Sample Category Title

EURUSD Intraday Analysis

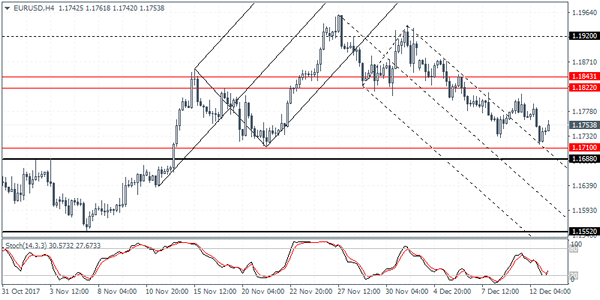

EURUSD (1.1753): The euro posted declines yesterday as the currency pair remains trading above the 1.1700 level of support. In the short term, we could expect to see a brief retest of this support level. On the 4-hour chart, price action posted a lower low but was seen finding support off the outer median line. A short term correction towards 1.1822 - 1.1843 is quite likely where resistance could be formed. The EURUSD could be seen maintaining the range within the resistance level mentioned and the support region near 1.1710 - 1.1700 level. A breakout below this support could potentially push EURUSD lower. This could see price action testing the November lows near 1.1552 support.

Trade Idea : USD/JPY – Buy at 112.90

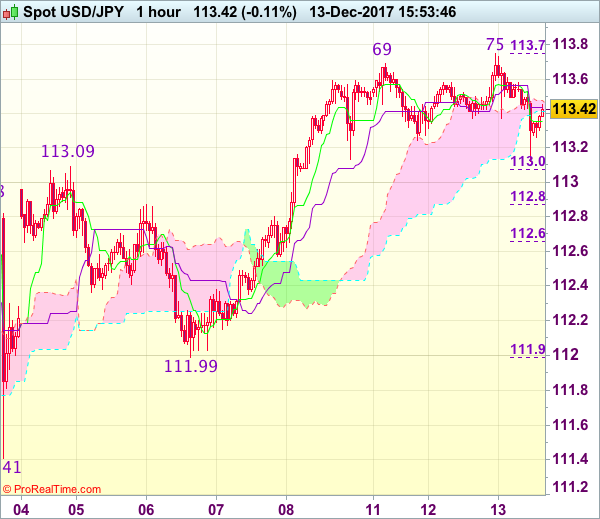

USD/JPY - 113.43

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.35

Kijun-Sen level : 113.44

Ichimoku cloud top : 113.47

Ichimoku cloud bottom : 113.41

Original strategy :

Buy at 112.90, Target: 114.00, Stop: 112.55

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.90, Target: 114.00, Stop: 112.55

Position : -

Target : -

Stop : -

As the greenback has retreated after marginal rise to 113.75, suggesting consolidation below this level would be seen and pullback to 113.08-09 (38.2% Fibonacci retracement of 111.99-113.75 and previous resistance turned support) is likely, however, reckon 112.85-87 (50% Fibonacci retracement) would limit downside and bring another rise later, above said resistance at 113.75 would extend recent upmove from 110.84 low to resistance area at 113.91-114.07 but a sustained breach above this region is needed to signal early uptrend has resumed for headway towards 114.34.

In view of this, would not chase this rise here and would be prudent to buy dollar again on pullback as 112.85-87 should limit downside and bring another rise later. Below 112.66 (61.8% Fibonacci retracement of 111.99-113.75) would defer and risk test of 112.55-57 but only break of latter level would signal top is formed instead, bring subsequent fall to 112.20-25.

Traders Look To FOMC Meeting, Fed Set To Hike Rates

The U.S. dollar was seen trading mixed as investors gear up for the Fed meeting today. On Tuesday, economic data from the U.S. showed that the U.S. producer price index advanced 3.1% on the year in November. This was the biggest gain since January 2012. The price increase at factory gate stoked expectations that the consumer price index could come out stronger.

The November CPI data will be released today with forecasts showing a 0.4% increase on the month. The Fed's rate hike decision is also coming up. Expectation for a 25 basis points rate hike is almost certain. The Fed's projections for the year ahead and forward guidance will be key.

In the UK, the inflation data for November released yesterday showed that CPI accelerated 3.1% on the month. However, core CPI was steady, rising 2.7%.

The UK's monthly jobs data will be coming out today with forecasts showing a modest increase in wages to 2.5%.

AUDUSD In A Downtrend, Bearish Below 200-Day MA

AUDUSD is clearly in a downtrend since falling from the multi-year high of 0.8124 to the 0.7500 area. The crossover of the 50-day moving average below the 200-day MA highlights the bearish outlook.

Immediate downside pressure has eased and the market has moved out of oversold conditions, as both the RSI and stochastics have risen out of their respective extreme levels.

The psychological level at 0.7500 has proven to be a strong support level and AUDUSD has been trading above it since June. This support is expected to remain firm and limit further downside for now. If it fails to hold, then prices could extend lower to re-test the May 9 low at 0.7328.

Looking at the Fibonacci retracement level of the upleg from 0.7328 to 0.8124, the market needs to rise above the 61.8% Fibonacci (0.7631) to develop stronger upside momentum and this would open the way towards the 200-day MA (0.7690) and 50% Fibonacci (0.7725).

AUDUSD has stalled its downtrend for now and is neutral in the near term. But the pair remains vulnerable with no change in the bearish outlook unless it can reclaim the 0.7900 handle.

GBPUSD Still Bearish Below 1.3340 Level

The British pound has fallen to the 1.3303 level against the U.S dollar, but managed to recover marginally overnight, on U.S political woes. The GBPUSD pair is currently trading around the 1.3326 level, after crashing below the 1.3340 support level yesterday. In the upcoming European trading session, the UK economy releases key wage data for the month of November. Any uptick in UK wage growth, or wage inflation will be taken as bullish for the pound, ahead of tomorrow’s Bank of England monetary policy decision.

The GBPUSD pair remains intraday bearish while trading below the 1.3340 technical level, strong support is found at the 1.3303 and 1.3268 levels.

Should GBPUSD buyers push price-action above the 1.3340 technical level, further buying towards the 1.3380 and 1.3400 levels seems possible.

EURO Still Intraday Bearish Below 1.1774 Level

The euro currency earlier failed to break below the key 1.1713 support level against the U.S dollar, as the pair quickly reversed direction during yesterday’s late U.S session. The EURUSD quickly slumped to 1.1717, but moved back above the 1.1750 level, after the greenback dipped following the U.S Democrat party winning the in the state of Alabama yesterday. The victory weakens the U.S Republican parties position in the U.S Senate and is weighing on the intraday sentiment around the U.S dollar. Traders now look to the U.S CPI reading for the month of November, ahead of the FED interest rate decision.

The EURUSD pair remains intraday bearish while price-action trades below the 1.1774 level, downside support is now found at the 1.1750 and 1.1717 technical levels.

If the EURUSD pair starts to move above the 1.1774 technical level, intraday buyers may start to target towards the 1.1790 and 1.1813 resistance levels.

Wednesday Is Fed Day

A deluge of market-moving events will make headlines on Wednesday, as all eyes turn to the Federal Reserve’s final policy meeting of the year.

Action begins at 06:00 GMT with a German report on the wholesale price index. One hour later, the German government will report on the final November consumer price index (CPI). Annual inflation in Europe’s largest economy is forecast to come in at 1.8% year-over-year. The harmonized index of consumer prices (HICP) is expected to hit the same level.

The United Kingdom will release headline employment data at 09:30 GMT. The number of unemployed workers is expected to rise by 3,200 in November following an increase of 1,100 the month before.

Unemployment, as calculated by the International Labour Organisation (ILO) standard, is expected to dip to 4.2% in the three months through October from 4.3%.

Meanwhile, average hourly earnings are expected to rise 2.5% annually in the three months through October.

Shifting gears to the Eurozone, Brussels will report on industrial production and employment at 10:00 GMT. Output in the 19-nation Eurozone is expected to rise 3.5% annually in October despite registering no growth month-on-month.

Overall employment is also expected to rise 0.4%.

In the United States, the Labor Department will issue its official consumer price index (CPI) at 13:00 GMT. Annual inflation in the world’s largest economy is expected to rise 2.2% annually in November, following a 2% gain the previous month.

The Federal Open Market Committee (FOMC) will deliver its rate verdict at 19:00 GMT. Policymakers are widely expected to vote in favour of a 25 basis-point increase in the federal funds rate, bringing it to 1.5%.

The Fed will also release a revised summary of economic projections covering GDP, unemployment, and inflation. It will be the last projection under the guidance of Chairwoman Janet Yellen. In February, she will be replaced by Fed governor Jerome Powell.

EUR/USD

Europe’s common currency tumbled to three-week lows on Tuesday, as investors turned their attention to the US Fed. The EUR/USD exchange rate was in recovery mode Wednesday, where it gained 0.2% to 1.1756. Its short-term outlook will be governed by the upcoming Fed decision.

GBP/USD

Cable has declined sharply in recent sessions, as sterling gave back some of last week’s rapid gains. GBP/USD was last seen trading around 1.3330. Wednesday is expected to be an active session for the pair amid UK data and Fed policy.

USD/CAD

The Canadian dollar has been on a sharp downward spiral for nearly a week after the Bank of Canada tempered expectations about future rate hikes. The USD/CAD approached 1.2900 on Tuesday, but has since tempered its gains. Prices were last seen consolidating around 1.2852, having declined 0.2% from the previous close.

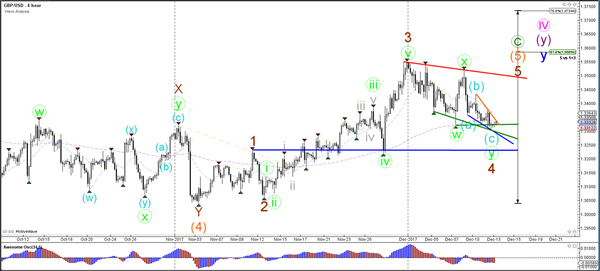

Daily Wave Analysis: EUR/USD, GBP/USD Retest Key And Vital Support Zone

Currency pair EUR/USD

The EUR/USD tested the 61.8% Fibonacci zone of wave 2 vs 1 and price used the support level for a bullish bounce. This could be part of an ABC (blue) flat correction within wave X (purple) of a larger wave 2 (pink) if price bounces at the resistance trend line (red). Alternatively a break below the 138.2% Fib invalidates the wave B (blue) and could indicate a bearish move towards 1.1650 and 1.16.

The EUR/USD could build a bullish ABC (blue) flat correction within wave X (purple). Price seems to be bouncing at the 127.2% Fib of wave B (blue) and could move towards the 61.8% Fib of wave X (purple).

Currency pair GBP/USD

A GBP/USD is showing choppy and corrective price action which is probably part of a wave 4 (brown). The wave 4 (brown) pattern is valid as long as price stays above the top of wave 1 (blue).

The GBP/USD is building a falling wedge reversal chart pattern which could indicate a potential bullish breakout if price manages to break above the resistance trend line (orange). A break below the support trend line (blue) could indicate a bearish breakout.

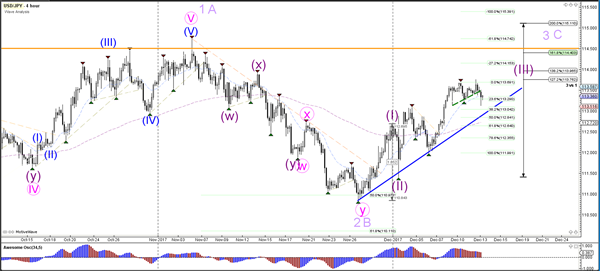

Currency pair USD/JPY

The USD/JPY could be a in wave 3 (purple) if price manages to stay above the support trend line (blue) and 50% Fibonacci level. The alternative scenario is that price is building a wave C rather than a wave 3.

The USD/JPY broke the trend lines but is still moving sideways. Price seems to be respecting the Fibonacci levels of wave 4 (blue) but a break below the 50% Fib would make a wave 4 unlikely.

Market Update – Asian Session: Oil Futures Rise After API

Headlines/Economic Data

General Trend: Asian equities trade mixed ahead of FOMC statement/forecasts

Chip-related shares decline

S&P 500 Futures decline, US dollar weakens as Democrat Jones projected to win the special US Senate election in Alabama

Japan

Nikkei 225 opened +0.1%; closed -0.5%

Chip-related firms generally lower: SUMCO -4%, Tokyo Electron -2%

DeNA: -3.5%, GungHo Online +8%: Nintendo said seek new game alliances, amid performance of prior alliance with DeNA, according to press report

Financials track outperformance in US banks: Sumitomo Mitsui +1.3%, Mitsubishi UFJ +1.1%;

JAPAN OCT CORE MACHINE ORDERS M/M: 5.0% V 2.9%E; Y/Y: +2.3% V -3.4%E

Japan Govt said to plan to keep the assumed interest rate at record low of 1.1% in FY18 budget draft - financial press

Japan govt said to plan to end tax liability on firms that eliminate shell companies acquired in foreign buyouts, aiming to simplify corporate structures and reduce tax avoidance – Nikkei

Toshiba (+1.3%) and Western Digital reach global settlement and agree to strengthen flash memory collaboration; participate jointly in future rounds of investment in Fab 6; agreed to withdraw all pending litigation and arbitration actions

7974.JP Reports global sales of Switch device above 10M units; -0.2%

9507.JP Japan Court bars restarting of Ikata reactor; Will file an objection over court ruling; -10%

Looking Ahead: BoJ Gov Kuroda expected to speak during the European Morning.

Japan Prelim Dec Manufacturing PMI and Oct Industrial Production due for release on Thursday

Korea

Kospi opened +0.1%

Weakness in chip sector: Hynix -1.6%, Samsung Electronics -1.1%

Financials gain: Woori +2%, Shinhan Financial +1.4%

(KR) UN Political Affairs Chief Feltman: North Korea leadership agrees it is important to avoid war

(KR) South Korea to hold emergency meeting related to trading of cryptocurrency, according to press report; Bank of Korea confirms government to announce measures on cryptocurrency trading on Friday

(KR) South Korea President Moon: South Korea and china to resume additional negotiations for FTA; Talks aimed at expanding FTA to service and investment

(KR) South Korea joint Govt statement: To consider taxing capital gains from cryptocurrency trading; Considering allowing cryptocurrency trading only on eligible exchanges that ‘uphold investor protection and trade transparency’

South Korea announces to propose bill to regulate crypocurrency speculation and exchanges - comments after special meeting on crypocurrency

Cosmetics firms gain after losses in prior session: Amorepacific +1.5%

South Korea saw a 50% drop in China tourists due to THAAD dispute - Korean press

South Korea Nov Unemployment Rate: 3.7% v 3.6%e

Sec of State Tillerson: US is ready to talk to North Korea without preconditions; North Korea must be "ready to make a choice"

UN Political Affairs Chief Feltman: North Korea leadership agrees it is important to avoid war **Note: Feltman was briefed following a visit to North Korea.

005380.KR Exec: Will dramatically beef up pure electric car (EV) lineup in the next eight years

China/Hong Kong

Hang Seng opened +0.2%, Shanghai -0.1%

Hang Seng Financial Index +0.7%, Telecom Index +0.5% (China Unicom +0.9%)

(CN) China President Xi urges sound development of China's manufacturing – Xinhua

(CN) China securities regulator CSRC said to advise companies to avoid ‘frequent’ capital raisings – China Securities Times

(CN) China Academy of Social Sciences (CASS) official Yin Jianfeng: interbank liquidity will remain tight until the Chinese Lunar New Year given restrictions on wealth management businesses and expected Fed rate hikes, to solve problems related to liquidity, the solution is to lower the required reserve ratio (RRR)

(CN) China Academy of Social Sciences (CASS) Researcher Feng: Domestic economy on track to achieve 6.8% GDP growth; Govt to likely set 2018 GDP target at around 6.5% (unchanged from 2017 target); Govt deleveraging campaign set to intensify

(CN) Analysts note that with little change expected in the yuan through 2018, there might be limited pressure on Chinese authorities to boost Treasury holdings as part of currency intervention efforts - financial press

(CN) Said that some China financial institutions are pressuring regulators to ease restrictions - Caixin

(CN) PBOC Open Market Operations (OMO): injects CNY130B v CNY150B prior in 7 and 28-day reverse repos v skips prior; Net injections CNY60B v CNY40B prior

(CN) China MoF sells 5-yr upsized bonds at 3.8605%, bid-to-cover 3.34x

(CN) PBoC sets yuan reference rate at 6.6251 v 6.6162 prior (lowest setting in 3-weeks)

(CN) China to invest $1.0T into autonomous driving - financial press

(CN) China to build cybersecurity industrial park in Beijing – Chinese Press

HNA Group Chairman and Directors to increase capital of Bohai Capital unit by CNY8.6M - US financial press

Looking Ahead: China Nov Fixed Assets Investment, Industrial Production and Retail Sales due for release on Thursday

Australia/New Zealand

ASX 200 opened flat: closed +0.1%

ASX 200 REIT index +1.9%; Westfield [WFD.AU] +14% (received offering from Unibail-Rodamco with $24.7B EV); Utilities -0.8%, Consumer Discretionary -0.7%

RBA officials don’t address monetary policy, instead focus on cryptocurrencies

(AU) Reserve Bank of Australia (RBA) Gov Lowe: bitcoin fascination feels like speculative mania - speaking at Australian Payment Summit

(AU) Reserve Bank of Australia (RBA) Assistant Gov Kent: External finance more redily available for firms - 30th Australasian Finance and Banking Conference

(AU) Australia Dec Westpac Consumer Confidence Index: 103.3 v 99.7 prior; m/m: +3.6% v -1.7% prior

(AU) Australia sells A$1.0B v A$1.0B indicated in 2.25% Nov 2022 bonds, avg yield 2.2218%, bid to cover 3.53x

(NZ) New Zealand Gov't expects previously announced law banning foreign house buyers to pass in early 2018; plans to introduce legislation on Thursday, Dec 14th

(NZ) New Zealand Nov Food Prices M/M: -0.4% v -1.1% prior

(NZ) New Zealand REINZ Nov House Sales Y/Y: -8.9% v -15.8% prior

Looking Ahead: Australia Nov Employment data due for release on Thursday

Other Asia

(SG) Singapore Central Bank (MAS) survey of economists: Sees 2018 GDP at 3%

Asia Development Bank raises 2017 Developing Asia GDP growth forecast to 6% from 5.9%

(IN) India 10-year bond yield opens 7.25% (up over 5bps), amid CPI data and rise in oil prices

Singapore’s Noble Group has gained over 54% in 3 sessions amid press speculation of debt-for-equity restructuring plan

North America

(US) DEMOCRAT JONES PROJECTED TO WIN ALABAMA US SENATE RACE VS REPUBLICAN MOORE - FOX NEWS AND AP; Jones with 50.38% of the vote v Moore's 48.24%

(US) The Senate race in Alabama is not expected to impact the GOP's plan to pass tax reform, as Republican leaders are racing to approve the tax legislation by early next week, which would be before the new Alabama Senator arrives in Washington D.C., says a financial press report

US equites closed mixed: Dow Jones +0.5%, S&P500 +0.2%, Nasdaq -0.2%, Russell 2000 -0.2%

S&P 500 Financials Index +1%; Utilities -1.7%

Western Digital [WDC]: +3.5% in afterhours: Announced settlement with Toshiba and raised Q2 EPS guidance

M&A: 21st Century Fox [FOX]: CNBC's Faber: sources say 21st Century Fox and Disney are on "glide path" for Thursday announcement about deal for Fox assets; Still not clear on the price being discussed, said to be an all stock deal. FOX spinco would retain approx $10/shr value

(US) Private economists expect 3 Fed rate hikes in 2018; expect rate hike at upcoming Dec meeting due to be concluded on Wed – US financial press poll; The forecasts are in line with the Nov survey.

(US) TREASURY'S $12B 30-YEAR BOND REOPENING DRAWS 2.804%; BID-TO-COVER RATIO: 2.48 V 2.53 PRIOR AND 2.33 AVG OVER THE LAST 8 SALES

Tax Reform: (US) White House: US President Trump to host House and Senate conferees on Wed (regarding tax bill)

(US) Ways and Means Chair Brady (R-TX): tax bill conference report release likely Friday

(US) Rep Lamar Smith (R-TX): House leadership indicates goal is for a vote next Tuesday (12/19) on reconciled tax reform bill

(US) GOP reportedly in talks to lower top income tax rate from 39.6% to 37% as part of final tax bill - Wash Post; Also said to be settling on 21% corporate rate starting in 2018 (vs 20% in initial bills), down from 35% currently

Government Funding: (US) Sen Maj Leader McConnell (R-KY): There is no chance we'll shut down govt

(US) Dem Leader Schumer (D-NY): negotiations on budget bill are advancing well

Energy: (US) Weekly API Oil Inventories: Crude: -7.4M v -5.5M prior

OPEC Barkindo: Affirms rebalancing of oil market ‘on its way’; Reiterates sees 2018 global oil demand up 1.5M B/D, in line with 2017

(US) Port Houston cargo handled through Nov: ~35M tons, +9% y/y; driven by steel volumes

Looking Ahead: US Fed FOMC Statement/Forecasts and US Nov CPI due to be released on Wed, along with weekly DOE Crude Inventories.

OPEC Dec Monthly Report tentatively due for release on Wed

Europe

(UK) EU Chief Brexit Negotiator Barnier: Friday's Brexit deal was an important step; we all must remain cautious on Brexit; Draft withdrawal agreement will come early 2018; Brexit treaty will include declaration on trade

Energy: (UK) Scotland Min: there are no plans to shut down Grangemouth refinery (200K bpd capacity) after Forties pipeline shutdown; Grangemouth refinery has enough oil stocks to run for about a week

Centrica [CNA.UK]: Revises end date for outage at UK North Morecambe gas sub-terminal to Dec 13th from Dec 12th

M&A: Abertis [ABE.ES]: Atlantia reportedly mulling all-cash offer for Abertis to outbid Hochtief - press

Levels as of 01:00ET

Nikkei225 %, Hang Seng +1.0%; Shanghai Composite +0.4%; ASX200 +0.1%, Kospi +0.5%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.0%, Dax -0.1%; FTSE100 +0.1%

EUR 1.1762-1.1736; JPY 113.57-113.13; AUD 0.7581-0.7553;NZD 0.6961-0.6932

Feb Gold +0.4% at $1,246/oz; Jan Crude Oil +0.7% at $57.55/brl; Mar Copper 0.0% at $3.02/lb

Forex: Trump Suffers A Setback, Oil Gains And GBP Stumbles

President Trump suffered a major setback as the once strictly Republican state of Alabama has, for the first time in 25 years, elected a Democrat to the US Senate. Democrat Doug Jones staged a stunning come-from-behind win against GOP Roy Moore in, what many believe, will trigger a political earthquake that will be felt nationally and internationally. The vote had been nip-and-tuck and, with 99% of the vote in, Jones was holding a 50% to 49% lead. The win puts the Democrats just two seats away from the majority in the US Senate in 2018. In early Wednesday trading, the markets have not yet digested the news as USD is relatively unchanged against its peers. Once we enter the European trading session we may see a negative reaction to USD, although today's US inflation data and FOMC meeting may provide some USD support.

On Tuesday, the American Petroleum Institute said crude stocks in the United States fell by 7.4 million barrels last week. That is almost twice the decline of market expectations, which were for a decline of 3.8 million barrels. WTI was higher on the drawdown news, trading up to $57.57 overnight. The markets will now be awaiting today's Energy Information Administration (EIA) report on Crude Oil Stocks change which could possibly see further strengthening in the price of Oil.

Data from the UK Office of National Statistics (ONS) on Tuesday showed that the annual rate of change in the consumer price index rose to 3.1% in November, compared with 3% in October. With inflation 1.1% above the Bank of England's 2%, Governor Mark Carney now must write a letter to the UK Chancellor of the Exchequer providing an explanation why the BoE has missed its inflation target after prices increased last month at the fastest rate for more than 5 years. With the UK Monetary Policy Committee meeting this week, the letter will not be published until the BoE publishes its next inflation report in February. GBP lost some ground on its peers following the release but has somewhat stabilized overnight.

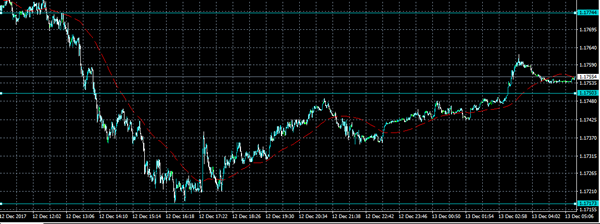

EURUSD is 0.1% higher in early Wednesday trading at around 1.1755.

USDJPY is 0.2% lower in early session trading at around 113.33.

GBPUSD is little changed overnight, trading around 1.3322.

Gold is unchanged in early trading at around $1,243.75.

WTI is 0.1% higher, trading around $57.47.

Major data releases for today:

At 07:30 GMT: Destatis will release German Harmonized Index of Consumer Prices annualized for November. Forecasts are suggesting the release will be unchanged from the previous release of 1.8%. Any significant deviation from forecast will see EUR volatility.

At 13:30 GMT: the US Bureau of Labor Statistics will release a plethora of Consumer Price Index data for November:

- Core CPI s.a. forecast at 253.961, previously 253.428

- CPI (MoM) forecast at 0.4%, previously 0.1%

- CPI ex-Food & Energy (YoY) forecast unchanged at 1.8%

- CPI (YoY) forecast at 2.2%, previously 2.0%

- CPI ex-Food & Energy (MoM) forecast unchanged at 0.2%

- CPI n.s.a (MoM) forecast at 246.660, previously 246.663

Any significant deviation from the forecast will likely see USD volatility in the markets.

At 15:30 GMT: the US Energy Information Administration will release EIA Crude Oil Stocks change for the week ended December 8th, an always impactful data release for both WTI and BRENT.

At 19:00 GMT: the US Federal Open Market Committee will announce its interest rate decision. The markets are fully expecting an increase from 1.25% to 1.5% and such a hike has been “priced-in” by the markets. The markets are keen to hear the Fed's economic projections, as the US economy experiences healthy economic growth. It is highly likely that there will be USD volatility following the announcement, as existing positions are closed and new positions opened.