Sample Category Title

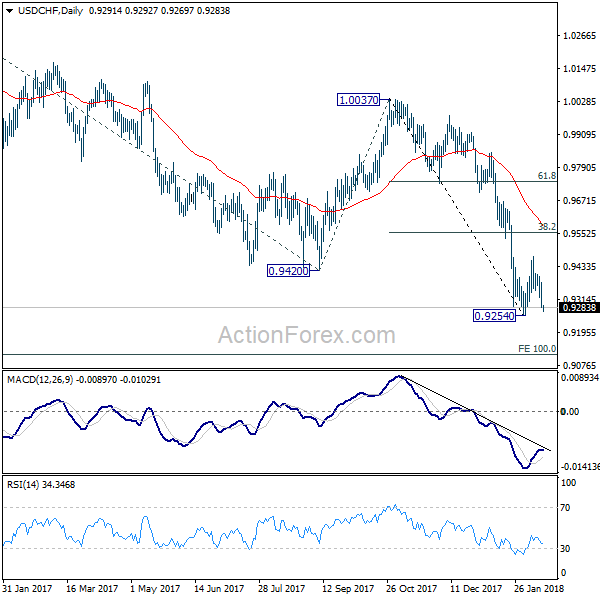

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9259; (P) 0.9317; (R1) 0.9349; More...

As long as 0.9373 minor resistance holds, fall from 0.9469 is in favor to extend to retest 0.9254 low. Break will resume larger down trend to next projection level at 0.9115. Above 0.9373 would bring another rise through 0.9469. However, note again that there is no sign of trend reversal yet. We'd be cautious on strong resistance from 38.2% retracement of 1.0037 to 0.9254 at 0.9553 to limit upside and bring down trend resumption.

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

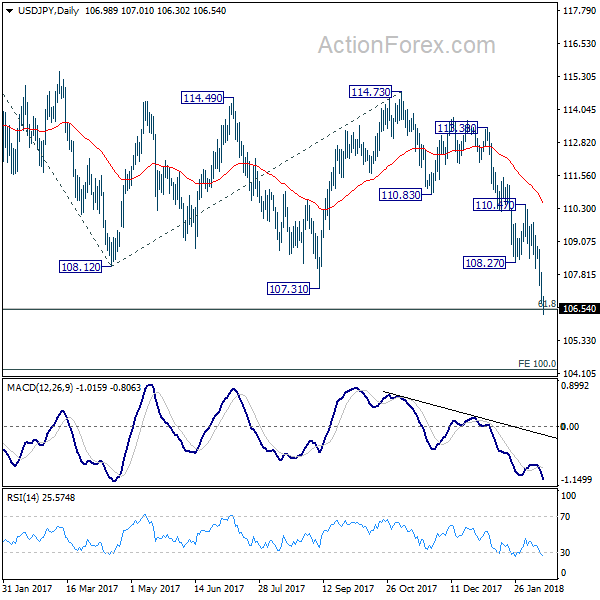

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.52; (P) 107.21; (R1) 107.69; More...

USD/JPY's fall extends to as low as 106.30 so far and is pressing 106.48 fibonacci level. At this point, we'd still look for strong support around 106.48 to bring rebound. But break of 107.89 minor resistance is needed to be the first sign of short term bottoming. Otherwise, outlook will stay bearish. Firm break of 106.48 will extend medium term fall from 118.65 to 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

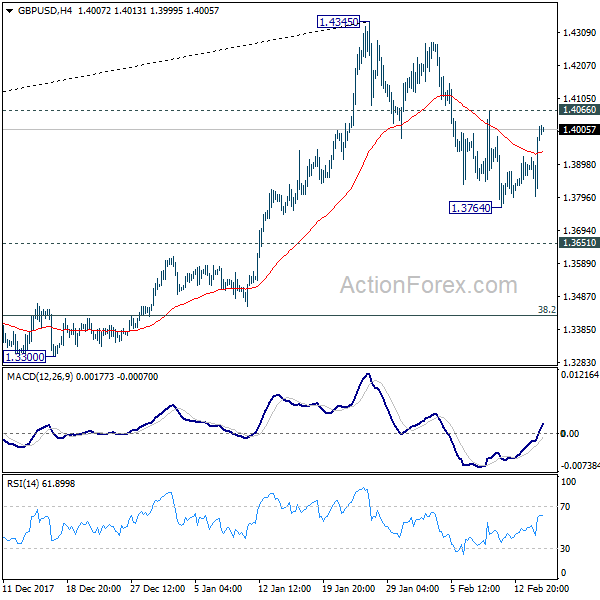

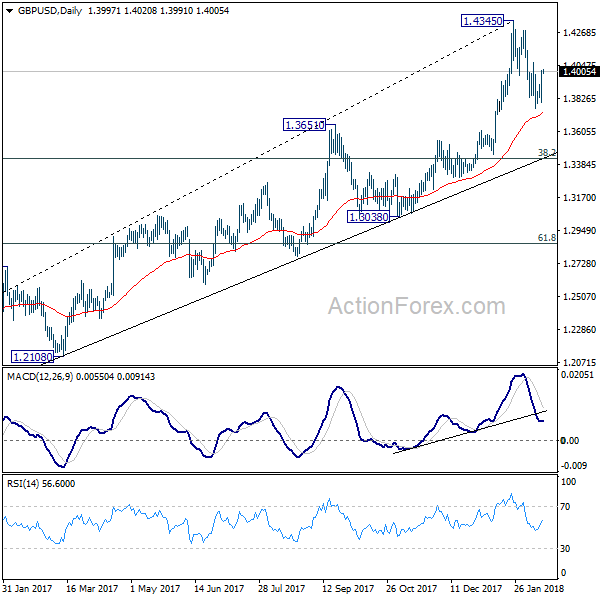

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3859; (P) 1.3938; (R1) 1.4075; More.....

Intraday bias in GBP/USD remains neutral for consolidation above 1.3764 temporary low. On the upside, break of 1.4066 minor resistance will suggest that corrective pull back from 1.4345 has completed. Intraday bias would then be turned back to the upside for retesting 1.4345. Break will resume larger up trend. On the downside, below 1.3764 will extend the correction to 1.3651 resistance turned support.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

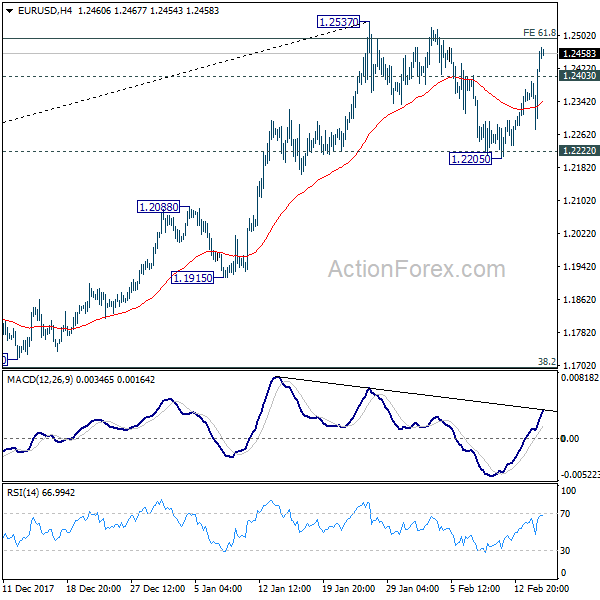

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2328; (P) 1.2397 (R1) 1.2518; More....

EUR/USD's strong rebound and break of 1.2403 suggests that pull back from 1.2537 has completed at 1.2205, after drawing support from 1.2222 key support level. Intraday bias is back on the upside for 1.2537 resistance. Decisive break there will resume larger up trend and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. In any case, for now, as long as 1.2205 support holds, outlook will remain bullish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

CPI Triggered Rebound Short Lived, Dollar Ready to Resume Down Trend

The moves triggered by stronger than expected CPI in the US proved to be short lived. DOW opened lower overnight to 24490.36 but quickly reversed. Eventually it ended up 1.03% at 24893.49. S&P 500 and NASDAQ also closed up 1.34% and 1.86% respectively. Dollar initially gained after the release but also reversed quickly. More importantly, it now looks like the greenback is ready to resume it's broad based down trend. Staying in the currency markets, Yen is trading as the strongest one for the week on revived speculations of stimulus exit. That's followed by Kiwi and then Euro. The only move that was persistent was the rally in treasury yields with 10 year yield closing up 0.073 to 2.913, resuming recent up trend towards 3.036 key resistance.

The post CPI rally in stocks could be seen as an indication that the crash in the prior weeks were excessive. That is, fear over aggressive Fed tightening was over-priced with DOW fall from 26616.71 historical high to 23360.29. Some analysts said that the worst is already over. We'll a bit more cautious stance for the moment. DOW will be entering into key near term resistance zone between 55 day EMA (24903) and 61.8% retracement of 26616 to 23360 at 25372. Reactions to this zone is the key to decide whether the correction from 26616.71 is over.

The sharp decline is Dollar index overnight now suggests that recent recovery from 88.43 is already over, limited well below 55 day EMA. The larger medium term down trend is ready to resume to target 61.8% projection of 103.82 to 91.01 from 95.15 at 87.23. This is in line with development in EUR/USD, which defended 1.2222 key support and is heading back to 1.2537 high.

Elsewhere

Japan machine orders dropped -11.9% mom in December. Australia employment grew 16k in January, unemployment rate dropped 0.1% to 5.5%. Australia consumer inflation expectation rose 3.6% in February. Eurozone trade balance is the only feature in European session. Later in the day, US will release regional Fed surveys from Empire state and Philadelphia, PPI, jobless claims, industrial production and NAHB housing index.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2328; (P) 1.2397 (R1) 1.2518; More....

EUR/USD's strong rebound and break of 1.2403 suggests that pull back from 1.2537 has completed at 1.2205, after drawing support from 1.2222 key support level. Intraday bias is back on the upside for 1.2537 resistance. Decisive break there will resume larger up trend and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. In any case, for now, as long as 1.2205 support holds, outlook will remain bullish.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Machine Orders M/M Dec | -11.90% | -2.30% | 5.70% | |

| 00:00 | AUD | Consumer Inflation Expectation Feb | 3.60% | 3.70% | ||

| 00:30 | AUD | Employment Change Jan | 16.0K | 15.2K | 34.7K | 33.5K |

| 00:30 | AUD | Unemployment Rate Jan | 5.50% | 5.50% | 5.50% | 5.60% |

| 04:30 | JPY | Industrial Production M/M Dec F | 2.70% | 2.70% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | 22.6B | 22.5B | ||

| 13:30 | USD | Empire State Manufacturing Feb | 18 | 17.7 | ||

| 13:30 | USD | Initial Jobless Claims (10 FEB) | 227k | 221k | ||

| 13:30 | USD | PPI M/M Jan | 0.40% | -0.10% | ||

| 13:30 | USD | PPI Y/Y Jan | 2.50% | 2.60% | ||

| 13:30 | USD | PPI Core M/M Jan | 0.20% | -0.10% | ||

| 13:30 | USD | PPI Core Y/Y Jan | 2.10% | 2.30% | ||

| 13:30 | USD | Philadelphia Fed Business Outlook Feb | 21.6 | 22.2 | ||

| 14:15 | USD | Industrial Production M/M Jan | 0.20% | 0.90% | ||

| 14:15 | USD | Capacity Utilization Jan | 78.00% | 77.90% | ||

| 15:00 | USD | NAHB Housing Market Index Feb | 72 | 72 | ||

| 15:30 | USD | Natural Gas Storage | -119B | |||

| 21:00 | USD | Net Long-term TIC Flows Dec | 50.3B | 57.5B |

At The Edge Of A Cliff

At the Edge of a Cliff

Was it the mixed data, skewed positioning or merely a lack of confidence that has the USD dollar precariously perched at the edge of the cliff.

Everyone one to a tee went all in on a dollar buying frenzy after the CPI number, but the lack of follow-through was very telling, and the quick rebound stopped out all those newly minted positions and then some. The markets sold AUD, NZD heavily at the lows and then got summarily spanked when traders started to factor in the conflicting data prints.

While the Strong CPI reading does present a hawkish risk for the Feds dot plots in March, the miss in the US retail sales data has the street scrambling to revise GDP estimates lower.The divergent data stream has escalated the market debate of critical importance, specifically is it inflation or growth that will dictate the Fed pace of interest rate normalisation?

But the bottom line for the US dollar in my view, amidst rising inflation the prospect of increasing deficits, both trade and budget, should weigh like an anvil around the dollar bulls neck

Equity markets

In seemingly absurd fashion, US equity investors ignored the inflationary signals and focused on weaker-than-expected US retail sales report. There is an increasing possibility that the Powell may blink and the Feds will be more hesitant to guide monetary policy hawkish given the waning growth narrative.

Gold Markets

Higher US inflation combined with the USD exhibiting zero correlation to higher interest rates amidst burdening duel deficits should play out favourably for Gold markets. The weaker dollar narrative is playing out most favourably across the broader commodity space and gold demand could surge and push above this year’s highs. Also, the sustainability of the frothy equity market given the weak retail sales print suggest increasing gold equity hedges is a practical move.

Oil Markets

A weaker dollar and verbal intervention from Saudi Energy minister who suggested significant oil producers would prefer tighter markets than end supply cuts too early has seen oil prices do an about-face. The Suadi signal is reasonably convincing suggesting OPEC and their partners are committed to maintaining an absolute floor on oil prices

As indicated earlier in the week, the battle lines are forming around this key WTI 60.00 bpd as the Shale oil gusher will continue to weigh heavily on OPEC effort to blow out the worldwide glut.

However physical demand remains weak globally so traders will continue to monitor the USD /Oil price correlation and at first sign of flutter, it could signal a downdraft.

Currency Markets

Japanese Yen

With the Interest rate to FX correlation is in “Neverland”, It could be open season on USDJPY after convincingly crossing the 107 USDJPY Rubicon. If the market focus aggressively shift to the US’s duelling deficit amid higher inflation, the dollar days are numbered in the 107’s if we factor in an expected Exporter flow panic which could be exacerbated by a push from Japanese investors to raise their hedge ratios on US investments fearing a further fall in the greenback.

While we should expect the usual verbal lashing from Japan’s currency officials, I suspect we are still ways off from overt intervention

The Austrailian Dollar

It’s always good to go into critical economic data with a plan B even if it’s from outer space. Expect the unexpected and today we see Aussie is benefiting from resurgent Commodities and US dollar weakness as the greenback is showing no correlation to higher US rates.

Malaysian Ringgit

A weaker US dollar, rebounding commodity prices have the MYR sitting well supported by yesterday’s robust GDP print adding good measure

Dollar weakness is seeping in the USDJPY and USDCNH which will provide a positive backdrop for regional currency markets, and we should expect the MYR to be one of the keys go to currencies as positions remain under positioned post-January monetary policy meeting. Higher US interest rates are showing little obstacle for regional currency appreciation so the MYR should benefit

Not to weave a cautionary tales but liquidy is a bit thin given in regional markets given the proximity of China Lunar New Year so best to be nimble in these conditions

Gold Jumps As Strong CPI And Weak Retail Sales Spook Markets

Gold prices have posted strong gains in Wednesday's North American session. Currently, the spot price for an ounce of gold is $1348.04, up 1.41% on the day. On the release front, January consumer inflation beat expectations. CPI jumped 0.5%, above the estimate of 0.3%. Core CPI remained steady at 0.3%, edging above the forecast of 0.2%. Consumer spending reports in January were dismal. Retail Sales was flat at 0.0%, short of the estimate of 0.5%. Core Retail Sales declined 0.3%, well off the forecast of +0.2%.

A strong CPI release for January has sent the US dollar lower against the major currencies, and gold has jumped on the bandwagon. Concerns of high inflation was a catalyst for the market sell-off last week, and fears of a resumption in the downward spiral are weighing on the dollar. If investors react negatively and ditch the markets yet again, safe-haven assets like gold will likely be the big winners. Gold prices were down in the first half of February, but gold has recovered these losses, after posting strong gains of 2.4% this week.

What about the Federal Reserve? Currently, the Fed is planning three hikes this year, but that could change to four or even five hikes, if inflation continues to head upwards and the robust US economy maintains its strong expansion. The new head of the Federal Reserve, Jerome Powell, received a rude welcome from the stock markets, as he started his new position last week. Powell sought to send a reassuring message on Tuesday, saying that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed's hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time.

Pound Jumps As US Inflation Drags Down Dollar

The British pound has posted gains in the Wednesday session. In North American trade, GBP/USD is trading at 1.3867, up 0.53% on the day. On the release front, January consumer inflation beat expectations. CPI jumped 0.5%, above the estimate of 0.3%. Core CPI remained steady at 0.3%, edging above the forecast of 0.2%. Consumer spending reports in January were dismal. Retail Sales was flat at 0.0%, short of the estimate of 0.5%. Core Retail Sales declined 0.3%, well off the forecast of +0.2%. The sole British event, CB Leading Index, declined 0.2%.

The US dollar has posted broad losses in the North American session, as CPI indicators were higher than expected. Concerns of high inflation was a catalyst for the market sell-off last week, and fears of a resumption in the downward spiral are weighing on the dollar. What about the Federal Reserve? Currently, the Fed is planning three hikes this year, but that could change to four, or even five hikes, if inflation continues to head upwards and the robust US economy maintains its strong expansion. The new head of the Federal Reserve, Jerome Powell, received a rude welcome from the stock markets, as he started his new position last week. Powell sought to send a reassuring message on Tuesday, saying that the Fed is on alert to any risks to financial stability. However, it is clear that the Fed’s hand is limited when it comes to stock markets moves, and the volatility which we saw last week could resume at any time.

There were no surprises from British inflation numbers on Tuesday. CPI, the primary gauge of consumer spending, was unchanged at 3.0% in January. CPI has hovered around the 3% level since August, well above the BoE target of 2.0%. Wage growth has not kept up with the brisk clip of inflation, putting a further squeeze on the British consumer. This could dampen consumer spending, a key driver of the economy. High inflation is putting pressure on the Bank of England to raise interest rates, and last week the Bank said that it was considering faster and larger rate increases than it had projected back in November. Many analysts have circled May as the date of the next rate increase.

No Love For The Dollar

The US dollar has been a dog for more than a year but the trade on Valentine's Day showed just how unloved it is. The dollar was a major laggard despite strong inflation data while commodity currencies soared. Australian jobs numbers are up next. A 2nd Aussie trade has been issued today to gear up for Aussie jobs figures due at 19:30 ET, 00:30 GMT/London, one of the trades is long AUD other is short AUD with the idea that both will move towards target over time based on the relationship between the cross currency relationship. Gold and silver were the stars of the day. Here is my reasoning 20 mins prior the release of US CPI & retail sales on why gold should rally regardless of the outcome.

All eyes were on US inflation numbers Wednesday as worries about inflation derailing corporate earnings and growth continue to circulate. The worst happened as CPI rose 0.5% m/m compared to +0.3% expected. Core numbers were equally hot.

The dollar shot higher on the headlines in 50-80 pip moves across the board but the highs were within moments. From there the US dollar embarked on an epic reversal that included a rally in cable to 1.40 from 1.3800 and in the euro to 1.2455 from 1.2275.

Part of the story was a dismal retail sales report. It was down 0.3% compared to the +0.2% consensus. Holes were also poked in the high CPI number because of a handful of jumps in odd categories.

Stock markets also made a major turnaround with the S&P 500 finishing 36 points higher after falling 40 points in the aftermath of the CPI print. Despite that and despite a march in US 10-year yields to 2.91%, USD/JPY finished at a 15-month closing low, breaking a major support level.

On a technical basis alone, the dollar is looking increasingly dismal. Wednesday's trade was a clear sign of how the market has lost faith in the dollar. We will continue to watch for a shift in the dollar-selling paradigm as US 10-year yields rise to 3% and beyond but the price action Wednesday spoke volumes.

One trade that will be in particular focus in the hours ahead is AUD/USD with the Aussie employment report due out at 0030 GMT. The consensus estimate is for a +15.0K print following a +34.7K rise in December. A strong number would put AUD/USD back on a path to the January high of 0.8130.

EURGBP Penetrates above Downward Sloping Channel

EURGBP has jumped above the downward sloping channel which was holding since October 2017. The price broke the 0.8900 handle and is trading above the 20 and 40 simple moving averages in the short-term timeframe. When looking at the bigger picture the pair lacks a clear tendency and the next days could be significant in case of a continuation of the slight upward movement.

In the daily timeframe, prices rebounded on the 0.8730 support level and based on the technical indicators, momentum is strong to provide a sustained move higher. The stochastic oscillator entered the overbought zone, while the MACD oscillator entered the positive territory and is holding above its trigger line.

If price action remains above the sloping channel, there is scope to test the 0.8930 resistance level. This is considered to be a strong resistance area which has been rejected a few times in the past. Rising above it could see prices re-testing the 0.8980 barrier.

On the flip side, in case of a failure to end the day above the upper band of the channel, the focus could shift to the downside towards the 20 and 40 SMAs near 0.8810 and 0.8840 respectively. If this level is breached, it could increase downside pressure and the price could move towards the 0.8730 support.