risk in the peninsula while the US and South Korea agree on KORUS amendments. But the rush is on to avoid the US designation as a currency manipulator as Seoul will soon go public with foreign exchange market interventions.

But in general, regional traders remain focused on trade tension, but with the US administration on the charge about ' currency manipulation 'again, it suggests that a weaker US dollar will be a by-product of policy rather than the fall guy stooge. With the US administration connecting regional currency policy to trade, its thought that this would limit regional central banks ability to intervene in currency markets, so traders continued to sell dollar against the local basket last week. But with Tech sector headed for regulatory clampdowns, the regional fall out remains a bit of a mystery.So regional equity market inflows and risk sentiment will remain fickle.

Growth in China manufacturing sector registered higher than expected in March as steel mills and an easing of trade fears continues to drive sentiment. The official Purchasing Managers' Index (PMI) released on Saturday rose to 51.5 in March, from 50.3 in February, and was solidly above the 50-point breakeven market. The mainland economy continues to churn despite some fear that deleveraging and regulation could hurt output.Improving PMI's implies better GDP print and provides regulators with more wiggle room on the regulatory and deleveraging front. It also clears up any lingering debate about last months PMI drop due to Lunar New Year effect

The Chinese Yuan

The inclusion of Chinese government bonds in the Bloomberg Barclays Global Aggregate Index is a huge win and with at least two more index announcements likely this year, this will bode well for capital inflow and will act as a stable anchor for domestic bond markets market.

And within the context of the trade negotiations its thought that a weaker US dollar will be an active ingredient to the process, so local traders continue to buy the Yuan

The Malaysian Ringgit

The easing of North Korea tensions is providing a positive backdrop to an already buoyant domestic Malaysian landscape and are offering a massive boost to local currency markets including the Ringgit. Malaysia had severed trading ties with North Korea over the brazen assassination of Kim Jong-Nam Kuala Lumpur International Airport in February 2017 but may be more willing to offer concession now. Strategically it makes sense as Malaysia will pick up another local trading partner.

On the market side of the equation, The Ringgit remains buoyant on the back of stable Malay bond markets. But with Malay election the next local headwind, we could see a slow down in offshore flows which are most typical ahead of any regional elections, but markets are expected to remain stable within current ranges.

Oil prices continue to trade firm, and with regional sentiment improving, the Ringgit should continue to benefit from both strong domestic and external factors.

Eco Data 4/2/18

[php_everywhere instance="1"]

Summary 4/2 – 4/6

Monday, Apr 2, 2018

[php_everywhere instance="1"]

Tuesday, Apr 3, 2018

[php_everywhere instance="2"]

Wednesday, Apr 4, 2018

[php_everywhere instance="3"]

Thursday, Apr 5, 2018

[php_everywhere instance="4"]

Friday, Apr 6, 2018

[php_everywhere instance="5"]