Sample Category Title

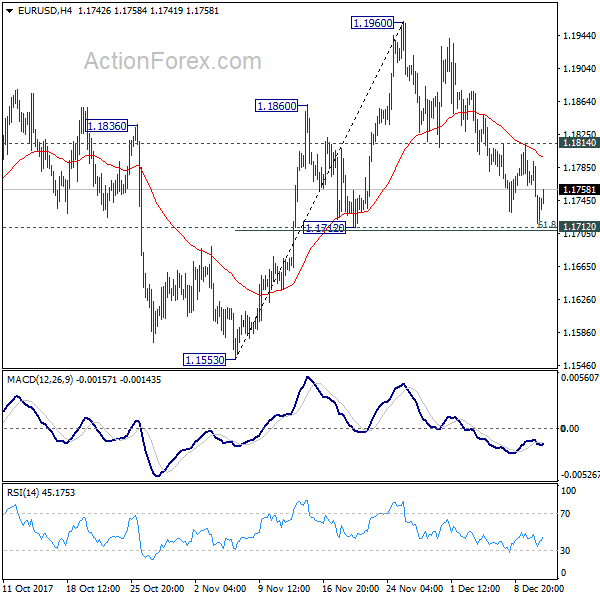

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1708; (P) 1.1750 (R1) 1.1783; More....

EUR/USD dipped to as low as 1.1717 but recovered ahead of 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708). Intraday bias remains neutral first. On the downside, decisive break of 1.1708/12 will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to 1.1553 and possibly below to extend the decline from 1.2091. On the upside, break of 1.1814 minor resistance will retain near term bullishness. And in that case, intraday bias will be turned back to the upside for 1.1960. Break will target 1.2091 high.

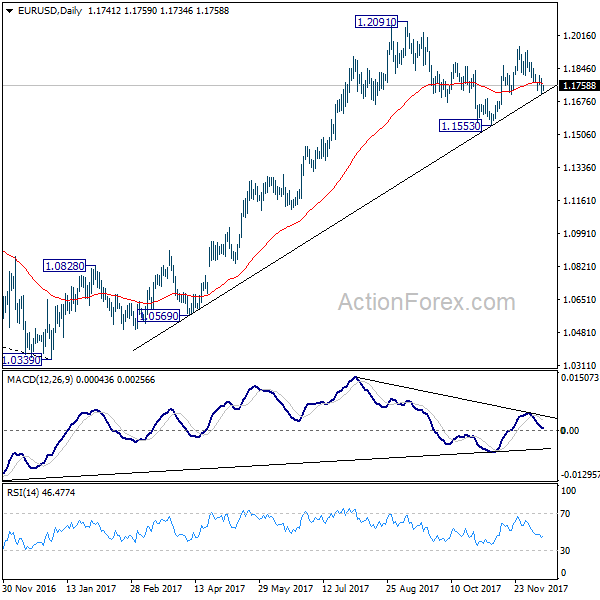

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Stocks Hit New Records, But Dollar Hesitates as FOMC Eyed

Investors expressed their vote of confidence overnight as they await the highly anticipated FOMC rate decision and press conference. DOW closed at record high at 24504.80, up 118.77 pts or 0.49%. S&P 500 followed closely and gained 4.12 pts or 0.15% at 2664.11, also a record. 10 year yield closed above 2.4 handle at 2.403, up 0.018. The dollar index breached 94.10 key near term resistance. However, EUR/USD is still holding on to equivalent support at 1.1712. The greenback is trading mixed only as traders seem to be cautious before Fed showing whether it's still on track for three hike next year. In the currency markets, New Zealand Dollar remain the strongest one for the week and helped keep Aussie up. Euro and Sterling are generally soft.

Fed to hike, eyes on voting and projections

Fed is widely expected to raise federal funds rate by 25bps to 1.25-1.50% today. There is little doubt about that. Janet Yellen will deliver her last press conference as Fed chair, before Jerome Powell takes over the job next year. The surprise elements could be found in the voting and the new projections. Minneapolis Fed President Neel Kashkari, who dissented the prior hikes, would very likely dissent again. Chicago Fed President Charles Evans could be another dissenter. The vote split could be seen as hawkish if only Kashkari dissents. However, three or more dissenting will signals spreading of the worries on slow inflations among policymakers. And that would be dovish. Fed will mostly upgrade GDP forecast for 2018 and 2019 while lower unemployment rate estimates. The keys will lie in the changes in inflation projections and interest rate projections. So far, hawks inside the FOMC are still expecting three more rate hikes next year.

FOMC September Projections

Before FOMC announcement, CPI release from US will also be a volatility driver. Headline CPI is expected to accelerate to 2.2% yoy in November. Core CPI is expected to be unchanged at 1.8% yoy. Dollar traders could jump the gun should there be any surprise there. Separately, US President Donald Trump will speak today to pitch the Republican's tax plan.

Australia consumer confidence improved, but not enough for RBA hike in 2018

Australia Westpac consumer confidence rose solidly by 3.6% in December. According to Westpac, that's a "surprisingly strong result" that appears to be boosted by "less threatening outlook for interest rates". Nonetheless, while expectation for an RBA hike in 2018 cooled, Westpac "doubt whether this welcome lift to confidence will be sufficient to see the Bank achieve its ambitious growth forecast in 2018 of 3.25%." And, with inflation projected to be below target in 2018, and a cooling Sydney property market, Westpac maintained the view that RBA will stand pat through 2018.

RBA Lowe: Cryptocurrencies "feels more like a speculative mania"

Staying in Australia, RBA Governor Philip Lowe criticized that current fascinations with cryptocurrencies "feels more like a speculative mania". And when though of "purely as a payment instrument", crytopcurrencies are "more likely to be attractive to those who want to make transactions in the black or illegal economy, rather than everyday transactions." Lowe also added that "the value of Bitcoin is very volatile, the number of payments that can currently be handled is very low, there are governance problems."

Elsewhere

Japan machine orders rose 5.0% mom in October. UK will release job data in European session. Eurozone will release industrial production, employment and German CPI final.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1708; (P) 1.1750 (R1) 1.1783; More....

EUR/USD dipped to as low as 1.1717 but recovered ahead of 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708). Intraday bias remains neutral first. On the downside, decisive break of 1.1708/12 will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to 1.1553 and possibly below to extend the decline from 1.2091. On the upside, break of 1.1814 minor resistance will retain near term bullishness. And in that case, intraday bias will be turned back to the upside for 1.1960. Break will target 1.2091 high.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1423) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | 3.60% | -1.70% | ||

| 23:50 | JPY | Machine Orders M/M Oct | 5.00% | 2.70% | -8.10% | |

| 07:00 | EUR | German CPI M/M Nov F | 0.30% | 0.30% | ||

| 07:00 | EUR | German CPI Y/Y Nov F | 1.80% | 1.80% | ||

| 09:30 | GBP | Jobless Claims Change Nov | 0.4K | 1.1K | ||

| 09:30 | GBP | Claimant Count Rate Nov | 2.30% | |||

| 09:30 | GBP | ILO Unemployment Rate 3M Oct | 4.20% | 4.30% | ||

| 09:30 | GBP | Average Weekly Earnings 3M/Y Oct | 2.50% | 2.20% | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | 0.10% | -0.60% | ||

| 10:00 | EUR | Eurozone Employment Q/Q Q3 | 0.40% | 0.40% | ||

| 13:30 | USD | CPI M/M Nov | 0.40% | 0.10% | ||

| 13:30 | USD | CPI Y/Y Nov | 2.20% | 2.00% | ||

| 13:30 | USD | CPI Core M/M Nov | 0.20% | 0.20% | ||

| 13:30 | USD | CPI Core Y/Y Nov | 1.80% | 1.80% | ||

| 15:30 | USD | Crude Oil Inventories | -5.6M | |||

| 19:00 | USD | FOMC Rate Decision | 1.50% | 1.25% | ||

| 19:30 | USD | FOMC Press Conference |

Market Morning Briefing: Euro Is Trading Just Above Immediate Support

STOCKS

Dow (24504.80, +0.49%) and Dax (13183.53, +0.46%) are up about 0.50%. While Dow has some more scope of rising towards 24600, Dax does not look very bullish while below resistance at 13200. Dax could test lower levels of 13000 while Dow may slowly inch up in the near term.

Nikkei (22816.93, -0.22%) has immediate resistance near 23200 which is likely to hold in the near term, pushing the index back to levels near 22600 or lower. But unless a sharp fall in Dollar Yen is seen, Nikkei could remain stable and trade along the near term channel resistance.

Shanghai (3281.75, +0.03%) is almost stable just now. Support near 3280-3270 is visible on the daily charts and while that holds, a bounce back to higher levels of 3320 is possible. Near term looks bullish.

Nifty (10240.15, -0.80%) and Sensex (33227.99, -0.68%) are in the correction phase as expected. Near term looks bearish. Sensex could fall towards 33000 while Nifty may test 10100 on the downside

COMMODITIES

Gold (1243.29) is almost stable. Need to see if it holds above 1240 today or comes down to test 1220. Movement in the next couple of sessions would be crucial.

Silver (15.72) is stable above 15.60. The price is likely to rise towards 16 and higher in the coming sessions.

Brent (63.95) and WTI (57.55) came off sharply but the bulls may continue to take the price up in the medium term. While WTI has resistance near 59-60, Brent looks positive towards 68 before a sharp fall is seen.

Copper (3.0180) is likely to trade within 2.95-3.10 region in the near to medium term. It could rise towards 3.10 in the next few sessions before again coming off towards 3.00.

FOREX

Dollar-Index (93.945) is now testing resistance around 94.00 on the 3 day candles and daily line charts. This is an important resistance, whose hold could indicate to a possible downtrend towards 93 by end of this month. However a breach of resistance would possibly lead to a test of 94.40-94.50 on the daily candles, from where a definitive dip could follow.

Euro (1.1768) is trading just above immediate support (around 1.173-1.175) on the 3 day candles, which is likely to hold and take it towards 1.19 by the end of the month. A break of immediate support could however lead to testing of lower support around 1.17 (as seen on daily candles, 3 day candles & daily line charts), which could then prove to be a strong support.

Dollar-Yen (113.48), like the Dollar Index, seems to be seeing a dip from resistance level (around 113.5-113.6) on the daily line chart. A further test of higher resistance at 114 could still be possible with an eventual dip back towards 112-112.5 by next month.

Pound (1.3340) has broken support at 1.335 and is now expected to move towards 1.32-1.3225, which is seen as a strong support level on daily, 3 day and weekly charts.

Dollar Rupee (64.3650) may test 64.30/25 today and then bounce back towards 64.50 by the end of the week. Possibility of corresponding movement in the Nifty towards resistance (10350) and a dip from there coincides with predicted Dollar Rupee movement.

INTEREST RATES

The US yields are have risen as expected. The 5Yr (2.17%), 10Yr (2.40%) and the 30Yr (2.78%) are slightly up from previous levels. The 10YR may come off from current levels or move up further to test 2.45-2.50% in the medium term. The 5Yr has scope of rising towards 2.25% while the 30Yr may face some rejection from 2.80%.

The US-Japan 10Yr (2.36%) is attempting to break above immediate resistance levels and if that sustains, it could move p towards 2.40% and higher, pulling up Dollar Yen and Nikkei along with itself.

The UK-US 10YR (-1.18%) is stable. While the spread looks bearish, Pound could also move down towards 1.32-1.31 in the coming sessions.

The German-US 10YR (-2.09%) could pause at -2.10%. Important events to note would be the FOMC tonight and the ECB policy meet tomorrow.

The Indian 10YR GOI (7.23%) continues to rise sharply favoring Rupee weakness in the near term.

Currency Market Have Remained Predictably Boring Ahead of FOMC

Currency traders have remained in a state of virtual suspended animation the past 48 hours. But with all the other hoopla surrounding Bitcoin and frothy equity markets, currency speculation has been dead money so far this week but perhaps things are about to change or maybe not.

To that point, Central Bank( CB) meetings have become all too predictable and boring. In fact, the market fully priced in this Fed December rate hike 4-6 weeks ago leaving traders with little more than CB verbal gymnastics to digest later tonight. And to that end, the FOMC forward guidance has been notoriously unreliable at times while continually erring on the side of data dependency. Absent is the unpredictability and exhilaration around CB meetings that is long forgotten and sadly, for Forex Traders, the days of 50 bp surprise rate hikes are ancient history.

Equity Markets

Aisa equity Investors traded with an air of caution on Tuesday while their European and US counterparts were brimming with vim and vigour overnight. European STOXX 600 index up + 0.6 percent and both the S&P 500 and Dow catalogued record closing highs with a surge from bank stocks as investors remain constructive about US tax reform and economic growth.

Apparently, the bull market has ways to run despite 2017 froth as tax cuts are expected to extend the current rally shelf life. And with the investors cheering on the December US rate hike as a sign of a healthy economy there's undoubtedly ample synchronicity in this markets.

US Economic Data

The US PPI printed a beefy reading of 0.44% in November versus 0.2% expected perhaps suggesting tomorrows CPI also top expectation. The stronger than expected inflation reading pushed the US 10 year yields through the often cited vital level of 2.4 % while lending support to the dollar.

The PPI has surprised to the upside on core measure which might help expectations into the CPI. But so far only a small USD positive reaction as the impact is limited ahead of the FOMC forward guidance.

NFIB small business survey was surging 3.8pts to 107.5 in November. This print is the highest reading since 1983.So apparently small firms are impressed by President Trump's tax reform proposal after all

Energy Prices

Yesterday's the North Sea gains were subsequently more than reversed leaving crude prices down for the day.

Overextended risk premiums with the Brent -WTI spread at $ 7 per barrel, the highest since May 25, likely triggered some profit-taking.Also, the Brent market turned less jittery when news out of Scotland suggested there are no plans to shut down Grangemouth refinery (200K bpd capacity) which has enough oil stocks to run for about a week.

On the WTI side of the equation, the omnipresent "nodding donkey" factor with shale oil output set to ramp up production as we near 60 per barrel continues to weigh on sentiment.

G-10 Currencies

The Australian Dollar

What appeared to be profit taking after the dismal housing data and the business confidence index reading blossomed into a full-bore short squeeze for the A dollar. apparently, the market had much weaker shorts than expected indicating that short-term positioning will likely be the primary factor over the next few week

The Japanese Yen

Trading remains incredibly low spirited after getting no rise from PPI or the boisterous small business data. There may be a trade to be had on the FOMC, but other than that I suspect dealers are content to remain on the sidelines.But with inflation apparently picking up, it could cement the long-awaited medium-term trend to emerge and USDJPY to move closer 115 in the New Year.

JAPAN OCT CORE MACHINERY ORDERS +5.0 PCT M/M (REUTERS POLL: +3.0 PCT) But little reaction to the data as the market has bigger fish to fry

Asia FX

Indian Ruppe

Indian Ruppe struggled yesterday with the move on Brent and the adverse knock-on effect to oil price sensitive constituents on the NIFTY. So with Brent oil prices coming off the highs overnight, we should expect a reversal of fortune of sorts for the Rupee when trading kicks in later today.

The Malaysian Ringgit

The Ringgit didn't benefit from rising oil price as local traders factored the risk premium as a short-term term factor. Expect the Ringgit to trade with a neutral bias today given that international investors are gearing down for the holiday season. But with energy prices holding up well and given the lack of positioning in the Ringitt may be less vulnerable to any FOMC surprises than regional peers.

Wednesday Market Musing

On the elections in the Heart of Dixie: If Moore does win, I suspect this will be Al Franken Redux but will have no impact on the Tax Reform vote given the patronage clause awarded the Governor of Alabama who would most certainly appoint a Republican

Fed Decision, US Inflation and Alabama Election to Guide Dollar

US benchmark rate expected to be 25 points higher

The USD was mixed against major pairs on Tuesday ahead of the release of the final results of the Alabama special election, inflation data in the US and the awaited December Federal Open Market Committee (FOMC) meeting.

Inflation data in the US will be published by the Bureau of Labor Statistics on Wednesday, December 13 at 8:30 am. Core CPI is expected to gain 0.2 percent but prices taking into consideration food and energy are forecasted to increase by 0.4 percent.

The U.S. Federal Reserve will release it's quarterly economic projections and Federal Open Market Committee (FOMC) statement on Wednesday, December 13 at 2:00 pm EST. The highly anticipated December meeting of the Fed is expected to bring a 25 basis points rate hike. The market has already priced in that move as it was heavily telegraphed by policy makers but there is a 12.4 percent probability of a 50 basis points hike. Economists are forecasting 3 rate hikes in 2018 and the dot-plots could align with those estimates if the central bank intends to speed up the current rate lift cycle. Fed Chair Janet Yellen will make her final appliance as Chair when she hosts the FOMC press conference at 2:30 pm EST.

The EUR/USD lost 0.23 percent on Tuesday. The single currency is trading at 1.1742 ahead of the end of the two-day Federal Open Market Committee (FOMC) meeting. The much awaited December rate hike is expected to be announced. If the Fed hikes rates it would have done so for the third time this year leaving the benchmark Fed funds rate in a 125 to 150 basis points range.

The meeting will mark an end of an era. Although it will be until February when Fed Chair Janet Yellen steps down, this will be her last appearance at the height of her powers. Jerome Powell will take over the US central bank and the market is starting to price in 3 rate hikes in 2018. The economy has not shown signs of overheating, which will be an argument used by the doves within the FOMC to reduce the path of hikes as inflation remains weak.

The dollar has risen ahead of the Fed meeting as producer prices have risen more than expected. Strong inflation would make Powell's job easier within the Fed. The higher price signal combined with a weaker than expected German ZEW economic sentiment. German investors have dialled back their optimism somewhat as the European Central Bank (ECB) remains dovish despite strong economic fundamentals in Europe. The ECB will also play a big part this week with the release of their rate statement at 7:45 am EST on Thursday, December 14. ECB President Mario Draghi will host a press conference at 8:30 am EST. The ECB is not expected to change its QE program or interest rates at this time, but the market will be on the lookout for its 2020 growth and inflation forecasts.

Market events to watch this week:

Wednesday, December 13

- 4:30 am GBP Average Earnings Index 3m/y

- 8:30 am USD CPI m/m

- 8:30 am USD Core CPI m/m

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Economic Projections

- 2:00 pm USD FOMC Statement

- 2:00 pm USD Federal Funds Rate

- 2:30 pm USD FOMC Press Conference

- 7:30 pm AUD Employment Change

- 7:30 pm AUD Unemployment Rate

- 9:00 pm CNY Industrial Production y/y

Thursday, December 14

- 3:30 am CHF Libor Rate

- 3:30 am CHF SNB Monetary Policy Assessment

- 4:00 am CHF SNB Press Conference

- 4:30 am GBP Retail Sales m/m

- 7:00 am GBP MPC Official Bank Rate Votes

- 7:00 am GBP Monetary Policy Summary

- 7:00 am GBP Official Bank Rate

- 7:45 am EUR Minimum Bid Rate

- 8:30 am EUR ECB Press Conference

- 8:30 am USD Core Retail Sales m/m

- 8:30 am USD Retail Sales m/m

- 8:30 am USD Unemployment Claims

*All times EDT

Gold Slide Continues as Markets Anticipate Fed Rate Hike

Gold has ticked lower in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1241.22, down 0.08% on the day. On the release front, PPI posted a gain of 0.4%, matching the estimate. Core PPI came in at 0.3%, above the estimate of 0.2%. On Wednesday, the Federal Reserve is expected to raise rates to a range between 1.25% to 1.50%. As well, the US releases CPI reports.

Traders should be prepared for a possible drop in gold prices on Wednesday, as the Federal Reserve meets to set the benchmark interest rate. The markets are expecting the Fed to raise rates by a quarter-point. Another rate hike is expected in January, with fed futures pricing a rate hike at 87%. The Fed is pleased with the strength of the US economy, but remains puzzled why strong growth and a red-hot labor market has not led to higher inflation. The labor market continues to operate at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages. On Friday, Average Hourly Earnings, which measures wage growth, came in at 0.2%, shy of the estimate of 0.3%. Whether inflation moves higher or remains depressed could have a significant effect on monetary policy – if wage growth and inflation shows improvement in 2018, the Fed could raise interest rates up to three times in 2018. After Wednesday's rate announcement, the markets will be looking ahead to the January policy meeting, with the odds of a quarter-point hike standing at 86 percent.

Dollar Solid Ahead of FOMC

The US dollar climbed ahead of the Wednesday's FOMC decision on signs of rising inflation. The Australian dollar was the top performer on Tuesday while the euro lagged. Japanese machine orders and the RBA's Kent are up before Yellen. A new Premium video has been issued and sent to subscribers on the rationale behind the 2 EURUSD trades and rest of 8 trades ahead of the Fed and ECB decisions, in light of the underlining technical developments shaping the EUR and USDX.

The US PPI report doesn't always foreshadow headline inflation but is often a clue. The November report showed pipeline pressures at the highest since February 2012, up 3.1% y/y compared to 2.9% expected. The US dollar got a lift from the report and continued higher for much of the day.

The USD also benefited from Congressional talk that passing the unified tax was imminent. That presents two-sided risks but early details show a 21% corporate tax rate, which is a touch higher than the 20% in the initial bill. What will matter more is how deductions and R&D are credited.

USD/JPY rose as high as 113.75, which was the best since Nov 14. The pair is slowly approaching the tough zone of resistance in the 114-115 range. It's a zone that's been tested four times in the past year and held.

The day ahead could be a big one on that front. If the FOMC hikes rates (an almost sure bet) and delivers some hawkish hints, along with a stimulative tax package, it could clear the way for a dollar rally into year end. However if the Fed decides to stay coy before Powell takes the reigns and the tax plan disappoints, the dollar could just as easily head in the other direction. Ashraf will post a full Fed preview in English and Arabic in Wednesday's early edition of this section.

Before then, some Asia-Pacific data could move markets. The RBA's Kent is due up at 0000 GMT. The market is increasingly expecting the RBA to stay on the sidelines for the first half of 2017 or longer. Yesterday's soft Q3 house price data underscored the challenges.

Another report to note is the October Japanese machine orders report. The consensus is for a 2.9% rise after the 8.1% drop in September.

Pound Edges Lower, British CPI Rises

The British pound has ticked lower in the Tuesday session. In North American trade, GBP/USD is trading at 1.3324, down 0.12% on the day. On the release front, British CPI came in at 3.1%, edging above the estimate of 3.0%. In the US, PPI posted a gain of 0.4%, matching the estimate. Core PPI came in at 0.3%, above the estimate of 0.2%. On Wednesday, the Federal Reserve is expected to raise rates to a range between 1.25% to 1.50%. As well, the US releases CPI reports.

Brexit negotiations are back on track, and the European Union is expected to give a green light to the talks shifting to trade issues. For months, the talks have been stuck over three issues: 1) the size of Britain's divorce bill; 2) the role of the European Court of Justice; and 3) Northern Ireland's borders with the UK and Ireland. After some feverish negotiations, sufficient progress has been made on these issues to satisfy the EU, which holds a key summit next week. What will a new trade relationship look like? Brexit policymakers appear divided on this question. On Sunday, Brexit minister David Davis said he envisions a comprehensive trade deal with Europe, which would be signed just after Britain leaves the bloc. The EU recently signed a free-trade treaty with Canada, and Davis said that he wants an agreement "Canada plus plus plus", meaning that the deep trading ties between the sides and access to European markets would remain intact. International Trade Secretary Liam Fox went a step further on Tuesday, saying that he wants a post-Brexit trading relationship with the EU that is "virtually identical" to the current relationship. It's questionable whether the EU would agree with Fox's comments, as Brussels doesn't want to give Britain too sweet a deal which could give other EU members any ideas about departing from the bloc.

All eyes are on the Federal Reserve, which meets on Wednesday for a policy meeting. The markets are expecting a quarter-point rate hike. Another rate hike is expected in January, with fed futures pricing a rate hike at 87%. The Fed has hinted that it could raise rates up to three times in 2018, and this upward movement in rates will likely propel the US dollar upwards. The US labor market remains at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages.

Crude Oil Trading In A Bullish Impulse and Aiming For 60/61 Per Barrel

Good day traders and welcome to the US session.

Today, let's talk about crude oil, its short and medium time frame.

On the daily chart crude oil has completed a complex correction labeled as wave II or B at the 42.03 level from where we started to track a new bullish impulse. An impulse is a five wave pattern, so there is room for much more gains on energy market since we see current leg up as blue wave 3 of an impulse. Wave 3) has in general five clear waves, which means oil price can still climb up to 60/61.9$ per barrel.

Crude oil, daily

Regarding the 4h chart of crude oil, we can see that energy found a possible base for higher degree wave 4) at the 55.77 level; near the Fibonacci support ratio of 38.2 and near the lower EW base channel line. A bounce followed from there, which can suggest higher degree wave 5) to be in progress towards 60.0 region and above in impulsive fashion. This means in clear five waves.

Crude oil, 4h

USDJPY Return above Daily Cloud is Bullish Signal

The dollar regained traction and returned above cloud top, boosted by better than expected US data.

Fresh bullish acceleration posts new highs (the highest in one month) and on track for the third consecutive close above daily cloud top which would boost bullish signal for test of immediate target at 113.81 (Fibo 76.4% of 114.73/110.83 descend) and possible extension towards key short-term barrier at 114.73 (06 Nov peak).

Fed's verdict tomorrow is expected to further boost the greenback on hawkish post-rate decision comments.

Res: 113.81; 114.27; 114.45; 114.73

Sup: 113.51; 113.25; 113.06; 112.83