Sample Category Title

EURUSD – Fresh Attempts Higher Face Strong Barrier At 1.2345, Four-Day Congestion Top

The Euro moved higher in early European trading after quiet trading in Asia on Tuesday.

Downbeat German retail sales data showed no impact, with focus turning towards Manufacturing PMI data from EU members.

Fresh attempts higher struggle at 1.2340 zone (converged 10/20/55SMA’s) after strong upside rejection at 1.2345 on Monday, keeping near-term action within 1.2280/1.2345 congestion for the fourth straight day.

Positive signals come from slow stochastic emerging from oversold territory and ascending 14-d momentum which attempts into positive territory, however, break above a cluster of MA’s and regain of next pivot at 1.2355/57 (Fibo 38.2% of 1.2476/1.2281/base of 4-hr cloud) is required to confirm recovery and expose key barriers at 1.2394/1.2401 (Fibo 61.8%/daily cloud top).

Otherwise, the pair could stay in extended consolidation on repeated recovery failure, with downside to remain vulnerable.

Bearish scenario sees violation of n/t congestion floor at 1.2280 as signal for fresh weakness which could extend towards double-bottom at 1.2240.

Res: 1.2345, 1.2357, 1.2401, 1.2430

Sup: 1.2292, 1.2280, 1.2240, 1.2200

UK PMI manufacutring ticked up, GBPUSD eyes 1.4095 minor resistance

UK PMI manufacturing rose 0.1 to 55.1 in March, above expectation of 54.7. Markit noted that it signals "steady growth rate at the end of opening quarter".

Quotes from the release:

Quotes from the release:

Rob Dobson, Director at IHS Markit, which compiles the survey:

- "The latest PMI survey provided further evidence that UK manufacturing has entered a softer growth phase so far this year. Although the pace of output expansion ticked higher in March, which is especially encouraging given the heavy snowfall during the month, this was offset by slower increases in new orders and employment. Average rates of increase over the opening quarter as a whole are also down noticeably from the growth spurt seen at the end of 2017. Compared to official data, the performance through quarter one is consistent with only a 0.4-0.5% gain in production volumes, a considerable slide from the fourth quarter's 1.3% increase.

- "The key question is whether growth can now be sustained, albeit at a lower level, into the coming months. On that front the news is generally positive. Manufacturers are still reporting solid inflows of new work from domestic and overseas markets. Business optimism is holding steady at an elevated level, with over 54% of companies expecting output to expand over the coming 12 months. With cost inflationary pressures also moderating to provide some respite for margins, the sector looks set to make further slow and steady progress as we head through the spring."

Duncan Brock, Group Director at the Chartered Institute of Procurement & Supply:

- "After the mini-boom of productivity at the end of last year, the sector still held its own, delivering a steady if unremarkable performance with overall activity improving very modestly from last month.

- "Purchasing activity was higher than February's 8- month growth low but purchasers were frustrated by their suppliers who failed to deliver essential materials on time and delivery times continued to get longer. As shortages were reported the finger of suspicion was pointed at the continuing impact of inflation on raw material prices caused by the scarcity, and subsequently forcing firms to pass on these increased prices to customers at a significantly elevated rate.

- "However, the biggest disappointment was the softening of new orders to a nine-month low followed by a feeble rise in job creation as the most discouraging result this year. While trade from the domestic market was still strong, and export markets also grew for the 23rd month in a row, the foundations for the sector's continuing strength were looking a little more unstable.

- "Without a significant rise in new orders, and if supply chains are still disrupted by shortages or the weather, for the next few months it's anticipated that there will be a continued muted pace of growth. A rather apathetic prediction, but while optimism remains high and the sector continues its efforts to increase marketing activity and launch new products, everything could change."

GBP trades notably higher today against USD and JPY. With 1.3982 minor support intact, choppy fall from 1.4243 is seen as a corrective pull back. Break of 1.4095 will suggests that such pull back is completed and bring stronger rebound back to 1.4243.

Forex Analysis: UK Manufacturing PMI Coming Up As RBA Leaves Rates On Hold At 1.5%

The UK Markit Manufacturing PMI is one of the data releases that will give traders a look into the performance of the European Manufacturing sector today. Most of the PMIs from across the continent are expected to show a softening. This is due to supply chain constraints and shortages of inputs, which have caused a rise in prices charged by suppliers. There is no easing expected in this, as new order inflows are continuing to grow. Supply is reaching its capacity limits and demand is still strong. This could lead to an increase in inflation down the line.

The RBA has left Interest Rates on hold at 1.5% today, with the main risk to the economy sited as a strengthening AUD that would lead to slower economic pickup. The outlook for household consumption was also a concern, cited by the bank as a source of uncertainty. The outlook on inflation was that it is expected to remain low for some time. The housing markets have slowed in both Melbourne and Sydney. There was little reaction in the markets, as the text was largely the same from the previous statement and the rate was left unchanged.

Japanese Tankan Large Manufacturing Outlook (Q1) came in at 20 against an expected 22, from 21 previously, which was revised up from 19. Tankan Large Manufacturing Index (Q1) was in at 24 against a consensus of 25, from 26 previously, which was revised up from 25. Tankan Large All Industry Capex (Q1) was 2.3% against a consensus of 0.6%, with a prior reading of 6.4%, which was revised down from 7.4%. USDJPY sold off from 106.352 to 106.182 following the data release.

Chinese Caxin Manufacturing PMI (Mar) came in at 51.0 against an expected 51.7, from 51.6 previously.

Canadian Markit Manufacturing PMI (Mar) was as expected at 55.7, from 55.6 previously. USDCAD moved higher from 1.28619 to 1.28924 after this data release.

US ISM Manufacturing PMI (Mar) was 59.3 against an expected 60.0, from 60.8 previously. ISM Prices Paid (Mar) was 78.1 against an expected 74.5, from a prior 74.2. This data shows a softening in US manufacturing after the data matched the multi-year high last month that was set in September. USDJPY fell from 106.434 to 105.939 after this release.

Australian AiG Performance of Mfg Index (Mar) came in as expected at 63.1, from 57.5 previously. As this data came in as expected it had little impact on the market but has reached new multi-year highs on surpassing the 60.0 level. This shows strong performance from the manufacturing sector and an improved economic outlook.

EURUSD is up 0.06% overnight, trading around 1.23090.

USDJPY is up 0.09% in early session trading at around 105.977.

GBPUSD is up 0.9% this morning, trading around 1.40564.

USDCAD is down -0.18% in early trade at around 1.28885.

Gold is down -0.17% in early morning trading at around $1,339.00.

WTI is up 0.27% this morning, trading around $63.08

Manufacturing PMI Data For European Economies On The Agenda

At 08:55 GMT, German Markit Manufacturing PMI (Mar) is expected to be unchanged at 58.4. This data set seems to have peaked in January at 63.3 when it exceeded the 2011 high of 62.7. The last two readings have shown a softening in the data, with an expectation for this reading to fall under the 60 mark. EUR traders will be closely following this data release.

At 09:00 GMT, Eurozone Markit Manufacturing PMI (Mar) is expected to be unchanged at 56.6. This dataset reached its peak in January at 60.6, when it exceeded the 2011 high of 59. The last two readings have shown a softening in the data, indicating a slowing of the manufacturing industry is on the cards. EUR crosses may be impacted by this data release.

At 09:30 GMT, UK Markit Manufacturing PMI (Mar) will be out with an expected headline number of 54.5, from 55.2 prior. The consensus is for a reading generally in-line with other releases this morning and for a further softening from the high created in December at 58.2. Seasonally, Q1 is a time where this data point tends to weaken, as has been seen over the last few years. Slower output growth was a factor cited in the weakening number, despite stronger new order inflows, strengthening job creation and demand. GBP pairs may see an impact from this data release.

At 14:30 GMT, US FOMC Member Kashkari is due to speak. Comments may result in moves in USD crosses.

Tentative – GDT Price Index was -1.2% previously. New Zealand Dollar traders will be closely watching this data release as the economy is largely agriculture-focused.

At 21:30 GMT, US FOMC Member Brainard is due to speak about financial stability at New York University’s Stern School of Business. Audience questions are expected and comments may result in moves in USD crosses.

China pledged retaliation to US at same proportion, scale and intensity

More response from China to the US regarding the Section 301 tariffs.

China's Ambassador to the United States Cui Tiankai said the tariffs on 128 US products started this week were a measure to the 232 steel and aluminum tariffs only.

For the Section 301 tariffs on the USD 50-60b Chinese imports to US, Cui pledged to take "countermeasures of the same proportion and the same scale, same intensity." But for now, Cui said China has yet to decide on the countermeasures.

Cui also added that China is strengthening its legal system and be ready to "look at the specific cases if there's any violation of intellectual property rights… no matter by whoever."

Cui emphasized that "The real question is how we can make all the technology benefit as many people as possible and all the economies, all the people, will benefit from such programs and there would be a better life for everybody." And, "It's not a matter of who will get supremacy, sort of."

Right now, there is no details on what products would be included in the Section 301 tariffs. And US Trade Representative Robert Lighthizer has until Friday to come up with that list.

Safe Havens Shine Brightly As Equities Extend Losses

Here are the latest developments in global markets:

FOREX: The US dollar traded 0.1% lower against a basket of six major currencies on Tuesday. Yesterday, the major mover was the Japanese yen, which surged on safe-haven demand, as trade concerns remained at the forefront. The Canadian dollar also gained amid speculation that the NAFTA talks could bear fruit soon.

STOCKS: US markets sank once more yesterday, beginning the new quarter on the back foot as worries over protectionism and the outlook for technology companies crippled demand for stocks. The tech-heavy Nasdaq Composite led the charge lower, falling by 2.7%, while the S&P 500 and the Dow Jones dropped by 2.2% and 1.9% respectively. Nonetheless, futures tracking the Dow, S&P and Nasdaq 100 are all flashing green at the moment, pointing to a higher open today. Asian markets were mixed, with Japan's Nikkei 225 and the Topix falling by 0.45% and 0.3% correspondingly, while in Hong Kong, the Hang Seng rose 0.5%. In Europe, futures tracking all the major indices are well into negative territory at the moment, suggesting these benchmarks are likely to open lower.

COMMODITIES: In energy markets, oil prices traded a little higher today, recovering some of the significant losses they posted yesterday. Both WTI and Brent crude plunged more than 2% on Monday, mimicking the sharp declines in equity markets. Today, prices will continue to respond to any changes in risk appetite, while investors will also look to the release of the private API crude inventory data for an update on the state of US production. In precious metals, gold soared yesterday, as continued trade uncertainties led traders to seek the safety of the yellow metal. Prices are currently consolidating near $1340 per ounce, and in case of further advances, resistance may be met near the metal's recent highs at $1356.

Major movers: Yen and gold shine, stocks drop as “China strikes back”

Trading at the start of the new quarter was largely characterized by heightened risk aversion. Major stock indices plummeted, while safe-haven assets like the yen and gold came under renewed buying pressure, as American traders returned to their desks and digested the latest chapter in the trade war saga, that China imposed its own tariffs on the US. Besides worries around trade, the tech sector also took a heavy hit, with fears of increased regulation following Facebook's privacy scandal and President Trump's salvo of Twitter attacks on Amazon taking their toll on these stocks.

The S&P 500 closed below its 200-day moving average, a critical support territory that had halted multiple declines in the recent past, tilting the technical picture to the downside and eroding one of the last lines of defense that had held in the index.

Moving forward, the spotlight may remain on whether the trade standoff will escalate further. Note that the latest Chinese tariffs on the US were retaliation to the original US steel and aluminum levies, not to the recent tariffs the US administration announced last week, which will be aimed at Chinese technology imports. This suggests more countermeasures by China may be in store soon, once the US formally unveils its technology tariffs. Interestingly enough, the Chinese Ambassador to the US said yesterday that his nation will counter any new US tariffs with measures of equal proportion, scale, and intensity. Overall, risk sentiment is on wobbly legs right now, and for it to recover, investors may need to see clear signs that this situation is just a prelude to serious trade negotiations, not the beginning of a tit-for-tat trade skirmish.

Elsewhere, dollar/loonie is nearly 0.3% lower today, with the Canadian currency enjoying increased demand amid encouraging NAFTA headlines, even despite the plunge in oil prices. Media reports yesterday suggested that President Trump is pushing to announce a preliminary NAFTA deal within two weeks, reigniting hopes that these talks could bear fruit soon.

The antipodeans were higher, with both aussie/dollar and kiwi/dollar rising by 0.5% and 0.4% respectively. The RBA rate decision earlier on Tuesday was rather uneventful. The Bank remained on hold as expected and provided almost no fresh clues about its policy outlook. The reaction in the Australian currency was muted on the news, though it did surge a few hours later.

Day ahead : EU & UK deliver Markit Manufacturing PMIs; New Zealand waits for dairy prices

On Monday, liquidity is expected to return to normal levels as investors are all now back on their desks after a four-day weekend due to Easter Holidays. But after a noisy first quarter which included a significant sell-off in global stocks and strong demand for safe-havens, the second quarter does not seem to be easier either and investors are likely to play safely once again, at least for the moment. Fears over a global trade war did not fade out but escalated after China decided to retaliate to the US import tariffs on steel and aluminum on Sunday, with its tariffs on US food imports taking effect yesterday.

Now remains to see whether the US will continue the tit-for-tat game with China, putting the trade future of the Chinese-depended and commodity-linked economies such as Australia, Canada, and Brazil in danger. It is also worth mentioning that Friday's NFP might bring fresh volatility to the markets as analysts predict further improvement in the US labor market. An upbeat report, for example, could provide substantial support to the dollar which faced severe pressure since the beginning of the year, raising the odds for further monetary tightening by the Fed.

In equity markets, the persisting sell-off in tech stocks will be closely watched as well after Trump unleashed fresh warnings to Amazon.com over its pricing strategy and Apple said that it would use its own chips over Intel's components to build its products. Note that the next earning easing begins in two weeks.

Turning to today's economic releases, final Markit manufacturing PMIs out of the eurozone for the month of March are expected to come into view at 0800 GMT, with analysts sticking to their previous estimate of 56.6. If this is the case, then the measure will drop to the lowest level seen since July. A half an hour later, the UK will also see its March Markit/CIPS manufacturing PMIs and according to forecasts, the gauge is said to slow down from 55.2 to 54.7, reaching an eight-month low as well. In the US, total vehicle sales, another proxy for consumer spending, will attract attention at 1930 GMT, while in New Zealand, eyes will turn to global dairy prices delivered at a tentative time (Reuters expect the report to be issued around 1200 GMT).

In energy markets, the American Petroleum Institute will give an insight into the US crude oil stocks for the week ending March 30 at 2030 GMT.

As of today's, public appearances, the FOMC Board Governor, Lael Brainard will speak out of the US at 2030 GMT, while earlier in the eurozone, comments by the ECB executive member, Yves Mersch will also be in focus at 1430 GMT.

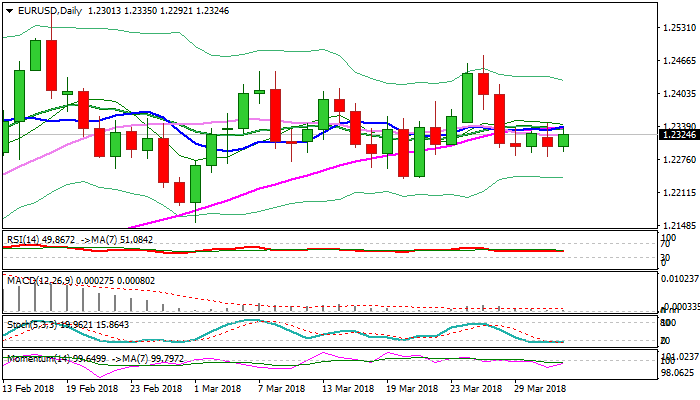

Technical Analysis – EURUSD bounce off from two-week lows but hold in a range

EURUSD made a big step towards a two-week low of 1.2281 yesterday but losses were short-lived, and the pair managed to rebound slightly above the 1.2300 key level today, remaining inside in a range started last week. The pair could maintain today's positive momentum in the short-term as the RSI is currently heading up towards its neutral threshold of 50 and the MACD is deviating above its red signal line in the four-hour chart.

However, if the eurozone Markit manufacturing PMIs beat expectations, embracing optimistic views on the bloc's industrial performance the market could gain further positive momentum, probably rising towards the 50-period simple moving average, which currently stands at 1.2348. Slightly above from here, resistance could be also found at the 38.2% Fibonacci of 1.2355 of the downleg from 1.2475 to 1.2281 before the door opens to the 50% Fibonacci of 1.2378.

However, if the data disappoint, the 20-period SMA a 1.2314 could offer nearby support, while steeper declines could also send prices back down to the two-week low of 1.2281.

BoJ Kuroda: There were internal discussions on stimulus exit

BoJ Governor Haruhiko Kuroda said they are "conducting various discussions" regarding stimulus exit "internally". However, it would confuse the markets by talking about the details now. And Kuroda said that would be inappropriate. In addition, Kuroda said the ETF buying program is "part of our monetary easing framework". For now, "there is still some distance to achieving our price target", we're not in a stage to debate the timing and means to (slow) ETF buying"

That's pretty much old stuffs we've heard from Kuroda countless times.

Eurozone PMI manufacturing at 56.6. Broad slowdown across “all nations”

Eurozone PMI manufacturing was finalized at 56.6 in March, unrevised, down from February's final reading of 58.6. It's also the biggest fall in the series since June 2011.  Markit noted broad slowdown across "all nations". And there is increased signs of "supply chain constraints".

Markit noted broad slowdown across "all nations". And there is increased signs of "supply chain constraints". Quote from the release:

Quote from the release:

Commenting on the final Manufacturing PMI data, Chris Williamson, Chief Business Economist at IHS Markit said:

- "March saw the biggest fall in the manufacturing PMI since June 2011 and the third successive slowing in the pace of expansion.

- "We should not be too worried by the fall in the PMI as some moderation in the pace of growth from the surge seen at the turn of the year was inevitable, not least because short-term capacity constraints limit the economy's ability to grow so quickly for long periods. This has been clearly evident in the recent lengthening of supply delivery times. Some of the slowdown has also been attributable to temporary factors such as bad weather.

- "However, the fact that business optimism about the coming year has slipped to a 15-month low suggests there are other factors that are now hitting factory order books. Export growth has more than halved since late last year, linked in part to the appreciation of the euro, and in some cases demand is being stymied by higher prices.

- "The overall pace of growth nevertheless remains robust by historical standards, with decent PMI readings seen in all countries, including Greece, to indicate a steady, broad-based expansion. Manufacturing should therefore make another substantial contribution to GDP growth in the first quarter, and the presence of sustained inflationary pressures will be welcomed by policymakers."

Also released, Germany manufacturing PMI was revised down to 58.2, from 58.4. France manufacturing PMI was revised up to 5.37, from 53.6. Italy manufacturing PMI dropped to 55.1 in March, down from 56.8 and missed expectation of 55.5.

Swiss retail sales dropped -0.2% yoy in February, better than expectation of -0.7% yoy. SVME PMI dropped to 60.3, down from 65.5 and missed expectation of 64.3.

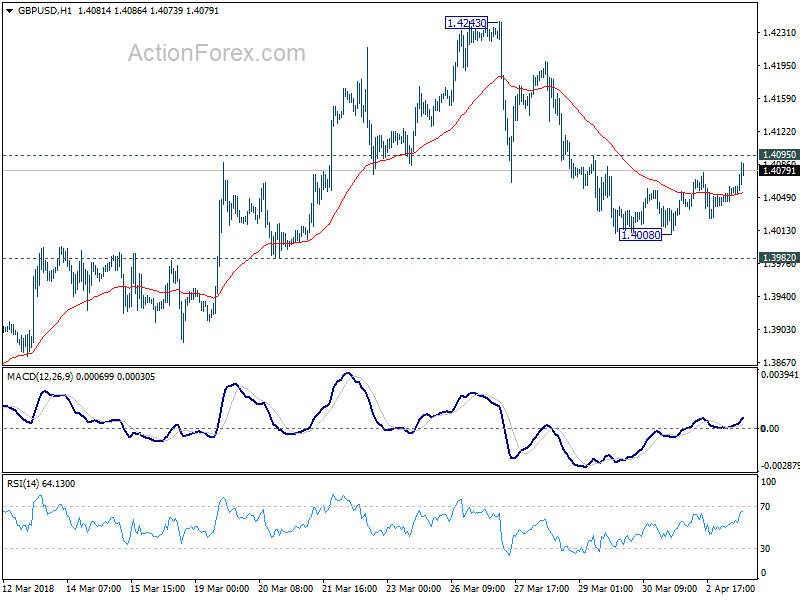

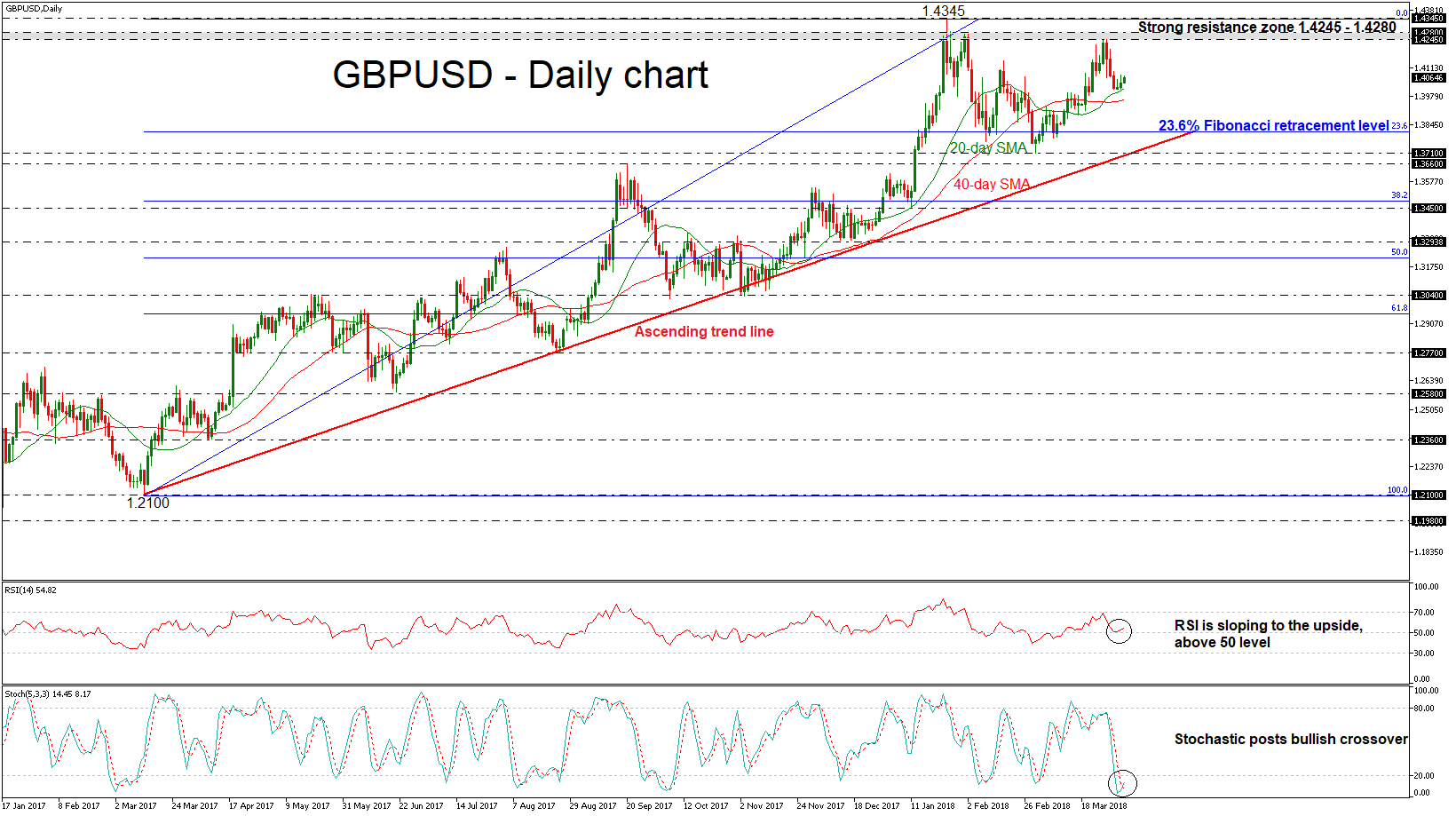

GBPUSD Pares Some Losses, Remains Above 20- And 40-Day SMAs

GBPUSD is trading marginally higher over the last couple of days following the rebound from the 1.4000 strong psychological level, which holds near the 20-day simple moving average (SMA). This week, cable is paring some of the previous week’s losses and is shifting the tendency back to bullish.

Having a look at the medium-term timeframe, the pair has been developing within an ascending tendency since March 2017 after touching the 1.2100 significant level.

Technically, the momentum indicators are confirming the recent upside potential move. The RSI indicator is holding in positive territory with stronger momentum than before and is sloping to the upside, while the stochastic oscillator completed a bullish crossover within the %K and %D lines in the oversold area, suggesting strong bullish move on price.

If the price continues to recover some losses, it could move towards the 1.4245 resistance level, taken from the high on March 26. A jump above this region could open the door for the next immediate resistance near 1.4280. Furthermore, breaking the aforementioned area could drive the buyers to the 19-month high of 1.4340.

In the wake of negative pressures and a slip below the 1.4000 handle and the 20- and 40-day SMAs could endorse the scenario for a bearish correction until the 23.6% Fibonacci retracement level near 1.3800 of the upleg from 1.2100 to 1.4345. The 20 and 40 SMAs are standing around 1.4010 and 1.3965 respectively at the time of writing. Following a drop below the Fibonacci level, a test of the ascending trend line near the 1.3710 support is possible.

Overall, GBPUSD has been bullish in the medium-term, while in near-term is expected to return back to gains after the soft downward correction.

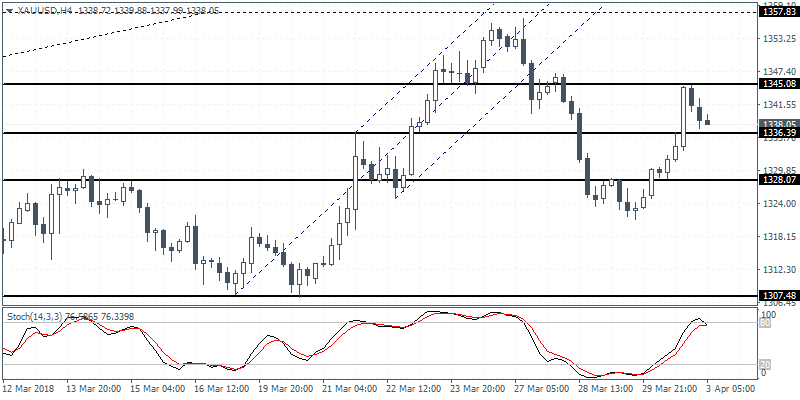

XAUUSD Intraday Analysis

XAUUSD (1338.05): Gold prices posted strong gains on the day following last Thursday's doji candlestick pattern. Price rallied close to the 1345 handle before giving up the gains promptly. We expect gold prices to resume the sideways range within 1345 and 1336 level with a breakout from this range likely to push gold prices back to the 1328 handle. Below this level, further declines could send gold prices falling toward the 1307 level of support.