Sample Category Title

Dollar Bears in Charge; European Equities Tumble as Trade Fears Persist

Here are the latest developments in global markets:

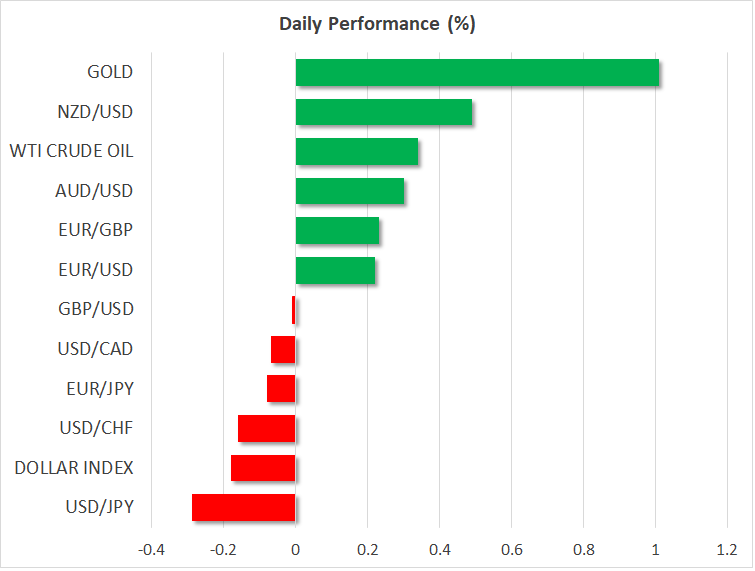

FOREX: The Japanese yen was moving sideways near a 16-month low of 104.60 reached during the Asian session, last seen at 104.98 (-0.27%), as financial markets were rattled by worries over rising US-China trade tensions. Moreover, Turkey's lira hit a record low of 4.03 to the dollar after the region failed to receive an exemption from the US import tariffs on Thursday. Dollar/lira surged 1.01% so far on Friday, paring some gains in the previous session. Pound/dollar changed hands at 1.4106 (+0.09%), reacting little to the confirmation of the 21-month Brexit transition offer by Donald Tusk, who chaired the EU summit in Brussels. Yesterday, the pair ended the day in the red despite an unexpected dissent vote on interest rates by BoE policymakers yesterday who decided to leave borrowing costs unchanged. Euro/dollar consolidated around 1.2334 during early European afternoon, remaining 0.24% up on the day. Dollar/loonie was also moving sideways around 1.2915 (-0.19%) after hitting a 1 ½-month low of 1.2828 earlier. Canada's inflation and retail sales reports are scheduled for release later today, shifting some focus to the loonie. Kiwi/dollar and aussie/dollar were last up by 0.33% and 0.55% respectively after Trump decided to exempt Australia and New Zealand from hefty import tariffs. Still, the economies were worried about the impact of trade restrictions on the Chinese economy since China is a major buyer of their exports.

STOCKS: Although Trump paused his punitive import tariffs on the EU on Thursday, European stocks tumbled on Friday at 1030 GMT amid concerns of a potential global trade war, with basic metals and technology sectors losing the most. The pan-European STOXX 600 dived by 1.19%, recording a one-year low, while the blue-chip Euro STOXX 50 plummeted by 1.47%. The British FTSE 100 was down by 0.69%, while the German DAX 30 and the Spanish IBEX 35 were heading lower by 1.58% and 1.16% respectively. US stock futures were pointing to a negative open.

COMMODITIES: Oil prices rose on Friday after the Saudi Arabian energy minister said that OPEC would keep coordinating supply cuts with non-member countries including Russia in 2019. WTI crude and Brent managed to recoup part of yesterday's gains, but they moved slightly lower from today's intraday highs. The former climbed to $64.52 a barrel (+0.33%), while the latter edged up to $69.12 a barrel (+0.19%). Gold rallied to $1,342 per ounce (+1.14%), hovering near one-month highs on the back of a weaker dollar. Also, silver jumped by 1.02% to $16.53 per ounce.

Day ahead: Trade developments in the spotlight; Canadian inflation pending

Day ahead: Trade developments in the spotlight; Canadian inflation pending

Looking ahead in the day, investors will continue to look for any updates on the trade front as Trump's signature on new import tariffs against China on Thursday and China's response on Friday to levy its own tariffs on US products increased speculation that the trade story is not likely to end anytime soon despite exemptions being made on several allies including the EU, Australia, and South Korea. A 30-day consultation period will follow once the list of products being targeted are published, while a 60-day deadline has been given to the Treasury Department to form restrictions aimed to prevent Chinese companies to acquire US tech-sensitive firms. Meanwhile, the US Trade Representative, Robert Lighthizer, had warned on Thursday that any retaliation from China could bring new actions by the US. Therefore, it would be interesting to see what the US reaction to China's threats would be. In case the US uses a tougher language, exasperating the trade turmoil, stock and FX markets could experience further downside pressures.

Developments in the White House would also be in focus after the replacement of the US National Security adviser, Herbert Mcmaster with the former ambassador to the UN in the Bush administration and a hawk on foreign policies, John Bolton, raised concerns over the US's relations with Iran and North Korea. Note that McMaster had previously backed the choice of using military forces against North Korea.

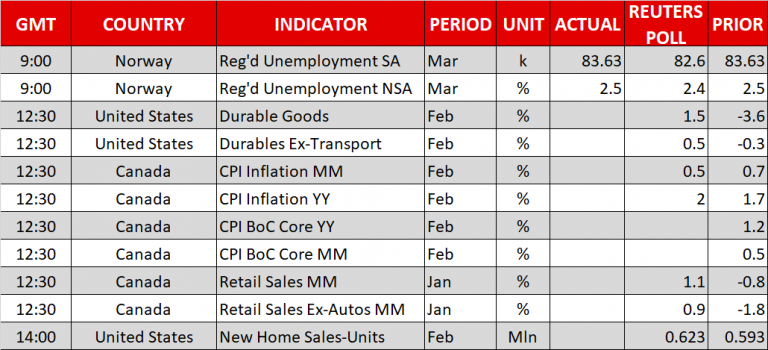

In terms of data releases, the calendar will feature US and Canadian figures later in the day. At 1230 GMT, traders will keep a close eye on Canadian consumer prices and retail sales. The headline inflation is expected to have risen by 2.0% year-on-year in February compared to 1.7% seen in the previous month, bringing some good news to BoC policymakers who are hoping for the measure to reach the midpoint of their 1-3.0% target. Growth in retail sales is also anticipated to have improved in January, with the gauge said to have surged by 1.1% month-on-month after a fall of 0.8% in December. If the data appear better-than-expected, the loonie could extend gains as this could signal further rate hikes by the BoC.

Regarding the US data, US durable goods orders, published at the same time, are likely to have strengthened in February as well. Particularly, analysts believe that new orders for long-lasting manufacturing products have rebounded by 1.5% m/m after tumbling by 3.6% in January. A few hours later, new home sales due at 1400 GMT could show an increase of 0.623 million units from a rise of 0.593 million in the preceding month.

In energy markets, Baker Hughes will report on the number of active US oil rig count.

Turning to today's public appearances, Atlanta Fed President Raphael Bostic (voter) will deliver remarks at 1210 GMT, while 20 minutes later at 1230 GMT, we will hear from BoE MPC member Gertjan Vlieghe. Then at 1430 GMT, Minneapolis Fed President Neel Kashkari (non-voter) will step up to the rostrum, followed by Dallas Fed President Robert Kaplan (non-voter) at 1530 GMT.

USD/CAD – Canadian Dollar Ticks Higher

The Canadian dollar has posted small gains in the Friday session. Currently, USD/CAD is trading at 1.2919, down 0.14% on the day. On the release front, it’s a busy day on both sides of the border. Canada will release key consumer spending and inflation data. CPI is expected to fall to 0.4%. Retail Sales and Core Retail Sales are expected to post gains of 0.9% and 1.1% respectively, after both posted declines in the previous releases. In the US, durable goods reports are expected to rebound after posting declines in January. Core Durable Goods Orders is expected to rise 0.5%, and durable goods orders is forecast to climb 1.6%. On the housing front, New Home Sales is expected to improve to 621 thousand.

Canada is heavily dependent on exports, so the specter of a global trade war could be disastrous for the Canadian economy. There is considerable worry in Ottawa, as US President Trump seems intent on “righting wrongs” in US trade balances by applying the hedge hammer of tariffs. On Thursday, US President Trump slapped 25% tariffs on up to $60 billion worth of Chinese imports on Thursday. For its part, China wasted no time in threatening to retaliate, saying it was planning to impose tariffs on 128 US products, which amounted to $3 billion in imports. The tariffs directed against China come on the heels of tariffs on steel imports coming into the US, although the US has exempted Canada and some other countries. There is serious concern that these moves could ignite a global trade war, and a downturn in the Chinese economy could spread and cause a global recession.

A major headache for Canadian policymakers is the NAFTA trade agreement, which the US has insisted at reopening and inserting more favorable terms for the US. Otherwise, the Trump administration has threatened to withdraw from NAFTA. The specter of the free-trade agreement being cancelled has weighed on the Canadian dollar for months. However, there was good news this week as US has dropped its demand that vehicles produced in Canada or Mexico, destined to the US, contain a minimum of 50% US content. This demand was one of the key sticking points in the negotiations, and its removal should speed up talks on the renegotiated NAFTA agreement. The positive shift in negotiations has boosted the Canadian currency.

As widely expected, the Federal Reserve raised rates by a quarter-point on Wednesday, bringing the benchmark rate to a range between 1.50% and 1.75%. The markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and if Fed policymakers reiterate positive sentiment towards the economy, could push the US dollar to higher ground.

EU adopted Brexit negotiation guidelines

EU leaders formally approved the guidelines for the negotiation of future relations with the UK after Brexit in the EU summit today. Only a few minutes were taken for the approval. While symbolic, the approval now clears the way to move one to the next phase of Brexit negotiation. And the process will likely gain momentum from now on. Brexit negotiator Michel Barnier will now talk directly to the US about future relationship. The target is to reach a broad political agreement by October.

The 7-page document can be found here.

UK Prime Minister Theresa May said that "I believe we are approaching this with a spirit of cooperation, a spirit of opportunity for the future as well, and we will now be sitting down and determining those workable solutions for Northern Ireland, but also for our future security partnership and economic partnership." And, she added that "the best interest of both the UK and the EU that we get a deal that actually is in the interests of both."

Stiglitz to China: Don’t appease to bully Trump

Nobel prize-winning economist Joseph Stiglitz commented on the intensification of trade war between US an China. He pointed out that China is "sitting on $3 trillion of reserves that it can use to help those adversely affected. On the other hand, in the US, "we don't have an economic framework that is able to respond to the particular places that will be affected by a trade war. Also, he pointed out that "the fiscal resources of the United States are strained."

In addition, Stiglitz also said that "when you have a bully like Trump, it would not be good to respond in a weak way." He added that "we know about appeasement from Munich. It's a different kind of a war but in a trade war appeasement could lead to more and more demands."

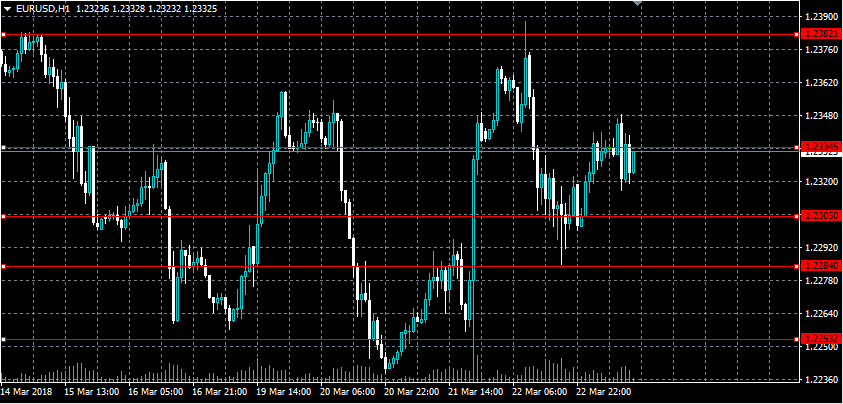

EURUSD Retains Bullish Bias Above 1.2305 Level

The euro is attempting to regain bullish trading momentum against the greenback, after retreating sharply from the 1.2382 resistance level on heightened risk-aversion in financial markets. The EURUSD pair is currently trading around the 1.2334 resistance level, after finding strong buying demand from the 1.2280 region yesterday. Moving into the U.S session, traders look to the release of U.S Durable Good Orders and New home Sales data.

The EURUSD pair retains a bullish intraday bias whilst price-action holds above the 1.2305 level, key resistance is now found at the 1.2348 and 1.2382 levels.

Should the EURUSD pair slip below the 1.2305 support level for a sustained period, a further decline towards the 1.2284 and 1.2253 levels remains possible.

USDJPY Next Downleg Below 104.64 Level

The U.S dollar is consolidating below the 105.00 handle against the Japanese yen, after earlier slumping to its lowest trading level since, November 2016. The USDJPY has so far found intraday support from the 104.64 level, although the pair remains under strong bearish pressure whilst trading below the 105.24 level. Moving into Friday’s U.S session, falling global equity markets and declining U.S Treasury bond-yields are currently weighing on overall U.S dollar sentiment.

The USDJPY pair is likely to see further declines below the 104.60 level, key long-term technical support is found at the 104.00 and 103.60 levels.

Should the USDJPY pair start to trade above the 105.24 level for a sustained basis, buyers may begin to target the 105.50 and 106.00 resistance levels.

BTC: Recovery Phase Stops

BitCoin after the recent recovery, yesterday the market showed with daily close a sell signal.

As shown below on the daily chart. Prices could not close above the resistance are of 9200. However, it created a sell signal which mean the prices would continue the mid-term down trend if the prices did not close above the mentioned levels.

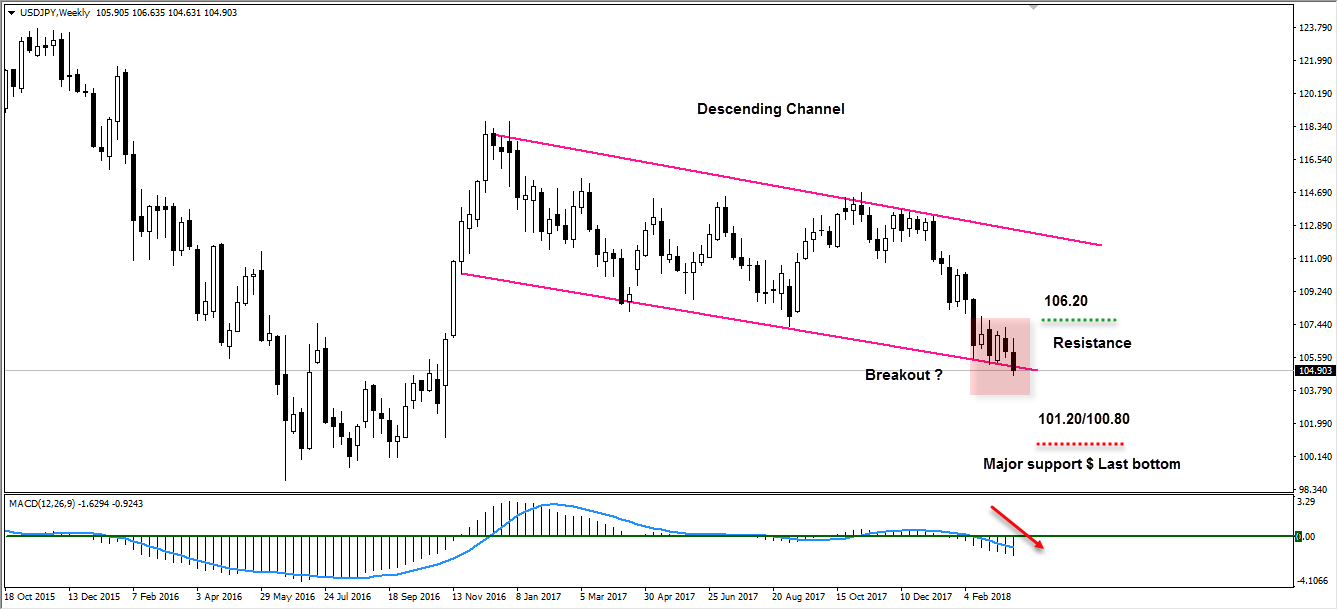

USDJPY: Exiting Descending Channel

USDJPY was trading on the bottom of the descending channel for the last couple of weeks, However, we notice an increasing selling pressure which pushing the prices to break this channel.

As shown on the weekly chart below, markets are successfully breaking the descending channel. So, if the prices did not bounce back to 106.20 levels again we would see a downtrend targeting the support area at 101.20/100.80.

DAX Slides As US Tariffs On China Spook Markets

The DAX index has recorded sharp losses for a second straight session. Currently, the DAX is trading at 11,912, down 1.55% on the day. On the release front, there are no German or eurozone releases on the calendar.

It's been a tough week for global stock markets, and the DAX has not been immune from the tumble. The DAX has shed 3.5% percent of its value, as investor risk appetite has waned after US President Trump slapped 25% tariffs on up to $60 billion worth of Chinese imports on Thursday. Trump said that the tariffs, which will take effect within 15 days, are needed to address the massive trade deficit with China, which stands at $375 billion. For its part, China wasted no time in threatening to retaliate, saying it was planning to impose tariffs on 128 US products, which amounted to $3 billion in imports. The tariffs directed against China come on the heels of tariffs on steel imports coming into the US, although the US has promised exemptions to the EU and some other countries. There is serious concern that these moves could ignite a global trade war, and a downturn in the Chinese economy could spread and cause a global recession. Predictably, US stock markets were down sharply on Thursday, and the gloom has spread to European stock markets in the Friday session.

The German business sector continues to have strong confidence in the German economy, but there is concern about possible headwinds due to recent tariffs imposed by the Trump administration. The German Ifo Business Climate report dipped to 114.7 in March, which matched the forecast. However, this marked a second straight drop, and was the lowest reading in 11 months. The report attributed lower business morale to concerns that tariffs could hurt transatlantic trade, as well as the negative impact of a stronger euro. On the bright side, tax reform in the US and the economic rebound in the eurozone have increased the demand for German goods and services.

Euro Steady, US Durable Goods Reports Next

EUR/USD has moved higher in the Friday session, erasing most of the gains seen on Thursday. Currently, the pair is trading at 1.2325, up 0.18% on the day. In economic news, there are no eurozone events on the schedule. In the US, durable goods reports are expected to rebound after posting declines in January. Core Durable Goods Orders is expected to rise 0.5%, and durable goods orders is forecast to climb 1.6%. On the housing front, New Home Sales is expected to improve to 621 thousand.

As widely expected, the Fed raised rates by a quarter-point on Wednesday, marking the first rate hike in 2018. The markets were looking for any clues with regard to the pace of rate hikes in 2018 – currently the Fed is projecting three hikes, but a robust US economy could push the Fed to press the rate trigger four times. The rate statement did not directly address the issue, but there was a refreshing lack of Fedspeak from policymakers, who said that “the economic outlook has strengthened in recent months”. This phrase has not been used in previous rate statements, and underscores a more hawkish stance from the Fed. The markets are expecting the Fed not to skip a beat, with the CME Group pricing another rate hike in May at 96%. This could translate into gains for the US dollar, at the expense of the euro and other major currencies.

The business sector continues to have strong confidence in the German economy, but there is concern about possible headwinds due to recent tariffs imposed by the Trump administration. The German Ifo Business Climate report dipped to 114.7 in March, which matched the forecast. However, this marked a second straight drop, and was the lowest reading in 11 months. The report attributed lower business morale to concerns that tariffs could hurt transatlantic trade, as well as the negative impact of a stronger euro. On the bright side, tax reform in the US and the economic rebound in the eurozone have increased the demand for German goods and services.