Sample Category Title

USD Weakens Following US Inflation

US Inflation data was released yesterday, with the initial reaction seeing USD pairs strengthen and Equities selloff. However, once the first 15 minutes had passed, post data, the trend reversed and the USD weakened further while Equities were short squeezed and bid higher. The US 500 Index dropped from 2672.90 to a low of 2627.7 but has since rebounded to highs of 2706.50. Gold sold off from 1330.70 to a low of 1317.20 but rebounded to currently trade around its highs of 1354.00. USDCAD moved higher after the data from 1.25763 to 1.26480 but is now trading at its lows near 1.24808.

German Harmonised Index of Consumer Prices (YoY) (Jan) was released coming in unchanged at 1.4%, as expected. Gross Domestic Product (QoQ) (Q4) was also as expected at 0.6%, from 0.8% previously. Gross Domestic Product (YoY) (Q4) was 2.3% v an expected 2.2%, from 2.3% previously. Gross Domestic Product w.d.a. (YoY) (Q4) was 2.9% v an expected 3.0%, from 2.8% previously.

SNB Governing Board Member Zurbrugg delivered a speech titled “Cash – a means of payment yesterday, today, and tomorrow” at the Bundesbank Cash Symposium in Frankfurt. His comments were: that the central bank is not planning to issue digital currency. He said that digital currencies won't displace cash anytime soon and they do not pose a problem for central banks currently. USDCHF moved higher from 0.93183 to 0.93582 after the comments.

Italian Gross Domestic Product (QoQ) (Q4) was as expected at 1.6%, from 1.7% previously. Gross Domestic Product (YoY) (Q4) was 0.3% v an expected 0.4%, from 0.4% previously.

Eurozone Gross Domestic Product s.a. (QoQ) (Q4) was as expected, unchanged at 0.6%. Gross Domestic Product s.a. (YoY) (Q4) was also as expected at 2.7%, from 2.6% previously, which was revised up to 2.7%. Industrial Production w.d.a. (YoY) (Dec) was released at 5.2% v a consensus of 4.2% and a prior of 3.2%, which was revised up to 3.7%. Industrial Production s.a. (MoM) (Dec) was 0.4% v an expected 0.2%, from 1.0% previously, which was revised up to 1.3%. The EURUSD pair moved lower to 1.23455 after this data.

US Retail Sales (MoM) (Jan) was released coming in at -0.3% against an expected 0.2%, from 0.4% previously. Retail Sales ex Autos (MoM) (Jan) was 0.0% v an expected 0.4%, from 0.4% prior, which was revised down to 0.1%. Retail Sales Control Group (Jan) was 0.0% v an expected 0.4%, from 0.3% prior. Consumer Price Index (MoM) (Jan) was 0.5% v an expected 0.3%, from 0.1% previously, which was revised up to 0.2%. Consumer Price Index (YoY) (Jan) was 2.1% v an expected 1.9%, from 2.1% previously. Consumer Price Index Ex Food & Energy (YoY) (Jan) was 1.8% v an expected 1.7%, from 1.8% prior. Consumer Price Index Ex Food & Energy (MoM) (Jan) was 0.3% v an expected 0.2%, from 0.3% previously, which was revised down to 0.2%. USDJPY went to a high of 107.541 before dropping back to 107.122. EURUSD dropped to 1.22757 from a high of 1.23508. GBPUSD dropped from 1.38874 to a low of 1.37996.

Japanese Machinery Orders (YoY) (Dec) were released at -5.0% with a consensus of 2.2% expected, from 4.1% prior. Machinery Orders (MoM) (Dec) were released at -11.9% with a consensus of -2.3% expected, from 5.7% previously.

At 01:30 GMT, Australian Unemployment Rate s.a. (Jan) came in as expected at 5.5%, from 5.5% previously, which was revised up to 5.6%. The Employment Change s.a. (Jan) was 16.0K v an expected 15.0K, from a previous 34.7K, which was revised down to 33.5K. The Participation Rate (Jan) was as expected at 65.6%, from a previous number of 65.7%. Consumer Inflation Expectation (Feb) was 3.6% from a reading of 3.7% previously.

EURUSD is up 0.14% overnight, trading around 1.24662.

USDJPY is down -0.50% in early session trading at around 106.469.

GBPUSD is up 0.08% to trade around 1.40089.

AUDUSD is up 0.22% overnight, trading around 0.79415.

Gold is up 0.16% in early morning trading at around $1,352.50.

WTI is up 1.10% this morning, trading around $61.36.

Major data releases for today:

At 08:15 GMT, ECB's Mersch will speak and this may impact on moves in EUR crosses.

At 10:45 GMT, ECB's Praet will speak. Comments from the speech may impact EUR crosses.

At 12:00 GMT, ECB's Lautenschlager will speak and any comments made could move EUR pairs.

At 13:30 GMT, US Continuing Jobless Claims (Feb 2) expected at 1.925M from a previous number of 1.923M. Initial Jobless Claims (Feb 9) is expected to come in at 230K with a prior reading of 221K. Philadelphia Fed Manufacturing Survey (Feb) is expected at 21.1 against a prior 22.2. USD crosses could see increased volatility around this data release.

At 14:15 GMT, US Industrial Production (MoM) (Jan) will be released. The consensus is for 0.2% from 0.9% previously. Capacity Utilization (Jan) is also released at this time, with an expectation for 78.0% v 77.9% prior. USD crosses may be impacted by this release.

At 15:00 GMT, US NAHB Housing Market Index (Feb) will be released and is expected to be unchanged at 72. This release may affect USD pairs.

At 18:30 GMT, Canadian BOC Governing Council Member will speak at the Manitoba Association for Business Economics in Winnipeg. Comments may affect CAD crosses.

At 21:30 GMT, New Zealand Business NZ PMI (Jan) is due to be released. The prior number was 51.2. NZD could see an increase in volatility due to this event.

At 22:30 GMT, Australian RBA Governor Lowe will testify before the House of Representatives' Standing Committee on Economics in Sydney. Volatility in AUD crosses is often experienced during his speeches.

At 23:50 GMT, Japanese Foreign Investment in Japan stocks (Jan 5) will be released with a previous number of ¥-126.7B. Foreign Bond Investment (Jan 5) had a prior number of ¥-866.6B.

Investors Shrug Off Inflation Fears

The U.S. inflation figures for January have been anxiously awaited by investors after wage growth sparked a sharp selloff in equity and treasury markets last week over fears of an overheating economy.

Wednesday's data confirmed that inflation in the world's largest economy is on the rise. Headline inflation hit 2.1%, beating the forecast of 1.9%. More importantly, the core CPI, which excludes volatile components like food and energy, rose 0.35% MoM, the biggest monthly rise since 2005, to stay unchanged for the year at 1.8%.

Higher prices are frequently accompanied by an increase in aggregate demand when the economy is at full employment. Making things more interesting, retail sales contracted 0.3% in January. This should become a complex situation for both investors and monetary policymakers if higher inflation accompanies lower spending.

So far, I still see three rate hikes in 2018 as the base case scenario and, in my opinion, this had already been baked into equity prices after last week's selloff. However, the risks are skewed to further monetary tightening and this will be problematic for the still overstretched valuations.

In such an environment, some investors might change their strategy to selling the rallies instead of buying the dips, which wasfollowed throughout last year. This requires a further rally in bond yields, and a significant break of 3% on the 10-year Treasuries will likely drive it.

Yesterday's reversal was quite surprising. Wall Street equities dipped immediately after the release of the data and the S&P 500 opened 0.5% lower to reverse losses within 30 minutes and ended the day 1.35% higher. A similar reaction was seen in European equities which turned to red, but managed to end the trading session in green.

The heightened expectations for rate increases and higher U.S. bond yields should be bullish for the U.S. dollar, particularly against the Yen. What we currently see is exactly the opposite. The Yen is sitting at a 15-month high against the dollar and showing no signs of giving up gains. This suggests investors are still nervous and unwilling to continue with the carry trade where they borrow the Yen at low interest rates in order to invest in higher-yielding currencies.

The dollar did not just decline against the Yen –it fell against a basket of currencies with the DXY falling 1.4% from yesterday's peak. This might be harder to explain when rate differentials widen. Markets seem to be expecting the rate differentials to narrow in the next couple of months, as other central banks begin with the tightening process. However, another spike in U.S. bond yields should start attracting more interest to the greenback.

Daily Wave Analysis: EUR/USD Bullish Bounce Retests 1.25 Resistance Zone

Currency pair EUR/USD

The EUR/USD bullish momentum is now approaching the previous top and resistance trend line (red). A break above the resistance could indicate an uptrend continuation within wave 5 (purple).A bull flag pattern or other chart pattern could indicate a pause before the breakout.

The EUR/USD strong pullback is probably a wave 2 (blue) but the bullish reversal is indicating that this is a potential wave 3 (blue).For price to confirm the wave 3 though, there will need to be a bullish break above the resistance trend line and a move towards the 161.8% Fib target.

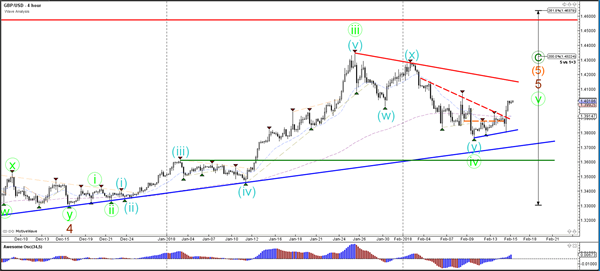

Currency pair GBP/USD

The GBP/USD made a bullish breakout above the previous tops (dotted orange) and resistance trend line (dotted red) which could indicate the start of wave 5 (green). A break above the next resistance (red) trend line could confirm a bullish breakout.

The GBP/USD bullish break is slow and corrective, which could indicate an ABC pattern rather than a 123. If price manages to stay above support (green/blue), then a 123 is more likely. Otherwise, if the support levels should break, then an ABC is more likely.

Currency pair USD/JPY

The USD/JPYused thesupportzone (dotted green) as resistance and broke below the -27.2% Fibonacci target. Price now has potential space to the next target which is the -61.8% Fib.

The USD/JPYis at the bottom ofa falling wedge pattern which could indicate a potential bullish retracement.

Australia’s Unemployment Rate Ticked Lower In January

For the 24 hours to 23:00 GMT, the AUD rose 0.48% against the USD and closed at 0.7919.

LME Copper prices rose 0.8% or $54.0/MT to $6962.0/MT. Aluminium prices rose 0.7% or $14.5/MT to $2138.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7936, with the AUD trading 0.21% higher against the USD from yesterday's close, after Australia's seasonally adjusted unemployment rate fell to 5.5% in January, at par with market expectations. Unemployment rate had registered a revised reading of 5.6% in the preceding month.

On the other hand, the nation's consumer inflation expectations eased to 3.6% in February, compared to a reading of 3.7% in the prior month.

The pair is expected to find support at 0.7824, and a fall through could take it to the next support level of 0.7712. The pair is expected to find its first resistance at 0.7997, and a rise through could take it to the next resistance level of 0.8058.

Going ahead, traders would keep a close watch on a speech by the Reserve Bank of Australia's (RBA) Governor, Philip Lowe, due overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Economy Grew As Initially Estimated In 4Q 2017, Industrial Production Zoomed In December

For the 24 hours to 23:00 GMT, the EUR rose 0.55% against the USD and closed at 1.2451, after the seasonally adjusted second estimate of the Euro-zone's gross domestic product (GDP) climbed 0.6% on a quarterly basis in the fourth quarter of 2017, confirming the preliminary print, thus suggesting that the region continued to witness strong growth in the final months of last year. In the prior quarter, GDP had registered a revised rise of 0.7%.

Additionally, the region's seasonally adjusted industrial production registered a rise of 0.4% on a monthly basis in December, higher than market expectations for a rise of 0.1%, amid a rise in the output of durable goods and intermediate goods. In the previous month, industrial production had risen by a revised 1.3%.

Separately, preliminary data revealed that economic activity in Germany expanded 0.6% on a quarterly basis in the three months to December 2017, meeting market expectations, owing to a strong pick-up in exports. In the prior quarter, GDP had climbed 0.8%. Moreover, the nation's final consumer price index (CPI) rose 1.6% on an annual basis in January, in line with the flash estimate. The CPI had registered a rise of 1.7% in the previous month.

The US Dollar declined against a basket of major currencies, after latest US economic releases painted a mixed picture of the health of the nation's economy.

Data indicated that consumer price inflation in the US jumped more-than-anticipated by 0.5% on a monthly basis in January, marking its sharpest increase in 5 months, thus offering signs of firming inflation that could force the Federal Reserve (Fed) to move aggressively in raising interest rates. In the prior month, the CPI had registered a revised rise of 0.2%, while markets were anticipating for a gain of 0.3%.

On the other hand, the nation's advance retail sales recorded an unexpected drop of 0.3% in January, dipping to its lowest in nearly a year. Retail sales had registered a revised flat reading in the previous month, while investors had envisaged for a rise of 0.2%. Also, the nation's MBA mortgage applications retreated 4.1% in the week ended 09 February, after recording an increase of 0.7% in the previous week.

In other economic news, business inventories in the US grew 0.4% on a monthly basis in December, topping market expectations for a gain of 0.3%. In the prior month, business inventories had registered a similar rise.

In the Asian session, at GMT0400, the pair is trading at 1.2460, with the EUR trading 0.07% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2333, and a fall through could take it to the next support level of 1.2206. The pair is expected to find its first resistance at 1.2530, and a rise through could take it to the next resistance level of 1.2600.

Looking ahead, traders would keep a close watch on the Euro-zone's trade balance data for December, slated to release in a few hours. Moreover, the US initial jobless claims followed by the industrial and manufacturing production data for January as well as the NAHB housing market index for February, all scheduled to release later in the day, will keep investors on their toes.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

UK Should Address Weak Productivity: IMF

For the 24 hours to 23:00 GMT, the GBP rose 0.62% against the USD and closed at 1.4002.

Yesterday, the International Monetary Fund (IMF) warned that Britain must focus on improving its productivity and international competitiveness in order to weather the shock of Brexit. Further, the Fund noted that weak domestic demand owing to rising inflation has asserted downward pressure on the nation’s economic growth.

In the Asian session, at GMT0400, the pair is trading at 1.4016, with the GBP trading 0.1% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3870, and a fall through could take it to the next support level of 1.3724. The pair is expected to find its first resistance at 1.4092, and a rise through could take it to the next resistance level of 1.4168.

With no macroeconomic releases in UK today, investor sentiment would be determined by global macroeconomic news.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Industrial Production Revised Higher In December

For the 24 hours to 23:00 GMT, the USD declined 0.15% against the JPY and closed at 106.93.

In the Asian session, at GMT0400, the pair is trading at 106.50, with the USD trading 0.4% lower against the JPY from yesterday's close.

Overnight data showed that Japan's machinery orders slid 11.9% MoM in December, more than market expectations for a drop of 2.0%. In the previous month, machinery orders had climbed 5.7%.

Earlier today, data indicated that the nation's final industrial production grew more than initially estimated by 2.9% on a monthly basis in December, while the preliminary figures had recorded an advance of 2.7%. In the prior month, industrial production had risen 0.5%.

The pair is expected to find support at 106.03, and a fall through could take it to the next support level of 105.55. The pair is expected to find its first resistance at 107.26, and a rise through could take it to the next resistance level of 108.01.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.38% against the CHF and closed at 0.9291.

In the Asian session, at GMT0400, the pair is trading at 0.9275, with the USD trading 0.17% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9239, and a fall through could take it to the next support level of 0.9203. The pair is expected to find its first resistance at 0.9343, and a rise through could take it to the next resistance level of 0.9411.

Amid no macroeconomic releases in Switzerland today, investors would focus on global macroeconomic releases for further direction.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading A Tad Higher, Ahead Of Canada’s Existing Home Sales Data

For the 24 hours to 23:00 GMT, the USD declined 0.57% against the CAD and closed at 1.2496.

On the macro front, Canada's Teranet/National Bank house price index climbed 0.3% on a monthly basis in January. In the previous month, the index had risen 0.2%.

In the Asian session, at GMT0400, the pair is trading at 1.249, with the USD trading slightly lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2430, and a fall through could take it to the next support level of 1.2371. The pair is expected to find its first resistance at 1.2599, and a rise through could take it to the next resistance level of 1.2709.

Ahead in the day, investors would await the release of Canada's existing home sales data for January.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

ECB’s Praet Speaks At 11:45 CET

Market movers today

In Norway, Norges Bank's governor Olsen is making his annual address at 18.00 CET, which will be interesting, not least as Norges Bank has made a U-turn from signalling further rate cuts to indicating a rate increase within a year (page 2).

In the US, we get PPI inflation data for January, which might attract more attention than usual after the higher-than-expected CPI inflation print released yesterday.

Also in the US today, we get production data for January and Empire and Philly regional manufacturing PMIs for February.

The Chinese financial markets are closed from today and until 22 February for the Lunar New Year.

ECB's Praet speak s at 11:45 CET.

Selected market news

The US CPI was the highlight of data points yesterday. Overall the strong CPI core 1.8% yoy (close to 3% annualised in the last three months), supports the case for the Fed to move forward with further rate hikes. Albeit , retail sales were weaker than expected. Over the day as a whole, risk sentiment was supported despite an initial knee-jerk on the US CPI. Global equities rose across the board. Asian equities followed the pattern by rising 1-2% in the overnight session. S&P 500 rose 1.4% as eurostoxx rose 0.9%, while the volatility index VIX fell rapidly after the knee-jerk reaction to the US data and ended around 19.3. The yen strengthened again yesterday. The treasury yields ended the day 7bp higher at 2.90%.

South African now former president resigned yesterday with immediate effect . ANC leader Cyril Ramaphosa will replace Zuma.

Euro area Q4 growth was confirmed at 0.6% q/q as expected. The flash release of Germany and Italy were also released. German Q4 17 growth came in as expected at 0.6% q/q, mainly due to strong foreign demand and a pick-up in exports. This leaves annual growth in 2017 at 2.5% and we expect the German economy to continue running on all engines. The Italian Q4 growth disappointing slightly at 0.3% q/q after 0.4% q/q in the previous quarter, despite the high manufacturing PMIs. This leaves annual growth in 2017 at 1.5%.

Yesterday, the Riksbank chose to reduce inflation (in part icular CPIF ex energy due to lowerthanexpected wage increases) and GDP forecasts (now recognising that housing construction activity will decrease more than expected previously) while keeping the reporate unchanged. We have elaborated with a base Riksbank scenario (no rate hikes this year) and a not improbable alternative scenario (one or possibly two hikes then a pause for a year or so). Admittedly, it looks like a close call. That the Riksbank is sticking to the rate path despite lowering the inflation forecast could be taken as hawkish but , in our view this is not really vindicated by the policy report . This suggests that the Riksbank was close to delaying the first hike. For now, we stick to our base case as the most probable but the minutes published on Friday next week will be of the essence just like the coming inflation data.