Sample Category Title

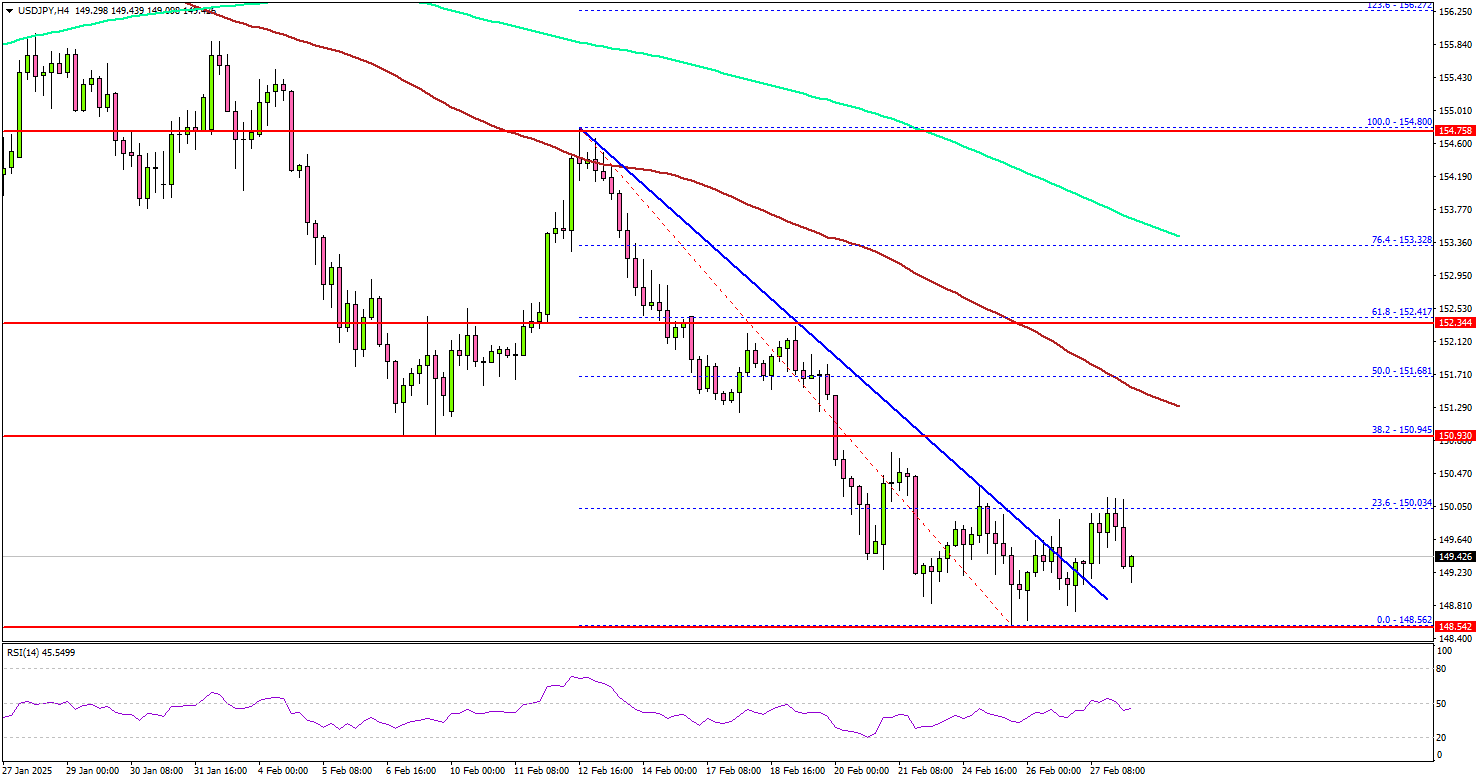

USD/JPY Eyes Rebound: Will Market Optimism Fuel Increase?

Key Highlights

- USD/JPY dipped toward the 148.50 support zone before a minor recovery.

- It cleared a key bearish trend line with resistance at 149.20 on the 4-hour chart.

- EUR/USD failed again to clear the 1.0535 resistance.

- GBP/USD is consolidating gains above the 1.2600 support.

USD/JPY Technical Analysis

The US Dollar extended losses below the 150.00 support zone against the Japanese Yen. USD/JPY traded close to the 148.50 level before the bulls appeared.

Looking at the 4-hour chart, the pair settled below the 151.20 pivot level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). It is now attempting a recovery wave above the 149.00 level.

There was a break above a key bearish trend line with resistance at 149.20 on the same chart. On the upside, the pair seems to be facing hurdles near the 150.50 level.

The next major resistance is near the 151.00 level. The main resistance is now forming near the 151.50 zone and the 100 simple moving average (red, 4-hour). A close above the 151.50 level could set the tone for another increase. In the stated case, the pair could even clear the 152.50 resistance.

On the downside, immediate support sits near the 149.00 level. The next key support sits near the 148.50 level. Any more losses could send the pair toward the 147.20 level.

Looking at EUR/USD, the pair failed to gain pace for a move above the 1.0535 resistance and corrected some gains.

Upcoming Economic Events:

- US Personal Income for Jan 2025 (MoM) - Forecast +0.3%, versus +0.4% previous.

- US Core Personal Consumption Expenditure for Jan 2025 (MoM) - Forecast +0.3%, versus +0.2% previous.

S&P 500 Index Wave Analysis

- S&P 500 index broke support zone

- Likely to fall support level 5800.00

S&P 500 index recently broke the support zone between the key support level 5925.00 (low of the previous waves a and c), the support trendline of the daily up channel from September and the 61.8% Fibonacci correction of the upward impulse from January.

The breakout of this support zone accelerated the active short-term correction ii – which belongs to the higher raves 3 and (C).

S&P 500 index can be expected to fall to the next support level 5800.00, a low of the previous minor corrections a and 2.

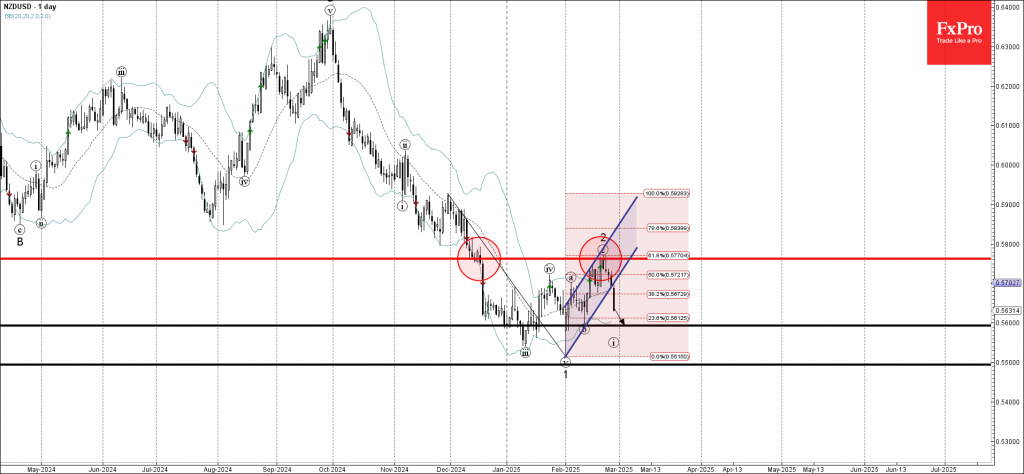

NZDUSD Wave Analysis

- NZDUSD under bearish pressure

- Likely to fall support level 0.5600

NZDUSD currency pair is under bearish pressure after the earlier breakout of the support trendline of the daily up channel from the start of February.

The breakout of this up channel continues the active impulse wave 3, which started earlier from the key resistance level 0.5760 (former support from December), intersecting with the aforementioned up channel.

NZDUSD currency pair can be expected to fall to the next support level 0.5600, a low of the previous minor correction b.

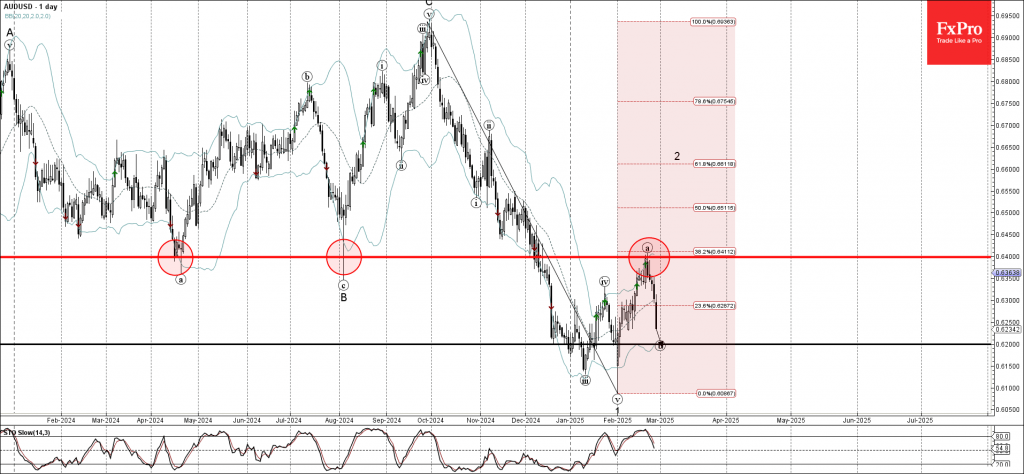

AUDUSD Wave Analysis

- AUDUSD falling inside wave b

- Likely to fall support level 0.6200

AUDUSD currency pair continues to fall inside the b-wave which started earlier from the major resistance level 0.6400 (former strong support from April and August of 2024).

The resistance level 0.6400 was strengthened by the upper daily Bollinger Band and by the 38.2% Fibonacci correction of the downward impulse from last October.

Given the strongly bullish US dollar sentiment and strong daily downtrend, AUDUSD currency pair can be expected to fall to the next support level 0.6200, the target price for the completion of the active wave b.

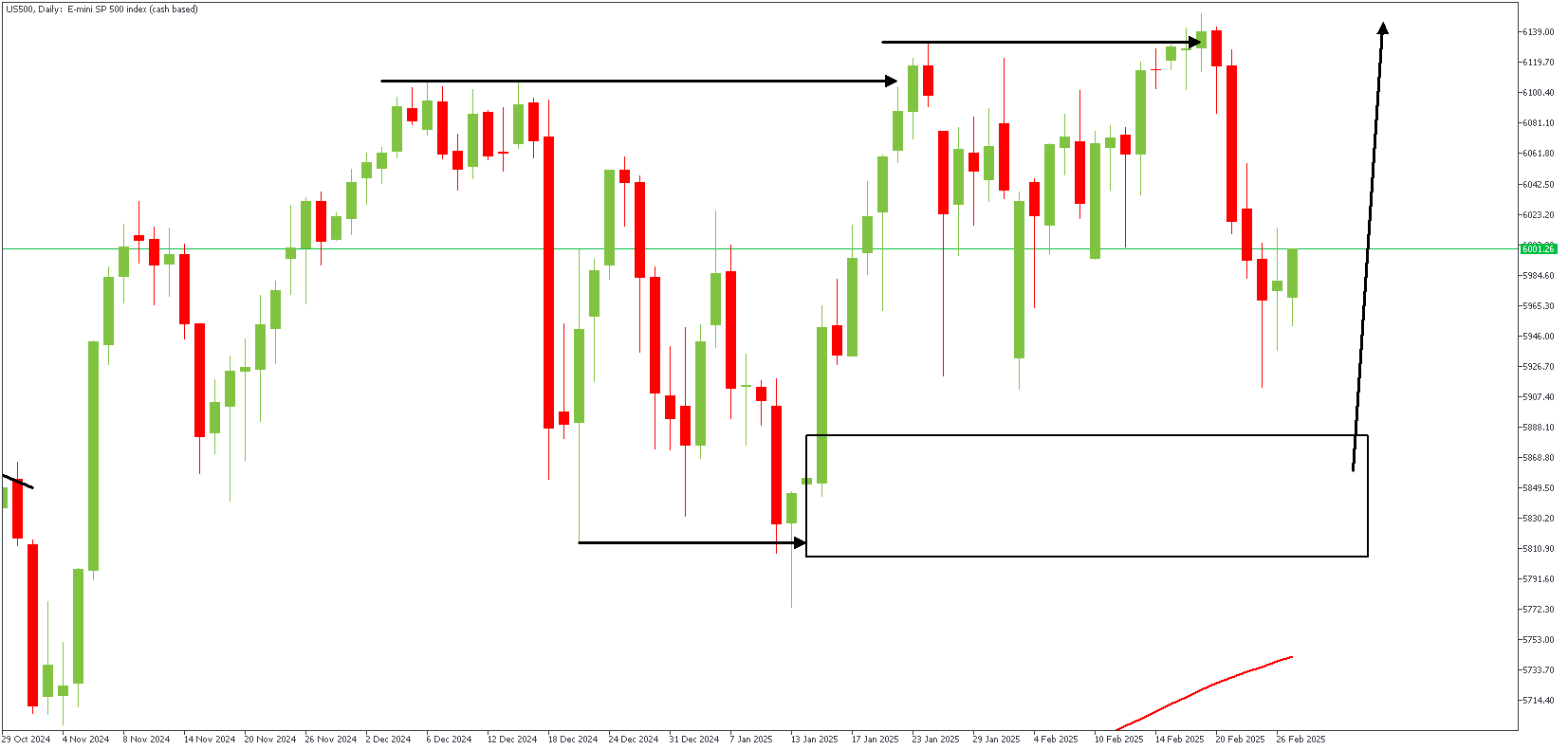

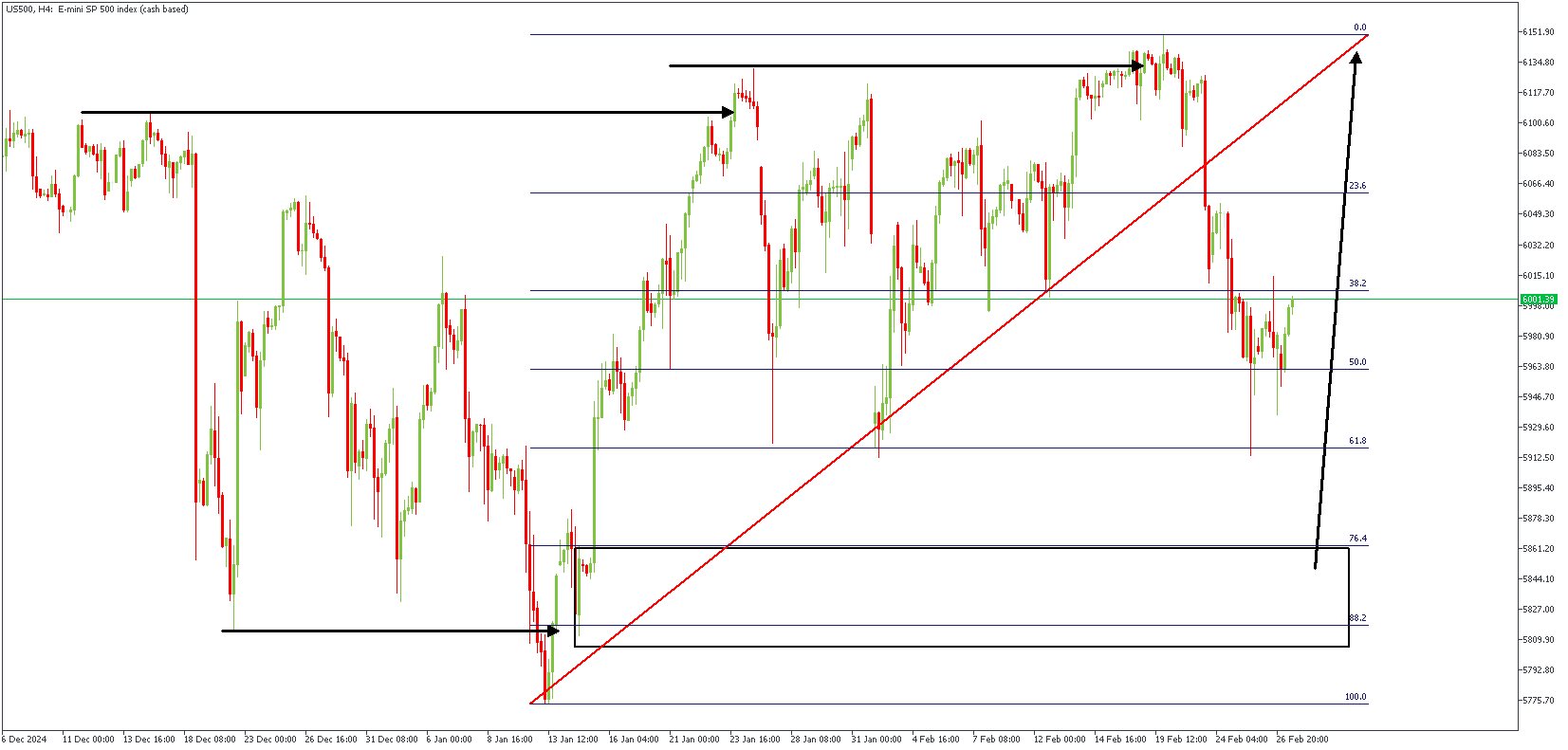

US500 Technical Analysis

The US Dollar (USD) is slightly stronger today, but gains against major currencies are limited, and most currencies stay within their established ranges. European stocks are down slightly, while US stock futures look better. Bond markets are weaker, with Treasury yields rising by 4-5bps. The Japanese Yen (JPY) and Swiss Franc (CHF) are underperforming, while the Mexican Peso (MXN) and Canadian Dollar (CAD) are doing better, possibly due to uncertainty over President Trump's tariff deadlines. Month-end demand may support the USD, but it's struggling to make significant gains. Technical trends have weakened slightly, with the USD Index (DXY) trading below its 100-day moving average. The market is also sensitive to weak US economic data, like the recent drop in Consumer Confidence.

US500 – D1 Timeframe

On the daily timeframe chart of US500, we see the initial liquidity sweep from the highlighted low right before the price broke above the previous high. The drop-base-rally demand zone at the trough of the SBR pattern is situated near the 76% Fibonacci retracement level, increasing the likelihood of a bullish reaction.

US500 – H4 Timeframe

The FVG (Fair Value Gap) left behind by the structure's double break needs to be filled, as hinted by the presence of liquidity at the equal lows on the 4-hour timeframe chart of US500. These serve as a confluence in favor of the bullish sentiment, and given the Fibonacci retracement factor in the equation, there is a high chance the outcome is bullish.

Analyst's Expectations:

- Direction: Bullish

- Target- 6144.04

- Invalidation- 5771.95

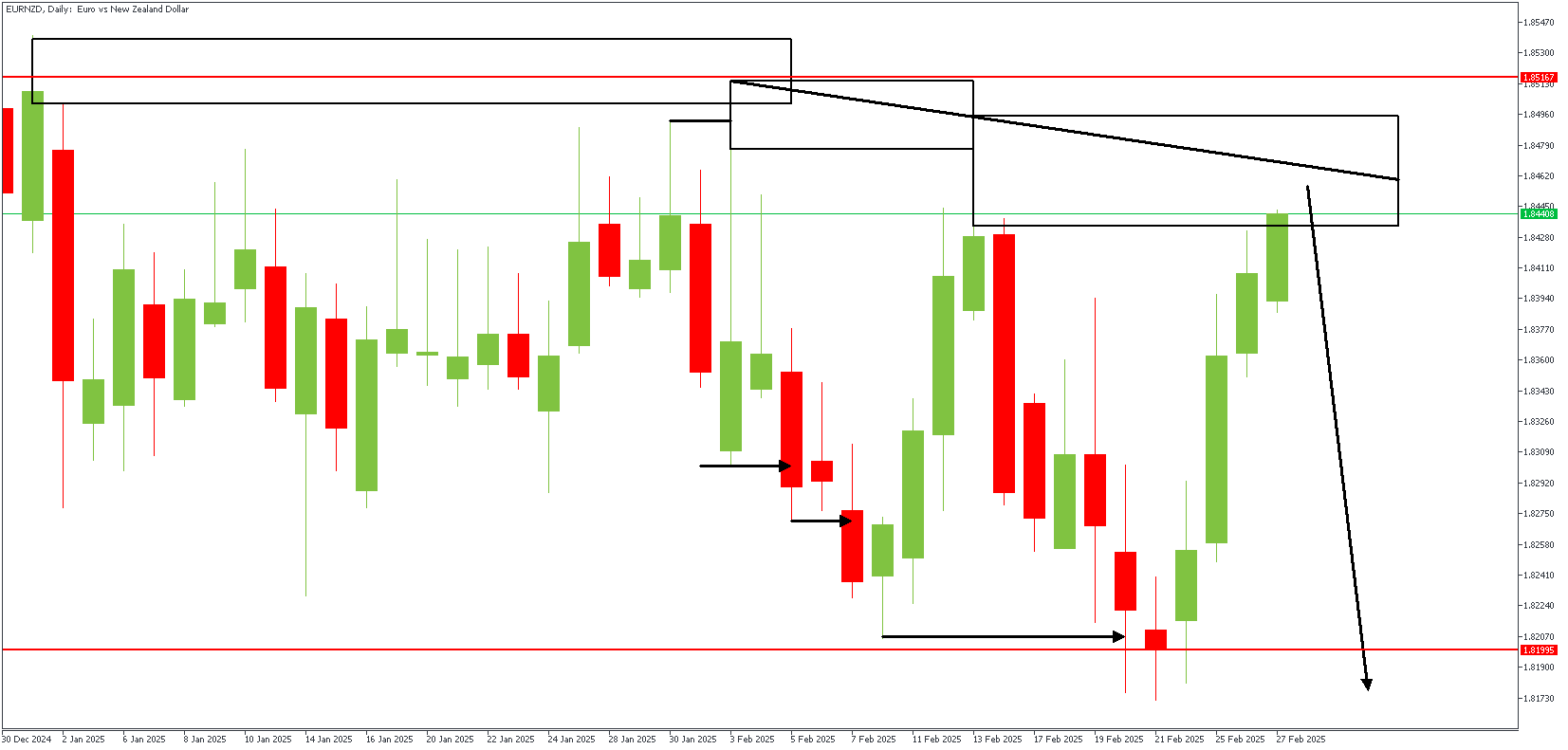

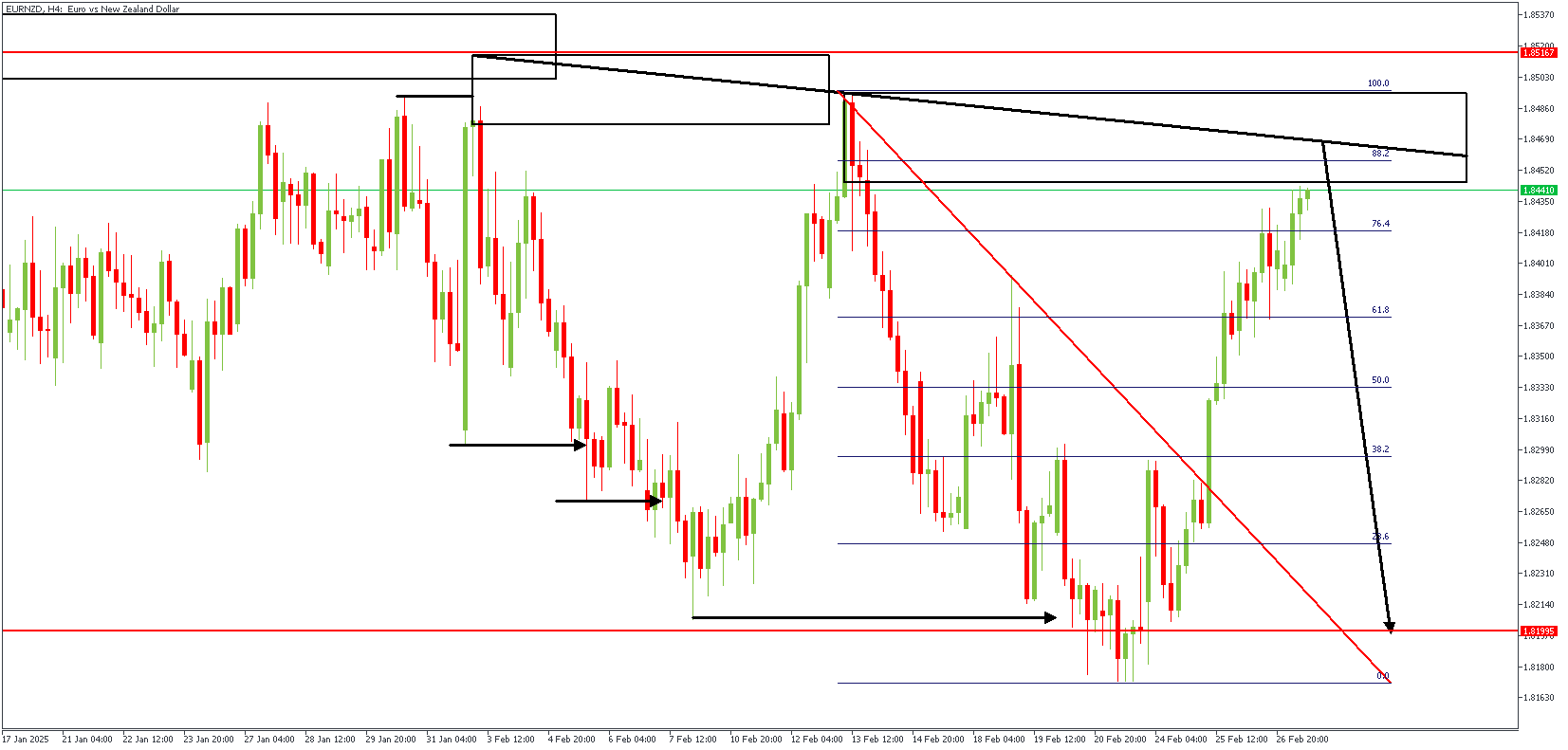

EURNZD Technical Analysis

EURUSD may struggle to stay above 1.05 for long as market dynamics shift. Concerns over a US economic slowdown have led to a slightly more dovish outlook for the Federal Reserve. The currency pair's direction will depend on future Fed and European Central Bank (ECB) policy moves and potential EU tariffs. Analysts expect tariffs to take effect in April, adding pressure on the euro. Currently, EURUSD is trading within a 1.0450–1.0530 range. Month-end portfolio adjustments could trigger some selling significantly, as eurozone equities have outperformed US stocks.

EURNZD – D1 Timeframe

At the far left of the attached price action chart on the daily timeframe chart of EURNZD, we see the initial supply zone followed by an SBR pattern, the peak of which was the rejection from the supply zone. The presence of trendline resistance at the newly formed supply region is the basis for the bearish sentiment.

EURNZD – H4 Timeframe

The 4-hour timeframe chart of the EURNZD pair's price action further reveals that the supply zone overlaps the 88% Fibonacci retracement level, with the liquidity from the recent high already swept. In this case, the overall sentiment aligns with the lower timeframe price action.

Analyst's Expectations:

- Direction: Bearish

- Target- 1.81995

- Invalidation- 1.85167

Fed’s Schmid: Inflation risks rising, but growth concerns loom

Kansas City Federal Reserve President Jeff Schmid cautioned in a speech today there were "sharp upward movement" in some measures of expected inflation in the past two months.

While acknowledging the imperfections and volatility of survey-based inflation expectations, Schmid emphasized that now is "not the time to let down our guard," given inflation’s recent history of reaching a four-decade high.

He expressed reluctance to dismiss the recent uptick in expectations as a "one-off transitory developments", stressing that Fed must remain vigilant against a resurgence in inflationary pressures.

At the same time, Schmid noted that the economic outlook is highly uncertain. Feedback from businesses in his district, along with some recent economic data, indicates that Fed might need to carefully "balance inflation risks against growth concerns."

Sunset Market Commentary

Markets

Trump’s tariff threat against Europe weighed on European risk sentiment with key indices losing between 0.50% and 1.50%. In the first cabinet meeting of his second term, the US president suggested that a plan was made and that then announcement would follow soon: “It will be 25% generally speaking, and that will be on cars and all other things.” The damage for the euro could have been bigger with EUR/USD slipping from just below the 1.0533 resistance area towards 1.0460-1.0480 until the early morning eco data releases. European yields were barely impacted. The European eco calendar contained sticky Spanish and Belgian inflation together with a slightly stronger economic confidence indicator by the EC. Minutes of the previous ECB meeting bolster the case for more rate cuts by the ECB beyond March as downside growth risks prevail, though at a slower pace. ECB Schnabel and Wunsch earlier hinted in the direction of pausing in April. Markets ignored today’s European input.

Volatility intensified in the run-up to the US opening bell. First, US eco data added to the recent shift from Goldilocks to stagflation with weekly jobless claims unexpectedly spiking from 220k to 242k (matching highest since early October 2024; DOGE at work?!), US core capital goods shipments (input for GDP calculation) declining (instead of the hoped-for increasing) by 0.3% M/M in January and the core PCE priced index facing an upward revision for Q4 (2.7% from 2.5%). The impact of the data mainly showed in a spike lower in US yields, but those moves didn’t last. Next came US President Trump who clarified yesterday’s messy communication on tariffs against neighboring countries Mexico and Canada. They will go into effect on March 4 instead of April 2 like Trump yesterday falsely suggested. China will also be charged an additional 10% tariff from that date onwards. Currencies of (potential) tariff victims suffered the biggest setback with EUR/USD extending its slide towards 1.0420. USD/CAD moves from 1.4360 to 1.4430 and USD/MXN from 20.35 to 20.55. US stock futures handed in some of the earlier gains because of the third element at play this morning: Q4 Nvidia earnings. Strong results were at first met by some skepticism as market gotten acquainted to stellar rather than good numbers. In pre-market trading, investors are nevertheless giving the thumbs up, supporting the broader equity market.

News & Views

Belgian inflation (CPI; national methodology) rose in February by 0.2% M/M and 3.55% Y/Y, easing from 1.39% M/M and 3.55% Y/Y in January. Core inflation excluding energy products and unprocessed food was little changed at 3.1% Y/Y. In a monthly perspective, gas prices rose 2.6%, electricity prices 1.5%, flowers and plants’ prices increased 8% M/M with the price of water consumption rising 5.5% due to a price increase in the Walloon region. Prices for clothes declined 4.3% M/M. In a broader perspective, services prices inflation rose 4.34% Y/Y from 4.13%. Rents inflation eased slightly (3.3 from 3.41%). Food inflation stood at 2.22% from 2.54%. Due to a base effect from the removal of household premiums last year, energy inflation also eased from 15.89% Y/Y to 8.71% Y/Y this month. The first estimate of according to European harmonized index (HICP) amounts to 4.4% (unchanged). A separate report, showed that hourly labour costs in the economy in Q4 increased by 2.2% at an annual basis.

Swiss Q4 GDP growth (adjusted for sporting events) was solid, accelerating from 0.2% Q/Q to 0.5% Q/Q. Activity was 1.2% higher Y/Y. In an expenditure approach, domestic demand was the main driver with a solid performance of private consumption and government consumption, both adding 0.5% Q/Q, slightly above historical averages. Construction investment also rose 0.5% Q/Q. After two negative quarters, spending on equipment and software investment grew 1.0% Q/Q. For 2024 as a whole, adjusted growth is estimated at 0.9% Y/Y, from 1.2% in the previous year. In a production approach, decent growth was recorded in manufacturing (1.9%) due to the chemicals and the pharmaceutical industry while accommodation and food services (+3.5%) profited from international tourism. Retail trade also performed well (1%) for the second consecutive quarter. With inflation still extremely low (0.4% Y/Y in Jan) and plenty of uncertainty looming, the solid Q4 data probably won’t prevent the SNB from further cutting its policy rate in March 20 from 0.5% now to 0.25%. EUR/CHF holds within the 0.932/0.952 range.

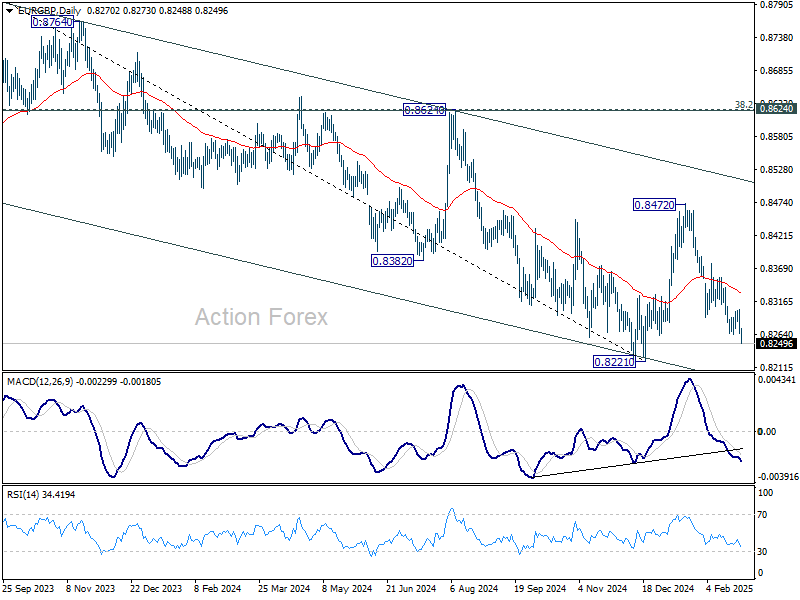

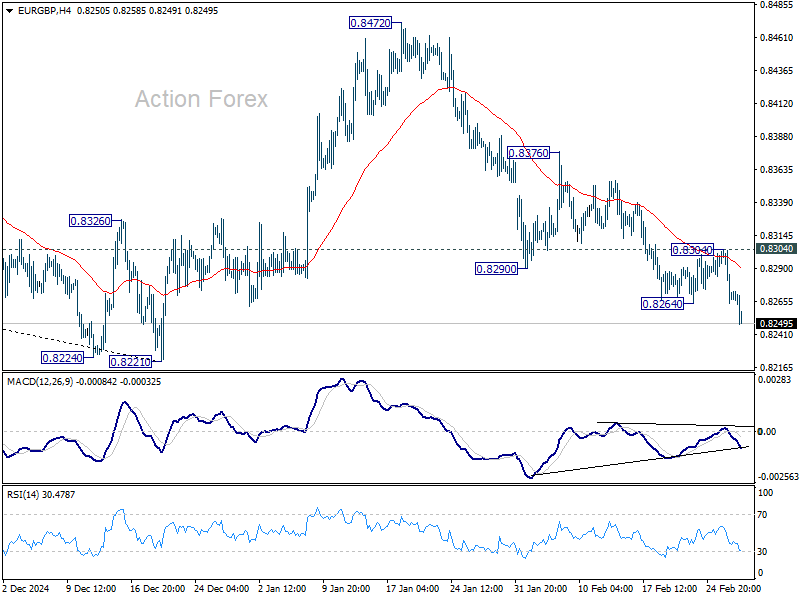

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8256; (P) 0.8280; (R1) 0.8295; More...

EUR/GBP's fall from 0.8472 resumed by breaking through 0.8264 temporary low. Intraday bias is now back on the downside for retesting 0.8201/21 key support level. Firm break there will carry larger bearish implications. For now, risk will stay on the downside as long as 0.8304 resistance holds, in case of recovery.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8431) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.