Sample Category Title

GBPUSD Intraday Analysis

GBPUSD (1.4056): The British pound formed an inside bar and price action was seen slipping back to previous levels, albeit forming a higher low. This suggests that price could be attempting to push higher in the near term. The immediate resistance level at 1.4115 is the ideal target to the upside that could be tested. To the downside, the support at 1.4000 is most likely to hold the declines.

EURUSD Intraday Analysis

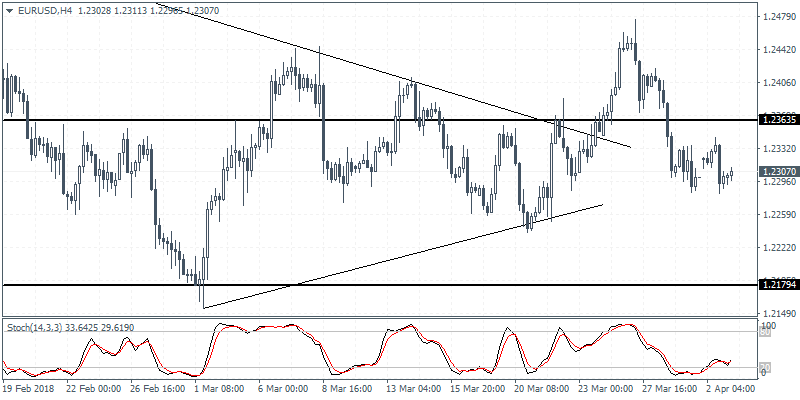

EURUSD (1.2307): The EURUSD rose to intraday highs of 1.2344 before giving up the gains. Price action remained weak on the day. However, the common currency is looking to post some gains in the early Asian trading session. We expect the euro to remain subdued below the 1.2363 level of resistance in the near term. Any gains are likely to be capped near the resistance level with the potential for a reversal expected to keep prices range bound below 1.2363 region.

China’s Tariffs On U.S. Imports Puts Investors On The Backfoot

The markets opened yesterday amid thin trading yesterday. Investors woke up to the news about China imposing fresh tariffs on certain U.S. imports which was seen as a retaliation to the U.S. tariffs on steel and aluminum. Equity markets fell on the day and the Japanese yen was seen strengthening on a modest risk off sentiment.

Gold prices surged 1.19% while the Japanese yen rose 0.27% on the day.

The ISM manufacturing PMI data for March showed that the index fell to 59.3 which was more than the forecast of a decline to 60.1. This comes amid the manufacturing index hitting recent fresh highs at 60.8 in February. The ISM manufacturing prices however posted strong gains, rising to 78.1 and beat forecasts of 72.5.

Earlier today, the Reserve Bank of Australia was seen keeping interest rates unchanged at 1.50% as widely expected for the 18th consecutive month. Looking ahead, the economic calendar for the day covers the final manufacturing PMI from the Eurozone.

In the UK, the manufacturing PMI data for March is expected to show the index slipping to 54.8 down from 55.2 in February. Fed member, Brainard is scheduled to speak later in the evening.

USDJPY Bearish Below 106.00 Level

The U.S dollar has turned lower against the Japanese yen, following a major sell-off in global equity markets, with riskier assets and so-called FANG stocks leading the declines. The USDJPY pair is currently trading around the 105.90 level, after breaking lower during Monday’s U.S trading session and finding support from the 105.64 level. Traders now look to the European markets open, with the 105.50 level the next key support area USDJPY traders are watching.

The USDJPY pair is bearish while trading below the 106.00 level, key technical support is found at 105.50, 105.24 and 104.64 levels.

Should price-action move back above the 106.00 level, a correction towards the 106.45 and 107.00 levels cannot be ruled out.

EURUSD Only Bearish Below 1.2300 Level

The euro currency has moved lower against the U.S dollar, as risk-off trading sentiment spreads through financial markets, following China’s decision to impose tariffs on imports of U.S Pork and Fruit products. The EURUSD pair is currently consolidating just above 1.2300 support level, after declining rapidly from the level 1.2345 area on Monday. The euro is likely to come under selling pressure once clearly below the 1.2300 level, with the 1.2275 level the key support area to watch.

The EURUSD pair is strongly bearish whilst trading below the 1.2275 level, further declines towards the 1.2239 and 1.2205 level seem likely.

Should price-action continue to hold above the 1.2300 level, further upside towards the 1.2334 and 1.2382 levels remains possible.

PMI Data Take Center Stage Tuesday

The global financial markets are back in full swing on Tuesday, with traders returning from the Easter long weekend. Action begins bright and early with a steady stream of Eurozone releases leading into a less active US session.

Germany's federal statistics department will report on retail sales at 06:00 GMT. Receipts at retail stores are projected to rise 0.8% in February, following a 0.7% drop the previous month. That translates into an annualized increase of 2.2%.

The Swiss government will also report on retail sales on Tuesday. The report, which is scheduled for release at 07:15 GMT, will likely show an annualized decline of 0.8% in February.

IHS Markit will release a steady stream of PMI reports for the Eurozone and UK economies beginning at 07:45 GMT. Italy, France, Germany, Eurozone and UK PMI will all be released within the span of 45 minutes. The Eurozone manufacturing PMI report is forecast to come in at 56.6.

In other European data, the Spanish government will issue its monthly unemployment report at 08:00 GMT. The data set is expected to show a sharp drop in the jobless count.

Shifting gears to North America, the Institute for Supply Management (ISM) will release the New York business conditions index at 13:45 GMT.

In terms of monetary policy considerations, Federal Open Market Committee (FOMC) members Neel Kashkari and Lael Brainard will deliver speeches at 13:30 GMT and 20:30 GMT, respectively.

Earlier in the day, the Reserve Bank of Australia (RBA) voted to keep interest rates on hold at 1.5%. The decision was in line with the consensus view.

AUD/USD

The Australian dollar has been in a gradual downtrend for the last two weeks, with the AUD/USD falling 250 pips over that period. At last check, the pair was trading at 0.7665, with immediate support located at 0.7625 and 0.7590. On the opposite side of the spectrum, resistance levels are seen at 0.7700 and 0.7740.

EUR/USD

Europe's common currency drifted lower on Monday, hitting a session low of 1.2297. EUR/USD is back to trade slightly above 1.2300, although downside risk remains. At current price levels, the pair faces immediate support at 1.2282, which corresponds to the 29 March low, followed by 1.2241, which corresponds to the 21 March low. On the opposite side of the spectrum, initial resistance is located at 1.2477, the high from 27 March.

GBP/USD

Cable is another US dollar pair in the midst of a downtrend. GBP/USD rose to a high of 1.4238 last week but has since declined nearly 200 pips to settle in the mid-1.4000 range. Immediate support levels include 1.4010 and 1.3985. On the flipside, resistance is located at 1.4040 followed by 1.4085.

Oversupply Concerns Haunt Oil Market

Crude oil prices recovered slightly after yesterday selloff taking both benchmarks to lowest levels in two week. The front-month WTI and Brent crude oil contracts stabilized after plunging -2.97% and -3.74%, respectively, on Monday. Concerns over oversupply have put a lid to any price rally. It has been reported that Russia output rose to 10.97M bpd in March, up from 10.95M bpd a month ago. This was surprising as the oil giant has pledged, alongside several OPEC members, to cut output so as to support oil prices. The output increase has raised concerns over the compliance of the participants of the deal.

Moving to the Gulf, it was reported that Saudi Arabia would lower prices for all crude grades for its Asian customers. Separately, Bahrain had just announced over the weekend the discovery of a new oil field off the country's western coast that is forecast to contain "highly significant quantities of oil and gas". According to the country’s oil minister, Shaikh Mohamed bin Khalifa Al Khalifa, the oil and gas reserve there is at “at substantial levels, capable of supporting the long-term extraction of tight oil and deep gas".

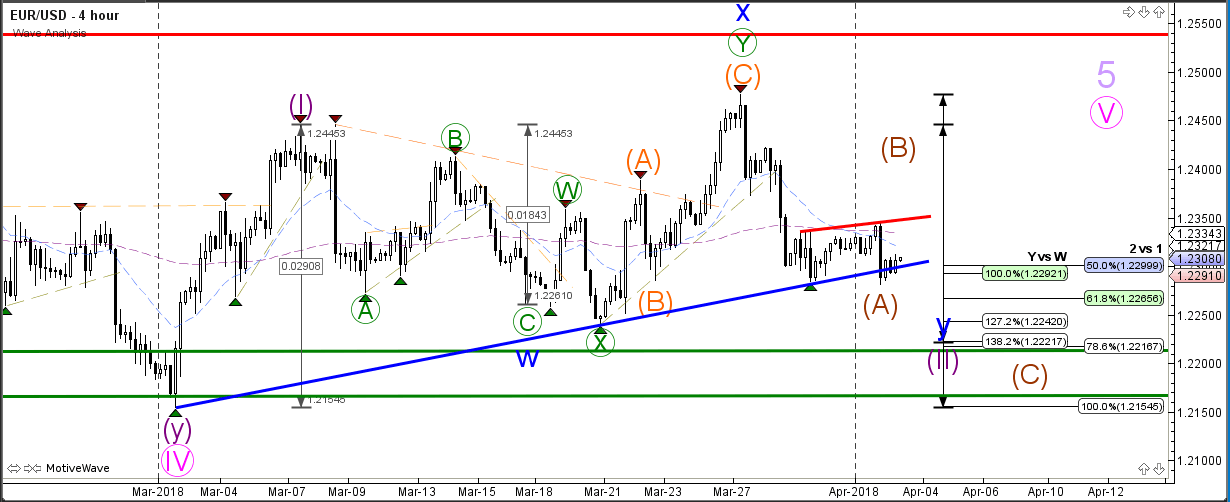

Wave Pattern EUR/USD Depends On Next Impulse Or Correction

The EUR/USD is still challenging the support line (blue), which is a key bounce or break spot. The bearish retracement is either completing a wave 2 (purple) or a wave A of larger bearish ABC (brown). If price breaks above the resistance (red), it will be important to see how price breaks above the trend line: correctively or impulsively. An impulse could indicate a bullish continuation.

The EUR/USD has clear support (blue) and resistance (red) trend lines at the moment. A bearish break could indicate a continuation of bearish wave 5 (red) whereas a bullish break could indicate the start of wave 3 OR a larger bearish ABC correction (brown).

Most European Markets Were Closed Yesterday For Easter Monday

Markets

Most European markets were closed yesterday for Easter Monday. The US Note future traded flat during European hours, awaiting the US stock market opening. Last week's tech sell-off continued with Amazon taking the biggest part of the beating after another round of rants by US President Trump and Republican senator Rubio. US stock markets eventually closed 1.9% to 2.75% lower with Nasdaq underperforming. Retaliatory tariffs from China weighed on general risk sentiment and commodity markets as well, even if they remain limited for now (eg not yet targeted at important US soy bean exports). The new US stock market swoon provided a safe haven bid in US Treasuries, though volumes were rather low. Another strong, but close to consensus, US manufacturing ISM couldn't change the tide. The ISM declined from 60.8 to 59.3 (vs 59.6 expected) in March. The “prices paid” component surged to 78.1, in a probable response to president Trump's hawkish trade rhetoric/actions. The US yield curve bull steepened compared with last Thursday's close with yields 2 bps (2-yr) to 0.9 bps (10-yr) lower.

EUR/USD is locked in an extremely narrow sideways trading range since last Thursday (1.2282-1.2345). Yesterday's only noticeable move occurred after the US stock market opening with EUR/USD dropping to the lower bound of the above mentioned range on deteriorating risk sentiment. The move occurred mainly through EUR/JPY selling. The trade-weighted dollar also managed to preserve small daily gains, closing above 90. EUR/GBP's intraday trading pattern resembled EUR/USD's with one move lower, from 0.8775 to 0.8755

Today's eco calendar remains rather thin with final EMU manufacturing PMI's (decline from 58.6 to 56.6 expected to be confirmed) and the UK manufacturing PMI (54.7 from 55.2 expected). We expect them to be of minor importance. Minneapolis Fed governor Kashkari (arch dove) and Washington Fed based governor Brainard (dove turned neutral) are scheduled to speak, but topics suggest that they won't touch on monetary policy. Fragile risk sentiment will remain the driving market force ahead key US eco data/events later this week. There's no reason to row against the current tide, suggesting more gains for core bonds, while the impact on FX markets will be more subdued. There's no reason to expect technical breaks in lasting ranges (see graphs). Some investors probably want to remain sidelined ahead of US ADP employment report, non-manufacturing ISM (Wednesday), payrolls and a speech by Fed chair Powell on the economic outlook (Friday). On intra-EMU bond markets, Italian BTP's might become more vulnerable as president Mattarella officialy starts negotiations to form a new government.

News Headlines

The Reserve Bank of Australia kept its policy unchanged at 1.5% for a 20th straight month. No change is expected until 2019. Growth is expected to outperform this year, but inflation will only very gradually move higher. Governor Lowe specifically mentioned the risk of a potential trade war, which could undermine Australia's current momentum and warrants the central bank to err on the dovish side. AUD/USD rises from 0.7650 to 0.7690 this morning, but that's mainly because of a bounce in base metals.

The Times reports that British banks operating in Europe have been warned by EU regulators (ECB) that they cannot rely on a transition deal with the bloc and must implement their hard Brexit contingency plans.

The Trump administration is pushing for a preliminary Nafta deal to announce at a summit in Peru next week, and will host cabinet ministers in Washington to try to achieve a breakthrough, according to three people familiar with the talks.

Risk Aversion Returns After Easter Break

The fall in tech stocks and escalating trade tensions continued to rattle markets after the Easter break. The S&P 500 fell 2.2% on the first trading day of the second quarter, sending the Index back into correction territory (a more than 10% fall from its peak). Although investors are trying to adjust to higher volatility in equities, the close below the 200-Day Moving Average for the S&P 500 will likely bring more anxiety. This is the first time since June 2016 the Index has closedbelow this key technical level, and the last time we had two consecutive trading days below the 200-Day Moving Average was in January 2016. Back then, the selloff was driven by the People's Bank of China, which shocked traders by setting the official midpoint rate on the yuan against the dollar at itslowest level since March 2011. The news sent global stock markets tumbling as investors feared it would trigger a currency war and the S&P 500 crashed by more than 10% in less than a month.

This time, it's Trump's tariffs and tech stocks driving the selloff, and I don't think the U.S. President is doinghimself any favors before the midterm elections. Beijing's response hasn't been aggressive, by imposing levies on $3 billion worth of imports from the U.S.; the question nowis - what's next?

A tariff ‘tit for tat' is a lose-lose scenario. So, it's likely that after this war of nerves, the world's two largest economies will find a middle ground. Markets should get used to Trump's negotiating style - kicking off with something dramatic, and then scalingdown through negotiations.

Investors will turn their attention today to the Manufacturing PMI reports from the E.U. and U.K., to find out whether the stock selloff is justified by an economic slowdown.

If forthcoming data starts pointing out that economic growth has peaked after a strong period of synchronized global expansion, we're likely to see further selloff in equities;otherwise, buying the dips will likely return, especially now that valuations are more attractive than whenwe started the year.