Sample Category Title

Canada: Retail Sales Edge up in January

Canadian retail sales rose 0.3% in January, following a sharp drop in December. Price increases were behind much of the gain; in real terms, sales edged up by 0.1%.

Sales were up in two thirds of the industries, with electronics and appliance stores (+4.0%), furniture and home furnishing stores (+3.4%) and general merchandise stores (+2.3%) leading the way. In contrast, sales at motor vehicle and parts dealers declined during the month due to a drop in new and used vehicle sales.

Regionally, the performance was mixed, with sales rising in six provinces. Manitoba (+2.7%), PEI (+1.7%) and Ontario (+1.2%) recorded the largest gains, while sales in B.C. (-1.0%) fell for a third straight month.

Key Implications

Retail sales were up in January, but the growth in volumes does little to offset the sharp drop recorded at the end of 2017, and reinforces our view that the Canadian economy got off to a soft start this year. Overall real GDP growth for the first quarter is expected to come in at around 1.4%.

Going forward, household spending should be supported by solid income and job gains, but rising interest rates and a cooling in the housing market will provide some offset. As such, consumer spending is expected to decelerate from last year's hearty pace this year.

While the inflation data reported this morning may give them pause, a soft pace of economic growth means that the Bank of Canada is likely to maintain a cautious stance to rate hikes. It has clearly stated that future decisions will be data dependent, and today's report will do little to move the needle – especially given weakness in other indicators so far this year. At this point, we don't expect the Bank to move off the sidelines before July.

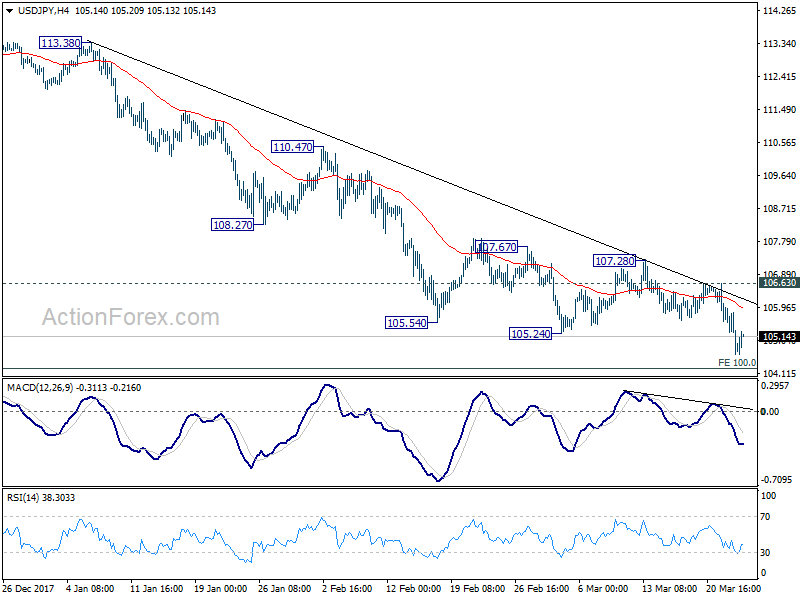

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 104.99; (P) 105.53; (R1) 105.82; More...

Intraday bias in USD/JPY remains on the downside despite today's recovery. Prior break of 105.24 support confirms resumption of decline from 114.73. Such fall is part of the whole pattern from 118.65. Intraday bias now stays on the downside for 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. Sustained break there will pave the way to 98.97 (2016 low). On the upside, break of 106.63 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish in case of recovery.

In the bigger picture, medium term down trend from 118.65 2016 high is still in progress and extending. Build up in downside momentum argues that it might be extending the whole corrective pattern from 125.85 (2015 high). 100% projection of 118.65 to 108.12 from 114.73 at 104.20 will be a key level to watch as firm break there could bring downside acceleration. And in that case, 98.97 key support level (2016 low) would at least be breached. This bearish case will now be favored as long as 108.12 support turned resistance holds.

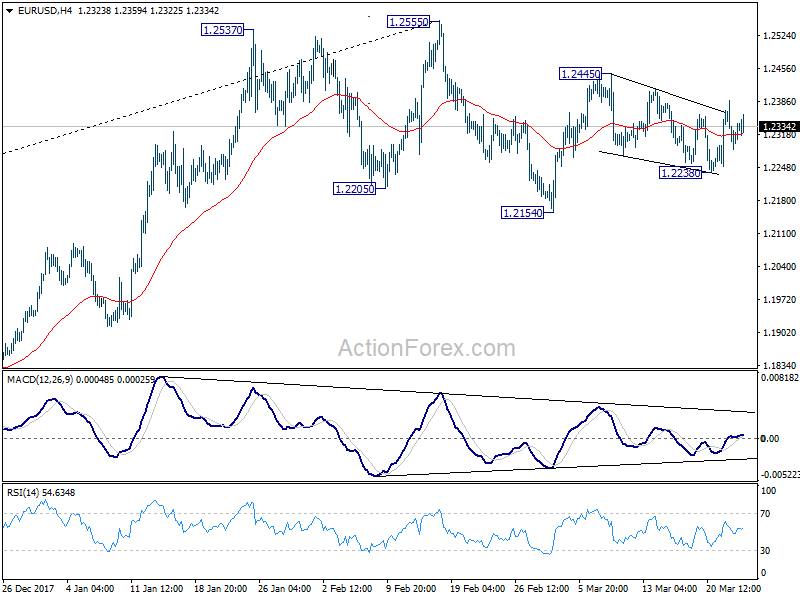

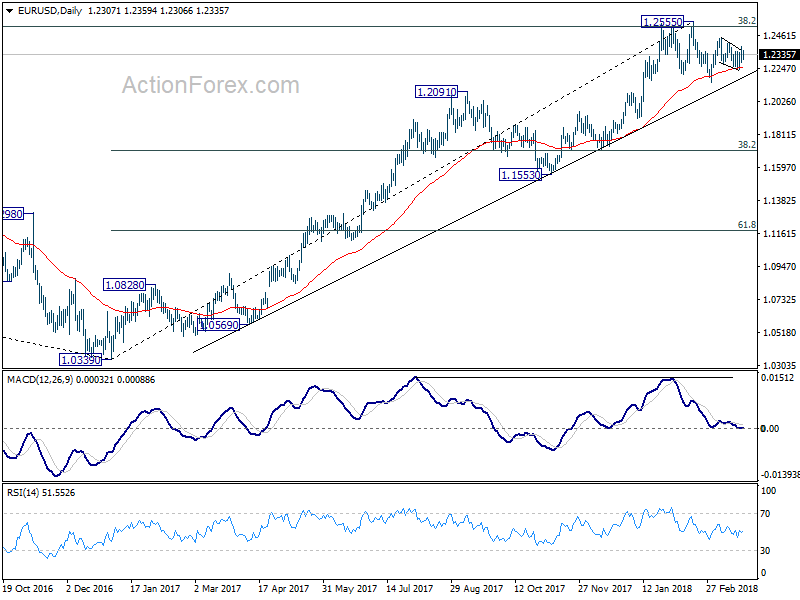

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2261; (P) 1.2324 (R1) 1.2364; More....

No change in EUR/USD's outlook. Price actions from 1.2445 is a corrective pattern in form of falling wedge. And, it might be completed at 1.2238 already. Further rise should be seen to 1.2445 first. Break will resume whole rebound from 1.2154 and target 1.2555 high, which is close to 1.2516 key long term fibonacci level. On the downside, however, firm break of 1.2238 will turn bias back to the downside, to resume the fall from 1.2555 through 1.2154.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. Firm break of 1.1553 support will add more medium term bearishness. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

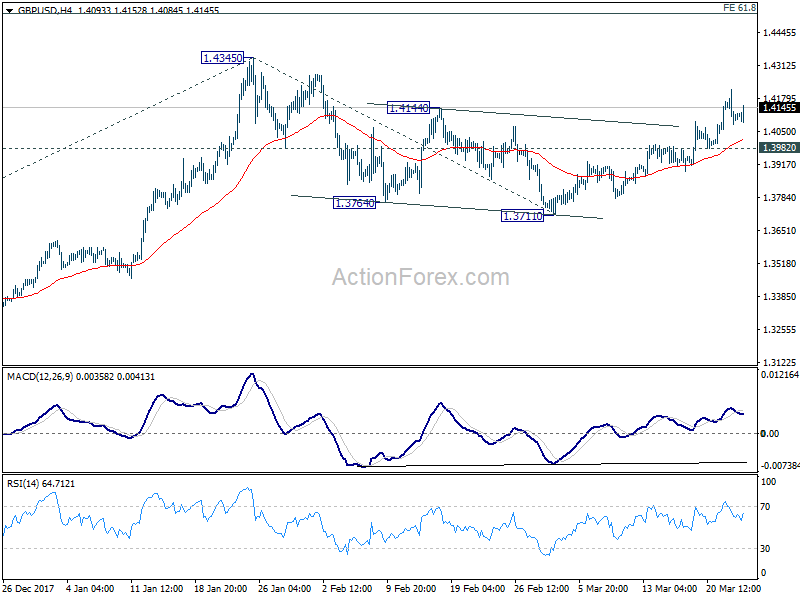

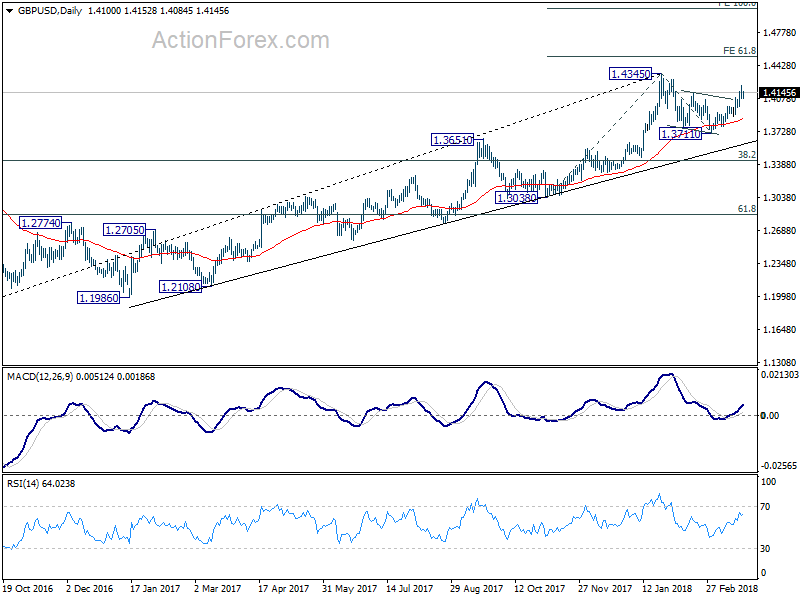

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4041; (P) 1.4128; (R1) 1.4181; More....

With 1.3982 minor support intact, further rise is expected in GBP/USD to retest 1.4345. Break there will resume larger up trend and target 61.8% projection of 1.3038 to 1.4345 from 1.3711 at 1.4519 next. Nonetheless, break of 1.3982 will argue that rebound from 1.3711 has completed. And, intraday bias will be turned back to the downside for 1.3711 support and possibly below, to extend the corrective pattern from 1.4345.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Which American Industries Are Vulnerable to Tariff Retaliation?

The aircraft, chemicals and machinery industries have significant exposure to exports, especially to the European Union. A trade war, should one develop, could have a meaningful effect on the U.S. economy.

Some Industries Have Significant Exposure to Exports

President Trump announced on March 8 that his administration would levy 25 percent tariffs on steel imports and 10 percent tariffs on aluminum imports, and he followed up these actions on March 22 by announcing tariffs worth at least $50 billion on imports exclusively from China. China has responded with some minor actions of its own, but it could do much more. The administration has temporarily excluded the European Union (EU) from the steel and aluminum tariffs, but those countries could eventually retaliate if tariffs are instated on them. Which U.S. industries would be most vulnerable to retaliatory steps?

We start by looking at the top export markets for the United States. As shown in the top chart, the EU and Canada were the top export markets for the United States in 2017. (All 28 EU countries have the same trade policy so we treat them collectively as a single economy.) Mexico is a close third, and China and Japan round out the top five. We next calculate the percentage of industry value added that is accounted for by exports to America's most important trading partners outside of NAFTA. (The administration has exempted Canada and Mexico from the steel and aluminum tariffs, so we remove them from the list because they have no grounds for retaliation at this point.) As shown in the middle chart, about 30 percent of value added in the "other transport equipment" industry (largely the aircraft industry) is accounted for by exports to America's top export markets outside of NAFTA. The chart also makes it clear that exports to the EU are an important component of the value added that is generated in that industry. Meaningful proportions of value added in the chemicals, machinery & equipment rental, computer and machinery & equipment industries are also accounted for by exports to these important trading partners. In most cases, these industries also have meaningful exposure to exports to the EU, which reflects the status of the EU as one of America's most important trading partners.

Clearly, retaliation that focused on the industries shown in the middle chart could have significant detrimental effects on those individual industries. But how big would the overall macroeconomic effect be? The bottom chart shows value added contributions of the industries shown in the middle chart. For example, the "other transport equipment" industry, which we have determined would be most vulnerable to foreign retaliation, accounts for only 0.6 percent of total value added in the U.S. economy. Retaliation that focused solely on this industry would not have a meaningful effect on the macro U.S. economy. But, foreign governments do not need to limit their retaliation to just this one industry. The 10 industries that are shown in the bottom two charts account for roughly 10 percent of the value added in the economy. An all-out trade war, should one develop, could have a noticeable effect on the U.S. economy.

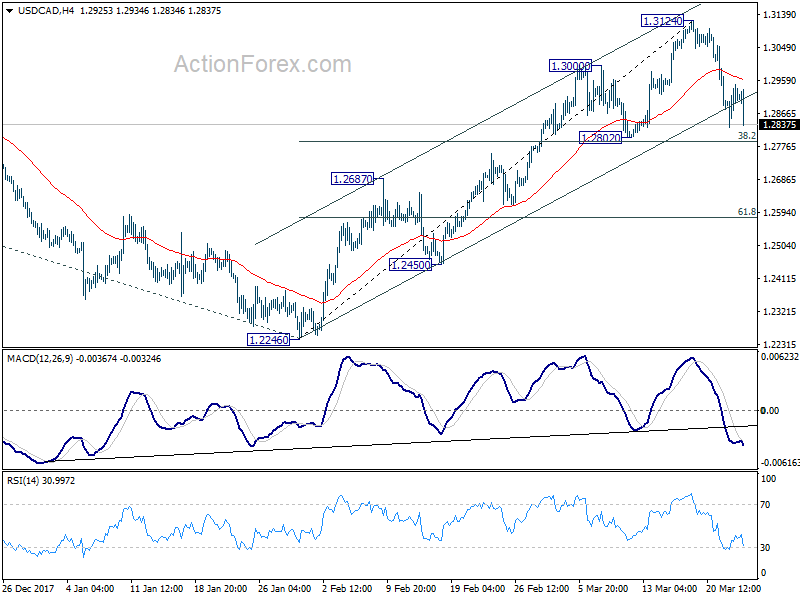

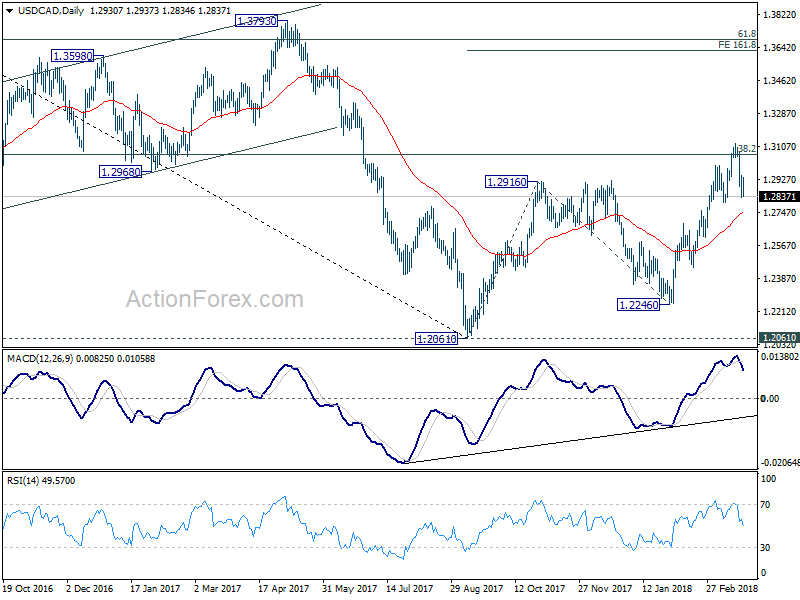

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2863; (P) 1.2905; (R1) 1.2982; More....

USD/CAD drops sharply in early US session. But for the moment, it's still staying above 1.2802 cluster support zone (38.2% retracement of 1.2246 to 1.3124 at 1.2789). Price actions from 1.3124 are viewed as a near term pull back only. And intraday bias stays neutral, and bullish outlook is unchanged. That is, further rally is expected. On the upside, break of 1.3124 will extend recent rally to 161.8% projection of 1.2061 to 1.2916 from 1.2246 at 1.3629 next. However, firm break of 1.2789/2802 will raise the chance of rejection by 1.3065 medium term fibonacci level and bring deeper fall to 55 day EMA (now at 1.2741).

In the bigger picture, we're favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061 as a correction, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Sustained break of 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will pave the way to 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2802 support holds. However, rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Canadian Dollar Lifted by CPI, Markets Stabilizing after Panic Selloff

After steep selloff in the Asian markets, sentiments stabilized mildly in European markets. At the time of writing, DAX is trading down -1.45%, CAC down -1.2 and FTSE down only -0.25%. US futures also point to a flat open, and stocks may recover from yesterday's panic selloff. In the currency markets, Canadian Dollar is the strongest one for today as boosted by stronger than expected consumer inflation reading. It's followed by Kiwi and Aussie as sentiments stabilized. Yen, on the other hand is paring back some gains. Meanwhile, Dollar continues to trade as the weakest one for the day, and the week, shrugging off solid durable goods orders.

Canada CPI gives CAD another lift

Canadian Dollar has been strong this week ever since the news that US dropped the toughest protectionist demand in NAFTA negotiations. Today's stronger than expected inflation data gives the Loonie another lift. CPI rose 0.6% mom, 2.2% yoy in February, beat expectation of 0.5% mom, 2.0% yoy. Annual rate also accelerated from prior month's 1.7% yoy. CPI core common accelerated to 1.9% yoy, up from 1.8% yoy. CPI core media rose to 2.1% yoy, up from 1.9% yoy. CPI core trimmed rose to 2.1% yoy, up from 1.8% yoy. retail sales was a disappointment but market shrugged that off. Canada retail sales rose 0.3% versus expectation of 1.2% mom in January. Ex-transport order, though, met expectation and rose 0.9% mom. Overall, recent developments are raising the chance of another BoC rate hike within the first half.

Fed Bostic: Fed at or near objectives, supports further rate hikes

Atlanta Fed President Raphael Bostic sounds upbeat in his prepared speech for Knoxville Economic Forum. With six month core inflation at 2%, and unemployment rate at 4.1%, he considered Fed is "at or near the sustainable employment and inflation objectives." Regarding interest rate, he said that "if the economy evolves roughly as I suspect, I will likely support further increases over the course of the year." And, "with the economy operating near its potential and inflation finally approaching the long-run target, it is appropriate, in my opinion, for monetary policy to be moving toward a more neutral stance."

Released from US, durable goods orders rose 3.1% in February, above expectation of 1.7%. Ex-transport orders rose 1.2% versus expectation of 0.5%.

Following yesterday's Section 301 tariffs targeted at China, US announced temporary suspension on some countries for the steel and aluminum tariffs. In short, the countries that are temporarily exempted include Argentina, Australia, Brazil, Canada, Mexico, EU and South Korea. They added up to 52.7% of US steel import in 2017. But two of US closest allies, Japan and Taiwan, are not in the exemption list.

China responds to US section 301 tariffs: Don't drag trade relations to a dangerous place

There are two responses from China today regarding recent protectionist trade measures by the US. Firstly, China's Ministry of Commerce announced measures countering the steel and aluminum tariffs. The MOFCOM proposed a list of 128 US imports with total value at over USD 3b in 2017. A 15% tariff will be imposed on the first group including wines, fresh fruit, dried fruit and nuts, steel pipes, modified ethanol, and ginseng. Then a 25% tariff could be imposed on the second group, including pork and recycled aluminium goods if both sides failed to reach a resolution through talks. China also said it could take legal action regarding the steel tariffs under WTO rules.

Secondly, China responded to the US Section 301 tariffs, targeted it, with a statement but without counter measures yet. The MOFCOM said it "doesn't hope to be in a trade war, but is not afraid of engaging in one." And, "China hopes the United States will pull back from the brink, make prudent decisions, and avoid dragging bilateral trade relations to a dangerous place." An MOFCOM spokesperson also said "we firmly oppose" to the section 301 tariffs. He added that "it is a typical unilateral and protectionist practice." And China is "fully prepared to firmly defend our interests." And have "have confidence and capability in dealing with any challenges." This is the response to the tariff on USD 50-60b) of China import.

Stiglitz to China: Don't appease to bully Trump

Nobel prize-winning economist Joseph Stiglitz commented on the intensification of trade war between US an China. He pointed out that China is "sitting on $3 trillion of reserves that it can use to help those adversely affected. On the other hand, in the US, "we don't have an economic framework that is able to respond to the particular places that will be affected by a trade war. Also, he pointed out that "the fiscal resources of the United States are strained."

In addition, Stiglitz also said that "when you have a bully like Trump, it would not be good to respond in a weak way." He added that "we know about appeasement from Munich. It's a different kind of a war but in a trade war appeasement could lead to more and more demands."

EU adopted Brexit negotiation guidelines

EU leaders formally approved the guidelines for the negotiation of future relations with the UK after Brexit in the EU summit today. Only a few minutes were taken for the approval. While symbolic, the approval now clears the way to move one to the next phase of Brexit negotiation. And the process will likely gain momentum from now on. Brexit negotiator Michel Barnier will now talk directly to the US about future relationship. The target is to reach a broad political agreement by October. The 7-page document can be found here.

UK Prime Minister Theresa May said that "I believe we are approaching this with a spirit of cooperation, a spirit of opportunity for the future as well, and we will now be sitting down and determining those workable solutions for Northern Ireland, but also for our future security partnership and economic partnership." And, she added that "the best interest of both the UK and the EU that we get a deal that actually is in the interests of both."

Japan CPI core hit 1% for the first time since 2014

Japan national CPI core accelerated to 1.0% yoy in February, up from 0.9% yoy and met expectation. That's also the first time it hits 1% level since August 2014. The so called core-core CPI, CPI excluding fresh food and energy, rose to 0.5% yoy.

Newly appointed BoJ deputy governor Masazumi Wakatabe said in the parliament that the reading, especially the core-core CPI, showed that Japanese inflation expectation remain weak. He noted that "when compared to the United States or Europe, gains in Japan's core-core CPI are insufficient." He added that "what we can learn from this is that people still don't believe inflation will reach 2 percent." And, "inflation expectations are not anchored." And he pledged to "maintain the regime and stance we have in place for monetary policy to meet 2 percent inflation and to strengthen it if possible."

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2863; (P) 1.2905; (R1) 1.2982; More....

USD/CAD drops sharply in early US session. But for the moment, it's still staying above 1.2802 cluster support zone (38.2% retracement of 1.2246 to 1.3124 at 1.2789). Price actions from 1.3124 are viewed as a near term pull back only. And intraday bias stays neutral, and bullish outlook is unchanged. That is, further rally is expected. On the upside, break of 1.3124 will extend recent rally to 161.8% projection of 1.2061 to 1.2916 from 1.2246 at 1.3629 next. However, firm break of 1.2789/2802 will raise the chance of rejection by 1.3065 medium term fibonacci level and bring deeper fall to 55 day EMA (now at 1.2741).

In the bigger picture, we're favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061 as a correction, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Sustained break of 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will pave the way to 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2802 support holds. However, rejection by 1.3065 will argue that price action from 1.2061 is merely a three wave corrective pattern. And 1.2061 will be put back into focus with medium term bearishness revived.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Feb | 1.00% | 1.00% | 0.90% | |

| 12:00 | GBP | BoE Quarterly Bulletin | ||||

| 12:30 | CAD | CPI M/M Feb | 0.60% | 0.50% | 0.70% | |

| 12:30 | CAD | CPI Y/Y Feb | 2.20% | 2.00% | 1.70% | |

| 12:30 | CAD | CPI Core - Common Y/Y Feb | 1.90% | 1.90% | 1.80% | |

| 12:30 | CAD | CPI Core - Median Y/Y Feb | 2.10% | 1.90% | ||

| 12:30 | CAD | CPI Core - Trimmed Y/Y Feb | 2.10% | 1.80% | ||

| 12:30 | CAD | Retail Sales M/M Jan | 0.30% | 1.20% | -0.80% | -0.70% |

| 12:30 | CAD | Retail Sales Ex Auto M/M Jan | 0.90% | 0.90% | -1.80% | -1.70% |

| 12:30 | USD | Durable Goods Orders Feb P | 3.10% | 1.70% | -3.60% | |

| 12:30 | USD | Durables Ex Transportation Feb P | 1.20% | 0.50% | -0.30% | |

| 14:00 | USD | New Home Sales Feb | 621K | 593K |

Fed Bostic: Fed at or near objectives, supports further rate hikes

Atlanta Fed President Raphael Bostic sounds upbeat in his prepared speech for Knoxville Economic Forum.

With six month core inflation at 2%, and unemployment rate at 4.1%, he considered Fed is "at or near the sustainable employment and inflation objectives."

Regarding interest rate, he said that "if the economy evolves roughly as I suspect, I will likely support further increases over the course of the year."

And, "with the economy operating near its potential and inflation finally approaching the long-run target, it is appropriate, in my opinion, for monetary policy to be moving toward a more neutral stance."

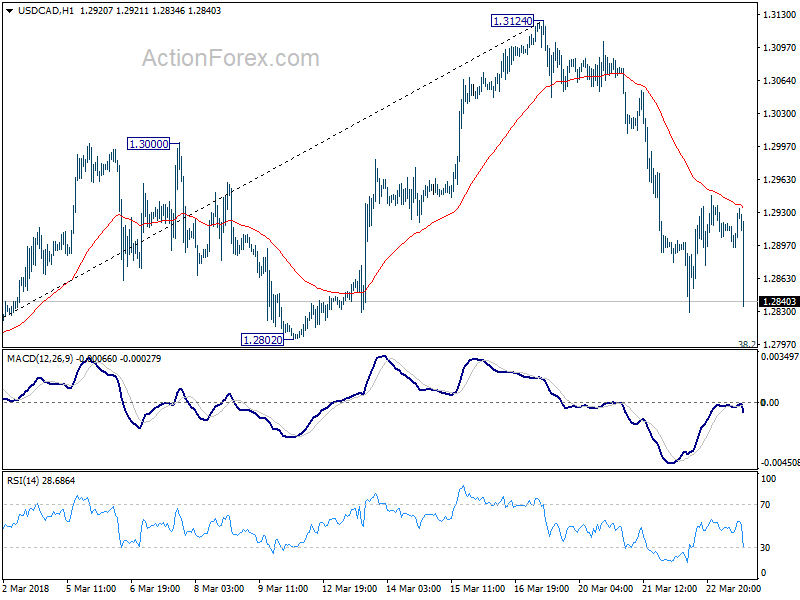

USD/CAD to revisit yesterday’s low as Canada CPI accelerated notably in Feb

USD/CAD dives sharply in early US session after data release.

From US, durable goods orders rose 3.1% in February, above expectation of 1.7%.

Ex-transport orders rose 1.2% versus expectation of 0.5%.

However, markets response to Canada inflation data seems to be much stronger.

From Canada, CPI rose 0.6% mom, 2.2% yoy in February, beat expectation of 0.5% mom, 2.0% yoy. Annual rate also accelerated from prior month's 1.7% yoy.

CPI core common accelerated to 1.9% yoy, up from 1.8% yoy. CPI core media rose to 2.1% yoy, up from 1.9% yoy. CPI core trimmed rose to 2.1% yoy, up from 1.8% yoy.

Canada retail sales rose 0.3% versus expectation of 1.2% mom in January. Ex-transport order, though, met expectation and rose 0.9% mom.

USD/CAD drops sharply and is set to test on yesterday's low at 1.2828. Rejection from 55 H EMA certainly carries near term bearish implication. However, there is a key support zone ahead at 1.2802 cluster support zone (38.2% retracement of 1.2246 to 1.3124 at 1.2789). For the moment, we'd still expect strong support from there to bring rebound.

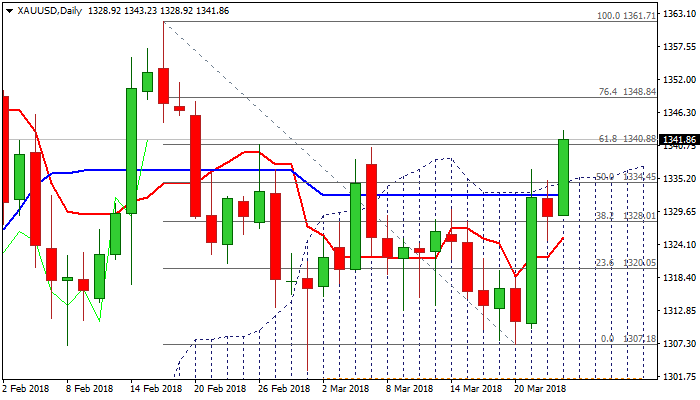

Spot Gold Rallied above Daily Cloud on Rising Safe-Haven Demand

Spot Gold hit one-month high at $1343 on fresh bullish acceleration on Friday, driven by increased safe-haven demand on rising fears about global trade war. Fresh extension higher signals continuation of recovery rally from $1307 (20 Mar low) which eventually broke above daily cloud top ($1334) after showing strong hesitation in past two sessions and also dented next pivot at $1340 (Fibo 61.8% of $1361/$1307 descend/former high of 07 Mar). Close above cloud top will be strong bullish signal which needs confirmation on close above cracked Fibo barrier ($1340). Daily MA's in bullish setup and north-heading 14-d momentum are supportive, with near-term action being also underpinned by thick daily cloud. Caution on slow stochastic entering overbought territory, which may delay bulls. Broken daily cloud top is expected to keep the downside protected.

Res: 1343; 1348; 1350; 1353

Sup: 1340; 1334; 1330; 1327