Sample Category Title

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4000; (P) 1.4029; (R1) 1.4048; More....

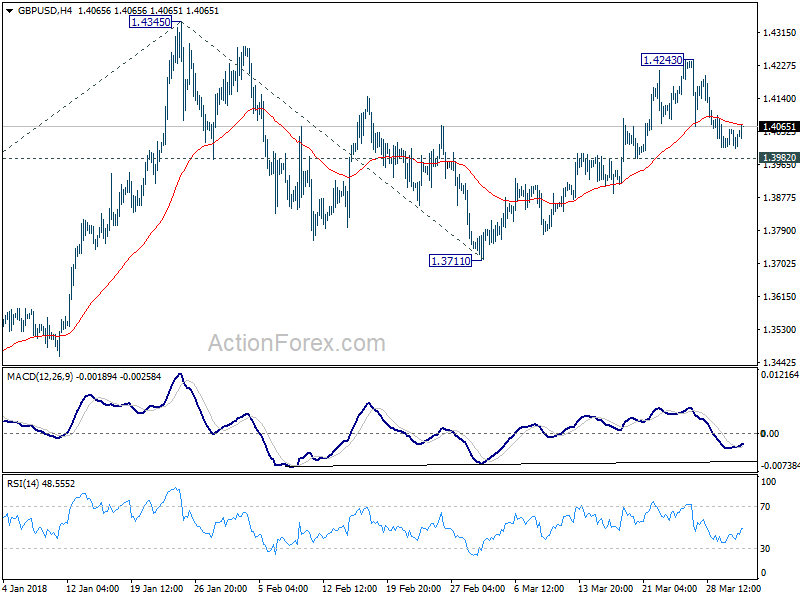

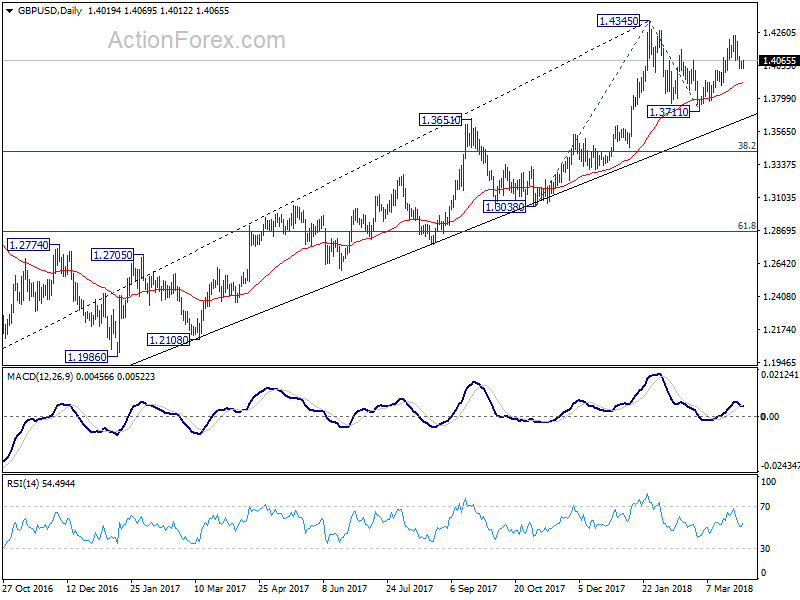

GBP/USD recovers ahead of 1.3982 minor support but it's limited well below 1.4243 so far. Intraday bias remains neutral for the moment. With 1.3982 minor support intact, further rise remains mildly in favor. On the upside, above 1.4243 will resume the rise from 1.3711 and target 1.4345 high first. Decisive break there will resume larger up trend and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, however, firm break of 1.3982 will indicate completion of rebound from 1.3711. In that case, intraday bias will be turned back to the downside for retesting 1.3711.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

EUR/USD Bullish Head And Shoulders Pattern During Bank Holiday

The EUR/USD has been contained in arrange during the Easter holiday. Banks are on holidays, so the slow-moving price is a regular thing. On Friday and early Monday, the EUR/USD has formed a bullish SHS pattern, and we might see a breakout to the upside or a continuation move possibly during US session. However, this could also be a false move due to thin liquidity that usually happens on holidays due to fewer market participants. If technical analysis is followed, then the pair should spike from 1.2310-10 zone and close above the SHS trend line (green). A close above targets 1.2370. 4h close or strong H1 momentum candle above 1.2370 targets 1.2423. As long as 1.2264 holds the price, bulls should be safe.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

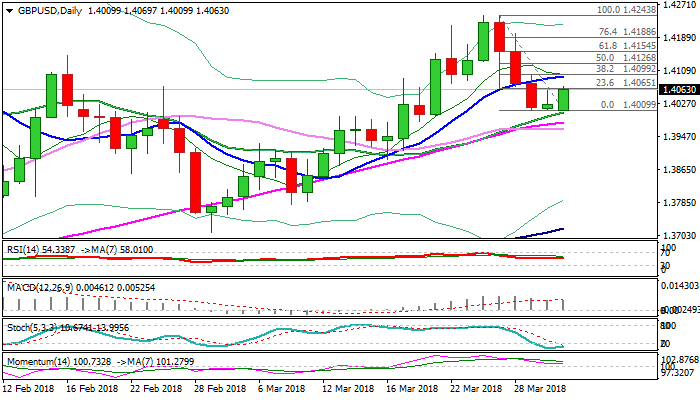

GBPUSD: Daily Cloud Top Continues To Underpin, But Recovery Needs To Clear 10SMA For Stronger Bullish Signal

Cable moves higher on Monday after the third straight rejection at 1.4010 (daily cloud top) and attempts to generate fresh bullish signal on probe above Friday's high at 1.4060 (also Fibo 23.6% of 4.4243/1.4010 bear-leg). Thick daily cloud continues to underpin (cloud top is reinforced by rising 10SMA), however, bulls need confirmation on firm break above 1.4093/99 (10SMA / Fibo 38.2%) to signal stronger recovery. Slow stochastic is reversing in oversold territory and may support scenario, but risk is seen on weakening momentum. Failure to clear 10SMA could be selling signal, but the pair may hold in extended consolidation while cloud top / 20SMA. Look for stronger direction signals on lift and close above 10SMA or loss of cloud top /20SMA lower pivots.

Res: 1.4099, 1.4126, 1.4154, 1.4188

Sup: 1.4010, 1.3981, 1.3966, 1.3915

Equities Soften As China Retaliates, US ISM Manufacturing PMI Pending

Here are the latest developments in global markets:

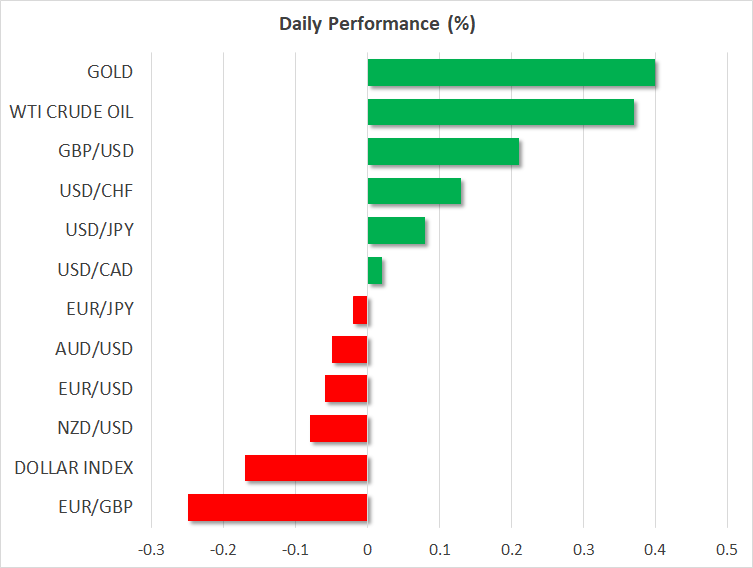

FOREX: The dollar index was nearly 0.2% lower on Monday to start the new quarter, amid continued concerns over a US-China trade dispute escalating following the latest tariffs by China, due to take effect today. The British pound was on the front foot, gaining against both the dollar and the euro, extending the significant gains it posted in the first quarter amid a reduction in Brexit uncertainties.

STOCK: US markets remained closed on Friday, in celebration of the Good Friday holiday. Trading will resume today in the US, and futures tracking the S&P 500, Dow Jones, and Nasdaq 100 are all currently in negative territory, signaling a lower open for these indices, possibly due to the announcement of new tariffs by China against the US. In Asia, Japanese indices started the quarter on a soft footing, with the Nikkei 225 and Topix declining by 0.31% and 0.44% respectively. Other Asian markets, like Hong Kong, stayed closed both on Friday and today for public holidays. Europe was a similar story, with almost all the major benchmarks set to remain shut today as well, in celebration of the Easter Monday holiday.

COMMODITIES: In energy markets, oil prices are higher to start the quarter, with WTI and Brent crude rising by nearly 0.5% and 0.6% respectively. Factors currently supporting prices include speculation that US production may be slowing down a little, following the latest Baker Hughes rig count showing a decline in active rigs, as well as expectations that the US could introduce fresh sanctions on Iran. In precious metals, gold is 0.4% higher on Monday, recouping some of the losses it posted in the prior week.

Major movers: Trade concerns back in the forefront as China slaps tariffs on the US

The US dollar index was slightly lower today, as the “trade war” saga got a new chapter. Effective today, China introduced extra tariffs of up to 25% on several US goods including food and wine, in response to the US tariffs on steel and aluminum. While the market response has not been massive so far, this is a particularly important development, as China is sending the message that it’s not hesitant to play the “tit-for-tat” game with the US.

The key question now for markets is whether, and how, the US will respond. Any announcement of fresh US countermeasures would further increase the risk of a retaliatory trade dispute escalating out of control, and could therefore take its toll on risk appetite. Such an outcome may spell more troubles for equities. Overall, risk sentiment is highly fragile at the moment and for it to recover, markets may need to see signs that this situation is simply a prelude to serious trade negotiations between the US and China, and not the beginning of something bigger.

The British pound was higher, gaining 0.20% and 0.25% against the dollar and euro respectively, with no clear fundamental catalyst behind the move.

Elsewhere, the yen remained largely unaffected by the BoJ’s Tankan survey for Q1 overnight, perhaps due to the mixed batch of data. Although most of the small-business indices beat their forecasts, most large-business prints disappointed. The results suggest that while Japan’s largest firms are still optimistic about the future, there are some signs of anxiety, particularly among big manufacturers.

Overall, there was very little to suggest any change in tone by the BoJ is imminent. As for the yen, the new Japanese fiscal year starts today. This is a period typically associated with Japanese funds moving money out of Japan, which in isolation, is a factor arguing for a weaker yen. Of course, the currency’s performance will also depend on any developments on the trade front, given the yen’s status as a safe-haven that strengthens when global uncertainties are riding high.

As for the antipodeans, both aussie/dollar and kiwi/dollar were marginally lower, perhaps due to the disappointing Chinese Caixin manufacturing PMI overnight.

Day ahead: Trade tensions remain in the spotlight; US ISM Manufacturing index set to lose steam

With Canadian, Australian and most of the European trading centers still being shut for Easter holidays, the focus will turn to the US where Easter Monday is not a public holiday and the economic calendar has some data to deliver today.

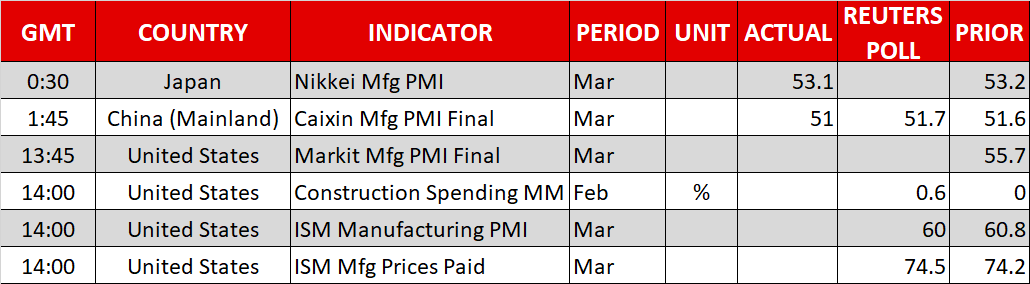

Particularly, at 1400 GMT, the Institute of Supply Management (ISM) will release the US Manufacturing PMI, with the index expected to decline from a 14-year high of 60.8, to 60.0 in March. However, as long as the index remains above 50, the sector is seen as being in expansion. Earlier, at 1345 GMT, the final Markit Manufacturing figure will also attract attention.

Still, the dollar might be more sensitive to any trade headlines that could deteriorate or ease trade tensions between the US and China following China’s decision on Sunday to retaliate to the US import tariffs on steel and aluminum. Investors were somewhat relieved during the previous weeks that things could work out between the countries, after US and Chinese officials showed their willingness to start with negotiations. But yesterday’s news brought new headaches to traders who are now concerned that the sell-off in stock markets might stretch to the second quarter, while safe-haven assets including the yen and gold might experience further demand. Friday’s nonfarm payrolls report could provide support to the dollar if the numbers indicate a tighter labor market, probably showing a fall in the unemployment rate and an acceleration in wage growth. Still, until then, the greenback could remain under pressure if trade tensions intensify in the following days, amid speculation that a global trade war could be around the corner.

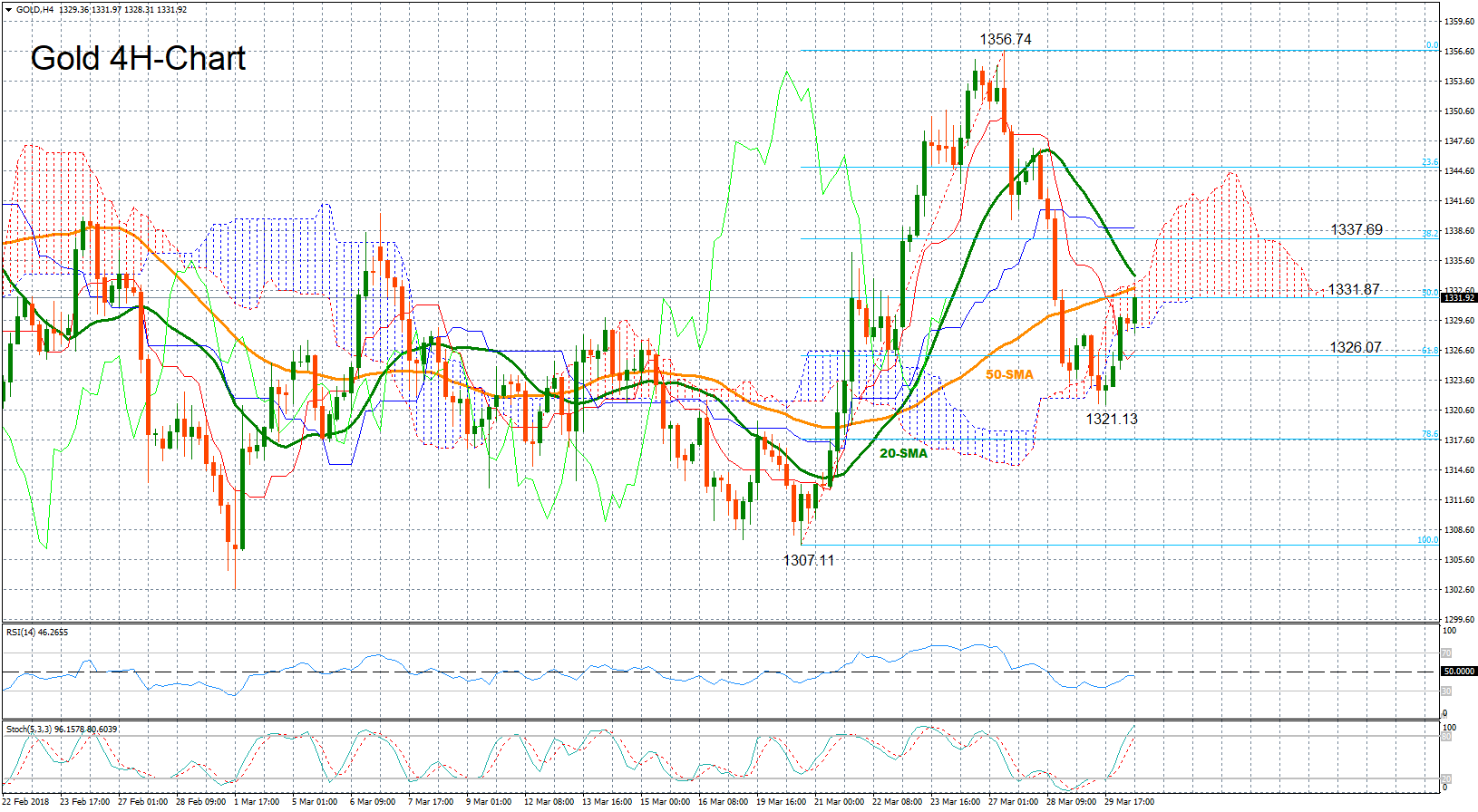

Technical analysis – Gold heads up but risks remain on the downside

Gold increased its positive momentum on Monday as the dollar was on the back foot, but the sentiment in the market remains bearish in the four-hour chart given that the RSI is still trending below 50, while stochastics are on track to post a bearish cross in overbought territory.

Should risk aversion deepen, the precious metal, which tends to rise when investors are concerned, could crawl up to 1,333 key-level, meeting its 50-period simple moving average before it targets the 20-period SMA at 1,334. Above from there, the next stop could be at 1337.69, which is the 23.6% Fibonacci of the upleg from 1307.11 to 1356.74.

On the downside, any headline that could ease uncertainties around the trade story could push gold down to the 61.8% Fibonacci of 1,326.07, while steeper declines could see a retest of the previous low of 1321.13.

EURUSD Holds Within Sideways Channel In Short-Term, Ascending Move In Medium-Term

EURUSD remains under pressure and has been trading within a sideways channel since January 12 with upper boundary the 1.2540 resistance level and lower boundary the 1.2160 support level. During Friday’s trading session, the price snapped a three-day losing streak and posted a bullish candle.

Having a look at the bigger picture, the single currency has been developing within an ascending tendency versus the greenback over the last year.

Looking at the technical indicators, in the daily timeframe the MACD oscillator is falling marginally and is below the trigger line but remains in positive territory, while the RSI indicator is holding near the threshold of 50 with weak momentum. It is worth mentioning that the pair is stuck below the 20 and 40 simple moving averages (SMAs) and a bearish crossover has been created.

An upside potential move above the SMAs could drive the price towards the 1.2470 barrier. A successful break above this level could extend gains until the more than 3-year high of 1.2540.

An alternative scenario is a downward penetration of the trading range. The next key level to have in mind is the 1.2160 lower band of the range, below the uptrend line. Further losses could shift the medium-term bullish bias to bearish and push the pair until the 1.2080 obstacle. A drop below this region could open the way towards the 1.1900 handle

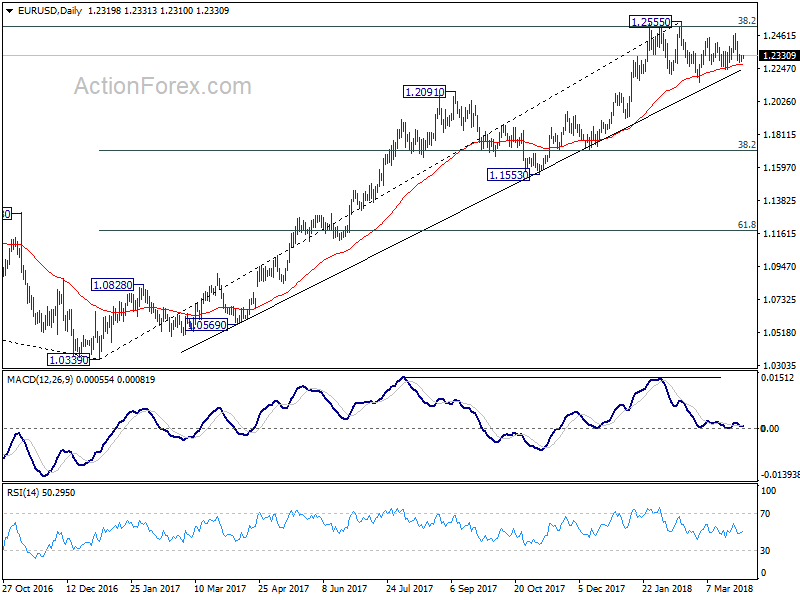

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2290; (P) 1.2310 (R1) 1.2337; More....

At this point, EUR/USD is still holding above 1.2285 minor support and intraday bias remains neutral. On the upside, above 1.2475 will target a test on 1.2555 high, which is close to 1.2516 key long term fibonacci level. We'd be cautious on reversal from there. But decisive break will carry larger bullish implications. On the downside, below 1.2285 minor support will turn bias to the downside for 1.2154 and below to extend the decline from 1.2555.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

Forex Markets Stay Quiet on Holiday Mood. RBA, ISM and NFP ahead

The forex markets are rather quiet today as most countries are still on holiday. Yen is trading generally lower but loss is limited so far. Japan Tankan survey posted some disappointing data but was shrugged off. Australian Dollar is also a touch weaker. Mixed data from China and the expectation of RBA standing pat and maintaining neutral stance is not providing much inspiration to Aussie. China formally started the refrained tariffs on 128 US products. While trading is subdued, there are a lot to look forward today during the week.

Technically, a key point to now is that EUR/USD, despite last week's decline, is holding on to 1.2285 minor support. Thus, there is no confirmation of near term bearish reversal yet. GBP/USD is also holding above 1.3982 minor support. These two levels will be closely watched ahead.

Japan Tankan shows slight deterioration in large manufacturer sentiment

There were slight deterioration in large manufacturing index from 26 to 24 and missed expectation of 25, and large manufacturers outlook from 21 to 20, missing expectation of 22. Large non-manufacturing index dropped to 23, down from 25 and missed expectation of 24. Large non-manufacturing outlook was unchanged at 20, below consensus of 21. Over business confidence were firm though. The fall in confidence and outlook is likely more due to Yen's recent appreciation. And so far, the fear of a global trade war had limit impact on sentiments. The indices were calculated, like many other similar series in the world, by subtracting the number of respondents saying conditions are poor from those responding conditions are good.

Also released from Japan, PMI manufacturing was finalized at 53.1 in March, revised down from 53.2.

China starts tariffs on 128 US products, in response to 232 steel tariffs

China formally starts the tariffs on 7 types, 128 products from the US today, according to a statement (link in simplified Chinese) by the Ministry of Finance. This is part of the packaged announced last month which targets up to USD 3b in imports. And it's a counter measure to the 232 steel and aluminum tariffs of the US that's non-geo-targeted.

China's response is seen by many as symbolic so far, and refrained. And the impact should be negligible comparing to the size of the bilateral trading relationship between the countries. Also, it's reported that the US is already in negotiation with China regarding a trade deal. However, for now, China is still holding the cards regarding the Section 301 tariffs, which are targeted on Chinese goods that adds up to USD 50-60b of value.

Talking about the Section 301 tariffs, Trump administration is expected to announce the list of products to be affected. It's believed that the list will concentrate on those affected by intellectual property theft only. And a major portion would be cutting-edge technology products.

China Caixin PMI manufacturing showed "marginal weakening" in March

China Caixin PMI manufacturing dropped to 51.0 in March, down from 51.6 and missed expectation of 51.7. That's also the lowest level in four months. Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group noted in the release that "manufacturing PMI reading in March showed that demand was not as strong as expected, leading to lower willingness of manufacturers to produce and restock."

However, "the ability of manufacturers to make a profit was beefed up by the stable increase in new orders and the much slower jump in input costs." Zhong also noted that "the growth momentum of the Chinese manufacturing economy may have weakened in March, but at a marginal pace."

Released over the weekend, however, the official China PMI manufacturing rose to 51.5, up from 50.3. Official PMI manufacturing rose to 54.6, up from 54.4.

RBA to stand pat, AUD to stay weak

RBA is widely expected to keep the cash rate unchanged at 1.50% tomorrow. Economists have been pushing back their expectation on the timing of an RBA hike after recent sluggish wage growth and inflation data. Late last year, there were speculations that RBA could hike twice by the end of this year. And now, markets are only pricing in around 40% chance of one hike in 2018. The majority expects that tightening won't start until 2019.

While the job markets have been strong in Australia, wage growth remained sluggish. Unemployment rate has now stabilized at 5.5-5.6% after last year's growth. However,the figure is floored by continue rise in participation rate. In that sense, the unemployment rate would stays away from hitting 5% level for a while, the level considered to be at full employment. That is, slack will remain in the economy.

RBA rate speculations, falling iron ore price and worries regarding US-China trade war left Aussie as one of the weakest back in March, in particular against Euro and Sterling. Aussie will likely stay pressured after tomorrow's RBA rate statement.

Looking ahead

ISM manufacturing will be the main focus today. And indeed, US data will be closely watched too, including ISM services, trade balance and non-farm payrolls. Other than that, UK will release PMIs while Eurozone will release CPI flash. Canada will release employment data and Ivey PMI too. It would also be a big week for Australian Dollar with RBA rate decision, retail sales and trade balance featured. But Aussie might react more to news regarding the trade tension between US and China.

- Monday: US ISM manufacturing, construction spending

- Tuesday: Japan monetary base; RBA rate decision; German retail sales; Swiss retial sales, manufacturing PMI; Eurozone manufacturing PMI final; UK manufacturing PMI

- Wednesday: Australia retail sales, building approvals; UK construction PMI; Eurozone CPI flash; US ADP employment, ISM services, factory orders

- Thursday: Australia trade balance; Swiss CPI; German factory orders, Eurozone services PMI final, PPI, retail sales; UK services PMI; US Challenger job cut, jobless claims, trade balance; Canada trade balance

- Friday: Japan household spending, average cash earnings, leading indicators; German industrial production; Eurozone retail PMI; Swiss foreign currency reserves; US non-farm payroll; Canada employment, Ivey PMI

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2290; (P) 1.2310 (R1) 1.2337; More....

At this point, EUR/USD is still holding above 1.2285 minor support and intraday bias remains neutral. On the upside, above 1.2475 will target a test on 1.2555 high, which is close to 1.2516 key long term fibonacci level. We'd be cautious on reversal from there. But decisive break will carry larger bullish implications. On the downside, below 1.2285 minor support will turn bias to the downside for 1.2154 and below to extend the decline from 1.2555.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q1 | 24 | 25 | 25 | 26 |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q1 | 20 | 22 | 19 | 21 |

| 23:50 | JPY | Tankan Large Non-Manufacturing Index Q1 | 23 | 24 | 23 | 25 |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q1 | 20 | 21 | 20 | |

| 23:50 | JPY | Tankan Small Manufacturing Index Q1 | 15 | 14 | 15 | |

| 23:50 | JPY | Tankan Small Manufacturing Outlook Q1 | 12 | 10 | 11 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Index Q1 | 10 | 8 | 9 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Outlook Q1 | 5 | 5 | 5 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q1 | 2.30% | 1.00% | 7.40% | 6.40% |

| 00:30 | JPY | PMI Manufacturing Mar F | 53.1 | 53.2 | 53.2 | |

| 01:00 | AUD | TD Securities Inflation M/M Mar | 0.10% | -0.10% | ||

| 01:45 | CNY | Caixin PMI Manufacturing Mar | 51 | 51.7 | 51.6 | |

| 13:30 | CAD | Manufacturing PMI Mar | 55.6 | |||

| 13:45 | USD | Manufacturing PMI Mar F | 55.7 | 55.7 | ||

| 14:00 | USD | Construction Spending M/M Feb | 0.40% | 0.00% | ||

| 14:00 | USD | ISM Manufacturing Mar | 60 | 60.8 | ||

| 14:00 | USD | ISM Prices Paid Mar | 72.5 | 74.2 | ||

| 14:00 | USD | ISM Employment Mar | 59.7 |

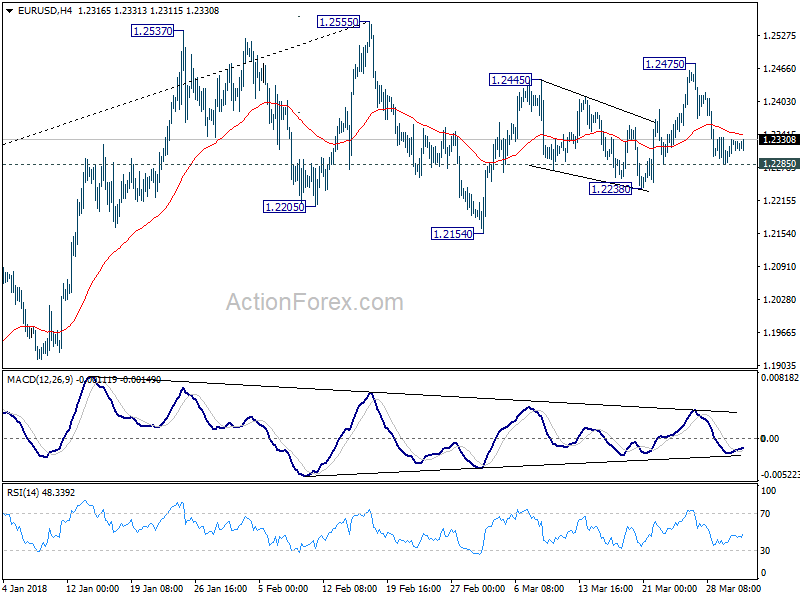

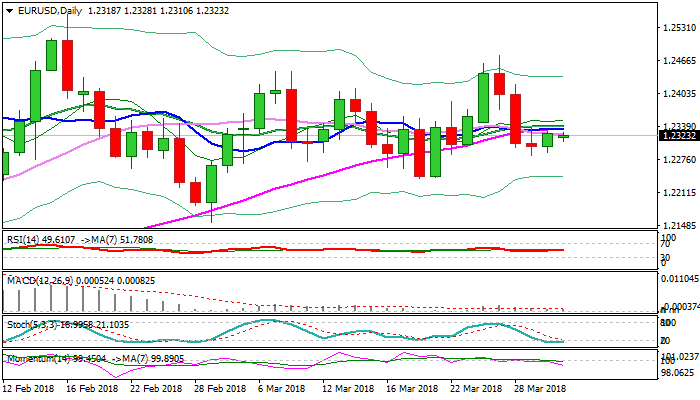

EURUSD Trades In Quiet Holiday Mode, Looks For Fresh Direction Signals

The Euro holds in tight range in holiday-thinned market on Monday, remaining capped by sideways-moving 10SMA at 1.2330 (also Fibo 23.6% of 1.2476/1.2283 bear-leg). The pair ended last week in red Doji with long upper shadow, signaling indecision, but also existing bearish pressure, following rejection of last week's strong rally at 1.2476 and subsequent reversal which fully retraced gains. Daily techs remain bearishly aligned as plethora of converged MA's (10,20,30 in 1.2320/40 zone) continues to cap and 14-d momentum turned south and penetrated negative territory. On the other side, oversold slow stochastic is turning north and may generate bullish signal on reversal, which would ease immediate downside risk. The pair looks for a catalyst to establish in fresh direction, with bullish scenario requiring firm break above a cluster of MA's to expose next key n/t barriers at 1.2394/1.2402 (daily cloud top/Fibo 61.8% of 1.2476/1.2283 descend) and revive bullish bias on break. Negative scenario sees break of pivotal 1.2283/77 zone (29 Mar low / Fibo 61.8% 1.2154/1.2476, 01/27 Mar rally) as a trigger for fresh bearish acceleration towards 1.2240 higher base (20/21 Mar). The pair is likely to remain in quiet mode on Easter Monday, with focus on Tuesday's releases of German retail sales as well as Manufacturing PMI data from bloc's members.

Res: 1.2340, 1.2357, 1.2402, 1.2430

Sup: 1.2310, 1.2280, 1.2240, 1.2200

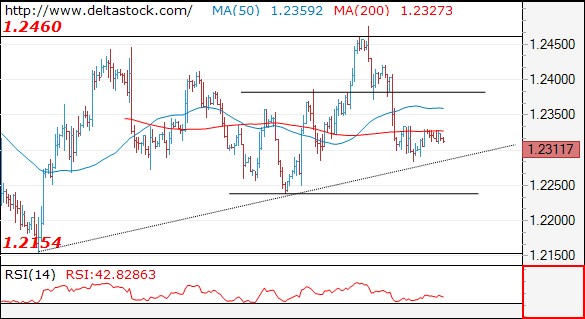

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2311

Thursday's test of 1.2280 dynamic support has failed and an intraday break through 1.2330 will challenge 1.2380 resistance area. The latter should reinstate the bearish bias, for a slide towards 1.2160.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2330 | 1.2560 | 1.2280 | 1.2160 |

| 1.2380 | 1.2560 | 1.2240 | 1.2090 |

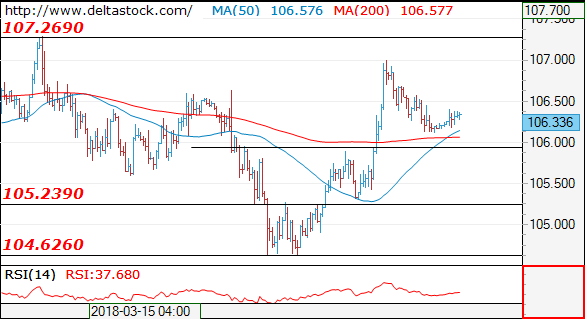

USD/JPY

USD/JPY

Current level - 106.33

The static support at 105.90 is intact and should provide a reliable bas for an upswing toward 107.30.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 107.00 | 108.30 | 105.90 | 105.20 |

| 107.90 | 110.40 | 105.20 | 104.60 |

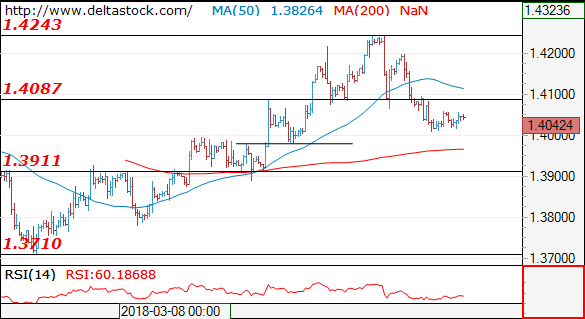

GBP/USD

Current level - 1..4042

The resistance at 1.4090 should cap the upside, for another leg downwards, to 1.3910 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4090 | 1.4280 | 1.3980 | 1.3710 |

| 1.4240 | 1.4340 | 1.3910 | 1.3620 |

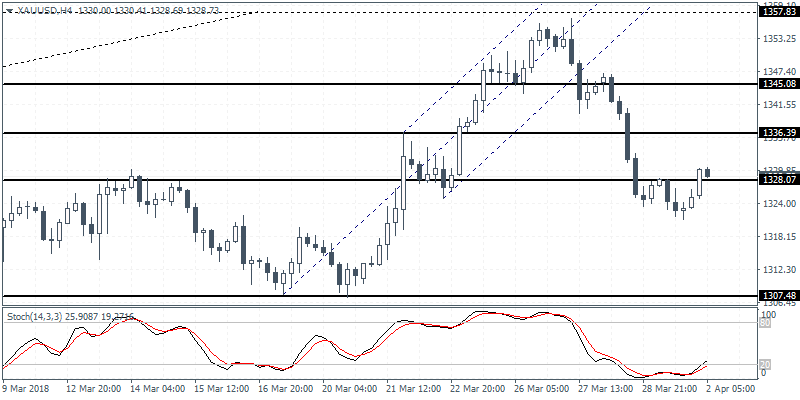

XAUUSD Intraday Analysis

XAUUSD (1328.07): Gold prices formed a doji pattern on Thursday following the previous two days of strong declines. The doji comes just below the 1328 level. A bullish close today could signal some near term correction in prices. Resistance at 1336 is seen which could come in as the first level of resistance and could keep gold prices caught within the range of 1336 and 1328 region. A breakout from either of these levels could determine the next leg of direction in the broader downtrend.