Sample Category Title

USD/JPY Starting A Recovery Phase

USD/JPY is recovering from recent fall at 104.64, breaking hourly support at 105.29 (02/03/2018). Expected to strengthen along the 105.20 range. Hourly support and resistance are now given at 104.30 (08/11/2016 low) and 107.90 (14/02/2018 high). The bearish pattern started in January 2018 is maintained. The short-term technical structure suggests short-term increase.

We favor a long-term bearish bias. Support remains at 101.20 (09/11/2016 low). A gradual rise toward the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 101.20 (09/11/2016 low). The pair trades largely below its 200 DMA.

GBP/USD Stabilizing At The 1.41 Range

GBP/USD is having a consolidation phase along the 1.41 range following recent break of hourly resistance at 1.4151 (05/02/2018). Hourly support and resistance remain at 1.3765 (09/02/2018 low) and 1.4345 (25/01/2018 high). The short-term bullish pattern is maintained. The technical structure suggests continued shortterm sideways trading moves.

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline but the pair is moving to 2016 highs. Long-term support and resistance are given at 1.1841 (07/10/2017 low) and 1.5018 (24/06/2016 high).

EUR/USD Grinding Higher

EUR/USD is bouncing back following slight decline at 1.2286. Expected to increase along the 1.2360 range. Hourly support and resistance are given at 1.2165 (17/01/2018 low) and 1.2537 (31/01/2018 high). The technical structure suggests short-term increase.

In the longer term, the momentum is turning largely positive. We favor a continued bullish bias. Key resistance is holding at 1.2886 (15/10/2014 high) while strong support lies at 1.1554 (08/11/2017 low).

Trade War Hype, Asian Markets Slump Against Threats

Fade the Trade War Hype

Markets are on a knife-edge. US President Trumps imposing new trade sanctions against China has meaningfully increased the probability of a trade war. China is unlikely to site idly buy this time around. While at the EU summit, which is expected to discuss the US steel and aluminum tariffs. Asia markets were lower across the board while safe haven CHF and JPY were the only real gainers in FX. Yet, picking trend in FX remains complicated and markets tries to pick winners and losers from an extended protectionism. Countries with significant export exposure to the US such as MXN have declined yet, counties with solid domestic and lower reliance on exports such as India remains supportive.

Surprisingly in this corned generally beta sensitive ZAR has also improved (marginally helped by gold trade). There still expectations for a favorable outcome with limited escalations based on negotiations and in our view Trump his using issue for political gain rather than actual trade repositioning. This action gives Trump a nice bullet point for stump speeches on the 2020 campaign trail. But he gains little from sparking a full-blown trade war. In addition, countries still taking grievances to WTO indicated trade remain within a management framework. Despite the intensifying hype we see this as an opportunity to reload in EM long positions. ZAR, INR, PLN and MXN all look interesting for varied reasons.

Asian markets slump, as US trade sanctions against China intensify

Relationship between the two largest economies does not bode well. The Trump administration memorandum released on Thursday to impose 25% tariffs on Chinese imports worth USD 60 billion is worrying investors.

The first signs are already in place: Hong Kong Hang Seng sells off -2.95%, hampered by IT (-6%) while China CSI300 dropped by -2.87%. On Japan side, Nikkei 225 dropped by -4.51%, followed by Topix (-3.62%).

Chinese retaliation measures did not take long to come as Chinese trade ministry communicated its willingness to impose tariffs on US imports on pork, fruits, nuts, wine and other construction-related products. Additionally, China is planning to initiate infringement procedures to the World Trade Organization concerning recent introduced iron and aluminum tariffs. The outcome won’t probably get anywhere, everything is about baring the teeth and putting economic matter aside. It is only a matter of time until the situation will be cooling down.

In spite of current political tensions between both nations, we see the USD/CNY strengthening in the short-term, currently trading at 6.32 and expected to head along the 6.33 range.

Technical Outlook: AUDUSD – Bears Remain Fully In Play But Extended Consolidation Is To Precede Fresh Downside

The Aussie dollar bounced above 0.77 mark on Friday after strong fall on Thursday threatened of retesting new three-month low at 0.7672, posted on Wednesday.

Recovery attempts were so far limited (capped at 0.7730) as technicals are firmly bearish and reinforced by risk aversion on trade war fears, but bears lacked strength for stronger downside action so far.

Near-term price action remains in extended congestion between new low (0.7372) and broken 100SMA (0.7782) which rejected repeated attacks and is reinforced by formation of 10/100SMA bear-cross, which formed today.

Bears may stay on hold for some time before continuing, with limited upside actions to be capped by falling 10SMA (currently at 0.7768).

Eventual break lower to expose support at 0.7650 (Fibo 76.4% of 0.7500/0.8135 rally), loss of which would risk return to key 0.7500 support as no significant obstacles lays en-route.

To neutralize persisting bearish pressure, break and close above 100SMA is required.

Res: 0.7730, 0.7768, 0.7775, 0.7804

Sup: 0.7686, 0.7672, 0.7650, 0.7600

Trade War Taking Its Toll On Markets

- Another Rough Day in Store as US-China Trade War Ramps Up;

- Investors Flee For Safety Putting Particular Pressure on Japanese Stocks;

- Sterling Slips as May Hopes to Secure Transition Deal Approval From EU.

Another Rough Day in Store as US-China Trade War Ramps Up

For a person who's been obsessed with stock market gains since his election victory 16 months ago, US President Donald Trump doesn't appear too concerned about the impact his tariffs are having at the moment.

Trump may be prepared to add the European Union to the list of those that are temporarily exempt from the tariffs – with Canada, Mexico and Australia having been allowed similar exemptions – but that has barely cushioned the blow for investors.

Understandably, the prospect of a trade war between the world's two largest economies is not particularly desirable for investors. The global economy is finally starting the tick along nicely after a decade of efforts to repair the damage of the global financial crisis and the issues that followed and now we're potentially having to deal with an entirely self-inflicted and avoidable problem.

Trump's decision to impose tariffs on $60 billion of Chinese products will undoubtedly trigger a retaliation from the world's second largest economy and bring about a series of actions that could end in a full blown trade war. Already investors have made their feelings known about such measures, with the Dow and S&P 500 yesterday shedding nearly 3% alone and futures suggest it's going to be another rough session as we head into the weekend.

Investors Flee For Safety Putting Particular Pressure on Japanese Stocks

Europe and Asia were not immune to the news, with Chinese stocks unsurprisingly taking a particular beating overnight. Japanese stocks were also hit particularly hard, with the appreciation of the safe haven yet delivering a second blow to domestic stocks that rely heavily on exports.

Clearly investors aren't particularly keen to carry much risk into a weekend that could see tensions escalate between the two nations. Another safe haven, Gold, is up more than 1% on the day and more than 2% over the last couple of days as investors typically opt for the yellow metal in times of uncertainty.

Sterling Slips as May Hopes to Secure Transition Deal Approval From EU

As the EU prepares to vote on the Brexit transition deal that was agreed earlier in the week, the pound is trading a little lower in a potential sign of exhaustion for the currency. Even a clear indication from the Bank of England on Thursday that a rate hike is near – probably May – wasn't enough for the pound to hold onto gains for very long, potentially a sign that all the sterling-positive news is now fully priced in.

If the vote passes as expected today, it may not be enough to improve the fortunes for the pound but it will come as a relief to Theresa May who will see it as a significant step towards achieving a Brexit deal that, at times, has looked in doubt. The challenge for May now centres on forging a future relationship with the EU that needs to be wrapped up by the end of the year, with the next mini-deadline being June.

Despite unrest among some Brexiteers to the terms of the transition deal, May must be feeling pretty pleased with herself but now needs to convince businesses that she can be entrusted to deliver a deal that protects their interests also. If nothing is, in fact, agreed until everything is agreed, May will have to rely on trust to prevent businesses from putting contingency plans into practice, something some have already started doing regardless.

Risk Aversion Shifts Into A Higher Gear On Trade War Concerns

Notes/Observations

- Geopolitics increase the level of uncertainty; risk aversion sentiment reigns for now as trade fears and more US cabinet reshuffles surface

Asia:

- China's Commerce Ministry (MOFCOM) responded to US tariffs; proposed a list of 128 U.S. products as potential retaliation targets. The US goods, which had an import value of $3 billion in 2017, include wine, fresh fruit, dried fruit and nuts, steel pipes, modified ethanol, and ginseng. Those products could see a 15 percent duty, while a 25 percent tariff could be imposed on U.S. pork and recycled aluminum goods

- Japan Feb inflation at its highest since March 2015 with National CPI Y/Y: 1.5% v 1.5%e; CPI Ex-fresh food (core) Y/Y: 1.0% 1.0%e; CPI (Ex-fresh food/energy) Y/Y: 0.5% 0.5%e (Core CPI has risen for the 14 months

Europe:

- ECB Draghi said to provide European leaders with upbeat view on economy at EU summit. Cautioned that European governments planning to raise spending even as growth picks up posed a medium-term risk to the economy

Americas:

- White House: President Trump will sign $1.3T spending bill that averted a govt shutdown and funds Govt until Sept 30th. House earlier passed the spending bill (vote was 256-167); Senate passed $1.3T spending bill (final vote 65 to 32)

- President Trump announced $50B in tariffs over China intellectual property trade violations (as expected). Identified 1,300 product categories that might be covered by the new tariffs. Many products targeted would be those that China had sought to acquire advantage on via forced technology transfers from US companies. Tariffs specifics to be published by USTR within 15 days; industry to get 30 day comment period

- US noted that tariffs on steel and aluminum imports from the following countries were suspended until May 1, 2018, pending discussions of satisfactory long-term alternative means to address the threatened impairment to U.S. national security: Argentina; Australia; Brazil; Canada; Mexico; the member countries of the European Union; and South Korea

- Trump Administration National Security Adviser McMaster to resign; to be replaced by Bush Admin official John Bolton

Economic Data:

- (DK) Denmark Feb Retail Sales M/M: 0.5% v 0.2%e; Y/Y: 1.7% v 1.6% prior - (HU) Hungary Q4 Current Account: €0.2B v €0.9Be

- (CN) Weekly Shanghai copper inventories (SHFE): 307.4K v 297.0K tons prior

- (FR) France Q4 Final Wages Q/Q: 0.2% v 0.1%e - (TW) Taiwan Feb Industrial Production Y/Y: -1.9% v +1.7%e

- (ES) Spain Feb PPI M/M: 0.1% v 0.1% prior; Y/Y: 1.3% v 0.1% prior

- (NO) Norway Mar Unemployment Rate: 2.5% v 2.4%e

- (PL) Poland Feb Unemployment Rate: 6.8% v 6.8%e

Fixed Income Issuance:

- (ZA) South Africa sold total ZAR900M vs. ZAR900M indicated in I/L 2029, 2038 and 2050 bonds

- Corporate issuance saw equity fund outflows of $9.6B in w/e Mar 21st vs inflows of $20.4B in w/e Mar 14th

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

- Indices [Stoxx600 -1.3% at 364.4, FTSE -0.8% at 6899, DAX -1.6% at 11900, CAC-40 -1.6% at 5083, IBEX-35 -1.4% at 9356, FTSE MIB -1.6% at 22046 , SMI -0.9% at 8562, S&P 500 Futures -0.5%]

- Market Focal Points/Key Themes: European Indices trade lower across the board tracking US futures lower following sharp declines yesterday and sharp declines in Asia where the Nikkei dropped over 4% and Shanghai lower by over 3.5% following the formally announcement of Trump Tariffs on China. In the retail space Next trades higher after results and affirmed guidance, while Smith Group is a notable faller after a decline in Rev and profits. GlaxoSmithKline trades higher after dropping their pursuit for Pfizers Consumer Health Unit, with Indivior a sharp decliner as a US court sees no Alvogen patent infringement. Looking ahead earners include Destination XL.

Movers

- Consumer Discretionary [ Next [NXT.UK] +3% (Earnings) ] -Industrials [Henry Boot [BOOT.UK] +2.8% (Earnings)]

- Healthcare [ GSK [GSK.UK] +2.7% (Ends pursuit for Pfizer consumer unit), Indivior [INDV.UK] -5% (Responds to court ruling ANDA litigation: may have increased difficulty successfully defending its intellectual property against future ANDA filers) ]

- Technology [Smith Group [SMIN.UK] -10% (Earnings) ]

Speakers

- EU's Tusk: EU27 had adopted guidelines for EU-UK relationship after Brexit

- Northern League leader Salvini (euro-skeptic): Will not break up center right coalition

- Sweden Central Bank (Riksbank) Business Su vey: Economic boom continues, uncertainty on housing market continues to be evident

- Indonesia Central Bank's Zulverdi: To keep presence in FX market to maintain confidence

- Japan Fin Min Aso reiterated G20 stance on FX that excessive moves were bad for economies. Believed that recent yen currency moves did not reflect economic fundamental

- China State Think Tank researcher Zhang Ming: China could devalue the CNY currency if there was a full-scale trade war. Expected USD/CNY to trade between 6.2-6.7 in 2018

Currencies

- Safe haven flows dominated in the wake of US trade tariffs on China and the Chines retaliation measures. The EUR, JPY and CHF currencies were firmer as risk aversion swept across global equity markets as geopolitics had increased the level of uncertainty

- EUR/USD higher by 0.2% just above the 1.2330 area while USD/CHF was off by 0.2% around 0.9470.

- The USD/JPY pair hit a 16-month low of 104.64 in Asia. Japanese official made their round of verbal intervention stating that the price action was one-sided and did not reflect fundamentals. Fin Min noted that the BOJ could not purchase foreign bonds as it would be viewed as FX manipulation under current Japanese law.

Fixed Income

- Bund Futures trade 15 ticks higher at 158.94 through multiple resistances to yet another new recovery high, sustaining and reinforcing the bull theme from the mid-March push. Upside targets 159.75, while a return lower targets the158.25 level.

- Gilt futures trade at 123.15 up 24 ticks as risk off hits as government bonds climbed as investors sought safer assets. Support continues stands at 121.75 then 122.15, with upside resistance at 123.35 then 123.85.

- Friday's liquidity report showed Thursday's excess liquidity rose to €1.810T from €1.806T prior. Use of the marginal lending facility increased from €55M to €70M.

- Corporate issuance saw equity fund outflows of $9.6B in w/e Mar 21st vs inflows of $20.4B in w/e Mar 14th

Looking Ahead

- (RO) Romania Feb M3 Money Supply Y/Y: No est v 12.9% prior

- (EU) EU leaders conclude 2-day Summit in Brussels

- 06:00 (EU) Daily Euribor Fixing

- 06:00 (FR) France Debt Agency (AFT) announces upcoming auctions

- 06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to cut Key Rate 25bps to 7.50%

- 06:30 (IN) India Weekly Forex Reserves

- 07:00 (BR) Brazil Mar FGV Consumer Confidence: No est v 87.4 prior

- 07:00 (UK) DMO to sell combined £3.5B in 1-month, 3-month and 6-month Bills (£0.5B, £1.0B and £2.0B respectively)

- 07:30 (IS) Iceland to buy back Oct 2018 RIKH Bonds

- 07:45 (US) Daily Libor Fixing

- 08:00 (CL) Chile Feb PPI M/M: No est v -0.6% prior

- 08:00 (BR) Brazil Mid-Mar IBGE Inflation IPCA-15 M/M: 0.1%e v 0.4% prior; Y/Y: 2.8%e v 2.9% prior

- 08:00 (RU) Russia Central Bank Gov Nabiullina post rate decision press conference

- 08:10 (US) Fed's Bostic (2018 voter, dove) speaks on the Economic Outlook

- 08:30 (US) Feb Preliminary Durable Goods Orders: +1.6%e v -3.6% prior; Durables Ex-Transportation: 0.5%e v -0.3% prior, Capital Goods Orders (Non-defensive/ex-aircraft): +0.9%e v -0.3% prior, Capital Goods Shipment (Non-defense/ex-aircraft): +0.5%e v -0.1% prior

- 08:30 (CA) Canada Feb CPI M/M: 0.4%e v 0.7% prior; Y/Y: 1.9%e v 1.7% prior, CPI Core- Common Y/Y: 1.9%e v 1.8% prior, CPI Core- Median Y/Y: No est v 1.9% prior, CPI Core- Trim Y/Y: No est v 1.8% prior, Consumer Price Index: 132.4e v 131.7 prior

- 08:30 (CA) Canada Jan Retail Sales M/M: +1.1%e v -0.8% prior; Retail Sales Ex Auto M/M: +0.8%e v -1.8% prior

- 08:30 (UK) BOE’s Vlieghe

- 09:00 (IN) India announces upcoming Bill auction (held on Wed)

- 09:00 (ES) Spain Debt Agency (Tesoro) announces upcoming bond issuance (held on Thursdays)

- 09:05 (US) Baltic Dry Bulk Index

- 09:30 (BR) Brazil Feb Current Account Balance: +$0.5Be v -$4.3B prior; Foreign Direct Investment (FDI): $4.5Be v $6.5B prior

- 10:00 (US) Feb New Home Sales: 620Ke v 593K prior

- 10:00 (MX) Mexico Jan IGAE Economic Activity Index (Monthly GDP) Y/Y: 2.0%e v 1.1% prior

- 10:30 (US) Fed's Kashkari (dove, non-voter) speaks in moderated Q&A

- 10:30 (US) Fed Kaplan (non-voter, dove)

- 12:00 (EU) Potential Sovereign ratings after European close: (S&P on Belgium, Spain, Norway; Moody’s on South Africa, Poland; Fitch on Switzerland, Norway

- 13:00 (US) Weekly Baker Hughes Rig Count data

- 19:00 (US) Fed's Rosengren (moderate, non-voter)

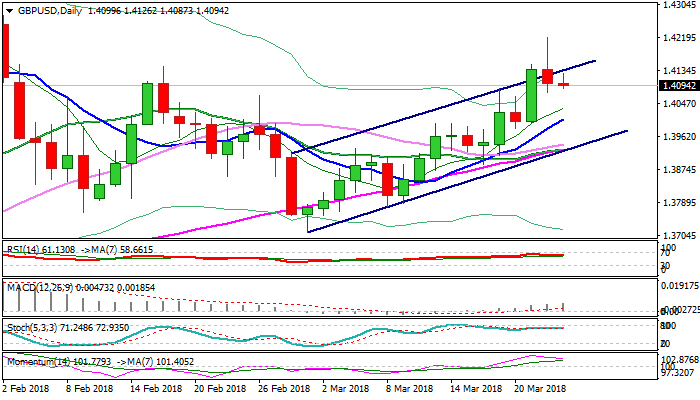

Technical Outlook: GBPUSD May Extend Pullback From New High At 1.4218 Before Bulls Resume

Cable is holding within tight range on Friday, after rallying to new 2 ½ month high at 1.4218 on Thursday but was unable to hold gains and ended day in red.

Return below cracked bull-channel’s upper boundary and Thursday’s bearish daily candle with long upper shadow, weigh and keep in play risk of deeper pullback.

Bullish daily techs and thick daily cloud continue to underpin and see dips as buying opportunities ahead of fresh upside action.

Initial bids lay at 1.4075/70 (Thursday’s low / 26 Feb former high) followed by rising daily Tenkan-sen (1.4046) which is expected to contain.

Key supports lay at 1.40 zone (daily cloud top / rising 10SMA), loss of which would sideline bulls for deeper correction of 1.3711/1.4218 recovery rally.

Res: 1.4137, 1.4150, 1.4195, 1.4218

Sup: 1.4070, 1.4046, 1.4000, 1.3945

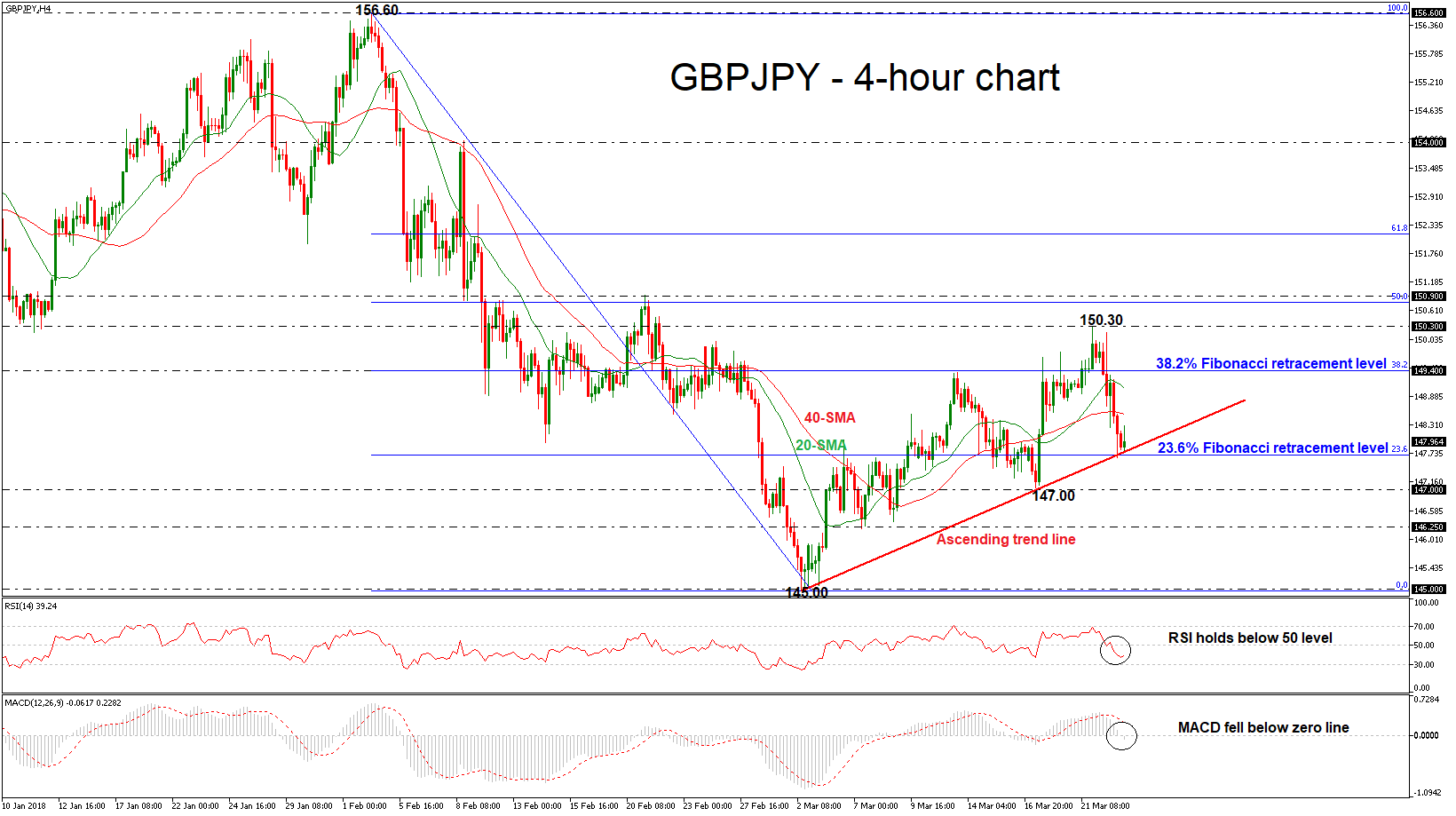

GBPJPY Builds Base Around 23.6% Fibonacci Mark And The Short-Term Ascending Trend Line

GBPJPY has reversed back down again after finding resistance at the one-month high of 150.30 achieved this week. The price plunged below the 38.2% Fibonacci retracement level of the downleg from the February 2 high of 156.60 to the March 2 low of 145.00.

Meanwhile, the price is re-challenging the 23.6% Fibonacci mark around 147.70, which holds near the short-term ascending trend line. The diagonal line has been standing since February.

Momentum indicators are pointing to a neutral to negative bias in the short-term with the RSI indicator bottoming out within the 30 and 50 level and the MACD oscillator turning negative below the trigger line, suggesting that a bearish movement is nearing again.

In the wake of negative pressures, the market could meet support near the 147.00 handle. A successful close below this level could see a retest of the previous low of 146.25, while in case of steeper declines, the pair could breach this barrier, diving towards the 145.00 psychological obstacle.

On the flip side, a move on the upside could see immediate resistance at the 40 and 20 simple moving averages in the 4-hour chart near 148.50 and 149.00 respectively. A stronger barrier could be found at the 38.2% Fibonacci mark of 149.40 since any strong violation of this price level could increase chances for further gains probably towards the 150.30 resistance.

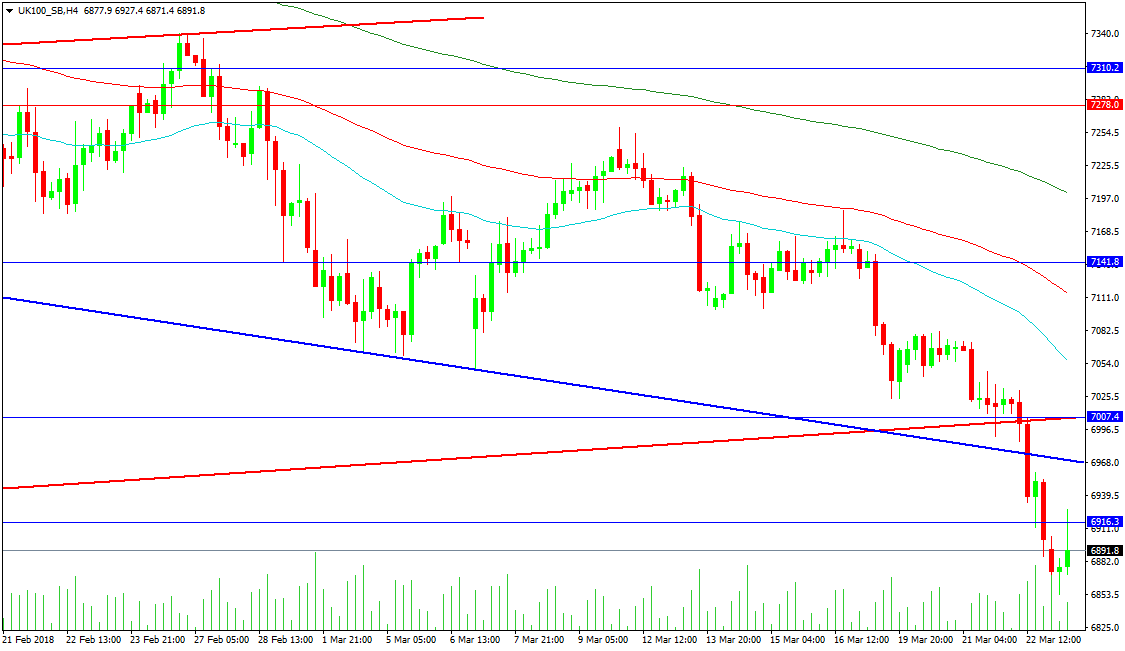

Forex Analysis: UK 100 And Silver Analysis

The UK 100 index has fallen below its February low at 6916.3, painting a bearish picture for 2018. The level was lost in the US session yesterday, and the index reached a low of 6835.7 overnight. Attempts to recover this morning are stalling above 6900.0. The increase in international trade tension has led to a fall in risk sentiment. The UK has been included in a list of exempted countries for the US trade tariffs due to its EU membership. Support below comes in at 6800.0 and 6765.8.

Resistance above comes from the trend lines broken in yesterday’s session, with the blue line at 6968.3 and the red line at 7007.4, a previous level of interest. The 4-hour moving averages are turning sharply lower, with the 50-period at 7055.0, the 100-period at 7115.0 and the 200-period at 7200.0. 7141.8 is the break down level and bulls would need to regain this area to wrest control from the bears.

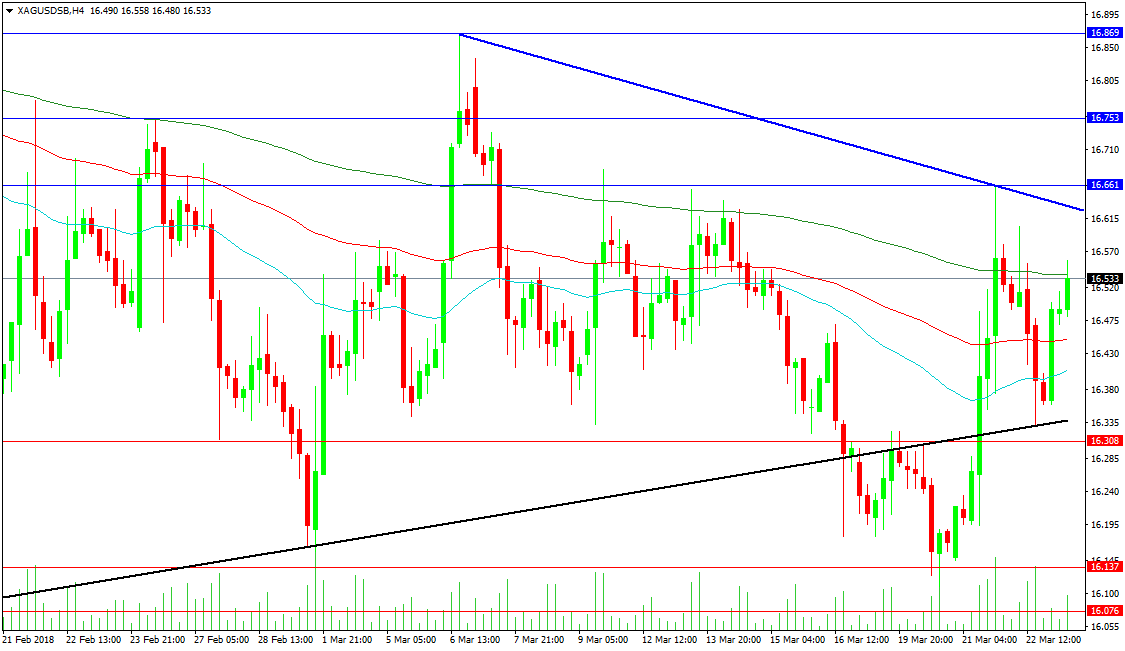

Silver

Silver has recovered to test its 200-period MA at 16.540, after finding support at the black trend line near 16.335 yesterday. This trend line has been breached on two occasions now but the move back higher on Wednesday presented excellent before and after touches, re-affirming its significance. Price reached up to the 16.661 level before retesting the black line and rebounding. This presents a bullish option for traders, with those missing out on the retest waiting for interaction with the falling blue two-touch trend line at 16.625, to see if price can rally further.

Support is found at the black trend line at 16.340, with the 16.308 level close below. Further support is located at 16.137 and 16.076. Resistance is at 16.661, with 16.753 and the most recent high at 16.869 above. The 17.000 level remains a target to aim for.