Sample Category Title

Stock Markets Took A Further Beating Yesterday

Market movers today

Focus today will continue to be on the equity market rout caused by worries over trade war and headwinds in the US tech sector. We should expect more news this week on the trade front as Commerce Secretary Wilbur Ross on Thursday last week said to Bloomberg that the announcement on tariffs on China would come 'very very soon'.

Markets will also look ahead for the US employment report on Friday, where wage growth will again be in focus.

On the agenda today are final Euro area PMIs and first PMI releases for UK, Sweden and Norway.

Selected market news

Stock markets took a further beating yesterday, as the S&P500 slid more than 2% leaving the index down 10% from the peak in late January. Tech stocks were among the big losers as Amazon came under fire from Donald Trump over Easter adding to the headwinds for tech stocks from Facebook and Tesla recently, see Bloomberg .

Bond yields and oil prices also moved lower, while the USD strengthened. Asian stock markets are trading in red this morning, whereas the S&P future is up slightly.

In addition to worries over trade and headwinds for tech stocks, there are rising signs of a turn in the global business cycle. The Chinese Caixin PMI for March dropped more than expected to 51.0 (consensus 51.7) from 51.6 in February. PMIs for other Asian countries were also softer in March and the US ISM index released yesterday dropped more than expected to 59.3 (consensus 59.6) from 60.8 in February. Overnight the Japanese Tankan survey for Q1 showed a similar picture of moderation in the business cycle, which has also been evident from a move lower in the Japanese PMI in recent months.

While the PMI data generally still point to robust growth, there are clear signs the global cycle is now decelerating . This normally causes more volatility in risk assets and provides support to core fixed income markets. We still expect equity markets to outperform bonds on a 12-month horizon but we are likely to see continued high volatility in the months to come. We also do not expect the next leg up in bond yields until 2019, see Yield Outlook: Higher 10Y yields very much a 2019 story , 15 March 2018.

On the trade front things may have to get worse before it gets better. The coming announcement from Trump on tariffs on Chinese goods will likely trigger a retaliation from China that may involve tariffs on US soybeans and aircraft, taking the trade worries a notch higher. We expect the trade tensions to calm down after that as negotiations unfold and no more measures are taken. However, until then the markets may worry over a further escalation, see also Flash Comment: Moderate Chinese retaliation but keeping the powder dry , 23 March 2018.

RBA Aware of Recent Rise in Yields

The April RBA meeting contained little surprise. Policymakers left the cash rate unchanged at 1.5% and made few changes in the policy statement. The central bank remained upbeat on growth and employment. Yet, it remained wary of the slow growth in wage. Meanwhile, the members took note of the recent decline in commodity prices and higher global short term interest rates. While the next rate move would likely be a hike, it might not be implemented for the rest of the year.

The central bank noted that business conditions are “positive” while non-mining business investment is “increasing”. While acknowledging slowdown in exports in late 2017, the members remained confident that exports growth would strengthen again later this year. Yet, it cautioned that household income growth stayed sluggish despite elevated debt levels. This might weigh on the level of household income. The employment situation has been strong as the decline in unemployment rate was accompanied with higher participation rate. The members repeated the concerns over slow wage growth, a situation that might continue for some time but the impact of strong economic growth is eventually passed to wage.

What was new in this meeting was the discussion on the higher short term rates. The members noted the recent “tightening of conditions in US dollar short-term money markets”, as a result of Fed funds rate hike. The members indicated that higher rates have been transmitted to other economies, including Australia. Yet, this has not yet caused a problem in the country. We expect the RBA would continue monitoring the development for now.

The monetary stance remained unchanged. As reiterated in the statement, “taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time”.

RBA Leaves Rate Unchanged

General Trend:

- Technology share declines continue into Asia

- Hong Kong listed utilities under perform; China President Xi urged curbs on pollution and coal usage

- South Korean chipmakers track declines in Intel

- Nikkei-weighed Fast Retailing in focus ahead of expected SSS figures (prior figures released after close)

- Australian natgas producer Santos rises on higher bid from Harbour Energy

- Reserve Bank of Australia (RBA) statement offers few surprises

- Conflicting signals from Australia March manufacturing surveys

- Australia money market rates continue to rise into new quarter

- Growth in Japan’s Monetary Base slows to 2012 level

- Chinese think tank expects Q1 GDP growth to maintain pace seen in Q4 2017

Headlines/Economic Data

Japan

- Nikkei 225 opened -1.3%; closed -0.5%

- TOPIX Electric Appliances Index -1%, Real Estate -0.5%

- Monex [+18%,before hitting daily limit], 8698.JP Said to have made offer to acquire cryptocurrency exchange Coincheck - Nikkei

- Renesas[-9%], 6723.JP INCJ may reduce its stake to ~33% in Renesas (vs 45.6% prior) - Japan press

- Itochu, 8001.JP Japan suspends company from importing rice, barely after it imported barely that has pesticides above regulatory levels

- Fanuc [6954.JP]: Declines over 2% after cautious broker commentary

- (JP) Japan Mar Monetary Base Y/Y: 9.1% v 9.4% prior; Monetary Base End of Period: ¥487.0T v ¥475.2T prior

- (JP) BoJ Tankan Inflation Survey: Japan companies expect consumer prices +0.8% 1-year from now v +0.8% prior; Companies expect consumer prices +1.1% 3-years from now v +1.1% prior; Companies expect consumer prices +1.1% 5-years from now v +1.1% prior

- (JP) Japan Industry Min Seko: China retaliatory tariffs do not benefit any nation, want to talk metals tariffs on basis of free trade

- (JP) Japan MoF sells ¥2.2T v ¥2.2T indicated in 0.1% (prior 0.1%) 10-yr JGB; avg yield 0.032% v 0.062% prior; bid to cover 4.16x v 4.53x prior

Korea

- Kospi opened -0.9%

- (KR) South Korea Govt flustered with US as it continues to make claims outside of the most recent trade agreement - Korean press

- (KR) SOUTH KOREA MAR CPI M/M: -0.1% V 0.1%E; Y/Y: 1.3% V 1.4%E

- (KR) South Korea Finance Ministry Official reiterates to take measures in case of excessive FX movements

- (KR) South Korea sells KRW1.85T in 30-yr bonds at 2.655%

China/Hong Kong

- Hang Seng opened -0.6%, Shanghai Composite -1.1%

- Hang Seng Utilities Index -1.4%, Energy -0.8%, Property/Construction, Info Tech -0.7%, Financials -0.4%; Consumer Goods +0.6%, Telecom +0.5%

- Shanghai Composite Property sub-index declines over 0.5%

- (CN) According to analyst from Savills, Beijing residential property market will reach a relatively stable level amid downside risks this year - China Daily

- (CN) PBOC imposed daily limits on payments conducted on mobile phones – Japanese Press

- (CN) China think tank CASS: Sees Q1 GDP at 6.8% - Chinese press

- (CN) China PBoC sets yuan reference rate at 6.2833 v 6.2764 prior

- (CN) China PBoC Open Market Operation (OMO): Skips OMO (8th straight session) v skipped prior; Net: CNY0B drain v CNY20B drain prior

- (CN) China Govt putting pressure on lenders to curb local govt debt risk – press

- (CN) China Finance Ministry (MOF): To cut resource tax on shale gas by 30% from April 1st

- (CN) China State Media comments on recently announced tariff counter measures: Imposed the tariffs on US products to ‘balance losses’

- (CN) China CBRC said to conduct inspections of certain large client loans - financial press

- Looking Ahead: China March Caixin Services PMI due for release on Wed

Australia/New Zealand

- ASX 200 opened -0.1%; closed -0.1%

- ASX 200 Consumer Discretionary Index -1.3%, REIT -0.6% Financials -0.5%, Utilities -0.5%; Energy +2.2%, Resources +1.8%

- Santos[+18.5%], STO.AU, Confirms received revised offer from Harbour Energy at A$6.50/shr/$4.98/shr ($4.70/shr cash and $0.28/shr special dividend) (prior offer was worth A$4.55/share), Reminder: Harbour made a A$4.55/shr offer for Santos about 6 months ago

- (AU) Australia Mar AIG Performance of Manufacturing Index: 63.1 v 57.5 prior (fresh record high)

- (AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50%; AS EXPECTED

- Looking Ahead: Australia Feb Building Approvals and Retail Sales due for release on Wednesday

North America

- US equity markets ended broadly lower: Dow -1.9%, S&P500 -2.2%, Nasdaq -2.7%, Russell 2000 -2.4%

- S&P500 Consumer Discretionary -2.8%, Consumer Staples -2.5%, Tech -2.4%

- CBS initial bid for Viacom reportedly values Viacom below current market value – press

- (US) Treasury Counselor Justin Muzinich reportedly to be nominated as Deputy Secretary of Treasury - press

Europe

- (UK) EU warns UK banks not to rely on Brexit transition deal - UK press

- AZN.UK Along with Shire said to be anonymously paying healthcare professionals and organizations to have drugs promoted through consultancy fees and related expenses, or for travel and accommodation at events the companies sponsored - London Times

- Looking Ahead: UK March Manufacturing PMI due for release

Levels as of 02:00ET

- Hang Seng -0.5%; Shanghai Composite -1.1%; Kospi -0.3%

- Equity Futures: S&P500 +0.2%; Nasdaq100 +0.2%, Dax -1.3%; FTSE100 -0.7%

- EUR 1.2311-1.2292; JPY 106.01-105.69; AUD 0.7693-0.7652;NZD 0.7237-0.7195

- Jun Gold -0.3% at $1,342/oz; May Crude Oil +0.1% at $63.06/brl; May Copper +0.6% at $3.06/lb

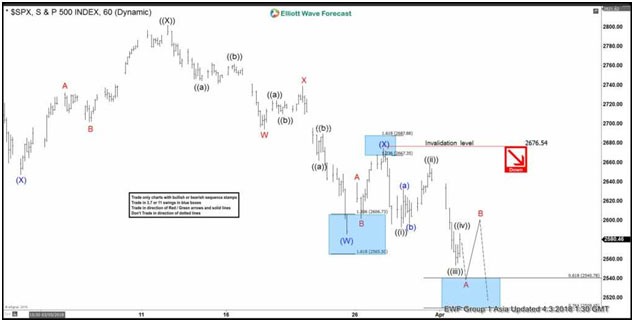

Elliott Wave View: SPX Further Weaknesses Likely

SPX Elliott Wave view suggests rally to 2801.90 on 3/13/2018 ended Primary wave ((X)). Decline from there is unfolding as a double three Elliott Wave structure where Intermediate wave (W) ended at 2585.89 and Intermediate wave (X) ended at 2674.22. Subdivision of Intermediate wave (W) unfolded as another double three of a lower degree where Minor wave W ended at 2694.59, Minor wave X ended at 2739.14, and Minor wave Y of (W) ended at 2585.89. Subdivision of Intermediate wave (X) unfolded as a zigzag Elliott Wave structure where Minor wave A ended at 2639.26, Minor wave B ended at 2601.81, and Minor wave C of (X) ended at 2676.54.

Intermediate wave (Y) is currently in progress as a zigzag Elliott Wave structure. A zigzag is a 5-3-5 Elliott Wave structure with ABC label. The subdivision of wave A is in 5 waves and the subdivision of wave C is also in 5 waves. In the case of SPX, decline from 2676.54 is unfolding as 5 waves impulse Elliott Wave structure where Minute wave ((i)) ended at 2593.06, Minute wave ((ii)) ended at 2659.07, Minute wave ((iii)) ended at 2553.80, and Minute wave ((iv)) is proposed complete at 2586.38.

Expect Index to extend lower 1 more time to end Minute wave ((v)) towards 2509.45 – 2540.78 and this next leg lower should also complete Minor wave A of a zigzag from 3.28.2018 high (2676.54). Afterwards, expect Index to bounce in Minor wave B in 3, 7, or 11 swing to correct cycle from 3.28.2018 high before the decline resumes. We don’t like buying the Index.

SPX Elliott Wave 1 Hour Chart

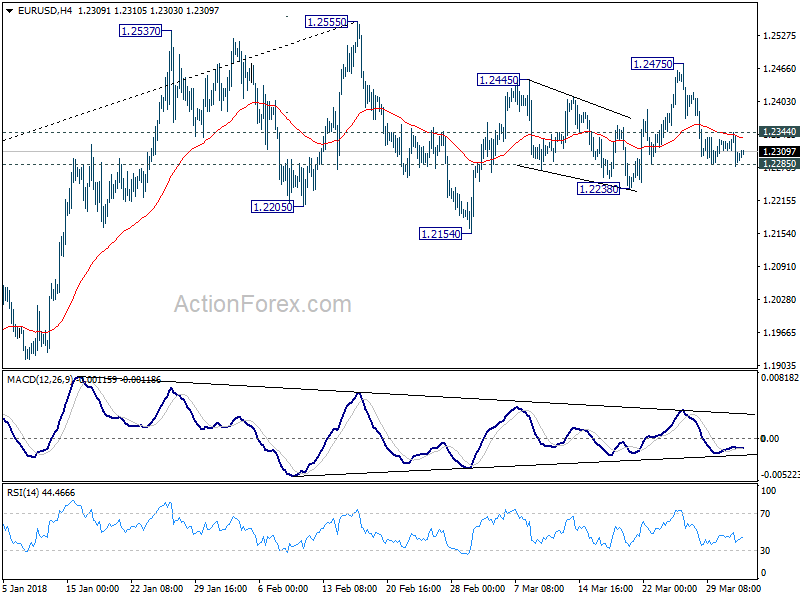

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2273; (P) 1.2309 (R1) 1.2337; More....

EUR/USD tried to break 1.2285 support but failed again. Intraday bias remains neutral with focus on 1.2285. Break will indicate hat whole rise from 1.2154 has completed with three waves up to 1.2475. And intraday bias will be turned to the downside for 1.2154 and below, to extend the decline from 1.2555. That will also be another sign of rejection from 1.2516 key fibonacci level. On the upside, above 1.2344 will turn bias back to the upside for 1.2475 and possibly further to 1.2555 high.

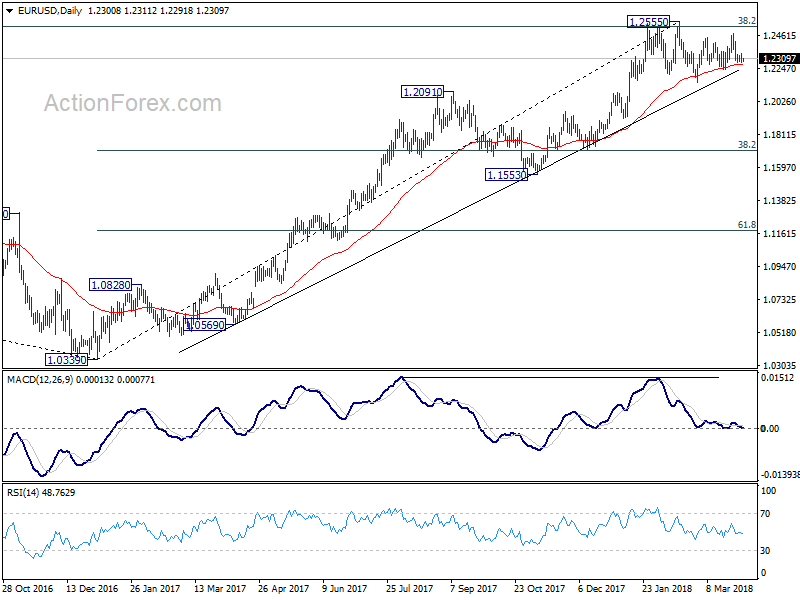

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862 in medium term.

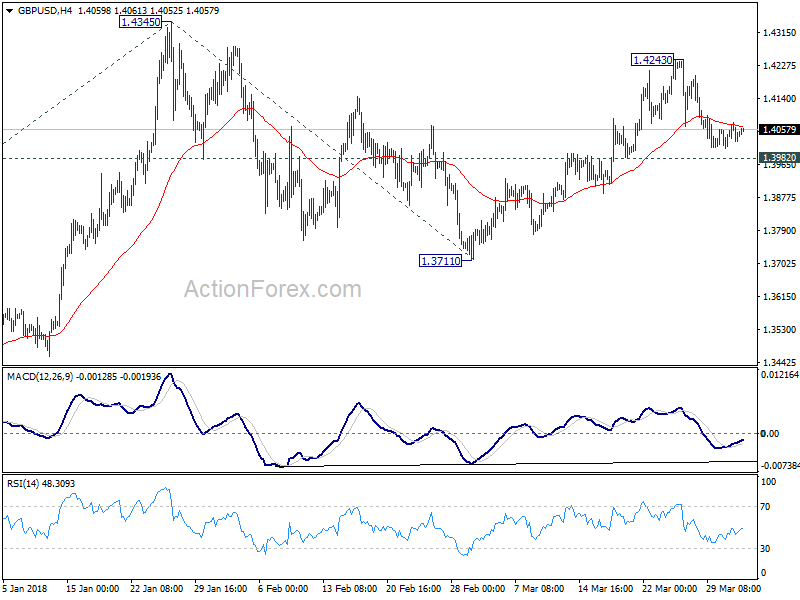

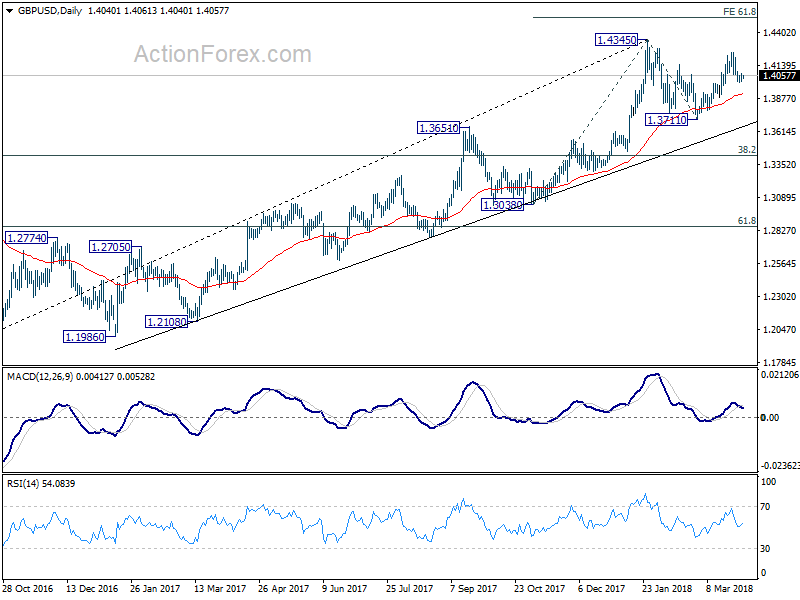

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4014; (P) 1.4046; (R1) 1.4074; More....

Intraday bias in GBP/USD stays neutral at this point. With 1.3982 minor support intact, further rise remains mildly in favor. On the upside, above 1.4243 will resume the rise from 1.3711 and target 1.4345 high first. Decisive break there will resume larger up trend and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. On the downside, however, firm break of 1.3982 will indicate completion of rebound from 1.3711. In that case, intraday bias will be turned back to the downside for retesting 1.3711.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

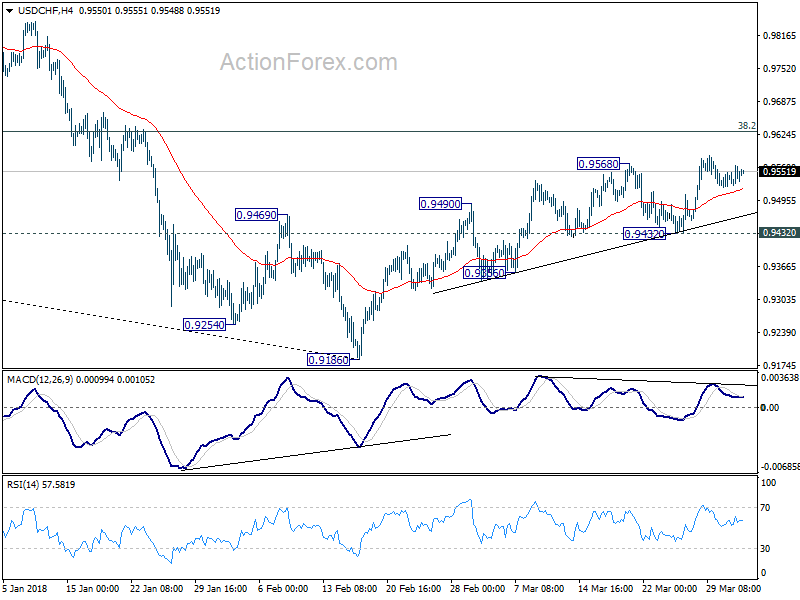

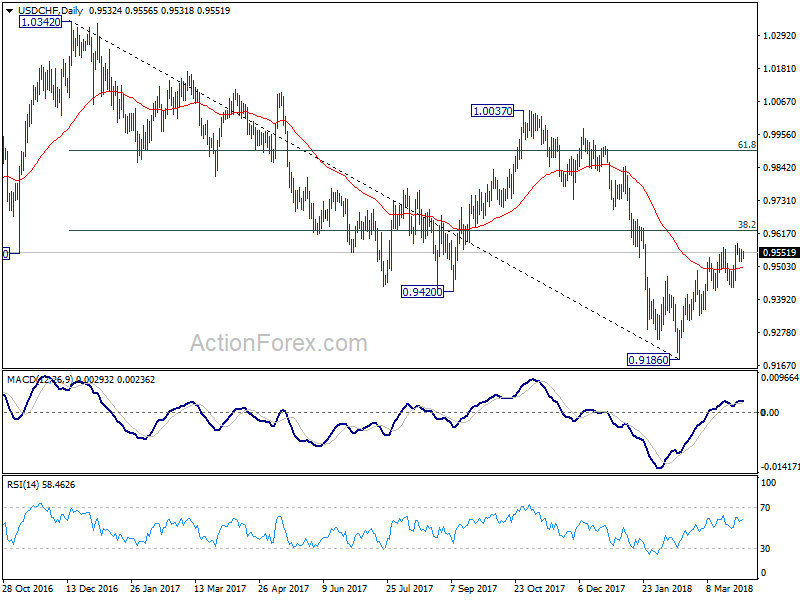

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9527; (P) 0.9546; (R1) 0.9570; More...

No change in USD/CHF's outlook. While the corrective rise from 0.9186 might extend higher, we'd expect strong resistance from 0.9626 key fibonacci level to limit upside. On the downside, break of 0.9432 support will indicate near term reversal and completion of rebound from 0.9186. In this case, intraday bias will be turned back to the downside for retesting 0.9186 low. However, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

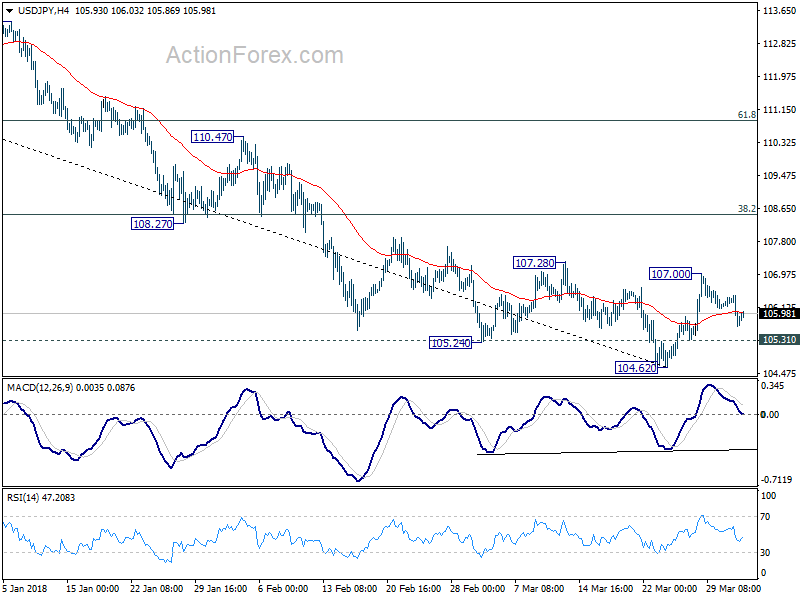

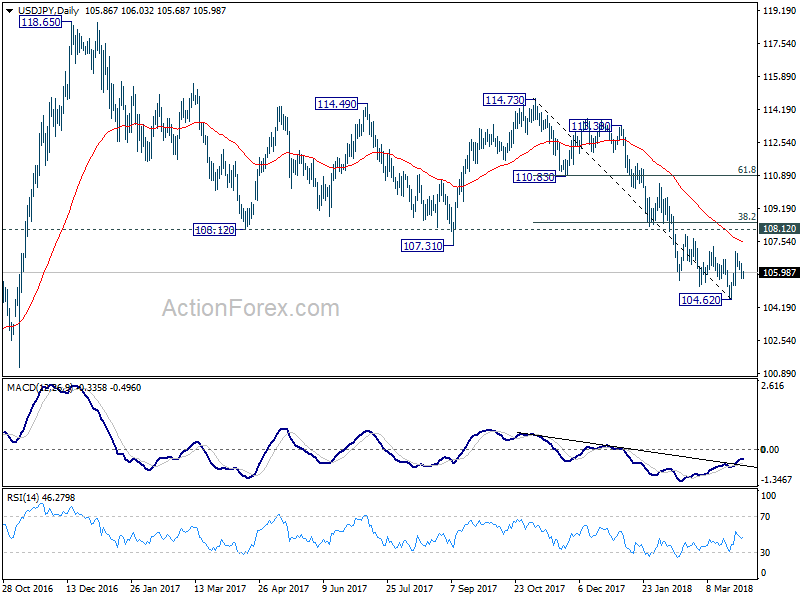

USD/JPY Daily Outlook

Daily Pivots: (S1) 105.55; (P) 105.99; (R1) 106.34; More...

With the retreat from 107.00, intraday bias in USD/JPY is turned neutral first. Another rise is mildly in favor as long as 105.31 minor support holds. Above 107.00 will target 38.2% retracement of 114.73 to 104.62 at 108.48. At this point, there is no confirmation of trend reversal yet. Hence, we'll look at the reaction from 108.48 (which is close to 108.12 too) to assess the chance. On the downside, below 105.31 minor support will indicate that the rebound is completed and turn bias back to the downside for 104.62 and below.

In the bigger picture, medium term down trend from 118.65 (2016 high) is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

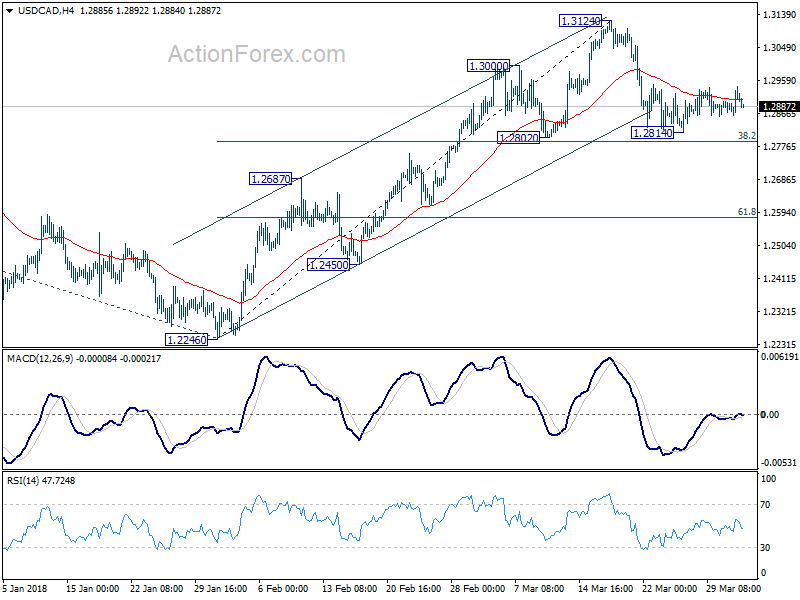

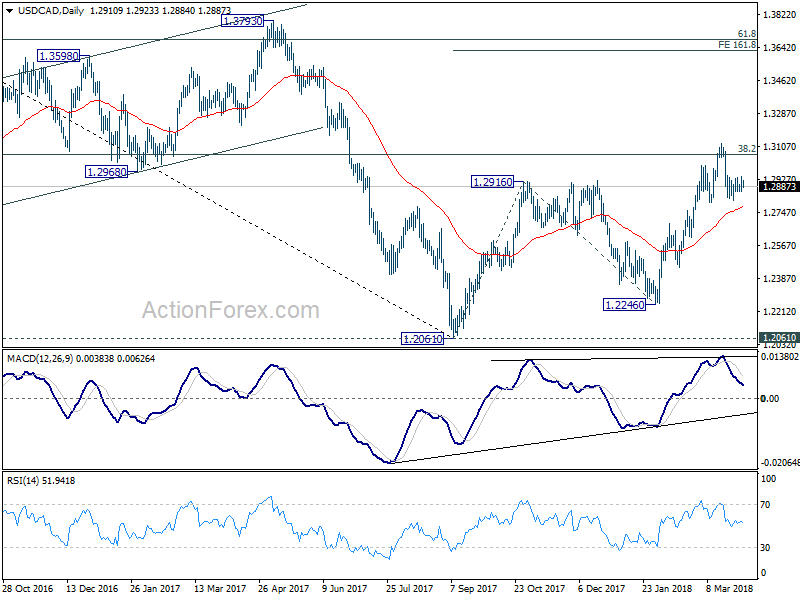

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2868; (P) 1.2906; (R1) 1.2949; More....

USD/CAD is staying in consolidation above 1.2814 and intraday bias remains neutral first. For the moment, we'd still expect strong support from 1.2802 cluster support zone (38.2% retracement of 1.2246 to 1.3124 at 1.2789) to contain downside and bring rebound. Break of 1.3214 will extend larger rise from 1.2061 to 161.8% projection of 1.2061 to 1.2916 from 1.2246 at 1.3629. However, on the downside, firm break of 1.2789/2802 will raise the chance of rejection by 1.3065 medium term fibonacci level. In that case, intraday bias will be turned back to the downside for 1.2246 support instead.

In the bigger picture, we're favoring the medium term bullish case. That is, larger down trend from 1.4689 has completed at 1.2061 as a correction, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Sustained break of 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will pave the way to 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2802 support holds. However, rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

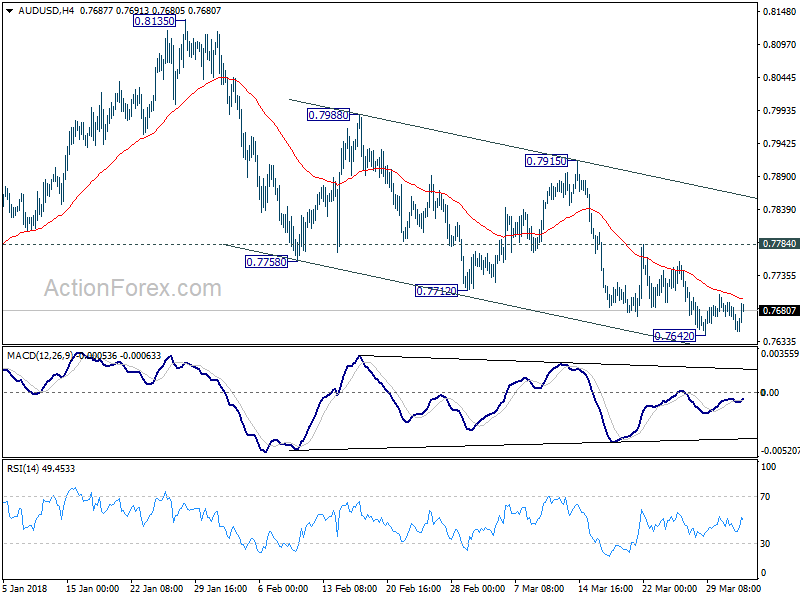

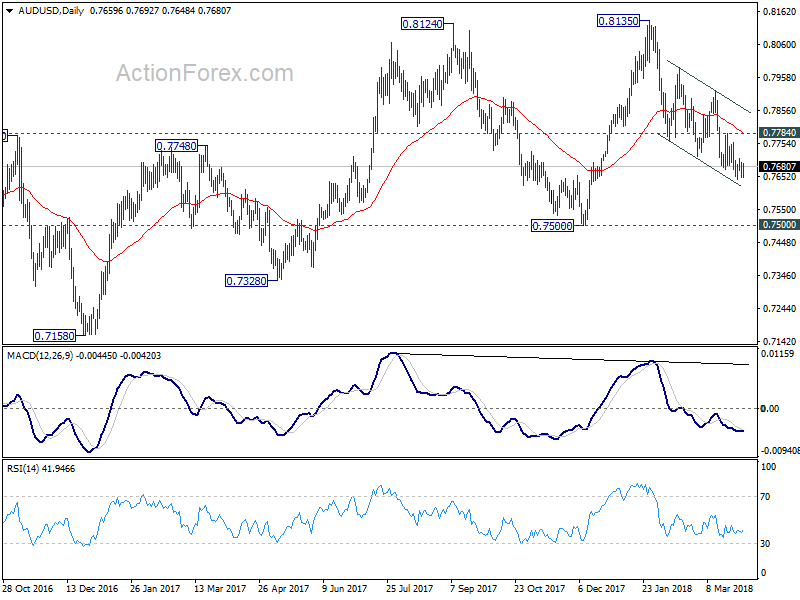

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7641; (P) 0.7668; (R1) 0.7687; More...

Intraday bias in AUD/USD stays neutral as it's bounded in consolidation above 0.7642 temporary low. More sideway trading would be seen and stronger recovery cannot be ruled out. Still, near term outlook stays bearish as long as 0.7784 resistance holds, and further decline is expected. Break of 0.7642 will extend recent fall from 0.8135 to retest 0.7500 key support level. On the upside, however, break of 0.7784 will suggest near term reversal and turn bias to the upside for 0.7915 resistance first.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.