Sample Category Title

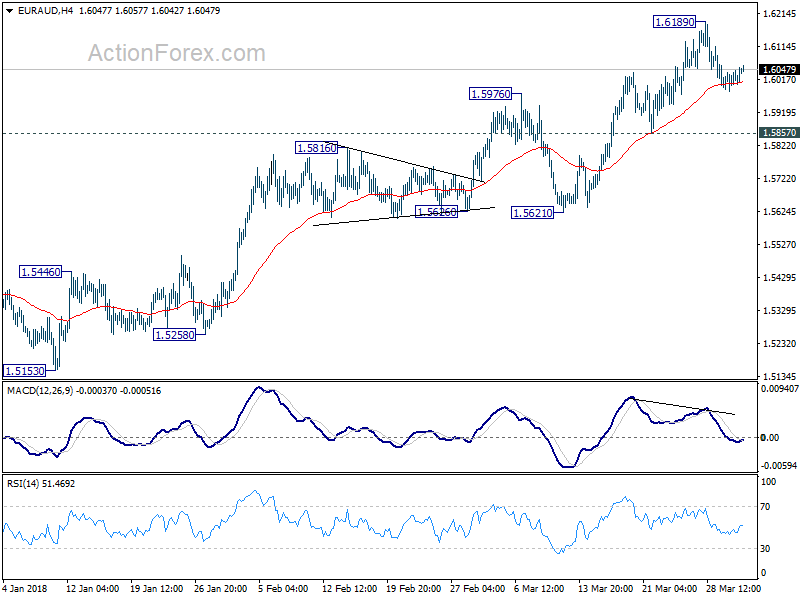

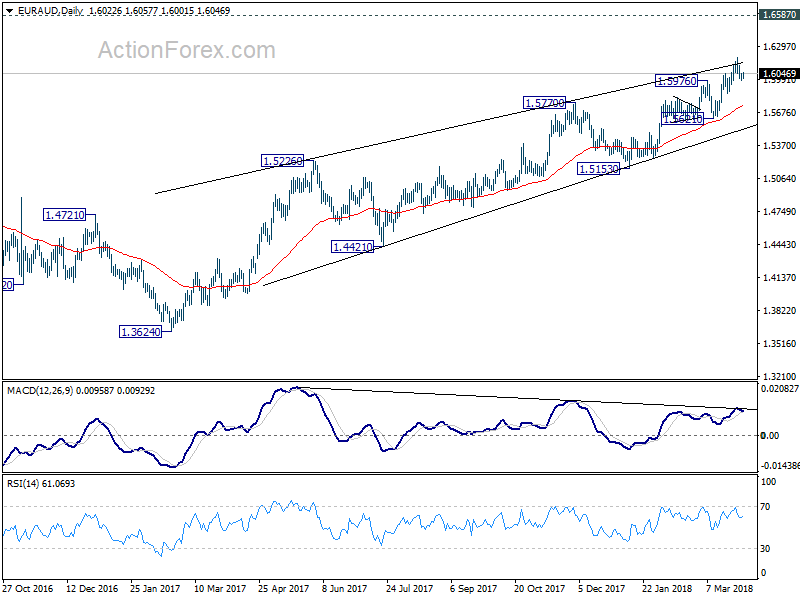

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5996; (P) 1.6018; (R1) 1.6054; More....

EUR/AUD is staying in consolidation below 1.6189 temporary top. Intraday bias remains neutral at this point. Further rally is expected as long as 1.5857 minor support holds. On the upside, break of 1.6189 will resume the whole rally from 1.5153 and target 1.6587 key resistance. Nonetheless, break of 1.5857 will be an early sign of trend reversal and turn bias to the downside for 1.5621 support to confirm.

In the bigger picture, current development suggests that rise from 1.3624 is not completed yet. And it's still in progress for 1.6587 key resistance level. We'd be cautious on strong resistance from there to limit upside, on bearish divergence condition in daily MACD. But for now, break of 1.5621 support is needed to be the first sign of medium term reversal. Otherwise, outlook will stays bullish even in case of deep pull back.

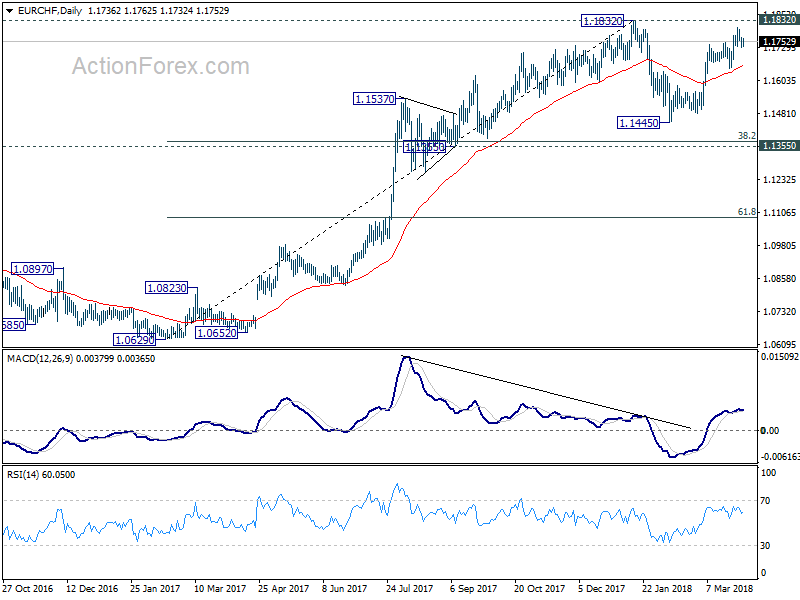

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1727; (P) 1.1746; (R1) 1.1764; More...

EUR/CHF lost momentum after hitting 1.1802 and formed a temporary top ahead of 1.1832 resistance. Intraday bias is turned neutral first. ON the downside, break of 1.1649 support will indicate completion of rebound form 1.1445. And the corrective pattern from 1.1832 would then extend with another decline to retest 1.1445. In case of another rise, we'd stay cautious on strong resistance from 1.1832. However, firm break of 1.1832 will confirm resumption of larger up trend.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

China And U.S Tit-For-Tat Tariffs Start

Monday April 2: Five things the markets are talking about

Trading remains light, with major currencies little changed, amid the last day of the Easter holidays.

Note: There is a bank holiday in most of Europe today (Sw., Ger., Fr., It. and the U.K).

This shortened trading week features inflation and unemployment figures in Europe, the March U.S and Canadian jobs report, and an interest-rate decision down-under.

On Tuesday (Apr. 3), the Reserve Bank of Australia (RBA) will release its policy statement. The inflation outlook, weak wage growth and consumer-spending risks give the RBA reason enough to stand pat.

Data last week showed that the eurozone's annual rate of inflation fell for a third consecutive month in February, reinforcing the ECB's sense of caution as it considers further steps to wind down its QE programs.

Nonetheless, this Wednesday (Apr. 4), relief may be at hand, with ‘flash' CPI forecasting from Eurostat are expected to record a pickup to +1.4% in March, from +1.1%. Other separate data is expected to show a further decline in E.U unemployment for February – this may strengthen the ECB's conviction that inflation will reach its target of just below +2% next year.

On Friday (Apr. 6), both the U.S and Canada will release jobs data for March. Both economies recorded robust growth in February, and given the recently low number of layoffs stateside, analysts are expecting the unemployment rate to drop to a near two-decade low of +4%.

1. Stocks in choppy waters

In Japan overnight, equities edged lower in choppy trading, with volume falling to the lowest in more than three-months, with real estate and banks again underperforming. The Nikkei ended -0.3% lower, while the broader Topix dropped -0.4%.

Down-under, the ASX 200 was closed for the holidays, while S. Korea's Kospi gained +0.8%.

Note: The Reserve Bank of Australia (RBA) meets tomorrow to decide on cash target rate – market expectations are for unchanged.

In Hong Kong, the Hang Seng was closed for the holidays.

In China, stocks kicked off Q2 with mild losses overnight, amid lingering worries of a full-blown trade war between the U.S and China. At the close, the Shanghai Composite index was down -0.2%, while the blue-chip CSI300 index was down -0.3%.

In Europe, most of the major bourses are closed for Easter Monday.

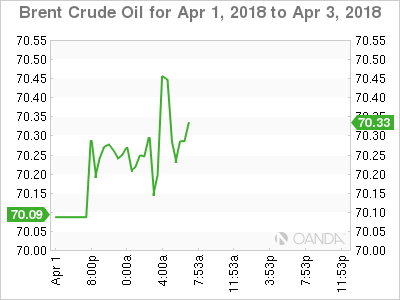

2. Oil is higher on lower U.S drilling, Iran sanctions concern

Oil rose towards +$70 a barrel, lifted by a drop in drilling activity in the U.S and concerns that Washington could reintroduce sanctions against Iran.

Brent crude futures have rallied +58c to +$69.92 a barrel. It still below this year's high of +$71.28 reached on Jan. 25, while U.S crude (WTI) added +38c to +$65.32.

Note: Trading volumes are lower than normal as many countries are still on Easter holiday.

Baker Hughes data last week showed that U.S drillers cut -7 oilrigs in the week to March 29, bringing the total down to +797, the first decline in three-weeks

However, the Iranian factor could have a significant impact on the market for the next month. President Trump has threatened to pull out of a 2015 international nuclear deal with Tehran under which Iranian oil exports have risen. He has given the European signatories a May 12 deadline to “fix the terrible flaws” of the deal.

Possibly capping prices could be the U.S/China trade war getting out of hand. Any increase in trade friction is likely to rock global markets and tarnish any bullish sentiment in crude prices.

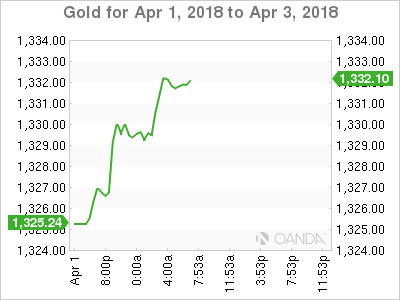

Ahead of the U.S open, gold prices have rallied as the ‘big' dollar eased a tad amid renewed concerns over a trade war after China imposed additional tariffs on U.S products (see below) in response to the U.S duties on imports of aluminum and steel. After falling in the past three-trading sessions, spot gold edged up +0.5% to +$1,331.19 per ounce.

3. Sovereign yields little changed

Narrow ranges across Bunds and most Euro and U.S spreads amid lower volumes, despite the U.S ‘s record supply last week, would suggest that the fixed income market remains in holiday mode.

Note: In total and by week's end, the U.S Treasury auctioned +$294B of bills and notes, its largest slate of supply ever.

From Thursday's close, the yield on 10-year U.S Treasuries have dipped -1 bps to +2.78%, the lowest in more than seven-weeks. While in the U.K, the 10-year Gilt yield has advanced +1 bps to +1.366%, the biggest gain in more than a week, while in Germany, the 10-year Bund yield increased + 1bps to +0.51%, the first advance in more than a week.

In Japan overnight, the key 10-year JGB futures contract touched a two-week low, weighed down by fixed income dealers selling ahead of a 10-year JGB auction on Tuesday.

4. Trade war looms for the dollar

FX markets are quiet as Europe continued with its extended Easter holiday, but investors and traders remain wary over global trade tensions.

On Sunday, China announced that it had increased tariffs by up to +25% on 128 U.S products including frozen pork, wine and certain fruits and nuts in response to U.S duties on imports of aluminum and steel last week. The tariffs are to take effect today.

On the other side, the Trump administration is expected this week to unveil the list of Chinese imports targeted for U.S tariffs to punish Beijing over technology transfer policies. The list of +$50B+ worth of annual imports is expected to target largely high technology. However, unlike China, the tariffs could take more than two-months before going into effect.

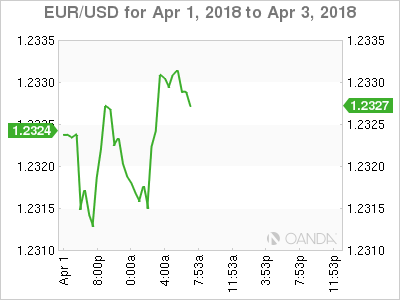

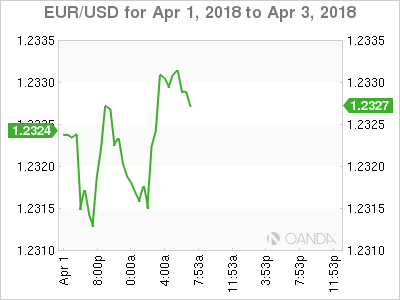

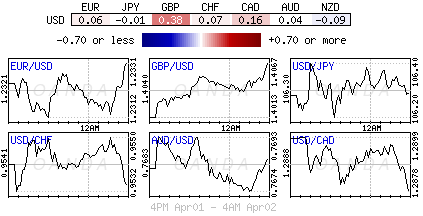

The EUR remains in the middle of this years trading range, trading atop of the psychological €1.23 handle at €1.2329. USD/JPY is little changed at ¥106.30, while the pound (£1.4069) came under pressure from quarter-end selling, and remains somewhat unmoved by last Thursday's U.K GDP data (unchanged at +0.4% q/q).

5. BoJ Tankan survey shows softer sentiment

A BoJ's survey showed that confidence among Japan's large manufacturers weakened for the first time in two-years in Q1 as they grew cautious about their business outlook amid the yen's appreciation, stock falls and the latest U.S trade measures.

The main index measuring large manufacturers' sentiment was at +24 in the three-month period, compared with plus +25 in Q4/2017.

Digging deeper, the BoJ's Tankan corporate survey shows price pressures are also rising. It suggests that consumer price inflation will rise to around +1.5% over the coming months.

Note: In February, core-inflation rose +1% for the first time in three and a half years.

The result comes at the end of a quarter in which the yen gained +6% outright, Japanese stocks fell -5.8% and the U.S slapped tariffs on steel and aluminum without giving Tokyo an exemption offered to other close allies. The survey also showed that big manufacturers see profits falling -3.2% in the year ending March 2019.

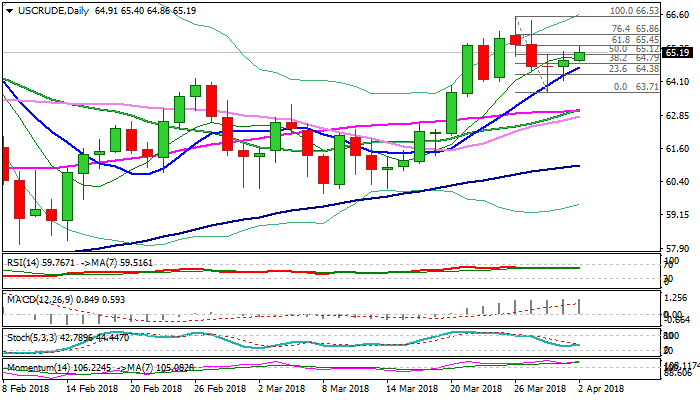

WTI Oil Extended Recovery Pressures Pivotal Fibo Barrier At $65.45

WTI oil maintains positive tone on Monday and extends recovery from last week’s correction low at $63.71.

Oil price regained momentum after pullback from $66.53 peak stalled on attempts through important Fibo support at $64.08 and subsequent bounce extended to $65.40 on Monday, retracing nearly 61.8% of $66.53/$63.71 pullback.

Concerns about reintroducing US sanctions against Iran and drop in drilling activity in the US (last Thursday’s release of Baker Hughes report showed a number of oil rigs dropped to 798 from 804), keep near-term action supported.

last week’s correction and continues to track fresh advance, offering initial supports at $64.82 (cloud top) and $64.62 (10SMA).

Recovery rally needs close above $65.45 (Fibo 61.8% of $66.53/$63.71 pullback) to generate fresh bullish signal and expose key barriers at $66.64/53 (25 Jan / 26 Mar peaks) and $66.75 (50% retracement of 107.45/$26.04 fall).

Near-term structure would weaken on break below rising 10SMA, while stronger bearish signal could be expected on close below $64.08 (Fibo 38.2% of $60.11/$66.53 rally).

Res: 65.45, 65.86, 66.00, 66.53

Sup: 64.82, 64.62, 64.08, 63.71

Muted Easter Trading With Bulk Of Europe Closed

Notes/Observations

- Soybeans sow seeds of discontent in US and China's trade war

- Japan Q1 Tankan Survey showed that non-manufacturing business mood soured for first time in two years (Non-Manufacturing Index: 23 v 24e)

- Muted Easter trading with bulk of Europe closed (HK, Australia and New Zealand were also closed)

Asia:

- China imposing new tariffs on 128 US products amounting to $3B including meat and fruit in response to US tariffs on steel and aluminum, effective Apr 1st (Note: A bigger dispute looms over Trump's approval of possible higher duties on nearly $50 billion of Chinese goods)

- Commerce Ministry reiterated trade talks with US needed to happen in order to prevent greater damage to relationship

- China Mar Manufacturing PMI (Govt official) 51.5 v 50.7e reinforcing views that China got off to a surprisingly strong start to the year.

- China Mar Caixin PMI Manufacturing: 51.0 v 51.7e (lowest reading since Nov)

- Japan Mar Final PMI Manufacturing: 53.1 v 53.2 prelim

- Japan Q1 Tankan Survey: Large Manufacturing Index: 24 v 25e; Large Manufacturing Outlook: 20 v 22e. Large Non-Manufacturing Index: 23 v 24e (1st decline in six quarters)

- US and South Korea start scaled down annual military drills after month-long delay, no response from North Korea

- Japan Feb Jobless Rate beat expectations but still registered its 1st rise in 9 months (2.5% v 2.6%e)> Jan reading was 2.4%

Europe:

- 9 members of Tory party said to back amendments to the legislation needed for Britain to leave the EU - including a parliamentary vote on staying in a customs union

- Germany Fin Min Scholz said to seek provision to cushion the burden on the federal budget with the aspect of sharply rising interest rates. If the average rate of interest on federal debt only rose by one percentage point, it would also have to raise more than ten billion euros in debt service.

Americas:

- President Trump recent tweets stated that NO MORE DACA DEAL - Border Patrol Agents are not allowed to properly do their job at the Border because of ridiculous liberal (Democrat) laws like Catch & Release

Economic Data:

- (RU) Russia Mar Manufacturing PMI: 50.6 v 51.0e (20th month of expansion)

- (TR) Turkey Mar Manufacturing PMI: 51.8 v 55.6 prior (13th month of expansion)

- (TH) Thailand Mar Business Sentiment Index: 53.3 v 51.4 prior

- (GR) Greece Mar Manufacturing PMI: 55.0 v 56.1 prior (10th month of expansion)

Fixed Income Issuance:

- None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Close for Easter Monday holiday

- Market Focal Points/Key Themes:

Speakers

- Trump Administration said to unveil the list of Chinese imports targeted for tariffs during the week of Apr 1st. Expected to target high technology products but could take more than two months before going into effect

Currencies

- FX markets were very quiet as Europe continued with its extended Easter holiday but traders were wary over global trade tensions.

- EUR/USD remained in the middle of its 2018 trading range just holding above the 1.23 area.

- USD/JPY was little changed at 106.30

Fixed Income

- Markets closed for holiday

Looking Ahead

- (RO) Romania Mar International Reserves: No est v $38.7B prior

- (RU) Russia Mar Sovereign Wealth Funds: Wellbeing Fund: No est v $66.4B prior

- (BR) Brazil Feb CNI Capacity Utilization: No est v 78.1% prior

- 07:25 (BR) Brazil Central Bank Weekly Economists Survey

- 07:30 (IN) India Jan Eight Infrastructure (Key) Industries: No est v 6.7% prior

- 08:30 (CA) Canada Feb MLI Leading Indicator M/M: No est v 0.4% prior

- 09:00 (BR) Brazil Mar Manufacturing PMI: No est v 53.2 prior

- 09:00 (SG) Singapore Mar Purchasing Managers Index (PMI): 52.8e v 52.7 prior

- 09:30 (CA) Canada Mar Manufacturing PMI: No est v 55.6 prior

- 09:45 (US) Mar Final Markit Manufacturing PMI: 55.7e v 55.7 prelim

- 10:00 (US) Mar ISM Manufacturing: 60.0e v 60.8 prior; Prices Paid: 72.5e v 74.2 prior

- 10:00 (US) Feb Construction Spending M/M: 0.4%e v 0.0% prior

- 10:00 (MX) Mexico Feb Total Remittances: $2.3Be v $2.2B prior

- 10:00 (MX) Mexico Central Bank (Banxico) Bank Economist Survey

- 10:30 (MX) Mexico Mar Manufacturing PMI: No est v 51.6 prior

- 11:30 (US) Treasury to sell 3-Month and 6-Month Bills

- 13:00 (MX) Mexico Mar IMEF Manufacturing Index: No est v 52.6 prior; IMEF Non-Manufacturing Index: No est v 53.4 prior

- 14:00 (BR) Brazil Mar Trade Balance: No est v $4.9B prior

- 16:00 (US) Weekly Crop Progress Report

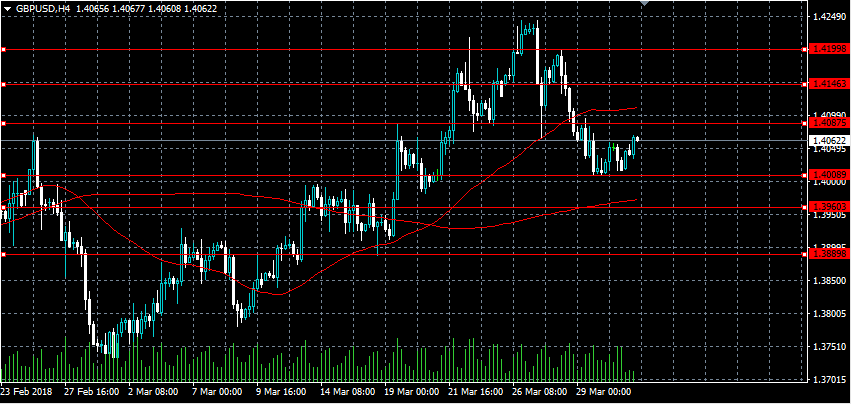

GBPUSD Moving Towards Key Resistance Level

The British pound has moved higher against the U.S dollar during a slow Easter Monday trading session, with price-action now edging towards the key 1.4087 resistance level. The GBPUSD pair has regained short-term bullish momentum, after sellers failed to move price below the psychological 1.4000 level. Moving into the U.S session, sterling traders look towards key March Manufacturing data from the United States economy and scheduled speech from FOMC member Kashkari.

The GBPUSD pair will turn further bullish above the 1.4087 level. Key technical resistance is then found at the 1.4146 and 1.4199 levels.

Should the GBPUSD pair fail to move above the 1.4087 level, sellers may test towards the 1.4008 and 1.3960 levels.

USDJPY Bullish Bias Intact Above 106.00

The U.S dollar continues to trade in narrow-band against the Japanese yen currency, with the pair still retaining an intraday bullish bias while trading above the key 106.00 level. The USDJPY pair moved back towards the 106.40 region, as dip-buying demand remained prevalent from the 106.00 level. The key market moving event for the pair today is the ISM Manufacturing report, with market expectations tilted slightly to the downside.

The USDJPY pair retains a bullish intraday bias whilst price-action holds above the 106.00 level, key resistance is currently found at the 106.45 and 107.00 levels.

Should the USDJPY pair slip below the 106.00 support level for a sustained period, a further decline towards the 105.50 and 105.24 levels remains possible.

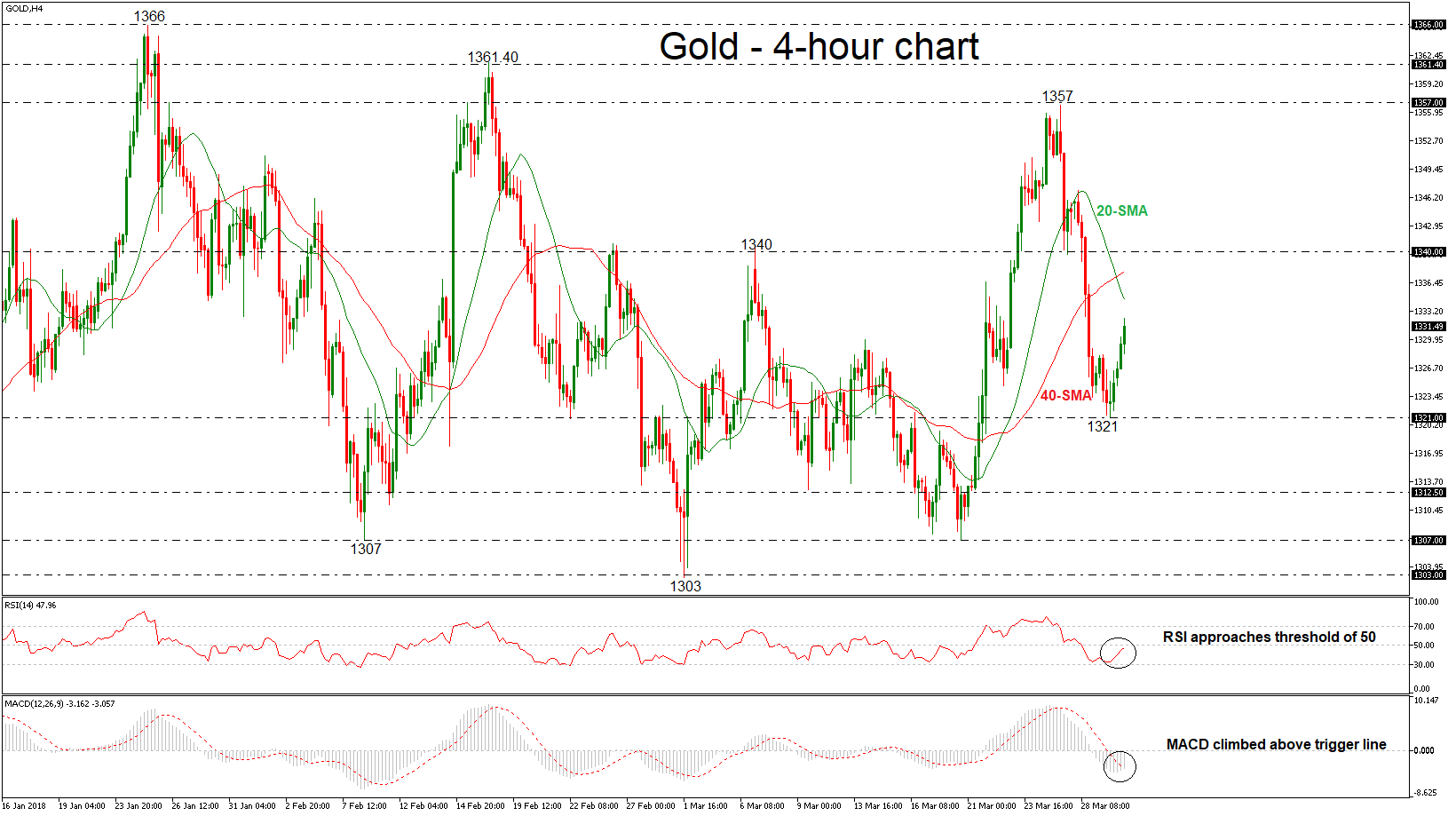

Gold Extends Gains After Rebound From 1321, Immediate Resistance At 20-SMA

Gold has been outperforming today following the rebound from the 1321 support level that hit last Thursday. Despite the latest pullback though, the precious metal has not posted a lower bottom below 1321, which makes one hesitant to trust further declines for now.

Looking at momentum oscillators in the 4-hour chart, they suggest further upside movement may be on the cards in the short-term. The RSI indicator is approaching the 50 level and is also pointing upwards. The MACD oscillator jumped above its red trigger line and is rising while in negative territory.

In case of further gains, immediate resistance may be found on the 20-simple moving average (SMA) around 1334. If price successfully surpasses the aforementioned obstacle, this would open the door towards the 1340 resistance barrier.

On the flipside, if the bears retake control, the price may stall initially near the latest one-week low of 1321. A potential downside violation of this level would raise the likelihood of more declines until the 1312.50 support.

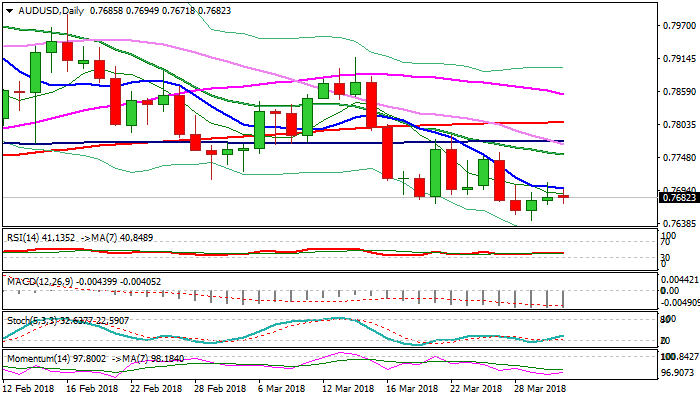

AUDUSD – Bearish Bias Will Remain Intact While 10 SMA Caps Recovery Attempts

Sideways mode dominates on Monday as Asian / early European action is shaped in tight Doji, due to Easter Monday's thinned conditions.

Recovery attempts off last week's low at 0.7642 (weekly cloud base) remain capped by falling 10SMA (currently at 0.7696) keeping risk shifted lower as daily techs are in firm bearish mode.

Current upside attempts could be seen as consolidation ahead of renewed attack at weekly cloud base, break of which would spark fresh extension of broader fall from 0.8135 and expose key supports at 0.7500.

Break and close above 10SMA would delay bears for extended recovery, but limited upside could be expected and stronger upticks should remain capped by falling 20SMA (currently at 0.7753).

Res: 0.7696, 0.7706, 0.7753, 0.7779

Sup: 0.7671, 0.7642, 0.7600, 0.7586

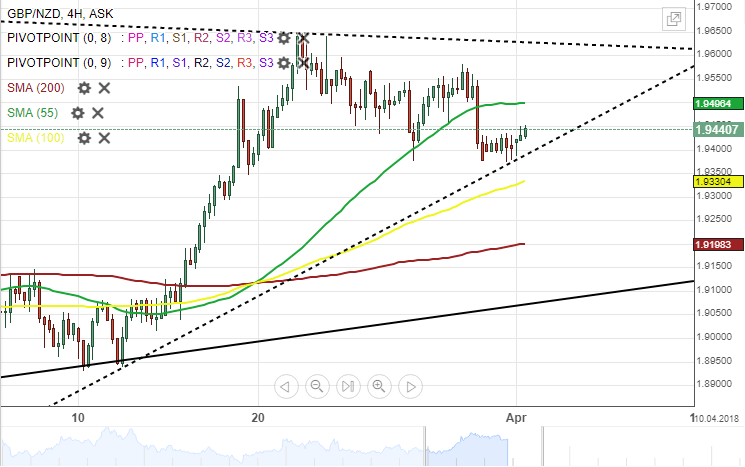

GBP/NZD 4H Chart: Trades In Medium-Scale Triangle

The British Pound has been constrained by several patterns against the New Zealand Dollar. The most important of which is the five-month medium-scale triangle which was formed on December 5.

During the past two weeks, the currency pair has been trading between the upper boundary and the lower boundary of the medium-scale triangle. A resistance set by the weekly pivot point was restricting the exchange rate to make any upward movement.

In the four-hour time frame, technical indicators suggest that the currency exchange rate could decline further. While on the daily time frame, its indicate that bulls are likely to grow stronger.