Sample Category Title

Currencies: Dollar Survives Mediocre US Payrolls

Sunrise Market Commentary

- Rates: Focus on US inflation this week

US Treasuries eventually lost some ground on Friday despite disappointing headline payrolls and non-manufacturing ISM. Today's eco calendar contains EMU EC confidence data and a speech by Atlanta Fed Bostic. The latter has market-moving potential, but investors are already eying US inflation releases at the end of the week. Inflation expectations are rising. - Currencies: Dollar survives mediocre US payrolls

On Friday, the dollar was hardly affected by a disappointing US payrolls report. The overall picture of the US currency remains fragile, but EUR/USD 1.2092 resistance wasn't broken. We start the week with a neutral bias on the dollar. US price data later this week may guide the next directional move of the US currency.

The Sunrise Headlines

- US stock markets ended the week with a bang, adding 0.8% to close the first week of the year 2.3% to 3.3% higher. Asian risk sentiment remains positive overnight with Japan closed for coming-of-age day.

- San Francisco Fed Williams, FOMC voter, said that something like three rate hikes this year made sense, confirming the Fed's median view. Philly Fed Harker, no voter, revealed his dovish feathers, putting forward 2 hikes in 2018.

- Britain is pushing to remain under EU regulation for medicines after Brexit, the latest sign ministers want to stay close to Europe in some sectors despite the bloc warning the UK cannot “cherry-pick” parts of the single market.

- ECB Weidmann told Spain's El Mundo newspaper he believes setting a clear end for institution's bond-buying program is justifiable. Monetary policy will remain very expansive, even after the end of net purchases, he added.

- Faster factory inflation and higher industrial profits in the past year have created space for an increase in overall interest rates, PBOC researcher Ji Min said, according to a report by China Daily.

- China's FX reserves rose to their highest in more than a year in December ($3.14 tn), blowing past economists' estimates, as tight regulations and a strong yuan continued to discourage capital outflows.

- Today's eco calendar contains EC confidence indicators. Fed governors Bostic, Williams and Rosengren are scheduled to speak

Currencies: Dollar Survives Mediocre US Payrolls

Dollar ‘survives' mediocre payrolls

The dollar was in the defensive early last week, but regained a few ticks going into the payrolls. Investors were apparently positioned a bit too much USD short. Employment growth disappointed, but the key wage data were as expected. The dollar spiked briefly lower upon the release. EUR/USD jumped to the 1.2080 area, but the 1.2092 range top was again left intact. The dollar soon reversed post-payrolls' loss. EUR/USD even returned below the pre-payrolls' level and closed the session at (1.2029). USD/JPY failed to regain the pre-payroll level, but still closed the day in positive territory (113.05). So, the payrolls disappointed but caused little damage for the dollar.

The dollar shows no clear trend overnight. EUR/USD was initially well bid, maybe supported by hawkish comments from ECB Weidmann. However, the moved had no strong legs. EUR/USD trades again in the 1.2020 area. USD/JPY maintains a cautious bid as global risk sentiment stays constructive. The eco calendar is only modestly interesting today. EC confidence data will confirm the strong growth momentum in the region. Fed members Bostic, Williams and Rosengren speak. We keep an eye at the comments of Fed's Bostic, but don't expect them to really change the outlook on the Fed's intentions in 2018. We start the week with a neutral dollar bias. Slightly disappointing payrolls didn't cause additional damage and EUR/USD 1.2092 resistance survived. This week's US price/CPI data might be a next tipping point for the dollar. Recently, the greenback suffered as the global recovery might force other major CB's (including ECB) to join policy normalisation. For now, we maintained the working hypothesis that enough good news on the euro/'bad news' on the dollar was discounted and that a sustained break beyond the 1.2092 cycle top is not evident.

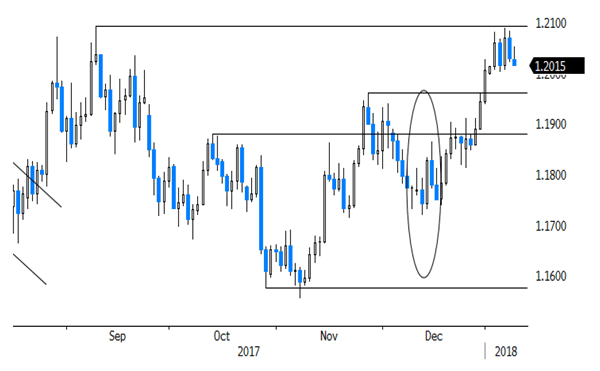

Sterling was in better shape compared to earlier last week on Friday. EUR/GBP returned below 0.89, but stayed within established ranges. This weekend, there was a lot of talk about a UK Cabinet reshuffle. If May succeeds, it might be an indication that she is regaining some grip on her party. Signs of more political stability in the UK might be slightly supportive for sterling. However, we don't see a strong case for a sustained sterling rebound (against EUR) anytime soon. GBP Medium Term: Recent UK data were mixed. We don't expect the BoE to raise rates soon. EUR/GBP 0.8700/60 support looks solid. Euro strength or soft UK data might keep EUR/GBP 0.90 on the radar further down the road. We keep a EUR/GBP buy-on-dips in case of return action to 0.87

EUR/USD 1.2092 range top survives despite disappointing payrolls

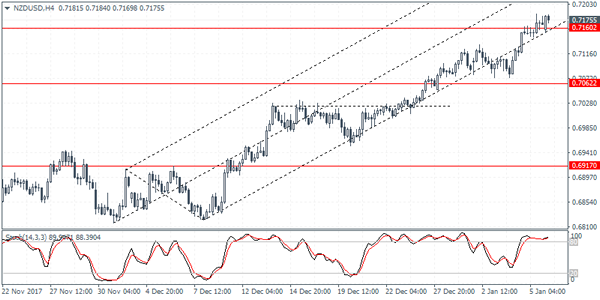

NZDUSD Intraday Analysis

NZDUSD (0.7155): The New Zealand dollar managed to complete its rally to the target area of 0.7160. Price action is showing some signs of exhaustion to the rally at this level. This is seen by the lower highs formed on the Stochastics oscillator. A convincing close below the previous low of 0.7144 could confirm the downside bias in price. The first support level that could be targeted comes in at 0.7062 which could mark the initial correction. However, further declines cannot be ruled out if price breaks down below this support. Expect to see a modest rebound off the 0.7062 with NZDUSD likely to make a lower high ahead of further declines to 0.6917.

USDJPY Intraday Analysis

USDJPY (113.21): USDJPY extended gains for three consecutive days, with Friday's session briefly rallying to highs of 113.30 before the dollar eased back to settle at 113.08. Price action remains trading within the consolidation pattern on the daily chart, as resistance at 114.07 remains a major hurdle. On the 4-hour chart, the reversal coincides with a medium-term trend line that has held on two past occasions. A continued follow through to the downside could mean that USDJPY could potentially signal declines to 112.04 level of support. The bias shifts to the upside if the currency pair can post a bullish close above the falling trend line.

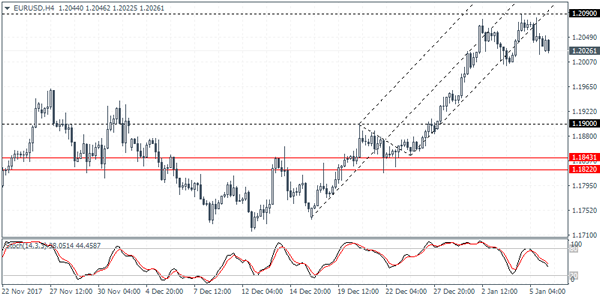

EURUSD Intraday Analysis

EURUSD (1.2026): The EURUSD closed with some losses on Friday and in the process, price action formed an inside bar near the current highs above 1.20. The break out from this inside bar could potentially spell the next stage of gains or declines in the common currency. On the 4-hour chart, the EURUSD is seen falling away from the lower median line after price broke to the downside. With the exception of some consolidation taking place here, the common currency could be seen extending the declines towards 1.190 at the minimum in the near term. However, this scenario could change on a bullish close above 1.2090. This would keep the upside momentum intact although, in the longer term, the possibility of a correction to the rally remains high.

USD Consolidates Above 91.50 – Is A Rebound On The Way?

The U.S. dollar index settled at 91.74 on Friday, after price action was seen consolidating above the 91.50 handle over the past four daily sessions. On Friday, the December nonfarm payrolls data was released. Although not a blockbuster report, the payrolls showed that wages edged higher to 2.5% on the year, the unemployment rate held steady for a third consecutive month at 4.1%. The pace of jobs created in December was however smaller than expected.

The Greenback, which has been in a strong decline over the past few months managed to stabilize. However, a lot remains up in the air regarding how the USD reacts from here on.

Economic data today is relatively quiet, meaning a slow start to the week. Data from the Eurozone will see the release of the German factory orders which are expected to rise at a slower pace. Bank of Canada will be releasing its business outlook survey. The report comes a week ahead of the BoC meeting next week. From the U.S., FOMC members Bostic and Williams will be speaking later in the day.

EURO Intraday Softness Below 1.2030 Level

The euro has slipped back below the 1.2030 level against the U.S dollar, after another failed attempt at the 2017 price-high at 1.2093 on Friday. The EURUSD currently trades around the 1.2020 level, as three technical failures below the 2017 price-high weigh heavily on the pair. Traders also remain cautious on Monday, as German politics comes back into the spotlight, with Angela Merkel trying to salvage a coalition deal between the SPD and CDU parties. During the upcoming European trading session, we see the release of the Eurozones Sentix Investor’s Survey and EU November Retail Sales data.

The EURUSD pair is likely to see intraday softness below the 1.2030 level, sellers may target the 1.1989 and 1.1958 support levels.

Should EURUSD price-action move above the 1.2030 zone, intraday resistance is found at the 1.2070 and 1.2093 levels.

USDJPY Buyers Still In Charge Above 113.10

The U.S dollar continues to trade well above the 113 handle against the Japanese yen, as rising Asian stock markets boost risk-on trading sentiment on Monday. The USDJPY pair hit 113.46 on Friday, following the release of the December Non-farm payrolls job report. Going forward, buyers will now need to break the Friday high and close price-action above the 113.60 level, and then look towards challenging the 114.40 region. With a lack of macroeconomic data from the U.S and Japan on Monday, the U.S dollar index will likely be the key driver for the USDJPY pair.

Further upside is expected while price-action trades above the key 113.10 level, bullish targets for the USDJPY pair remain 113.60 and 114.40.

Should the USDJPY pair start to trade below the 113.10 technical level, further selling towards 112.70 and 112.30 should be expected.

European Sentiment Indicators Carry Weight On Monday

A batch of European sentiment indicators will headline an otherwise quiet day of trade on Monday. The first full week of the year is expected to see a deluge of economic data, culminating in Chinese and US inflation figures.

Action begins at 07:00 GMT with a report on German factory orders. November bookings are expected to rise 0.8% month-on-month, following a gain of 0.5% the previous month.

Switzerland's Federal Statistical Office will release official inflation figures at 08;15 GMT. The Consumer Price Index (CPI) is expected to come in at 0.8% year-over-year in December, unchanged from the previous month.

European sentiment data will be released at 10:00 GMT, including the Sentix investor confidence index.

Separately, the European Commission's statistical agency will report on services sentiment, consumer confidence, industrial confidence, business climate and economic sentiment. All figures will be based on the month of December.

Data on Eurozone retail sales will also be released Monday.

In North America, the Bank of Canada will release its first Business Outlook Survey of 2018. The report provides an analysis of the nation's economy through the eyes of business executives.

The only US report of note is consumer credit change for November. The Federal Reserve will issue the data at 20:00 GMT.

The US dollar rose slightly against a basket of currencies Monday. The DXY basket was last seen trading at 92.00. The greenback plunged toward four-month lows in the first week of 2018. Analysts say it could be a tough year for the US currency even as the economy shows signs of strengthening. The greenback is coming off its worst year since 2003.

EUR/USD

Europe's common currency traded comfortably above 1.2000 US on Monday, as the EUR/USD consolidated near four-month highs. The regional currency is benefitting from a stronger economic recovery and the gradual removal of policy accommodation by the European Central Bank (ECB). The EUR/USD was last seen trading at 1.2033 for a gain of 0.1%. Despite the upsurge, the pair faces a major resistance test around 1.2100.

GBP/USD

Cable settled well off multi-month highs on Friday, but remains in a firm uptrend as traders continue disavowing the dollar. The GBP/USD exchange rate was last seen trading around 1.3570, where it was little changed compared to the previous close. The pair is seeing strong support at the psychological 1.3500 level. On the opposite side of the ledger, resistance is likely found at 1.3560.

USD/CAD

The North American cross resumed its descent last week, with the USD/CAD falling to its lowest level since September. The pair was last seen trading just below 1.2400. Immediate support is located at 1.2350. If the greenback recovers, the 1.2570 region is likely the next resistance region.

Forex Analysis: Canadian Data Centre Stage

Canadian Jobs reports came in strongly for the second month in a row, far exceeding expectations and leading to strong moves in CAD crosses. Unemployment is at a low of 5.7% and focus is shifting today towards the Bank of Canada Business Outlook Survey at 15:30 GMT. Traders will look for any indicators that could influence a change in monetary policy with regards to rate hikes, in view of the strong labour market, during the next BOC monetary policy meeting on the 17th of January.

Eurozone Consumer Prices Index – Core (YoY) (Dec) was out at 1.1% v an expected 1.0%, from a previous 0.9% that was revised up to 1.1%. Consumer Price Index (YoY) (Dec) was 1.4%, as expected, from a prior 1.5%. EURUSD bottomed at 1.20404 and rallied to 1.20550 after the data.

US Non-Farm Payrolls (Dec) was a miss to the downside when they were released. 148K new jobs were created from an expected 190K, compared to 228K previous that was revised up to 252K. The Unemployment Rate (Dec) was as expected at 4.1%, unchanged from the prior reading. EURUSD rose from 1.20445 to 1.20825 but then sold back down to 1.20203 after the data release.

Canadian Unemployment Rate (Dec) was 5.7% v an expected 6.0%, from a prior of 5.9%. Net Change in Employment (Dec) was 78.6K v an expected 1.0K, with a previous read of 79.5K. USDCAD started to selloff before the release from 1.25118. This move lower accelerated once the data was out and price bottomed at 1.23542.

US ISM Non-Manufacturing PMI (Dec) was in at 55.9 v an expected 57.6, from a prior of 57.4. Factory Orders (MoM) (Dec) were 1.3% v an expected 1.1%, with a previous reading of -0.1%, which was revised up to 0.4%. USDJPY fell from 113.253 to 113.080 upon the release.

Baker Hughes US Oil Rig Counts were released with a headline number of 742 from last week’s 747. WTI Oil extended its gains from $61.45 to $61.57 after the event.

EURUSD is down -0.09% overnight, trading around 1.20162.

USDJPY is up 0.18% in early session trading at around 113.216.

GBPUSD is down -0.09% to trade around 1.35507.

USDCAD is down -0.06%, trading around 1.24043.

AUDUSD is down -0.18% this morning, trading around 0.78446.

Gold is unchanged in early morning trading at around $1,318.40.

WTI is down -0.08%, trading around $61.51.

Major data releases for today:

At 08.00 GMT, Swiss Consumer Prices Index (YoY) (Dec) is expected unchanged at 0.8%. Consumer Price Index (MoM) (Dec) will also be released, with a prior value of 1.5%. Swiss Franc pairs may see price movement if the data released varies from the consensus.

At 10:00 GMT, Eurozone Business Climate (Dec) will be released, the previous was 1.49. Also at this time, Consumer Confidence (Dec) is expected to be unchanged at 0.5. Industrial Confidence (Dec) was 8.2 previously. Services Sentiment (Dec) was 16.3 previously. Economic Sentiment Indicator (Dec) is expected to be 115.0 v 114.6 prior. EUR crosses could experience volatility around this data release.

At 15:30 GMT, Bank of Canada Business Outlook Survey is expected to be released. CAD crosses could make sudden moves to test support and resistance after the data points are released.

At 20:00 GMT, US Consumer Credit Change (Nov) is expected at $18.75B from a prior of $20.52B. This data shows the amount of money that individuals borrowed and can move USD pairs upon its release.

Major data releases for this week:

Wednesday, 09:30 GMT, Manufacturing Production (MoM) (Nov) is expected at 0.3% with a prior of 0.1%.

Friday, 13:30 GMT, US Retail Sales (MoM) (Dec) is expected at 0.4% from a previous read of 0.8%. US Consumer Price Index (YoY) (Dec) is expected to come in unchanged at 2.2%.

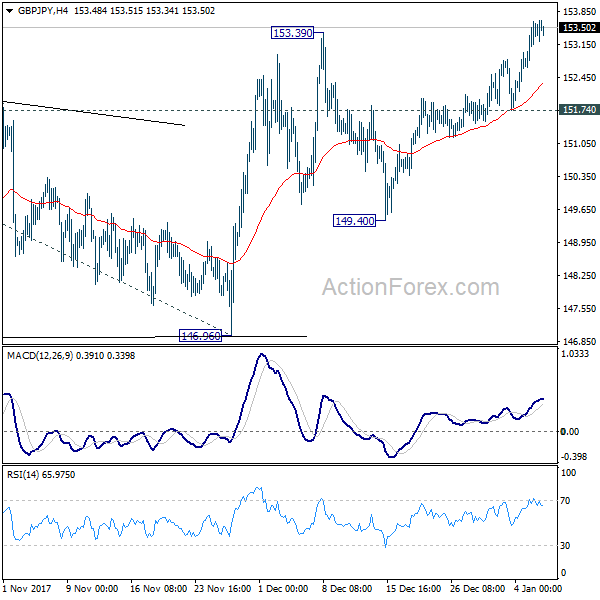

GBP/JPY Daily Outlook

Daily Pivots: (S1) 152.80; (P) 153.21; (R1) 153.74; More...

Intraday bias in GBP/JPY remains on the upside. Current rally would target 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32 first. Break will target 100% projection at 160.49 next. On the downside, break of 151.74 is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, it now looks like GBP/JPY has finally taken out 38.2% retracement of 195.86 to 122.36 at 150.43. Medium term rise from 122.36 should be targeting 61.8% retracement at 167.78. This will now be the favored case as long as 146.96 support remains intact.