Sample Category Title

Daily Wave Analysis: EUR/USD Bullish Breakout Above 1.23 Resistance And Bearish Channel

Currency pair EUR/USD

The EUR/USD broke above the resistance (dotted red) of the bearish trend channel after bouncing at support trend lines (blue), which could indicate the end of the wave 4 (purple) correction. A bullish continuation could indicate the start of wave 5 (purple) within wave 3 (pink).

The EUR/USD broke above the resistance levels and fractals of wave 4 (orange) and the top of wave 1 (blue). The bullish breakout could be part of a wave 3 (blue). This wave count could get confirmed if price manages to reach the 161.8% Fibonacci target at the minimum before building a wave 4.

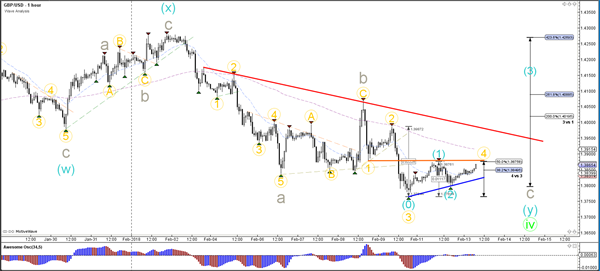

Currency pair GBP/USD

The GBP/USD failed to break below the previous low which indicate failure to continue with the downtrend. The Cable could be respecting the Fibonacci levels of wave 4 vs 3 (green) and a bullish breakout could indicate the start of wave 5.

The GBP/USD is at crossroads. It could break above resistance (orange) and invalidate the wave 4 correction (orange), which means that a bullish wave (blue) could start. Or price will bounce again at resistance and complete the 5th bearish wave (orange) before completing wave C (grey).

Currency pair USD/JPY

The USD/JPY is retesting a strong support zone again (green/blue). A break below this support zone could indicate a bearish continuation within wave 2/B (light purple) whereas a bullish bounce could see price complete the wave B/2.

The USD/JPY is showing strong bearish breakout candles below the support trend line (dotted blue). A break below the 100% Fib invalidates the wave 1-2 reversal.

Market Update – Asian Session: Equities Continue To Follow Wall Stlead

Headlines/Economic Data

General Trend: Equities in China and Hong Kong outperform

Kospi supported by gains in chip sector

In Asia, S&P500 and Nasdaq Futures move between gains and losses

Nikkei pares opening gains

Shanghai Property Index rises over 3%, later pares gain

China PBoC said to ask banks to temporarily halt new loans after Jan New Yuan Loans hit record high

PBoC offers 1-year medium-term lending facility (MLF) ahead of Chinese Lunar New Year

USD/JPY declines as Japanese traders return from holiday

Japan Q4 Prelim GDP data due on Wednesday

Japan

Nikkei 225 opened +1.2%; closed -0.7% (was closed on Monday for holiday)

TOPIX Iron & Steel Index -1.2%

Pioneer [6773.JP] Declines over 9% after cutting FY forecast

Renesas Electronics [6723.JP] Declines over 2%, guided Q1 semiconductor sales lower q/q

Fujifilm [4901.JP]: Declines over 1% as activist Carl Icahn urged Xerox to vote against planned merger

Toyota Motor declines over 1% amid stronger yen

(JP) Japan Fin Min Aso: Trying to promote new type of tax free NISA program

(JP) Japan Jan PPI (CGPI) M/M: 0.3% v 0.3%e; Y/Y:2.7% v 2.7%e

(JP) Japan Econ Min Motegi: PM Abe stance on monetary policy must be maintained- answer when asked about Gov Kuroda being reappointed

(JP) Japan PM Abe: Undecided on next BoJ Gov

(JP) Bank of Japan (BOJ) Gov Kuroda: Reiterates must maintain 'powerful' easing for economy, still distant to price target -speaking in parliament

Korea

Kospi opened +0.7%

Chip makers gain: Samsung Electronics and Hynix rise over 3%

Coway [021240.KR]: Declines over 6% after reporting FY earnings

Kangwon Land[035250.KR]: Declines over 1% as Q4 Op profit missed ests

(KR) South Korea Jan Export Price Index M/M:-0.4% v -1.5% prior; Y/Y: -3.5% v -2.0% prior; Import Price Index M/M: +0.7% v -0.7% prior; Y/Y:-2.4% v -0.9% prior

(KR) South Korea economist are worried about the fallout from a reversal ofcorporate tax rates and interest rates in Korea and the US; when the Fed raisesrates next time, it will create the first rate reversal between the twoeconomies in 11 years - Korean press

China/Hong Kong

Hang Seng opened +1.3%, Shanghai Composite +0.7%

Hang Seng Info Tech Index +3.5%, Materials +3%, Industrial Goods +2.8%, Consumer Goods +2.5%, Property/Construction +2.3%, Financials+2.3%, Services +2.3%

(CN) China PBOC has asked banks to defer new loans until after Feb 15th (start of Lunar New Year)

(CN) CHINA JAN NEW YUAN LOANS (CNY): 2.900T V2.050TE (fresh record high) after the closeyesterday

(CN) CHINA JAN M2 MONEY SUPPLY Y/Y: 8.6% V 8.2%E; M1 MONEY SUPPLY Y/Y: 15.0% V13.5%E after the close yesterday

(CN) CHINA JAN AGGREGATE FINANCING (CNY): 3.060T V 3.200TE afterthe close yesterday

USD/CNY (CN) PBOC SETS YUAN REFERENCERATE AT 6.3247 V 6.3001 PRIOR

(CN) CHINA PBOC LENDS CNY393B V CNY398B PRIOR IN 1-YR MEDIUM-TERM LENDINGFACILITY (MLF) AT RATE OF 3.25% V 3.25% PRIOR

(CN) PBoC: Skipped Open Market Operation (OMO) for 15th straight session

(CN) China Insurance Regulator (CIRC): Insurance firms offshore financingbalances backed by domestic guarantees cannot exceed 20% of net assets at endof prior quarter

Sunny Optical, 2382.HK Reports Jan handset lens setsshipments +19.6% y/y; Guides FY17 Net to rise more than 120% y/y

HNA unit HKICIM to sell Kai Tak sites to Henderson Land for HK$16.0B

Australia/New Zealand

ASX 200 opened +0.1%; closed +0.6%

ASX 200 Telecom Index +0.7%, Resources +0.8%, Financials +0.4%

(AU) RBA's Assistant Gov Ellis: Retail competition to work against wage pressures, no reason yet to change full employment est from 5%

(AU) Australia Bureau of Agricultural and Resource (ABARES): Total area plantedto summer crops is estimated to have increased by 2% in 2017-18 to 1.3M hectares,-9% from Dec forecast

(AU) Australia sells A$150M v A$150M indicated in Nov 2027 indexed bonds, bidto cover 4.20x, avg yield 0.85333%

(AU) Australia Jan NAB Business Confidence: 12 v 10 prior; Conditions: 19 v 13prior

PilbaraMinerals (+10%), PLS.AU Reports Pilgangoora Project Pre-Feasibility Study results, DefinitiveFeasibility Study to complete by mid 2018

(NZ) New Zealand Government 6-Month FinancialStatements; Budget Surplus NZ$1.09B, +NZ$779M more than forecasted

Other Asia

(TW) Taiwan Final Q4 GDP due for release during European session

North America

US equity markets ended broadly higher: Dow +1.7%, S&P500 +1.4%, Nasdaq +1.6%,Russell 2000 +0.9%

S&P500 Materials +2%, Technology +1.8%

(US) White House released 2019 budget plan: seeks$1.7T of cuts to mandatory spending and receipts

AmerisourceBergen (ABC) Walgreens said to be in early stage talks to acquire the company - US financial press

GM GM Korea to shut down one of its factors; Confirms that it needs support from stakeholders to normalize its business in South Korea; to take charges of up to $850M

Wynn Resorts [WYNN]: Special Committee retains law firm Gibson, Dunn & Crutcher LLP and expands review

Looking Ahead: US Weekly API Crude Oil Inventories due later today

Europe

(UK) BOE’s McCafferty (dissenter): interest rates will have to rise gradually - press interview; UK economy is holding up relatively well,so rates will probably start rising sooner than previously thought

(SA) South Africa's Zuma reportedly wants 3-month notice period before resigning – press; Reportedly Zuma was given 48 hours to resign

Michelin[ML.FR]: Reports FY17 Op Net €2.74 v €2.75Be, Rev €22.0B v €20.9By/y; Guides initial FY18 Recurring Op income higher y/y, FCF over €1.1B

Looking Ahead: UK Jan CPI data due later today, along with the IEA Monthly report

Levels as of 01:00ET

Nikkei225 -0.7%, Hang Seng +1.6%; Shanghai Composite +1.1%; ASX200 +0.6%, Kospi +0.7%

Equity Futures: S&P500 -0.3%; Nasdaq100 -0.2%,Dax -0.2%; FTSE100 -0.2%

EUR 1.2312-1.2284; JPY108.78-108.24; AUD 0.7874-0.7848;NZD 0.7272-0.7247

Apr Gold +0.2% at $1,328/oz; Mar Crude Oil +0.6% at $59.62/brl; Mar Copper +0.9% at $3.11/lb

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2250; (P) 1.2274 (R1) 1.2313; More....

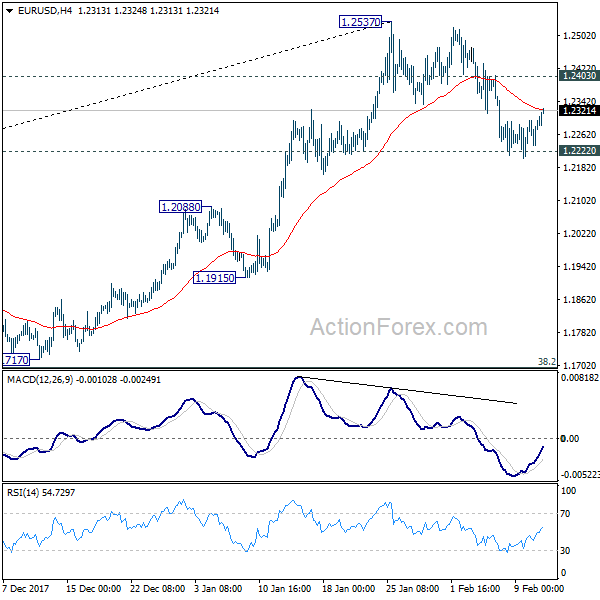

Intraday bias in EUR/USD remains neutral with focus on 1.2222 key near term support. Sustained break there should confirm rejection from 1.2516 key fibonacci level, as well as near term reversal, on bearish divergence condition in 4 hour MACD. That could also signal completion of medium term up trend from 1.0339. In that case, near term outlook will be turned bearish for 38.2% retracement of 1.0339 to 1.2537 at 1.1697. On the upside, though, above 1.2403 minor resistance will revive bullishness and turn focus back to 1.2537.

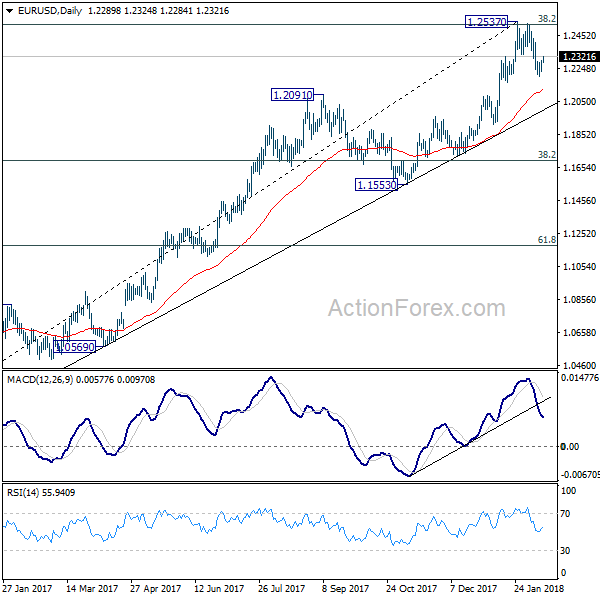

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

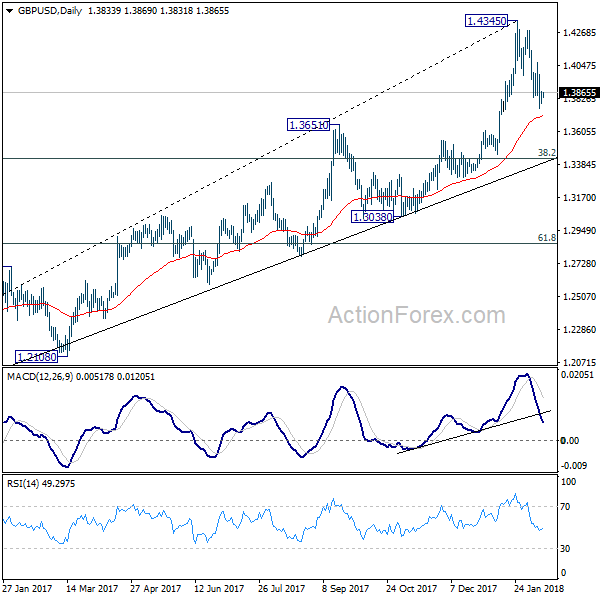

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3796; (P) 1.3835; (R1) 1.3876; More.....

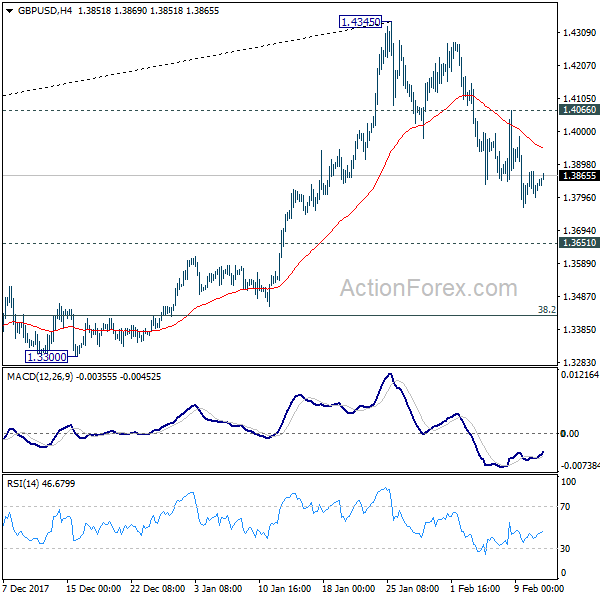

With 1.4066 minor resistance intact, deeper fall is expected in GBP/USD for 1.3651 resistance turned support. It's still unsure whether decline from 1.4345 is correcting rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn focus to key fibonacci level at 1.3429. On the upside, break of 1.4066 will turn bias back to the upside for retesting 1.4345 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279 so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

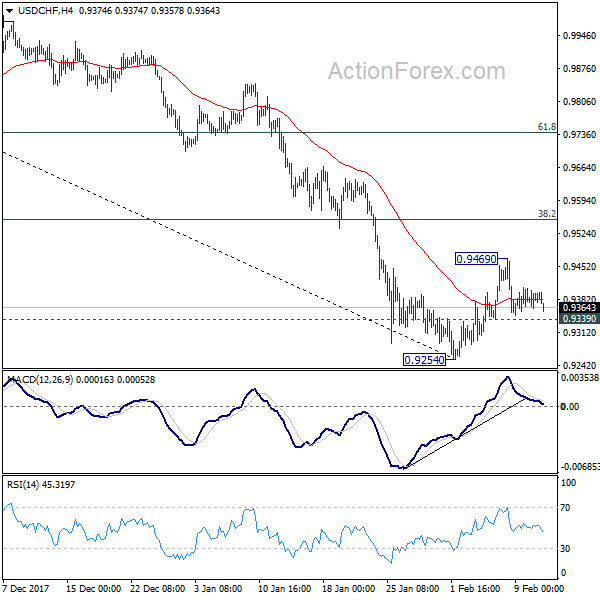

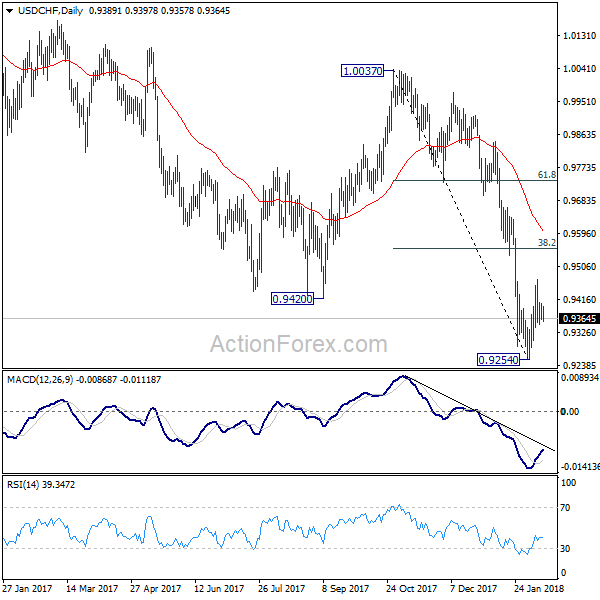

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9368; (P) 0.9386; (R1) 0.9409; More...

Intraday bias in USD/CHF remains neutral at this point. Again,here is no clear sign of trend reversal yet. Therefore, in case of another rise, we'd be cautious on strong resistance from 38.2% retracement of 1.0037 to 0.9254 at 0.9553 to limit upside and bring down trend resumption. On the downside, below 0.9339 minor support will turn bias to the downside for 0.9254. Nonetheless, firm break of 0.9553 will bring stronger rebound to 55 day EMA (now at 0.9599).

In the bigger picture, fall from 1.0342 is developing into a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

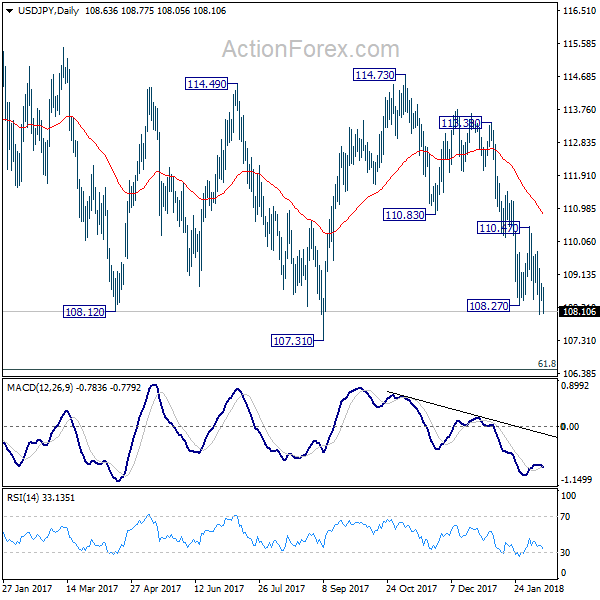

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.43; (P) 108.65; (R1) 108.88; More...

No change in USD/JPY's outlook. Intraday bias remains on the downside. Current fall from 114.73 is part of the pattern from 118.65 high and should target 106.48 fibonacci level. On the upside, break of 110.47 resistance is needed to indicate near term reversal. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2549; (P) 1.2586; (R1) 1.2617; More....

No change in USD/CAD's outlook. Intraday bias stays neutral for consolidation below 1.2687 temporary top. Further rise is in favor as long as 1.2489 minor support holds. Above 1.2687 will extend the rise from 1.2246 to 1.2919 resistance next. However, below 1.2489 will turn bias back to the downside for 1.2246 again.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 day EMA, hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Australia’s Business Confidence Hit A 9-Month High Level In January

For the 24 hours to 23:00 GMT, the AUD rose 0.43% against the USD and closed at 0.7862.

LME Copper prices rose 0.5% or $31.5/MT to $6786.5/MT. Aluminium prices declined 0.6% or $12.5/MT to $2129.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7873, with the AUD trading 0.14% higher against the USD from yesterday's close, following upbeat Australian economic data.

Data showed that Australia's NAB business confidence index advanced to a level of 12.0 in January, notching its highest level since April 2017, suggesting that firms are getting increasingly optimistic over their growth prospects in the wake of improving global economic conditions. In the previous month, the index had registered a revised reading of 10.0. Moreover, the nation's NAB business conditions index jumped to a level of 19.0 in January, pointing to strong business activity in the country and following a reading of 13.0 in the previous month.

The pair is expected to find support at 0.7831, and a fall through could take it to the next support level of 0.7788. The pair is expected to find its first resistance at 0.7895, and a rise through could take it to the next resistance level of 0.7916.

Going ahead, traders would keep a close watch on Australia's Westpac consumer confidence index for February, set to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the EUR rose 0.12% against the USD and closed at 1.2297.

In economic news, data showed that budget surplus in the US narrowed more-than-anticipated to $49.2 billion in January, compared to a surplus of $51.3 billion in the prior month. Markets were expecting for a surplus of $51.0 billion.

Meanwhile, the US President, Donald Trump unveiled a plan to spend $200.0 billion over 10 years to revamp the nation’s infrastructure.

In the Asian session, at GMT0400, the pair is trading at 1.2296, with the EUR trading slightly lower against the USD from yesterday’s close.

The pair is expected to find support at 1.2252, and a fall through could take it to the next support level of 1.2207. The pair is expected to find its first resistance at 1.2324, and a rise through could take it to the next resistance level of 1.2351.

With no macroeconomic releases across the Euro-zone today, traders would look forward to the US NFIB small business optimism index for January, slated to release later in the day.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

GBP/USD: Pound Trading Slightly Higher, Ahead Of Britain’s Inflation Numbers

.

For the 24 hours to 23:00 GMT, the GBP traded flat against the USD and closed at 1.3843.

Yesterday, the Bank of England’s (BoE) policymaker, Gertjan Vlieghe, suggested that a further hike in interest rates was probably needed if the global economic recovery and a pick-up in wages continued to offset headwinds from Brexit.

In the Asian session, at GMT0400, the pair is trading at 1.3846, with the GBP trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3803, and a fall through could take it to the next support level of 1.3759. The pair is expected to find its first resistance at 1.3883, and a rise through could take it to the next resistance level of 1.3919.

Trading trend in the Pound today is expected to be determined by UK’s consumer price inflation and producer price index data for January, slated to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.