Sample Category Title

GBPUSD Intraday Analysis

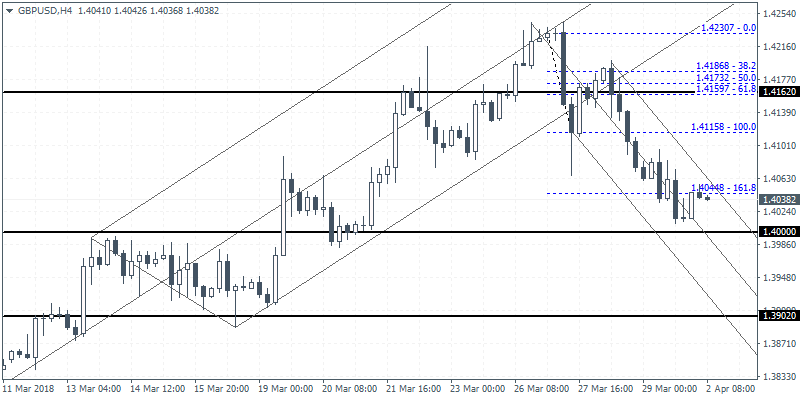

GBPUSD (1.4038): The British pound closed onFriday with strong declines, touching below the 161.8% measured move target of the bearish flag pattern formed on the 4-hour chart. The reversal which came just a few pips shy of the 1.40 round number support saw prices briefly retesting 1.4044 level. A follow through from here could signal a touchdown to the 1.40 handle. Only a close above 1.4044 will shift the bias to the upside, with the resistance at 1.4115.

EURUSD Intraday Analysis

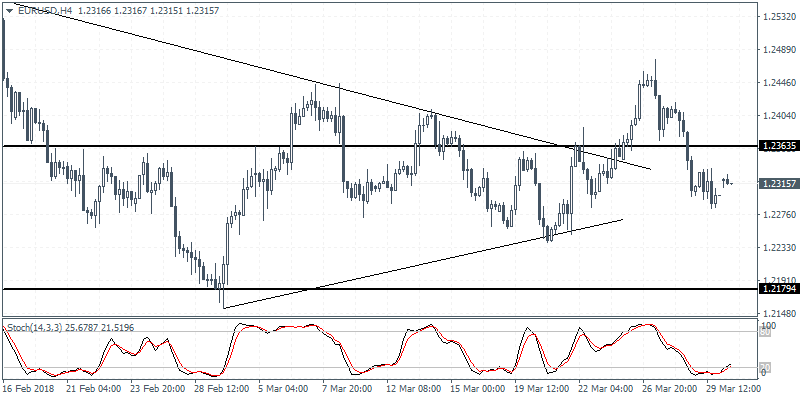

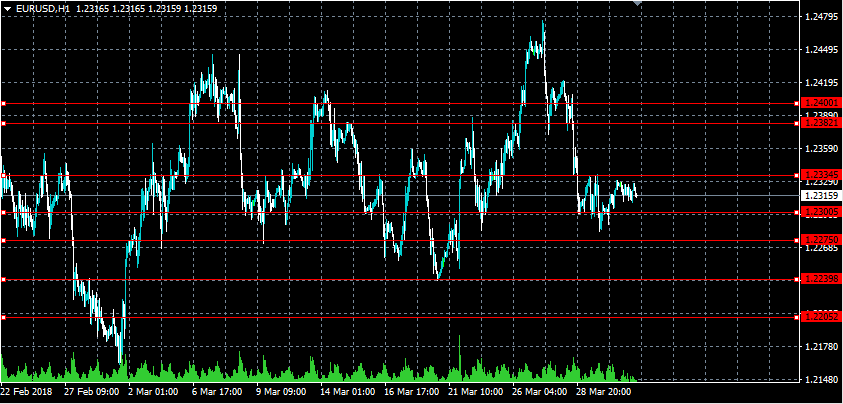

EURUSD (1.2315): The EURUSD closed on Thursday with a doji and price action is expected to see a possible reversal if the declines can stall around Thursday's close near 1.2300 region. On the four hour chart, we expect the near term to be biased to the upside. Resistance at 1.2363 is likely to be tested. However, in the event that price action continues to slip below Thursday's close, we could expect to see further declines pushing the EURUSD lower toward the 1.2180 handle.

China Hits Back With New Tariffs On U.S. Imports

The markets gapped higher this morning following a three day weekend. The U.S. dollar was seen closing flat on Thursday. Economic data was relatively sparse with the end of quarter flows driving prices.

News over the weekend included China imposing fresh tariffs on imports from the U.S. This is expected to hit the market sentiment especially during the NY trading session. Over the weekend, the BoJ's tankan surveys showed that business sentiment weakened in the first quarter of the year. This came amid higher revised readings for the fourth quarter of last year.

Looking ahead, the European markets are closed today on account of Easter Monday holiday. The economic calendar is relatively quiet but gets busy during the NY trading session. Important economic data for the day includes the ISM's manufacturing PMI for March. Economists forecast that manufacturing activity slipped modestly to 60.1 from 60.8 in February.

Later in the day, the construction spending data for February is expected to show a 0.4% increase following a flat reading the month before.

RBA to stand pat, AUD to stay weak

RBA is widely expected to keep the cash rate unchanged at 1.50% tomorrow. Economists have been pushing back their expectation on the timing of an RBA hike after recent sluggish wage growth and inflation data. Late last year, there were speculations that RBA could hike twice by the end of this year. And now, markets are only pricing in around 40% chance of one hike in 2018. The majority expects that tightening won't start until 2019.

While the job markets have been strong in Australia, wage growth remained sluggish. Unemployment rate has now stabilized at 5.5-5.6% after last year's growth. However,the figure is floored by continue rise in participation rate. In that sense, the unemployment rate would stays away from hitting 5% level for a while, the level considered to be at full employment. That is, slack will remain in the economy.

RBA rate speculations, falling iron ore price and worries regarding US-China trade war left Aussie as one of the weakest back in March, in particular against Euro and Sterling. AUD will likely stay pressured after tomorrow's RBA rate statement.

EURUSD Still Bearish Below 1.2382 Level

The euro remains under selling pressure against the U.S dollar, as the new month of April gets underway, amidst slow Bank holiday trading conditions. The economic calendar remains busy for the EURUSD, with the U.S Manufacturing, eurozone CPI and Retail sales data, whilst the U.S Nonfarm Payrolls jobs report may provide a much-needed directional catalyst for the pair. Moving into the U.S session, the 1.2275 level is key downside support, whilst the 1.2382 level remains key technical resistance.

The EURUSD pair retains a short-term bearish bias whilst trading below the 1.2382 level, further declines towards 1.2239 and 1.2205 remain possible.

Should the EURUSD pair move above the 1.2382 level, further upside towards 1.2430 and 1.2475 seems likely.

GBPUSD Key Support At 1.3960 Level

The British pound starts the month of April with a slightly negative bias against the U.S dollar, after suffering heavy losses towards the end of last week. The GBPUSD pair needs to move price-action above the 1.4200 level to regain bullish momentum, negating last week’s bearish outside reversal candle. Sterling traders now look towards the release of the March Manufacturing PMI and ISM Manufacturing readings from the U.S economy.

The GBPUSD pair retain a short-term bearish bias whilst price-action trades below the 1.4087 level. Key support I found at the 1.3960 and 1.3890 levels.

If the GBPUSD pair moves above the 1.4087 level, key intraday resistance is found at the 1.4145 and 1.4200 levels.

PMI Data Headline Easter Monday

A steady stream of PMI data will make its way through the financial markets on Monday, although trading activity is expected to be muted as Australian and key European markets pause for the Easter holiday. The purchasing managers’ index (PMI) provides a high-level overview of domestic economies, focusing on manufacturing and services sectors.

Action begins at 13:30 GMT with a report on Canadian manufacturing PMI. The March reading is expected to show 55.7, on a scale of 1-100 where 50 separates expansion from contraction.

Investors are also bracing for a pair of US manufacturing PMI reports courtesy of IHS Markit and the Institute for Supply Management (ISM). The reports, released 15 minutes apart, are expected to show steady expansion in US manufacturing activity. The ISM report, which is more closely monitored by investors, is expected to come in at 60 in March compared with 60.8 the month before.

The US government will report on construction spending at 14:00 GMT. The monthly report is expected to show growth 0.6% for February following no change the previous month.

On the monetary policy front, Federal Open Market Committee (FOMC) member Neel Kashkari is scheduled to deliver a speech at 22:00 GMT. The Fed raised interest rates last month for the first time since December and is planning to gradually normalize monetary policy over the next two years.

Market participants can expect a more active release schedule later in the week, including high-profile jobs data from the United States. Friday’s nonfarm payrolls report is forecast to show a monthly gain of 198,000 jobs in March. Nonfarm payrolls surged by 313,000 the month before.

EUR/USD

Europe’s common currency lost momentum last week, with the EUR/USD plunging from a high of 1.2470 to a low of 1.2291. The pair regained the 1.2300 handle last week and was last seen trading at 1.2314. The common currency faces immediate support at 1.2240, followed by the 1.2200 handle. On the opposite side of the spectrum, key resistance is located at 1.2340, followed by 1.2400.

GBP/USD

Cable is coming off a turbulent week, with prices falling more than 200 pips. GBP/USD was last seen trading at 1.4030, where it was little changed compared with Friday’s close. Immediate support levels are located at 1.4010, 1.3985 and 1.3940. On the opposite side of the spectrum, the pair is likely to face resistance at 1.4040, 1.4085 and 1.4125.

USD/CAD

The USD/CAD fell sharply in the latter half of March, as the loonie gathered strength on positive NAFTA speculation. The USD/CAD was last seen trading below 1.2900, which is roughly in line with its pre-holiday range. The pair is currently testing the 1.2885 resistance level, with key support located at 1.2800.

Attention Turns Back To Data This Week

Asian equities kicked off Q2 on a positive note, taking their cue from Wall Street's rally on Thursday. The gains came despite China imposing retaliatory tariffs on U.S. imports and Manufacturing PMI data falling short of economists' forecasts.

So far China's response has only been on the aluminum and steel tariffs, announced by the White House last month, and not on the proposed $60 billion in annual tariffs against Chinese products. This shows Beijing is unwilling to enter a trade war with the U.S., knowing that it has more to lose than to win. However, trade dispute will continue to dominate investors' decisions heading into Q2.

Many traders remain away from their desks on Monday to spend time with their friends and family, so barring an unexpected announcement from the White House, expect markets to stay calm.

Macro data will be back in focus

Manufacturing and Service PMIs from Europe, UK, and the U.S. will be closely scrutinized by investors this week. In March, the euro area private sector expanded at its weakest pace since 2017, raising questions on whether the robust economic performance in the Eurozone during 2017 has come close to an end. Another slip in these leading indicators may well reinforce the belief that the global synchronized growth is losing momentum. This will also justify the underperformance in European equities, where the DAX, CAC and IBEX fell 6.35%, 2.73% and 4.4% YTD respectively.

Eurozone inflation

Euro traders will have to give a special attention to the Eurozone preliminary CPI release for March on Wednesday. In February the harmonized inflation came at 1.1%, a 0.2% fall from January's reading and slipping further away from European Central Bank's target of just under 2%. Another disappointment on this front will raise the voices within the ECB members, advising against tightening monetary policy which is likely to add further pressure on the EURUSD after falling by more than 1.3% from last week's highs.

U.S. NFP, the main event of the week

Friday's U.S. nonfarm payrolls release is undoubtedly the key event of the week. The U.S. is expected to have added 198,000 jobs in March versus 313,000 in February. Meanwhile, unemployment is expected to drop by 0.1% to 4%, the level last seen 18 years ago. However, wage growth remains to be the key market moving piece, after showing an unexpected fall from 2.8% to 2.6% last month. Given that one of the main arguments in markets today is whether the Fed will raise rates by another 2 or 3 times in 2018, this figure will play an important role in pricing interest rates expectations, and thus the dollar's direction.

China Launches Counter Tariffs On 128 US Products

General Trend:

- Trading remains light amid the last day of Easter holiday

- Major currencies little changed, while Korean Won makes multi-year high

- S&P futures slightly lower ahead of US open after long holiday weekend

- China official PMI and Caixin both remain in expansion

- Japan Q1 Tankan survey shows first decline in 2 years

Headlines/Economic Data

Japan

- Nikkei 225 opened -0.1%; closed -0.3%

- (JP) JAPAN Q1 TANKAN LARGE ALL INDUSTRY MANUFACTURING INDEX: 24 V 25E; LARGE MANUFACTURING OUTLOOK: 20 V 22E; LARGE ALL INDUSTRY CAPEX 2.3% V 1.0%E

- Toshiba, 6502.JP Sale of Westinghouse claims delayed; In process of reviewing FY17/18 forecast

- (JP) Japan Mar Final PMI Manufacturing: 53.1 v 53.2 prelim

Korea

- Kospi opened +0.4%

- (KR) US and South Korea start scaled down annual military drills, no response from North Korea

- (KR) South Korea Mar Trade Balance: $6.9B v $5.8Be

- POSCO, 005490.KR On its 50-yr anniversary will look to reduce the amount of profit from from steel by half and look to replace it with profit from biopharma and lithium - Korean press

- (KR) South Korea Mar PMI Manufacturing: 49.1 v 50.3 prior

- (KR) Bank of Korea (BOK) Gov Lee: FX rate is determined by markets; hard to make big rate hikes when potential growth is low

- (KR) Bank of Korea (BoK) sells KRW540B in 6-month monetary stabilization bonds (MSBs): yield 1.73% v 1.68% prior

- (KR) North Korea leader Kim Jong Un enjoyed concert with wife and hundreds of citizens by South Korean pop stars visiting Pyongyang

China/Hong Kong

- Hang Seng closed for holiday; Shanghai Composite opened flat

- (HK) Macau Mar Gaming Rev MOP25.9B, y/y: 22.2% v 16.6%e

- (CN) CHINA MAR GOVT OFFICIAL MANUFACTURING PMI: 51.5 V 50.7E; Non-manufacturing PMI: 54.6 v 54.5e; Composite PMI: 54.0 v 52.9 prior

- (CN) China Mar Caixin PMI Manufacturing: 51.0 v 51.7e

- (CN) China imposing new tariffs on 128 US products including meat and fruit in response to US tariffs on steel and aluminum, effective today; 25% tariff on pork and new 15% tariff on 120 other products including fruit - press

- (CN) China MOFCOM: Trade dispute should be resolved through dialogue; hope US withdraws measures that violate WTO rules

- (CN) China Securities Regulatory Commission (CSRC): Announces pilot plan to encourage qualified companies in select industries to float shares on its domestic stock market, in order for tech giants to list at home

- (CN) China PBoC Open Market Operation (OMO): Skips OMO (7th straight session) v skipped prior; Net: CNY20B drain v CNY30B drain prior

- (CN) China PBoC sets yuan reference rate at 6.2764 v 6.2881 prior

- (CN) China politician Yang Jiechi’s two-day trip to South Korea is a sign that the Communist Party aims to take a bigger role in diplomacy – SCMP

- (CN) China Foreign Min Wang Yi: China will import $8T of goods and attract $600B of foreign investment in the next five years

- (CN) China Protection and Coordination Department at the State Intellectual Property Office Dir Zhicheng: Issues new guidelines tightly reviewing the transfer of intellectual property rights to overseas buyers with the aim to build a more fair and transparent regulation process for technology exports and foreign investment

Australia/New Zealand

- ASX 200 closed for holiday

- (AU) Australia Mar Melbourne Institute Inflation m/m: +0.1% v -0.1% prior; y/y: 2.1% v 2.1% prior

- Looking ahead: RBA meets tomorrow to decided on cash target rate, widely expected to be left unchanged

Other Asia

- (SG) Singapore Q1 URA Property Index q/q: 3.1% v 0.8% prior

- (TW) Taiwan Central Bank Gov rejects media reports of a rate hike plan; Market is over interpreting that the central bank will raise rates in order to let TWD appreciate

- North America

- Hudson’s Bay, HBC.CA Reports data breach involving in store customer payment card data at certain Saks Fifth Avenue, Saks OFF 5TH, and Lord & Taylor stores in North America

- President Trump: Mexico is doing very little, if not NOTHING, at stopping people from flowing into Mexico through their Southern Border, and then into the U.S. They laugh at our dumb immigration laws. They must stop the big drug and people flows, or I will stop their cash cow, NAFTA. NEED WALL! – tweet

Europe

- (EU) Japan indicates that a trade deal with the EU is a greater priority than one with the UK - press

Levels as of 02:00ET

- Shanghai Composite +0.1%; Kospi -0.0%

- Equity Futures: S&P500 -0.2%; Nasdaq100 -0.5%

- EUR 1.2330-1.2311; JPY 106.41-106.19; AUD 0.7697-0.7672;NZD 0.7239-0.7225

- Apr Gold +0.5% at $1,329/oz; May Crude Oil +0.4% at $65.17/brl; May Copper +0.8% at $3.05/lb

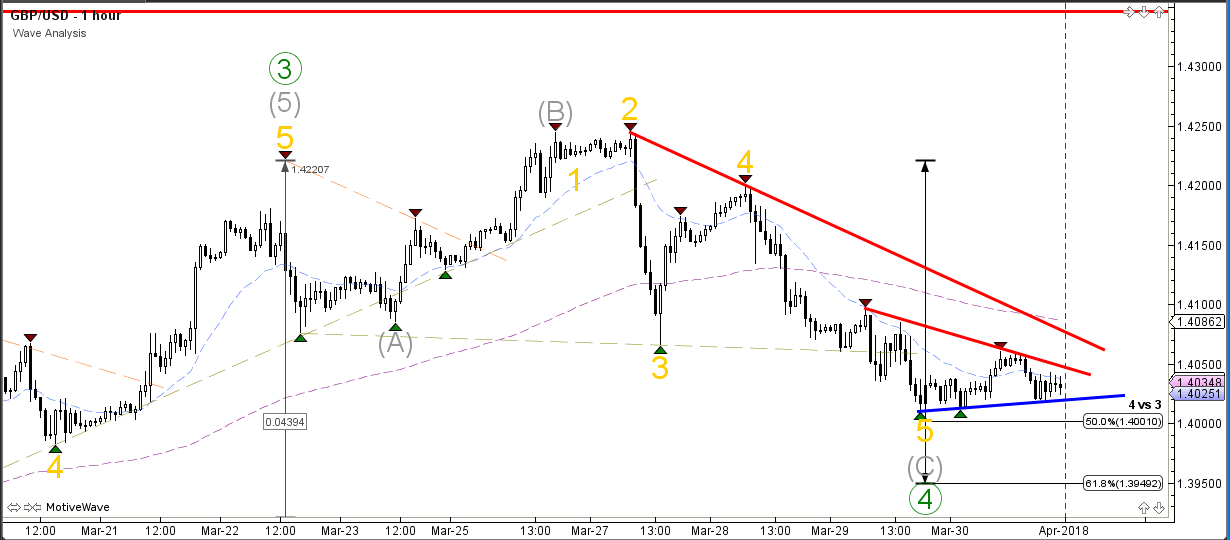

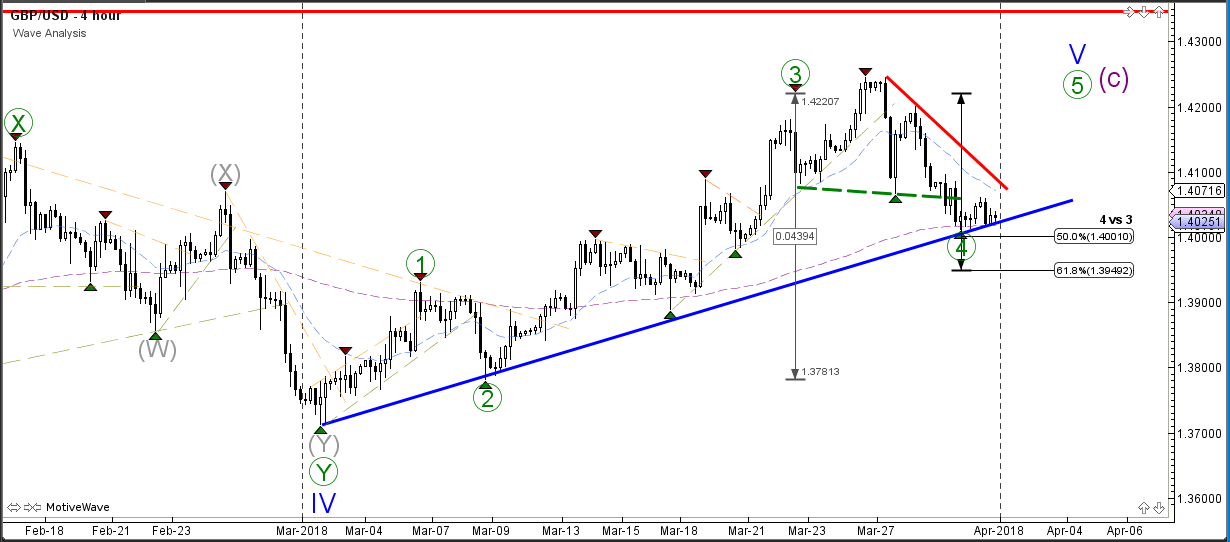

GBP/USD Bearish Retracement Retests Key 1.40 Support Zone

Currency pair GBP/USD

The GBP/USD istesting the Fibonacci levels of the potential wave 4 (green) retracement. Price is a key support zone due to the 50% Fib, 1.40 round level, long-term moving average, and support trend line (blue). A bullish bounce could see price move up within the trend whereas a bearish break could indicate a reversal.

The GBP/USD might have completed a wave C (grey) of a wave 4 (green) retracementif price manages to break above the resistance trend lines (red). A break below the 50 and 61.8% Fibonacci level makes a wave 4 (green) less likely.