Sample Category Title

Daily Wave Analysis: EUR/USD, GBP/USD Bullish Reversals At Fibonacci Support Levels

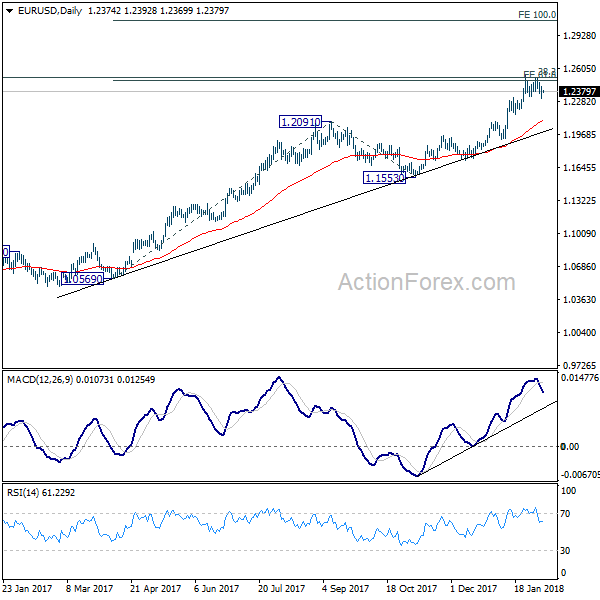

Currency pair EUR/USD

The EUR/USD bounced at the support trend line (green), which could indicate that the WXY (blue) correction within wave 4 (purple) has been completed. A break above the resistance trend lines (red) would confirm the end of wave 4 and could indicate an uptrend continuation within wave 5 (purple).

The EUR/USD The EUR/USD seems to have completed a bearish ABC (green) correction within wave 4 (purple). The bullish bounce at support (green) could indicate a wave 1 (blue) and the start a continuation of the uptrend. A break below the 100% Fib would invalidate the wave 1-2 pattern. be building a bearish ABC (green) correction within wave 4 (purple). A bullish bounce at support (green/Fibs) and bullish break above resistance (red) could start a continuation of the uptrend.

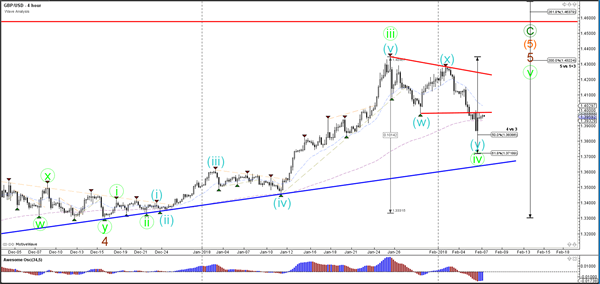

Currency pair GBP/USD

The GBP/USDbounced at the 50-61.8% Fibonacci zone which could still be part of a wave 4 (green) correction. A break above the previous top (red) could indicate a continuation rally.

The GBP/USD has probably completed a bearish ABC (grey) zigzag correction and is now building a wave 1-2 (blue) pattern.A break above resistance (red) could indicate the start of wave 3 (blue)

Currency pair USD/JPY

The USD/JPYis trapped betweenstrong support (green/blue) and resistance (red/orange). For the moment, a wave 1-2 (purple) seems the most likely but a bearish break below the bottom and 100% Fib invalidates the wave 2 (purple).

The USD/JPYneeds to break above resistance (red) before an uptrend continuation is likely.

EUR/USD Has Stabilised At 1.2388

Market movers today

The general market conditions continue to be the main focus. Yesterday we saw the first signs of stabilisation – see more below.

In terms of economic data releases it is a quiet day but we have a series of Fed speeches today with the outgoing vice-chairman Bill Dudley (voter, neutral) being the most interesting. He will speak in a moderated Q&A and will probably get quest ions on the current market situation and hopefully he will shed light on whether the Fed has become more hawkish or just more confident in its out look, including its three hikes signal for 2018 after inflation and wage growth surprised slightly to the upside. T he Fed's Evans, Kaplan and Williams also speak.

German industrial production for January should be robust following strong factory orders data yesterday. Chinese FX reserves should show a decent increase due to valuation effects as the USD weakened sharply in January (raising the value of non-USD reserves).

In Europe , the EU Commission publishes new economic forecasts at 12:00.

In Scandi it is time for Norwegian and Danish industrial product ion (see next page).

Selected market news

After a rollercoaster day, S&P500 closed 1.75% higher yesterday after the big correcion Monday and the improved sentiment is also reflected in Asian markets, where most equity indices are flashing green (although the indices in Japan and Hong Kong fell during the night after a very strong opening). S&P500 future for March is trading unchanged this morning. Also VIX recovered after a bumpy day and is now at 30, which is st ill elevated compared to what we are used to but below the 50 peak yesterday. It is worth noting that the higher equity volatility has not spilled over significantly to other markets yet – the reason is probably that investors betting on calm markets (low VIX) have lost money causing VIX to rise even further. US 10- year Treasury yield has declined a few bp this morning to 2.78% after it recovered to 2.80% yesterday. Brent oil is trading at 67.4 dollars per barrel and EUR/USD has stabilised at 1.2388.

While it is difficult to say whether the market turmoil is over for now, we still believe that the correction is more technical than fundamental and we remain overweight in equities. The business cycle st ill looks strong, as PMIs are st ill high and optimism is high among businesses and consumers. We st ill believe the central banks will only tighten monetary policy gradually despite increasing concerns in the markets that inflation is on the rise. After having struggled with low inflation for so long, central banks will likely welcome higher inflation if it comes true.

In Germany, the IG Metal l agreed to a wage settlement yesterday, which shows that wage pressure is increasing but not going through the roof yet .

The US House of Representatives passed another short-term funding bill, as the current funding bill expires tomorrow, meaning the government may shut down again on Friday. While the bill is dead on arrival in the Senate, the Senate is working on a two-year funding bill, which may be put to a vote today or tomorrow. Overall, political analysts see the risk of a government shutdown as low.

Market Update – Asian Session: Equities Reverse On A Better Day In The US

Headlines/Economic Data

General Trend: Asian markets trade mixed after Tuesday’s sell off: Nikkei and Australian markets advance, while Chinese and South Korean equities pare gains.

Kiwi (NZD) underperforms ahead of Thursday’s RBNZ rate decision

Japan

Nikkei 225 opened +1.8%; closed +0.2%

TOPIX Electric Appliances Index +1.7%, Real Estate +1.4%, Iron & Steel +1.5%

Chip-related firm Sumco [3436.JP] gains over 12% after reporting FY results and guidance

Toyota[7203.JP]: Trades higher by over 5% after raising guidance

Softbank[9984.JP]: Trades higher by over 4% ahead of expected earnings report

Kirin Holdings [2503.JP]: Trades higher amid earnings speculation

(JP) Japan Dec Labor CashEarnings y/y: 0.7% v 0.5%e; Real Cash Earnings y/y: -0.5% v 0.1% prior

(JP) BOJ announcement related to daily bond buyingoperation: raises 3-5-yr offer

(JP) Japan Fin Min Aso: Cannot comment if Coincheck was hacked by North Korea at this point - Parliament

(JP) Japan Dec Preliminary Leading Index: 107.9 v 108.1e; Coincident Index: 120.7 v 120.5e

Looking Ahead: BoJ board member Suzuki expected to comment on Thursday, along with 30-year JGB auction

Korea

Kospi opened +1.2%, later pared gain

Chip makers trade mixed: Samsung Electronics declines, while Hynix gains over 2%

(KR) South Korea to take market stabilizingmeasures if needed

Samsung, 005930.KR Considering building a 2nd chip line in South Korea, amid rising demandfor semiconductors - Korean Herald

(KR) 7 out of 10 businesses in South Korea planning a Lunar New Year bonus; Avg bonus KRW1.161M v KRW1.129M y/y - Korean press

(KR) ~30 subsidiaries of South Korea family-controlled conglomerates may benewly subject to a ban on inter-affiliate trading when antitrust watchdogtoughens a related rule - Korean press

(KR) Bank of Korea (BOK) sells KRW2.41T in 2-yr monetary stabilization bonds(MSBs) at 2.16%

China/Hong Kong

Hang Seng opened -0.3%, Shanghai Composite +0.1%

Shanghai pares opening gains amid weakness in property sector

Hang Seng Information Tech Index +3.5%, Consumer Goods +1.7%, Financials +1.7%, Materials +1.6%,Energy +1.6%

(CN) China Ambassador to US Tiankai: despite misjudgment from some in the United States, China will remain confident in its path of development and those hoping otherwise should face the reality – CD

(CN) China PBoC: Skips OMO (10th straightsession) v skipped prior; Net drain CNY100B v CNY80B prior

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.2882 V 6.3072 PRIOR

(CN) China banks have raised mortgage rates in several cities - Chinese press

(CN) China to probe fake information from listed companies - Xinhua

(CN) China PBOC sells CNY120B in 3-month MOF Deposits at 4.50%

(CN) China files new challenges on US tariffs on solar panels and washing machines at the World Trade Organization - financial press

Looking Ahead: China Jan FX Reserves due to be released later today

China Jan Trade Balance may be released on Thursday

Australia/New Zealand

ASX 200 opened +0.5%; closed %

ASX 200 Resources Index+1.9%, Energy +1.7%, Consumer Discretionary +1.8%, Financials +0.2%; Utilities-0.8%

Rio Tinto [RIO.AU]: Trades higher by over 3% ahead of later today earnings report

Commonwealth Bank [CBA.AU]: Pares gain seen after H1 earnings report

(NZ) NEW ZEALAND Q4UNEMPLOYMENT RATE: 4.5% V 4.7%E (Lowest Level Since Financial Crisis)

(AU) Australia Jan Foreign Reserves (A$): 65.3B v 85.4B prior

CBA.AU Reports H1 (A$) cash profit4.8B v 5.2Be; Net interest income 9.25B v 9.3Be; Rev 21.3B, +2% y/y

(AU) Australia AOFM sells A$600M v A$600M indicated in Nov 2028 bonds, avgyield 2.8862%, bid to cover 5.43x

(AU) Australia PM Turnbull: No plans to allow big 4 Australia bank mergers

(AU) Australia Jan AIG Performance of Construction Index: 54.3 v 52.8 prior

Looking Ahead: Reserve Bank of New Zealand(RBNZ) rate decision due on Thursday

Other Asia

(IN) Reserve Bank of India (RBI) policy meeting due later today (no changes expected)

North America

US equity markets ended higher: Dow +2.3%, S&P500 +1.7%, Nasdaq +2.1%, Russell 2000+1.1%

S&P500 Materials +3.2%, Technology +2.8%

Wynn Resorts [WYNN]: Steve Wynn has resigned as CEO and Chairman; promotes Matt Maddox CEO and Boone Wayson Chairman; effective immediately

Supervalu [SVU]: Activist investor Blackwells (~4.4% stake) said to urge board to explore either sale or breakup - US financial press

(US) Treasury Sec Mnuchin: administration is monitoring markets situation but long-term fundamentals are very strong,markets are functioning normally in terms of liquidity; Correct to say that I support a strong Dollar; US debt plan hasn't impacted markets at the moment; debt market is one of the most liquid in the world

(US) Pres Trump: if we don't get rid of immigration loopholes, 'let's have a shutdown'

(US) Fed's Bostic (2018 voter, dove): See slow gradual pace of rate rise, if growth is robust

(US) US House has votes to pass stopgap funding bill to fund government until March 23rd; final vote 245 to 182; The bill now moves to the senate, where lawmakers are expected to rewrite the measure to eliminate higher defense spending and potentially attach a bipartisan deal to raise budget caps.

(US) Weekly API Oil Inventories: Crude: -1.1M v +3.2M prior

Looking Ahead: Fed’s Dudley due to speak during NY morning, Weekly DOE Crude Oil Inventories to be released

Europe

(EU) European Commission wants to punish UK non-compliance during the Brexit transition by summarily cutting off the country’s access to parts of the single market - FT citing draft treaty

(IE) Ireland is pushing for a settled “legal text” over the Brexit border question as early as next month in a move that threatens once again to derail the Brexit negotiations – Telegraph

(UK) National Institute of Economic and Social Research (NIESR): Forecasts UK 2018 and 2018 GDP growth at 1.9% vs 1.7% in Nov

Levels as of 01:00ET

Nikkei225 +0.2%, Hang Seng +0.4%; Shanghai Composite -1.5%; ASX200 +0.8%, Kospi -1.4%

Equity Futures: S&P500 -0.8%; Nasdaq100 -0.9%,Dax -0.6%; FTSE100 -1.3%

EUR 1.2393-1.2372; JPY 109.71-109.14; AUD 0.7909-0.7878;NZD 0.7346-0.7305

Apr Gold +0.2% at $1,332/oz; Mar Crude Oil +0.8% at $63.88/brl; Mar Copper -0.2% at $3.21/lb

Australia’s Construction Sector Activity Accelerated In January

For the 24 hours to 23:00 GMT, the AUD rose 0.44% against the USD and closed at 0.7904.

LME Copper prices rose 0.1% or $10.0/MT to $7060.0/MT. Aluminium prices declined 0.3% or $6.0/MT to $2196.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7882, with the AUD trading 0.28% lower against the USD from yesterday's close.

Data released overnight indicated that Australia's AiG performance of construction index advanced to a level of 54.3 in January, compared to a reading of 52.8 in the prior month.

The pair is expected to find support at 0.7842, and a fall through could take it to the next support level of 0.7802. The pair is expected to find its first resistance at 0.7916, and a rise through could take it to the next resistance level of 0.7950.

Looking forward, Australia's NAB business confidence index for 4Q, slated to release overnight, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Germany’s Factory Orders Soared To A 4-Month High Level In December

For the 24 hours to 23:00 GMT, the EUR slightly rose against the USD and closed at 1.2380, following a pair of upbeat economic releases in Germany.

Data revealed that Germany's seasonally adjusted factory orders rebounded more-than-anticipated by 3.8% MoM in December, rising by the most in 4 months, thus boosting optimism over the health of the nation's industrial sector. Factory orders had recorded a revised drop of 0.1% in the prior month, while markets were expecting for an advance of 0.7%. Additionally, the nation's construction sector expanded at its fastest pace in nearly 7 years in January, after the Markit construction PMI climbed to a level of 59.8, compared to a reading of 53.7 in the preceding month.

Macroeconomic data showed that trade deficit in the US widened to a 9-year high level of $53.1 billion in December, as growth in imports outpaced that of exports. Market participants had expected the nation's trade deficit to widen to $52.1 billion, after recording a revised deficit of $50.4 billion in the prior month. Additionally, the nation's JOLTS job openings dropped more-than-expected to a level of 5811.0K in December, compared to a revised reading of 5978.0K in the prior month, while investors had anticipated for a fall to a level of 5961.0K.

In the Asian session, at GMT0400, the pair is trading at 1.2384, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.2321, and a fall through could take it to the next support level of 1.2257. The pair is expected to find its first resistance at 1.2441, and a rise through could take it to the next resistance level of 1.2497.

Moving ahead, investors would look forward to Germany's industrial production data for December as well as the European Commission's economic growth forecast report, both scheduled to release in a few hours. Moreover, the US MBA mortgage applications followed by consumer credit data for December, set to release later in the day, will be on investors' radar.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Pound Trading Marginally Higher This Morning

For the 24 hours to 23:00 GMT, the GBP declined 0.06% against the USD and closed at 1.3954.

In the Asian session, at GMT0400, the pair is trading at 1.3960, with the GBP trading a tad higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3864, and a fall through could take it to the next support level of 1.3768. The pair is expected to find its first resistance at 1.4028, and a rise through could take it to the next resistance level of 1.4096.

Going ahead, traders would focus on UK’s Halifax house prices data for January, due to release in a few hours.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Japanese Yen Reverses Its Losses In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.89% against the JPY and closed at 109.70.

In the Asian session, at GMT0400, the pair is trading at 109.33, with the USD trading 0.34% lower against the JPY from yesterday’s close.

Earlier today, data indicate that Japan’s flash leading economic index eased more-than-anticipated to a level of 107.9 in December, compared to a reading of 108.3 in the prior month, while investors had envisaged for a fall to a level of 108.1. On the contrary, the nation’s preliminary coincident index advanced to a level of 120.7 in December, surpassing market expectations for a rise to a level of 120.5. The index had recorded a level of 117.9 in the previous month.

The pair is expected to find support at 108.62, and a fall through could take it to the next support level of 107.91. The pair is expected to find its first resistance at 109.88, and a rise through could take it to the next resistance level of 110.43.

Going ahead, investors would closely monitor Japan’s trade balance (BOP basis) for December and the Eco-Watchers survey for January, both due to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Swiss Franc Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.48% against the CHF and closed at 0.9361.

In the Asian session, at GMT0400, the pair is trading at 0.9355, with the USD trading 0.06% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9309, and a fall through could take it to the next support level of 0.9262. The pair is expected to find its first resistance at 0.9400, and a rise through could take it to the next resistance level of 0.9444.

Amid no major macroeconomic releases in Switzerland today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canada’s Ivey–PMI Declined In January, International Merchandise Trade Deficit Unexpectedly Widened In December

For the 24 hours to 23:00 GMT, the USD declined 0.33% against the CAD and closed at 1.2498.

In economic news, Canada's seasonally adjusted Ivey–PMI fell to a level of 55.2 in January, compared to a reading of 60.4 in the prior month. Furthermore, the nation's international merchandise trade deficit surprisingly widened to C$3.19 billion in December, amid a surge in imports and confounding market expectations for the deficit to narrow to C$2.32 billion. The nation had registered a revised trade deficit of C$2.71 billion in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2513, with the USD trading 0.12% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2481, and a fall through could take it to the next support level of 1.2449. The pair is expected to find its first resistance at 1.2556, and a rise through could take it to the next resistance level of 1.2599.

Ahead in the day, traders would keep a close watch on Canada's building permits data for December.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2315; (P) 1.2374 (R1) 1.2436; More....

EUR/USD is still staying in consolidation below 1.2537 and intraday bias remains neutral. As long as 1.2222 support holds, further rise is in favor. Sustained break of 1.2494/2516 will target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.