Sample Category Title

AUD/USD: Australian Retail Sales, RBA Interest Rate Decision

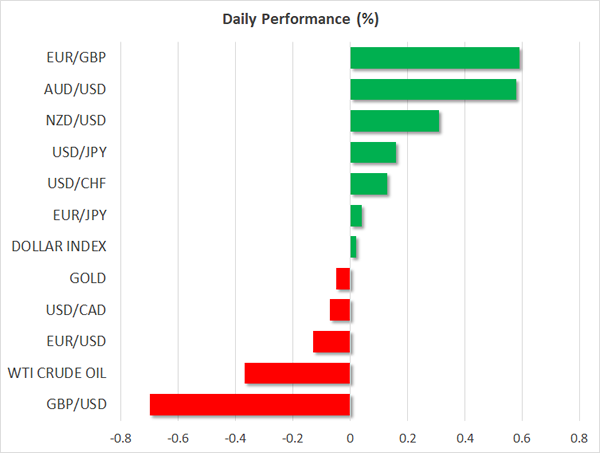

The Aussie was under stronger bullish sentiment against the Greenback on early Tuesday reports. The AUD/USD currency pair added 14 base points initially after the country's retial sales report and managed to sustain gains, as the RBA announced its rate decision.

The Australain Bureau of Statistics reported that the country's retail sales rose at a stronger-than-expected pace of 0.5% in October, following an upwardly revised 0.1% gain in the prior month. The most of contribution came from a stronger sales in eating out and clothing sectors. Later, the Reserve Bank of Australia stated that it kept its key interest rate unchanged at the historical low of 1.50%. The next move in the pair would be determined by the substantial GDP report on Wednesday.

Aussie Boosted By Retail Sales While Tech Selloff Spreads To Asia

Here are the latest developments in global markets:

FOREX: The RBA held rates unchanged on early Tuesdayas expected, but the aussie hit a three-week high following upbeat retail sales figures which pointed to an improved economic outlook. The kiwi also posted a strong rebound, erasing yesterday’s losses after the RBNZ governor said that the central bank had less leverage over inflation. Sterling was on the backfoot as the UK Prime Minister failed to satisfy the EU on Brexit elements, while the dollar inched up versus the yen as investors continued to see positive momentum following the Senate’s passage of the US tax code.

STOCKS: The Nikkei 225 retreated by 0.4% on a day when tech stocks underperformed in Asian equity markets as yesterday’s selloff in the US reverberated into the continent. At 0800 GMT, Euro Stoxx 50 futures were down by 0.1%. Dow futures were higher by 0.2%, S&P 500 contracts traded up by 0.1% and Nasdaq 100 equivalents were unchanged.

COMMODITIES: Oil prices were steady around yesterday’s lows ahead of the API weekly report as investors remained cautious on rising US crude inventories. WTI crude and Brent were last trading at $57.44 and $62.37 per barrel respectively. Gold was flat at $1,275.40 per ounce.

Major movers: Aussie surges on retail sales; pound pressured on Irish border

The RBA decided on Tuesday to leave interest rates steady at a record low of 1.5% for the sixteen-consecutive meeting as expected. The monetary policy statement following the decision was perceived as hawkish by investors as policymakers omitted the phrase “inflation is likely to remain low for some time”, providing some support to the aussie. Moreover, better-than-expected readings on Australian retail sales published prior the RBA statement were good news for the central bank which hopes inflation would pick up and the economic outlook would improve. Retail sales rose by 0.5% m/m in October, surprising analysts who forecasted a growth of 0.3%. September’s mark was also revised upwards from 0.0% m/m to 0.1%. In the wake of the news, the aussie surged to a three-week high of $0.7653 (+0.61% on the day).

The New Zealand dollar followed an uptrend as well towards a session high of $0.6906 (+0.35%), supported by comments delivered by the acting RBNZ governor, Grant Spencer. Spencer said that “In pursuing long-term price stability objective, relatively more weight is being attached to output, employment, and financial stability” due to persistent low import prices – a fact that could reduce chances for further rate cuts.

The pound retreated back to $1.3385 (-0.71%) after progress on Brexit talks was stuck in Brussels, with the UK Prime Minister Theresa May unable to persuade the EU on any positive developments on issue of the Irish border. Euro/pound was 0.61% up at 0.8856.

Dollar/yen gained 0.18%, rising to 112.60 while euro/dollar edged up by 0.12% to 1.1850. The dollar index was flat at 93.19.

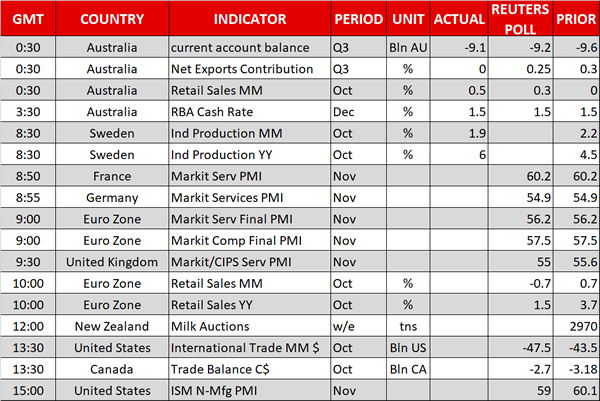

Day ahead: UK services PMI, eurozone retail sales & PMIs, US and Canadian trade data as well as ISM’s services PMI to attract most attention

At 0900 GMT, the eurozone will see the release of November services and composite PMI figures. Those would pertain to their final readings though and are not expected to gather much attention – analysts expect the figures to be released unchanged relative to their flash estimates. One hour later, euro area retail sales for the month of October will be made public. Month-on-month, sales are expected to contract by 0.7% and year-on-year to grow by 1.5% (September’s respective readings stood at 0.7% and 3.7% respectively).

Out of the UK, the November Markit/CIPS services PMI is due at 0930 GMT. The gauge of activity in the UK’s largest sector is forecasted to fall to 55.0 – remaining though comfortably above the 50 threshold that separates contraction from expansion – from October’s 55.6.

The outcome of the global milk auction will be known around 1200 GMT (the release is tentative though, lacking a certain time of release). Major dairy exporter New Zealand and consequently the kiwi will be in focus.

US international trade data and Canada’s trade balance (both for the month of October) will be made public at 1330 GMT. The US will also see the release of ISM’s services PMI for November at 1500 GMT. Activity in the sector is expected to ease with the index falling to 59.0 – still a robust reading – from October’s more than two-year high of 60.1.

API weekly data, including on US crude oil stocks are due at 2135 GMT.

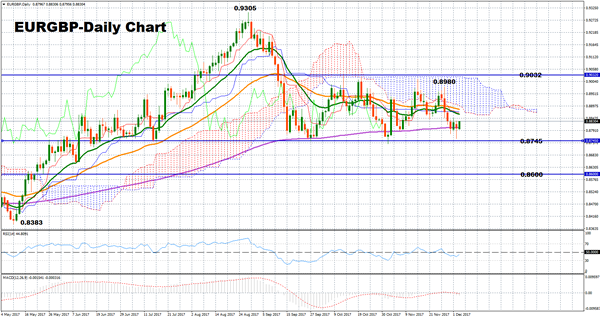

Technical Analysis: EURGBP holds neutral bias in short-term; bearish outlook still in place

EUGBP has been moving sideways between 0.8745-0.9032 since the end of September following a sharp fall from an eight-year peak at 0.9305. In the short-term the bias is looking neutral with the pair looking likely to remain within the current range. The technical indicators also support this view, with the RSI trending marginally below 50 and the MACD being attached to zero.

However, any close below 0.8745 would resume the medium-term downleg starting from 0.9305 and shift focus to the 0.8600 key-level. Deeper falls could also target the seven-month low of 0.8383.

On the upside, immediate resistance could emerge between the 20-day EMA and the 50-day EMA (0.8861-0.8883) before the pair heads up to the upper bound of the range at 0.9032. If this point is broken, the scope would open for a revisit of the eight-year high of 0.9305, turning the bias from neutral to bullish.

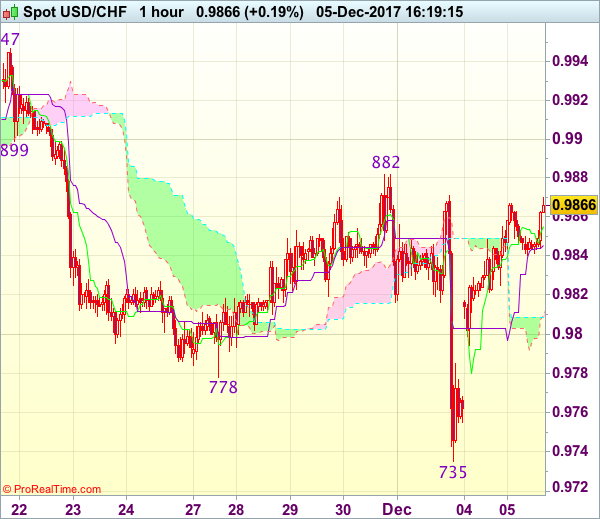

Trade Idea : USD/CHF – Buy at 0.9795

USD/CHF - 0.9859

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9855

Kijun-Sen level : 0.9846

Ichimoku cloud top : 0.9812

Ichimoku cloud bottom : 0.9809

Original strategy :

Buy at 0.9785, Target: 0.9885, Stop: 0.9750

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9795, Target: 0.9895, Stop: 0.9760

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after staging a strong rebound from 0.9735 (last Friday’s low), adding credence to our view that a temporary low has been formed there and consolidation with upside bias remains for gain to last week’s high at 0.9882, however, a sustained breach above this level is needed to confirm this view and bring at least a retracement of recent decline to 0.9900 and later towards resistance at 0.9947.

In view of this, we are looking to buy dollar on dips as 0.9775-85 should limit downside and bring another rebound. Below 0.9750 would risk a retest of said last week’s low at 0.9735 but only break there would signal the decline from 1.1038 top has resumed for weakness to 0.9705 support.

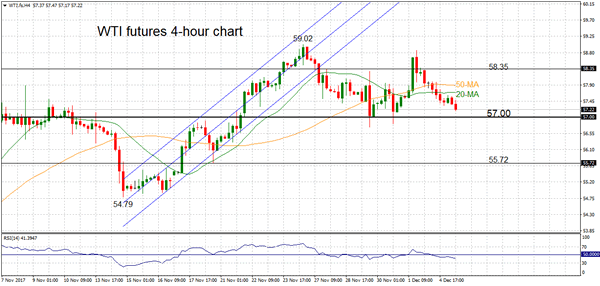

WTI Oil Futures In Bearish Phase But Maintain Medium-Term Neutral Outlook

WTI oil futures have unwound almost all of the gains made from the recent rally off the key 57 level. The near-term bias is to the downside and last Friday’s 58.86 high remains unchallenged.

Technicals are bearish on the 4-hour chart. The market has dropped below the 20 and 50-period moving averages which are negatively aligned. The RSI has fallen below 50.

Prices are expected to grind lower with the next target at the key 57 level. This level has held strong support during the past two weeks, keeping the market neutral in the medium-term. A break below 57 would strengthen the bearish momentum to target previous lows at 55.72 and 54.79.

Only a clear break above 58.35 would open the way for a re-test of the more than two-year high of 59.02. The odds for clearing this peak are low in the near term.

The medium-term neutral outlook is expected to remain in place with more range trading above the 57 base as the market enters a consolidation phase following the rally from 54.79 to 59.02.

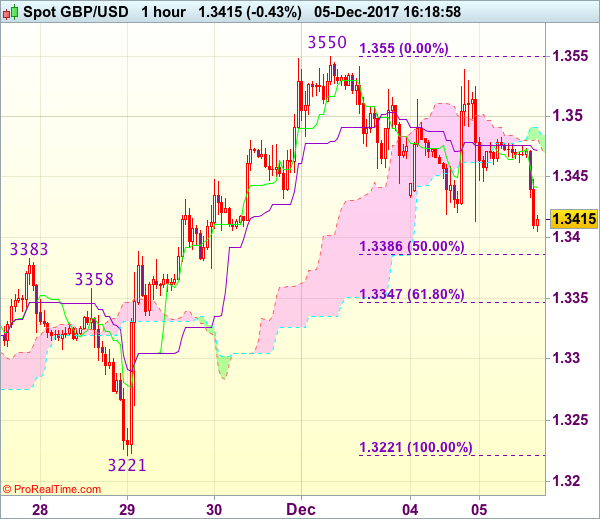

Trade Idea : GBP/USD – Target met and sell at 1.3440

GBP/USD - 1.3392

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3425

Kijun-Sen level : 1.3455

Ichimoku cloud top : 1.3491

Ichimoku cloud bottom : 1.3482

Original strategy :

Sold at 1.3500, met target at 1.3400

Position : - Short at 1.3500

Target : - 1.3400

Stop : -

New strategy :

Sell at 1.3440, Target: 1.3340, Stop: 1.3475

Position : -

Target : -

Stop : -

Current selloff has reinforced our view that top has been formed at 1.3550 and consolidation with downside bias remains for the fall from 1.3550 to bring retracement of recent rise, hence further weakness to 1.3340-50 (61.8% Fibonacci retracement of 1.3221-1.3550) would be seen, however, near term oversold condition should prevent sharp fall below 1.3300 and reckon 1.3260-65 would hold, bring rebound later.

In view of this, we are looking to reinstate short on recovery as 1.3440-50 should limit upside.Above the Kijun-Sen (now at 1.3455) would defer and risk test of resistance at 1.3483 but only break there would signal an intra-day low is formed instead, bring another bounce to 1.3530-35 first.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

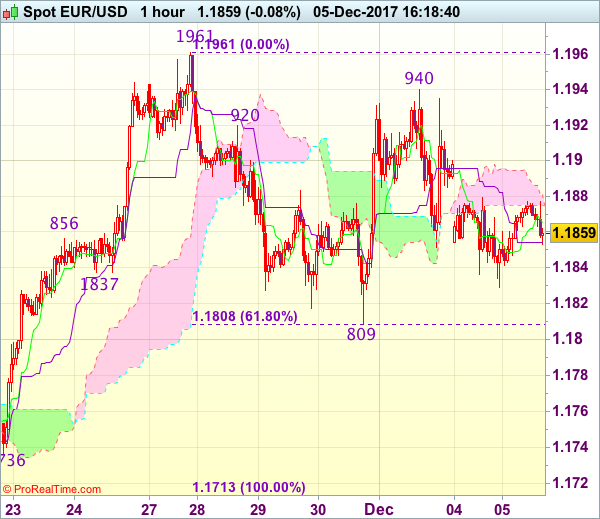

Current level - 1.1866

The forecast is for another test of the support level at 1.1808 down to 1.1740. In positive direction the next resistance level will be at 1.1932 and after that at 1.1962.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1932 | 1.2090 | 1.1824 | 1.1690 |

| 1.1960 | 1.2090 | 1.1811 | 1.1550 |

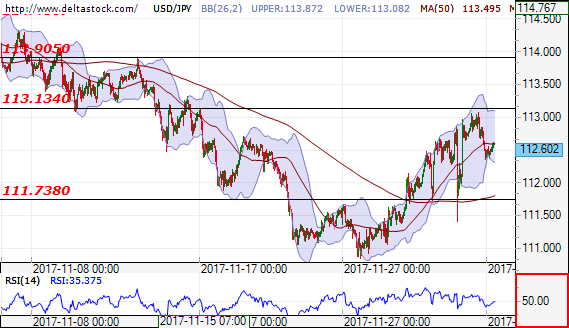

USD/JPY

Current level - 112.602

The outlook is still positive for breakthrough of the resistance level at 113.1340. That will lead to increase of the price of the currency pair and test at 113.9050. In negative direction the resistance level is at 111.7380.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.72 | 113.90 | 111.73 | 109.50 |

| 113.13 | 114.70 | 109.50 | 107.30 |

GBP/USD

Current level - 1.3465

The outlook is negative for test of the support level at 1.3370. Successful breakthrough of this level will lead to another test at 1.3219. In positive direction if we have a successful breakthrough of the resistance level at 1.3550, we might expect increase up to 1.3623.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3550 | 1.3460 | 1.3370 | 1.3220 |

| 1.3623 | 1.3660 | 1.3219 | 1.3020 |

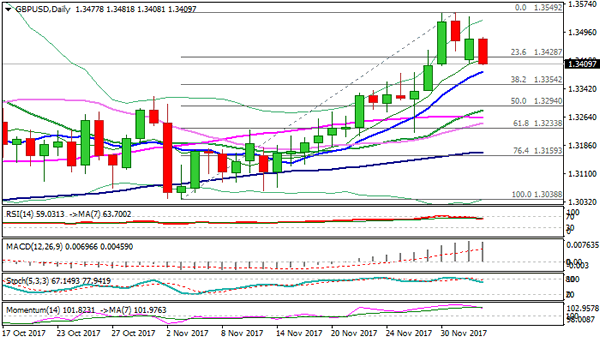

Technical Outlook: GBPUSD – Overall Bullish Bias Sees Deeper Correction Preceding Fresh Rally

Cable stands at the back foot in early Tuesday's trading and pressuring Monday's low at 1.3412, n bearish acceleration from Asian high at 1.3481.

Yesterday's strong upside rejection near key 1.3549 barrier and subsequent pullback was negative signal, with near-term sentiment turning into negative mode following disappointing news from Brexit talks on Monday.

The pair is likely to extend correction after repeated rejections at 1.3549 tops and challenge pivotal support provided by rising 10SMA (currently at 1.3391).

Corrective dips are seen as an opportunity to re-join broader uptrend. Ascending 10SMA is initial entry point, but deeper pullback towards strong support at 1.3354 (Fibo 38.2% of 1.3038/1.3549 ascend) cannot be ruled out.

Sustained break below 1.3354 would soften near-term structure, while loss of daily Kijun-sen (1.3294) will be bearish signal.

Res: 1.3481, 1.3500, 1.3549, 1.3595

Sup: 1.3391, 1.3354, 1.3294, 1.3233

Currencies: Dollar Rebound Stalls Despite Rising Interest Rate Support

Sunrise Market Commentary

- Rates: Front end US yield curve rises further

The main item on today's agenda is the US non-manufacturing ISM which is expected to remain very strong. In theory, that's negative for US treasuries, but we don't expect a strong reaction. The front end of the US yield curve continues to underperform, discounting already two rate hikes for 2018 going into next week's FOMC meeting. - Currencies: Dollar rebound stalls despite rising interest rate support

The dollar profited temporary from the tax bill approval in the US Senate yesterday, but the rally stalled as US equities turned south. Today's eco data probably won't cause a big directional USD move. Even so, the ongoing rise in ST US yields is making USD shots expensive and should protect the USD downside going into the payrolls and next week's Fed meeting

The Sunrise Headlines

- US stock markets ended varied with Nasdaq (-1%) underperforming as a last-minute change to Senate Republicans' tax-overhaul plan may mean higher taxes for corporations, including IT firms. Asian bourses trade mixed overnight.

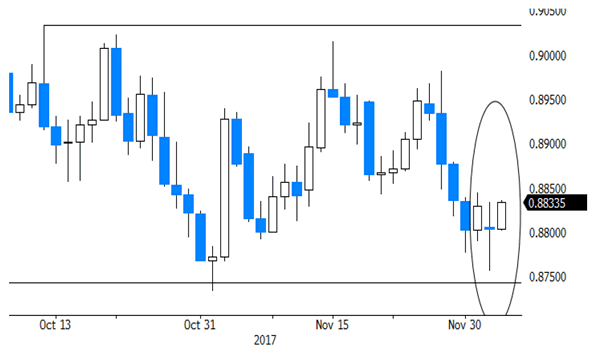

- A carefully choreographed divorce deal between London and Brussels was derailed at the eleventh hour after Northern Ireland's hardline Unionists rejected Theresa May's agreement to potentially keep the province aligned with EU law after Brexit. EUR/GBP rose back above 0.88.

- Growth in China's services sector activity picked up to a three-month high in November (PMI: 51.9), buoyed by a solid rise in new business, though the rate of expansion remained moderate and weaker than the long-run trend.

- The Reserve Bank of Australia kept its policy rate unchanged at 1.5%, but a shift in the inflation language signalled that the central bank is arguably offering a less dovish tone. AUD/USD rises from 0.76 to 0.7650.

- The Reserve Bank of New Zealand's new assumption that global inflation will stay lower for longer means it is more exposed to the risk of prices picking up, Acting Governor Spencer said. NZD/USD moves higher towards 0.69.

- European Finance Ministers shifted power from the north of the continent to the south, providing a boost to opponents of austerity policies. They chose Portugal's FM Centeno to lead the Eurogroup to succeed Dijsselbloem.

- Today's eco calendar contains November services PMI's in EMU (final), the UK and the US (ISM). EMU retail sales are also up for release

Currencies: Dollar Rebound Stalls Despite Rising Interest Rate Support

Dollar rebound stalls despite higher ST yields

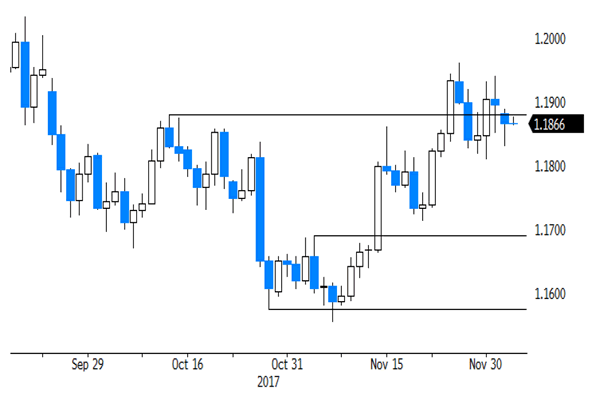

European (and US) markets initially reacted in a positive way to the approval of the US tax bill. European equities jumped higher. ST US yields rose further and the dollar extended cautious gains. USD/JPY tested the 113 area. The gain of the dollar against the euro was again more limited. Later in US dealings, tax optimism dwindled, reversing most of the intraday ‘reflation trade'. The dollar returned a big part of the early gains. USD/JPY closed the session at 112.41 (from 112.17 on Friday). EUR/USD finished the day at 1.1866 (from 1.1896). Asian equity indices show a mixed picture. A new setback in US tech stocks also affects (parts of) the Asian markets. The dollar ‘bottoms' after the late session setback in the US yesterday evening. USD/JPY trades in the 112.60 area. EUR/USD is changing hands near 1.1870 area. The RBA as expected left its policy rate unchanged at 1.50%, but expects that a stronger labour market could see some lift in wage growth over time. Better than expected retail data also supported the Aussie dollar. AUD/USD trades in the mid 0.76 area. The kiwi dollar made some modest gains after RBNZ's Spencer indicated that the bank could give more weight to output employment and financial stability.

The eco calendar contains the final EMU (services) PMI's, EMU retail sales and the US non-manufacturing ISM. EMU PMI's are expected to confirm the strong growth momentum (57.5 for the composite PMI). Retail sales are expected to have declined in October (-0.7% M/M and 1.6% Y/Y). We don't expect the EMU data to have a lasting impact on the euro. The US non-manufacturing ISM is expected to ease slightly from 60.1 to 59, still a very high level. Last week's manufacturing ISM showed a similar pattern. We have no reason to take a different view from the consensus. Of late, markets mostly reacted rather muted to (US) activity data. Investors are more sensitive to price data.

The dollar showed a mixed picture last week, rebounding against the yen but holding relatively soft against the euro. Yesterday, the pattern initially continued, but the USD rebound was aborted by a new up-tick in US equity volatility later in the session yesterday. The US 2-yr yield continues an astonishing rise (currently above 1.80%!), but it was only of little help for the dollar of late. Even so, it should at least help to put a floor for the US currency as USD shorts are becoming ever more expensive. We don't expect a really big directional move ahead of next week's Fed policy decision/statement.

That said, except for high profile negative news from the US (or negative risk sentiment) we see no reason for EUR/USD to rise beyond the 1.1961/1.20 area. The downside of USD/JPY looks better protected, but the rebound might slow if it isn't supported by developments on other markets.

From a technical point of view: EUR/USD set a post-ECB low mid-November, but dollar momentum wasn't strong enough. EUR/USD regained the 1.1880 MT correction top, opening the way for a full retracement to the 1.2092 top. A return below 1.1713 would signal that the rebound in EUR/USD is aborted. For now, there is no clear technical signal. The USD/JPY momentum deteriorated early November. USD/JPY dropped below the 111.65 neckline, but there was no aggressive follow-through selling. Last week the pair even succeeded a nice rebound, calling off the downside alert. The pair again hovers in the 110.84/114.73 consolidation range. We amend our ST bias on the pair from negative to neutral.

EUR/USD: rally aborted, but no clear trend yet

EUR/GBP

Sterling hit by last-minute Brexit failure

Brexit headlines caused a rollercoaster ride for sterling yesterday. UK PM May met with EU Commission president Juncker. EUR/GBP initially hovered in the 0.8825 area. Around noon there were press headlines from several sources that EU's Barnier had indicated that negotiations on the separation issues were headed for a breakthrough. Sterling jumped higher across the board as markets assumed that Brexit negotiations could move to the content of the new relationship between the UK and the EU post Brexit. However, at a joined press conference, UK PM May and EC's Juncker said that progress had been made, but no final agreement was reached. Sterling reversed most of the intraday gains. EUR/GBP finished the session at 0.8803. GBP closed the session at 1.3480.

Overnight, BRC UK retail sales rebounded to 0.6% Y/Y. However, it doesn't help sterling. The UK currency remains under pressure. Markets are disappointed on yesterday's last minute failure to reach a separation deal. Both parties are still trying to reach a deal to be proposed to the EU summit next week. Yesterday's failure is the perfect illustration of the difficult balancing act that PM May faces and will continue to face during the next stages of the negotiations. Today, the UK services PMI will be published. A slight decline from 55.6 to 55 is expected. The report probably will only be of intraday significance for sterling trading. The focus remains on Brexit. Sterling remains in the defensive, unless there is hard evidence of a deal.

MT view/technical picture: A BoE driven sterling rebound ran into resistance early last month. Sterling declined again as markets anticipated that the rate cycle would be very gradual and limited. EUR/GBP trades in a 0.8733/0.9033 consolidation range. Brexit headlines cause day-to-day gyrations. We changed our ST bias on EUR/GBP from positive to neutral mid-November. The 0.9015/33 area might be tough to break short-term. In case of more positive news on Brexit, return action to the 0.8733 (or below) level is possible ST.

EUR/GBP: downside test rejected as Irish border deal fails last minute

Trade Idea : EUR/USD – Sell at 1.1915

EUR/USD - 1.1857

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1865

Kijun-Sen level : 1.1854

Ichimoku cloud top : 1.1881

Ichimoku cloud bottom : 1.1875

Original strategy :

Sell at 1.1915, Target: 1.1815, Stop: 1.1950

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1915, Target: 1.1815, Stop: 1.1950

Position : -

Target : -

Stop : -

As the single currency recovered after holding above support at 1.1809, retaining our view that further consolidation below resistance at 1.1961 (last week’s high) would be seen and mild downside bias remains for weakness towards support at 1.1808-09 (61.8% Fibonacci retracement of 1.1713-1.1961 and previous support), however, break there is needed to retain bearishness and extend weakness to 1.1770 and possibly to support at 1.1736 but price should stay above previous key support at 1.1713.

In view of this, we are looking to sell euro on recovery as 1.1910-20 should limit upside and bring another decline. Above said Friday’s high at 1.1940 would revive bullishness, bring retest of 1.1961, break there would confirm early upmove has resumed for headway to 1.1990-00 which is likely to hold from here.

XAUUSD Intraday Analysis

XAUUSD (1275.40): Gold prices continue to remain flat with price action showing strong consolidation near the 1274 level of support. Failure to establish a clear trend suggests that the sideways price action might continue. Below the 1274 support, gold prices could be at risk of posting a decline towards the 1262 support level. To the upside, the 1285 resistance is likely to maintain the gains in the near term. On an intraday basis, gold prices could be seen posting a modest rally to fill Friday's gap at 1280.46 but further gains beyond this could be limited.