Sample Category Title

Elliott Wave View: Calling The Low In Placed In Bitcoin

Bitcoin ticker symbol: ( BTCUSD ) Short Term Elliott Wave view suggests that the decline from December 17.2017 peak to February 05.2018 low (5920.72) ended the Super Cycle wave “(b)” lower. Above from there, the rally is unfolding as a leading diagonal Elliott Wave structure. Where Intermediate wave (1) ended at 9090.8 high as Elliott Wave Double three structure. Where internals of Intermediate wave (1) ended in Minor wave W at 8648.9 high and Minor wave X at 7543.3 low.

Below from 9090.8 high, the pair ended it’s short-term correction against 2/05 cycle in Intermediate wave (2) low at yesterday’s low 7820. The internals of Intermediate wave (2) unfolded as Elliott Wave Zigzag correction, where Minor wave A ended at 8170.9 and Minor wave B ended at 8589.1 high. Above from there, the pair is expected to resume the upside. However, a break of 9090.8 high remains to be seen to avoid the double correction lower in Intermediate wave (2) dip. Up from 9090.8 low, the rally is unfolding as Zigzag Elliott wave structure. Where Minute wave ((a)) ended in 5 waves at 8992.9 high, below from there, the pair is doing a short-term correction against 7820 low in 3, 7 or 11 swings within Minute wave ((b)) dip. Near-term, while dips remain above 7820 low and more importantly the pivot from 5920.72 low remains intact during the dips pair is expected to resume higher. We don’t like selling it into a proposed pullback.

BTCUSD 1 Hour Elliott Wave Chart

GBPUSD Bearish Phase Continues, Momentum Indicators Look Negative

GBPUSD fell as low as 1.3770, a level that has been standing near the 40-day simple moving average during the past week. Since yesterday, the price has been trading slightly higher and successfully surpassed the 23.6% Fibonacci retracement level near 1.3820 of the last upward movement with the low of 1.2100 and the high of 1.4345.

Looking at the daily timeframe, the aggressive sell-off started after the pullback on the 1.4280 strong resistance level and the bearish correction is still in progress. The Relative Strength Index (RSI) is holding in the negative zone and is flattening, while the MACD oscillator is falling below its trigger line in the bullish territory.

Remaining in the same timeframe, if price continues the downside retracement and extends its losses below the 1.3770 support level, it could open the door for the 1.3660 barrier. If there is a fall below the latter level, there would be scope to test the 38.2% Fibonacci mark of 1.3490, which is near to the 11-month ascending trend line.

To the upside, the cable it could move towards the 1.4000 handle, which overlaps with the 20-day SMA at the time of writing. A break above the aforementioned obstacle could take the price towards the 1.4070 resistance level.

Currencies: USD Rally Running Into Resistance?

Sunrise Market Commentary

- Rates: Core yields holding near recent top head of US CPI

Yesterday, core bond yields held tight ranges near the recent peak as equities rebounded from last week's sell-off. Today, the calendar is again thin. More technical trading might be on the cards as markets look forward to tomorrow's US CPI. Global risk sentiment remains a wildcards. - Currencies: USD rally running into resistance?

Yesterday, the dollar lost slightly ground as sentiment on risk turned further positive. This morning, the US currency feels further selling pressure, with USD/JPY taking the lead. We expect more technical trading in the EUR/USD 1.22/24 trading range. EUR/GBP is nearing the 0.89 level. Today, UK CPI data might set the tone for GBP-trading

The Sunrise Headlines

- US equities continued Friday's comeback, closing the day with gains between 1.40% and 1.70%, the Dow Jones outperforming. Most Asian indices are also trading with good gains this morning. Chinese equities outperform. Japan trades in slightly negative territory as markets reopen after a long weekend.

- On Monday, President Donald Trump proposed a budget that calls for cuts in domestic spending and social programs such as Medicare and seeks a sharp increase in military spending and funding for a wall on the Mexican border..

- South Africa's ruling African National Congress decided to tell President Jacob Zuma to step down after he refused the top party leadership's request for him to resign voluntarily, according to five people familiar with the matter.

- Assistant governor of the Rank of Australia, Luci Ellis, said any pick up in wage growth was likely to be slow and protracted, weighing on household incomes and spending power amid high levels of debt. Australia still has more spare capacity than other developed countries, meaning it would take longer for wages and inflation to accelerate.

- The Japanese government wants Kuroda to serve another term as governor, according to a senior government official. PM Abe said he hasn't decided yet who to pick as next BOJ governor, but rebuffed calls from an opposition lawmaker to replace Kuroda given the pain the BOJ's negative interest rate policy was inflicting on commercial banks.

- Today's eco calendar is again thin in Europe. In the US, the NFIB small business confidence will be published. In the UK, the January price data take centre stage. Fed's Mester will speak on monetary policy and on the economic outlook. Italy will sell bonds of different maturities

Currencies: USD Rally Running Into Resistance?

USD rally running into resistance?

Last week, USD trading was only modestly affected as global volatility rose sharply. Yesterday, USD trading develop along the same lines. Equities recouped part of last week's sell-off. The dollar lost slightly ground against the euro, but the EUR/USD rise was capped near 1.23. USD/JPY was also little affected by the risk rebound, hovering in a tight range in the 108 big figure. The price action mainly occurred in equities with little impact on bonds and even less on the major USD cross rates. USD/JPY closed the day at 108.66. EUR/USD finished at 1.2292.

Asian equities mostly join the rebound from WS yesterday, with China outperforming. However regional indices are giving up part of the earlier gains toward the end of the session. Japanese equities are trading in negative territory as markets reopen after a long weekend. The dollar is ceding ground, with USD/JPY taking the lead. The pair trades in the 108.10 area. EUR/USD tries to regain the 1.23 mark. The USD correction occurs as US yields ease slightly this morning.

Today, the calendar is again thin. US NIFB small business confidence is expected to rebound from 104.9 to 105.3 after a decline last month. Fed's Mester will speak on Monetary policy (with Q&A). Will she give her view on recent market developments? FX traders will also keep an eye on bond and equity markets, even as they had little impact on the dollar of late. This morning, the dollar is ceding ground. This decline is a bit ‘strange' given the intraday price development on Asian equity markets. Even so, we assume EUR/USD to maintain a wait-and see modus in the 1.22/1.24 area going into tomorrow's US CPI release. Technically, the dollar decline slowed. EUR/USD dropped below the 1.2323/35 support but follow-through price action was modest. A break below 1.2165 would call off the ST downside alert (for USD).

Yesterday, BoE's Vlieghe reiterated that probably slightly more than three rate hikes are needed to keep inflation on target. It didn't help sterling. EUR/GBP closed at 0.8884. Today, the UK price data will be published. Headline CPI is expected to ease to 2.9% Y/Y, but other price indicators might paint a slightly different picture. A big positive surprise is probably needed to trigger a sustained comeback of sterling. Brexit uncertainty remains a sterling negative. EUR/GBP is trending higher in the 0.8690/0.9033 trading range, with intermediate resistance at 0.8930. We hold our view that the 0.8690 support probably won't be easy to break without big progress on Brexit.

USD trade-weighted (DXY): dollar rebound running into resistance?

Central Bank Speakers Start A Quiet Week In FX

Swiss Consumer Price Index (YoY) (Jan) was 0.7% v an expected 0.8%, from a previous 0.8%. Consumer Price Index (MoM) (Dec) was as expected at -0.1% from 0.0% previously. USDCHF fell from 0.93976 to 0.93664 after the data was made public.

UK MPC Member Vlieghe spoke at the Resolution Foundation in London. Some of the comments made were: If there is less credit headwind to the UK economy, then we may be ready for higher rates. There is increasing evidence that tighter labour markets are beginning to have an upwards effect on wages. The rise in the UK debt burden is not sustainable if it continues for many years. Households are leveraging up when there is not much slack in the economy. MPC should take an interest in that matter. Vlieghe says that the central bank is doing macro-prudential tightening but it is also appropriate to raise rates. Nothing has happened to challenge the BOE’s view about raising rates before reversing QE. The BOE has discovered it can cut rates lower than 0.5% since it gave guidance of a 2% threshold for reversing QE. The US Fed’s experience of reversing QE will also influence the level of rates at which BOE starts to reverse QE. The UK rate outlook depends on the uncertain economic outlook over next few years and the neutral UK interest rate is also very uncertain. GBPUSD made a low of 1.38319 before moving higher to 1.38738 during the speech.

UK MPC Member McCafferty spoke on the economic outlook and monetary policy. Some of the comments made were: It is quite likely that rates will move up slightly faster. The market is expecting three hikes over the next three years. There is a need for hikes because growth is strong and inflation is above target. Rates will have to go up gradually and the BOE will be watching data and making decisions on a month by month basis. The desire is to get rates to a place where they could be cut if it became necessary. EURGBP moved lower from 0.88887 to 0.88739 during the speech.

US Monthly Budget Statement (Jan) was $49.0B v an expected $51.0B, from a previous reading of $-23.0B.

Australian RBA Assistant Governor Ellis spoke about the economic outlook at the Australian Business Economists Forecasting Conference, in Sydney. Some of the comments made were: weak income growth very risky given high debt levels. The RBA is a bit more confident about the pickup in wages and inflation. Progress is, however, expected to be gradual and to lag other advanced economies. Central estimate is that NAIRU in Australia is still around 5 pct. Risk unemployment could fall further before stoking wages. No immediate pick up in wage growth is expected but a gradual rise is expected over time. Recent enterprise agreements to weigh on wage growth for a while. Retail competition to work against a rise in inflation and household income growth has been particularly weak in Australia. Households could curb spending if weak income growth becomes seen as permanent.

EURUSD is up 0.20% overnight, trading around 1.23153.

USDJPY is down -0.51% in early session trading at around 108.086.

GBPUSD is up 0.12% to trade around 1.38524.

AUDUSD is up 0.06% overnight, trading around 0.78630.

Gold is up 0.25% in early morning trading at around $1,325.75.

WTI is up 0.20% this morning, trading around $59.58.

Major data releases for today:

At 09:30 GMT, UK Consumer Price Index (YoY) (Jan) is expected out at 2.9% v 3.0% previously. Core Consumer Price Index (YoY) (Jan) is expected at 2.6% from 2.5% prior. Consumer Price Index (MoM) (Jan) is expected at -0.6% from 0.4% prior. Producer Price Index – Output (MoM) n.s.a. (Jan) is expected at 0.2% from 0.4% previously. Producer Price Index – Output (YoY) n.s.a. (Jan) is expected at 3.0% from 3.3% previously. Producer Price Index – Input (MoM) n.s.a. (Jan) is expected at 0.7% from 0.1% previously. Producer Price Index – Input (YoY) n.s.a. (Jan) is expected at 4.2% from 4.9% previously. PPI Core Output (MoM) n.s.a. (Jan) is expected to be unchanged at 0.3%. PPI Core Output (YoY) n.s.a. (Jan) is expected at 2.3% from 2.5% previously. Retail Price Index (MoM) (Jan) is expected at -0.7% from 0.8% previously. Retail Price Index (YoY) (Jan) is expected to be unchanged at 4.1%. GBP crosses could be moved by the data released at this time.

At 13:00 GMT, US FOMC Member Mester will speak about the economic outlook and monetary policy at the Dayton Area Chamber of Commerce Government Affairs Breakfast. Audience questions are expected to follow and this may impact US Assets and USD crosses.

At 23:30 GMT, Australian Westpac Consumer Confidence (Feb) will be released, with a prior reading of 1.8%. This could affect AUD crosses.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.57; (P) 150.66; (R1) 152.42; More...

At this point, intraday bias in GBP/JPY stays on the downside. The decline from 156.59 short term top should target 146.96 support. Considering bearish divergence condition in daily MACD, firm break of 146.96 will be another sign of medium term trend reversal. On the upside, break of 154.03 resistance is needed to confirm completion of the fall. Otherwise, outlook will remain cautiously bearish even in case of recovery.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal after rejection by 55 month EMA. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43.

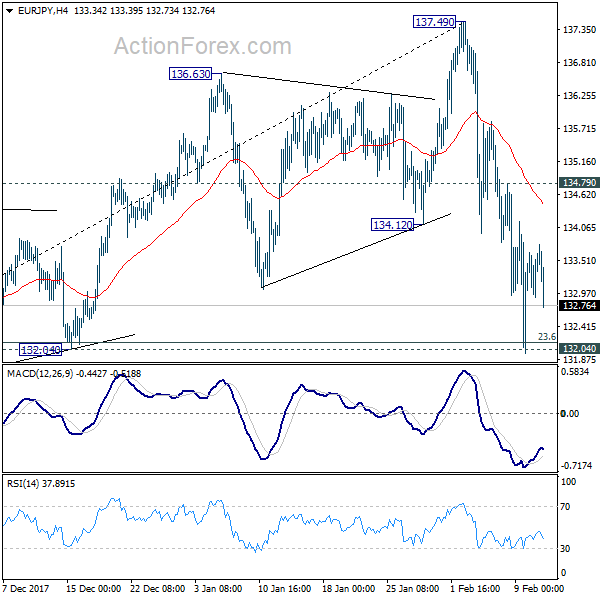

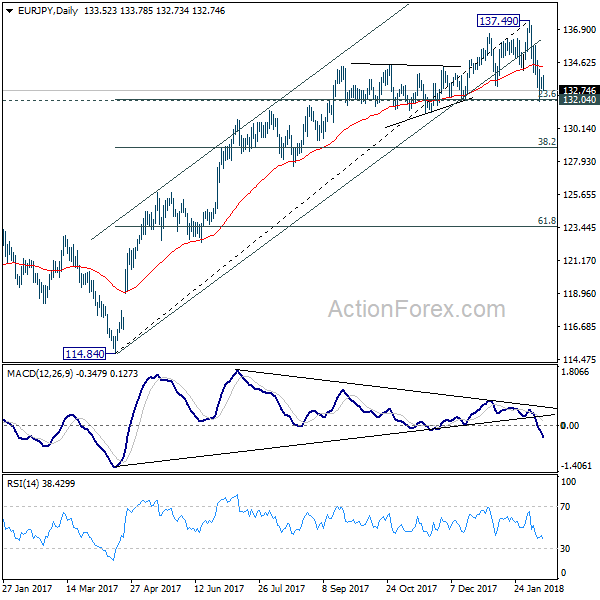

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.07; (P) 133.36; (R1) 133.82; More....

Intraday bias in EUR/JPY remains neutral for the moment. Deeper fall is still expected with 134.79 resistance intact. Decisive break of 132.04 cluster support (23.6% retracement of 114.84 to 137.49 at 132.14) will indicate larger trend reversal on bearish divergence condition in daily MACD. In such case, outlook will be turned bearish for 38.2% retracement at 128.38 first. Nonetheless, rebound from 132.04 will retain near term bullishness. Break of 134.79 minor resistance will bring retest of 137.49 high instead.

In the bigger picture, bearish divergence condition in week EMA indicates lost up medium term up trend momentum. But there is no clear sign of completion of up trend from 109.03 yet. Break of 137.49 will target 141.04/149.76 resistance zone. However, sustained break of 132.04 will be the early sign of long term reversal and should bring deeper fall back to retest 124.08 key support level.

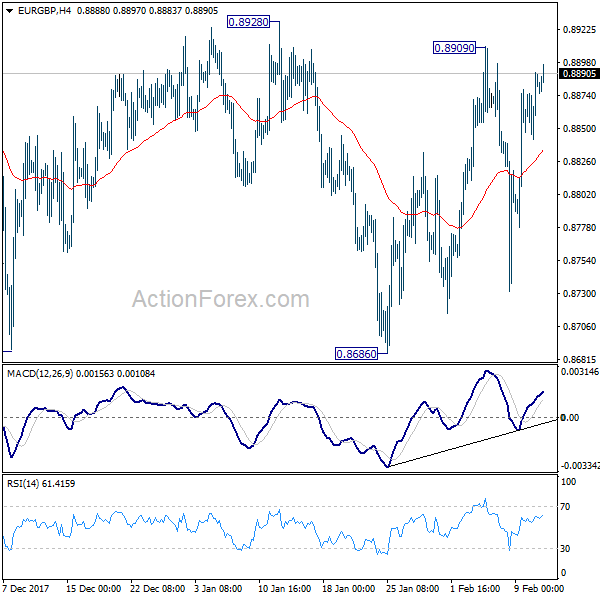

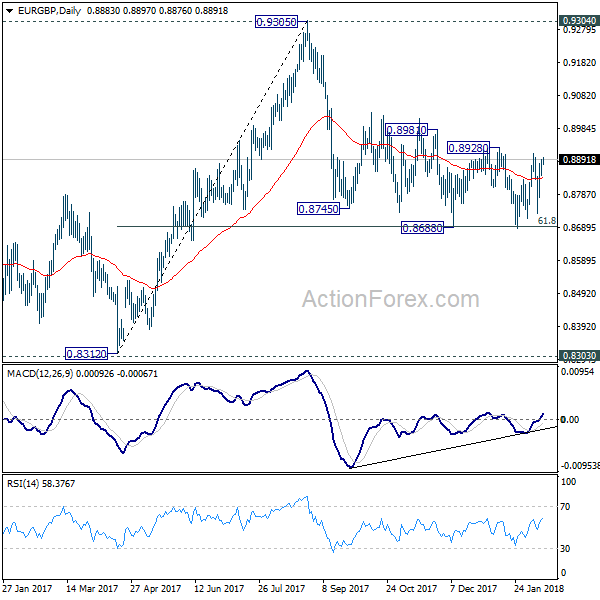

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8852; (P) 0.8871; (R1) 0.8901; More...

Intraday bias in EUR/GBP remains neutral as range trading continues. Near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

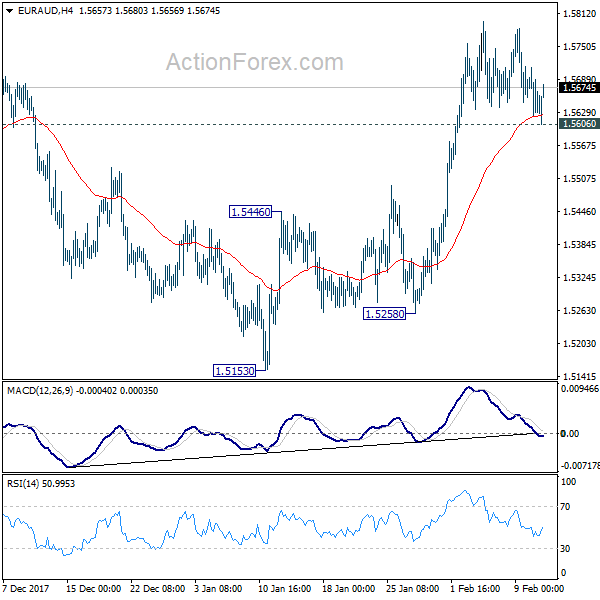

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5599; (P) 1.5655; (R1) 1.5687; More....

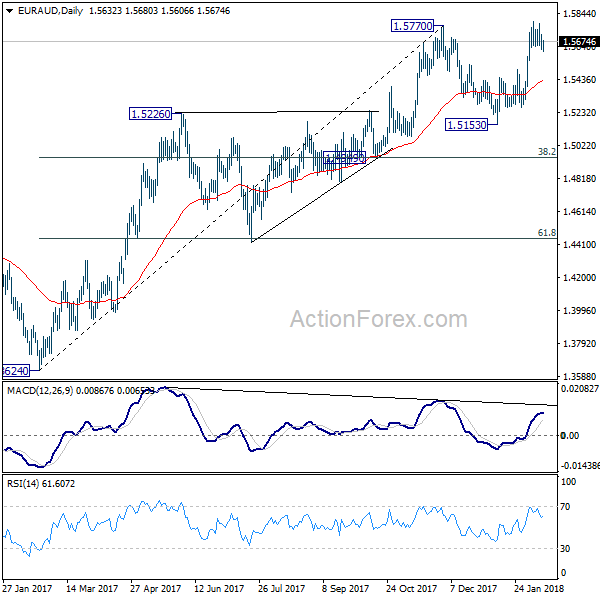

Despite breaching 1.5633 minor support, EUR/AUD quickly recovered, as supported by 4 hour 55 EMA. Intraday bias stays neutral and another rise is still in favor. Sustained break of 1.5770 resistance will confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance. However, below 1.5633 minor support minor support will dampen this bullish case and turn bias to the downside.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

The Most Important Release Is The UK CPI Inflation

Market movers today

The calendar is thin again today and overall focus remains on market sentiment . US stocks closed higher for the second consecutive day yesterday.

The most important release is the UK CPI inflation. We estimate CPI inflation fell from 3.0% in December to 2.9% in January, driven mainly by a smaller contribution from the energy component , as a big monthly increase in January 2017 falls out , and food. We estimate CPI core inflation rose from 2.5% to 2.6%. CPI inflation remains one of the key release after Bank of England turned more hawkish at last week’s meeting,

Despite being a tier-2 release, look out for the US NFIB small business optimism for January. Business optimism is very high at the moment indicating increasing growth in business investments.

IEA will publish its monthly oil market report today. Following the recent rise in the US oil rig count , oil market fundamentals have come back into focus and the market will watch out for revisions in particular to US output forecast .

Selected market news

Asian stocks are advancing for the second day, after the S&P 500 jumped by 1.4% yesterday and volatility retreated, with VIX falling below 26. EUR/USD and 10-year US Treasuries are little changed this morning, while oil crept higher. The rand slipped after South African President Zuma defied calls by his party to resign.

In the US, the White House yesterday unveiled its federal budget proposal for the fiscal year 2019, including a proposal of USD1,500bn spending on infrastructure (USD200bn of which being Federal funds). Democrats needed to enact any legislation have already dismissed the proposal due to lack of significant federal spending, while many Republican fiscal hawks are wary of any big spending bill. The proposal would see the deficit almost double from projections last year despite cuts to domestic programmes and foresees the budget in deficit until the fiscal year 2039. Overall, the proposal would only worsen the already unsustainable debt path and we remain sceptical that any such legislation will actually pass Congress.

On the foreign policy front , Washington signalled readiness for direct talks with Pyongyang after reaching a deal with South Korea on a diplomatic approach to North Korea. However, despite possible negotiations, the Trump administration intends to maintain the pressure on the North Korean regime with more sanctions still to come, according to US Vice-President Mike Pence.

Danish inflation surprised on the downside yesterday falling from 1.6% y/y in September to 0.7% in January. A mix of longer lasting and more volatile factors caused the fall, but overall this has caused us to revise down our inflation out look to 0.9% in 2018 and 1.4% in 2019 – an out look that was already at the low end versus other forecasts. See more in Flash Comment Denmark: January surprise paves way for another year of muted inflation - we revise down our forecast, 2 February.

GBP Under Brexit Pressure

The British pound is recovering after a massive selloff that occurred a while ago. GBP is looking for reasons for becoming stronger, but is somewhat calm for now.

Brexit talks between the United Kingdom and the European Union have been back since last week, and the new phase traditionally began with discussing EU claims. Michel Barnier, a key representative of the EU party of the talks, made a statement that sent the pound lower.

Barnier emphasized that the parties may still not come to an agreement. The problem is that the UK is all for the 'mild' Brexit scenario, while the EU is insisting on 'hard' Brexit, which could become far more painful for London. The parties have not yet agreed on the European Court role after the UK leaves the Union, as the civil right acts passed by the EU are here to stay. The parties have no intention of putting each other's interests at any disadvantage, but as long as there's no clear policy specified, it is a reason for the EU to suspend the talks.

The market are discussing whether the 'mild' Brexit is feasible or only the 'hard' scenario is now viable. The UK is still making it clear and consistent, but this does not support the British pound at all.

The Brexit uncertainty makes the fundamentals a bit frightening. The manufacturing production in December dropped by 1.30% MoM, which appeared to be a 10-month low. Meanwhile, the PMI went from 54.20 to 52.00, that being a 18-month low.

Technically, there are several trends dominating in GPB/USD. The major trend is still ascending, while the mid-term one is a correctional downtrend with the target at the major channel support, or at 1.3650. The short term trend is also descending and is a part of the mid-term impulse. This short term movement may become the final component of the internal correction. After the price achieves 1.3650, it may bounce off to the mid-term descending channel resistance at 1.3890, and then head towards the upper projection channel at 1.4060