Sample Category Title

ECB QE: German Purchases Suggest no ISIN Restriction in 2018, While Irish Purchases Have Doubled in Q4

QE figures for November showed monthly German PSPP purchases in line with the previous month (EUR11.5bn). The monthly purchases in November fully reflect the new QE horizon (until end September 2018) i.e. the November figure suggests that QE purchases in Germany are unlikely to be constrained by the ISIN restriction within the announced QE horizon.

The reported figures are increasingly 'distorted' by redemption and reinvestment effects, highlighted by Irish net purchases being at an all-time high of EUR1.2bn in November, up from EUR-32m in October. Gross purchases (including reinvestments) have likely been above EUR1bn in both October and November (See chart) reflecting the combination of reinvestment flows and issuer constraint no longer being a constraint. We expect this to be the case in December as well. Distortion due to reinvestments is also visible in the Finnish figures which have returned to 'normal' following elevated reported figures in October (EUR1.1bn) and a low September figure (EUR0.2bn).

Note that total QE in December is set to slow into the year-end with 21 December being the last day of QE purchases in 2017 and total December purchases of c.EUR50-53bn.

Redemption details for the next 12 months. Total QE redemptions (December 2017 to November 2018) amount to EUR133.7bn of which EUR104.1bn is in PSPP.

Aussie Awaits RBA’s Rate Decision But Eyes on Consumption

"If the economy continues to improve as expected, it is more likely that the next move in interest rates will be up, rather than down," said the RBA Governor, Philip Lowe in his speech at the Australian Business Economists' annual dinner two weeks ago. But then he immediately highlighted that in the near term, an adjustment in monetary policy is not strongly considered as inflation remains subdued while the economy has still room for growth. Given this statement, RBA policymakers are less likely to raise interest rates in their policy meeting on Tuesday. However, GDP growth readings out of Australia on Wednesday and particularly the consumption component of the measure are expected to draw more attention and therefore generate greater volatility to the Australian dollar.

On Tuesday, the RBA is anticipated to hold interest rates unchanged at a record low of 1.5% for the sixteenth consecutive meeting. Even though inflation is not far away from the central bank's target of 2.0% (1.8% y/y in Q3 2017), as is the case in other economies, including the US, Japan and the EU, policymakers are said to avoid exiting monetary stimulus for the moment as Australian household debt-to-GDP is still among the highest in the world (122% as of March 2017). Besides that, the wage growth has so far shown a slow reaction to the RBA's easy monetary policy, continuing to trend at record low levels since stimulus implementation despite the unemployment rate hitting a four-year low of 5.4% in October. Regarding that, rate setters believe that companies refuse to increase wages as they also face strong competition by new entrants. Higher interest rates are thus not expected to boost consumers' purchasing power but instead squeeze disposable income (due to high debt levels that need to be serviced) and consequently harm consumption which accounts for half of Australia's economic growth.

A day after the RBA's rate decision, the Australian Bureau of Statistics will publish figures on GDP growth, with analysts predicting an expansion of 3.0% y/y in the third quarter compared to 1.8% seen previously. However, on a quarterly basis, forecasts see the growth rate slowing down by 0.1 percentage points to 0.7%. Household final consumption expenditure will be also in main focus on Wednesday as any decreases in household spending would indicate that economic growth will likely suffer in the upcoming quarters. First evidence on consumption could be given by retail sales figures due on Tuesday as well. According to forecasts, retail sales might post positive growth in October for the first time in three months, rising by 0.3% m/m.

Even if the RBA decides to leave rates unchanged tomorrow, an increasing gap between the Australian and the US interest rates would force the central bank to reduce stimulus in the subsequent periods given that the Fed is considering to keep raising rates in the coming years. With the US banks offering attractive deposit rates, the Australian banks will be forced to raise mortgage rates to some extent to attract deposits, hurting the already indebted consumers even more.

Turning to forex markets, the aussie is currently consolidating near six-month low levels, maintaining a bearish bias below the Ichimoku cloud and the exponential moving average lines. The RSI is below 50, suggesting that negative movements are more likely to occur in the near term. However, the oscillator is pointing to the upside, hinting that the pair might move upwards for a while before it resumes its downtrend (The RSI is marginally above 50 in the 4-hour and the 1-hour chart). Should Australian data disappoint, the pair might find immediate support at the previous low of 0.7531. Steeper decreases could also approach the one-year low of 0.7328. Alternatively, encouraging economic releases would shift focus to the previous high of 0.7644, while the 0.7700 key level could be a strong resistance as the 50-day and the 200-day EMA are also laying in that area. A close above the EMA lines could turn the bias from bearish to bullish.

Brexit Bringdown, RBA Next

Ireland is a fresh thorn in the side of Theresa May as she attempts to score a Brexit victory. The Canadian dollar was the top performer while the Swiss franc lagged. The RBA decision is up next. The EURUSD Premium short was closed for 60-90 pip gain (depending on entry), while a new JPY trade was issued.

Cable climbed early in trading on Monday on expectations for a breakthrough in EU/UK negotiations. Rumors of a divorce settlement were rampant last week and today was supposed to be the announcement. However, May and Juncker were forced to call off meetings after May's coalition partners from the Irish DUP said they wouldn't accept any form of regulatory divergence between the Britain and Northern Ireland.

The breakdown sent cable more than 100 pips lower on the headlines to just above 1.3400. It eventually bounced to 1.3475 but the quick rise and fall on the day were a reminder of a large intraday risks for GBP traders.

Meanwhile, the optimism from the Trump-Russia story faded in stocks as tech led a retreat. The Nasdaq closed 1% lower in a fresh sign of weakness. The drop came despite the GOP passing tax reform in the Senate and the correction on the ABC story. That's a sign that the good news might be priced in and that markets are increasingly concerned about a hawkish Fed.

USD/JPY followed stocks lower to close near 112.50 after rising above 113.00 early.

Looking ahead, the Australian dollar will be hogging the spotlight. First are the Aussie Q3 current account and October retail sales reports at 0030 GMT. Those are followed by the RBA decision at 0330 GMT. The overwhelming consensus is for no move from the 1.50% cash target and no signs of a shift. We will look for comments on wages and global growth as potential market movers.

The Pound Trades Like an Old Beach Roller Coaster

Equity markets have remained cheered up by the passage of the Senate tax reform bill. But the market closed below interday high water marks as renewed weakness in the tech sector weighed at the bell. However, it's not as if the tech sector is under stress but rather some equities rotation remain in vogue as investors seek out opportunities in more tax reform sensitive stocks.

So much for what was supposed to be the dollar's day in the Sun, the G-10 focus was all about Brexit and Cable.

The British Pound

Last nights crucial negotiations put the Pound through a wringer.The initial headlines looked positive after some encouraging news on the almost unresolvable question of the Irish border sent the Pound skyrocketing to 1.3540 The move was then wholly unwound and some when " no complete deal today " was announced. While the Brexit divorce arrangements looked close on Monday, the talks failed as the DUP reservations scuttled the proposal.

As is so often the case in FX markets, after all was said an done, we are right back to where we started

The Japanese Yen

The USDJPY has come under pressure on reports the Japan is readying it's " intercept command system starting in fiscal 2018 to cope with advancements in North Korea's weapons technology, such as faster-descending missiles launched at a steeper trajectory."( Nikkei news). But the USDJPY and US yields were trading with a heavy tone overnight almost as if waiting for the next wave of risk aversion to rear its ugly head and this morning's geopolitical gamesmanship continues to validate this concern.

On the flip side, one of the best trades of the year has been to fade USDJPY's geopolitical hysterics, but this move is far too shallow to bring out risk hunters but regardless its hard to envision a broader push lower given the more widespread positive USD sentiment. And at least for today, it looks like we're back to the old tug of war between US yields and risk sentiment as we to settle back into the battle-tested 111.75-113.25 range

The Euro

Not sure if it's year-end creeping in early but he Euro refuses to show any clear direction so providing market commentary is turning into an exercise in repetition. But it could be a case of the market in total data focus mode and unwilling to commit to any direction ahead of US NFP or more precisely the wages component. However most traders remain incredibly constructive on the EURO, but as year-end approaches, traders are timing their entry decision more precisely

The Australian Dollar

RBA decision day, comments to follow.

In early trade, the Aussie is picking up some pre-RBA steam from the positive retail sales print

Energy market

Traders are starting to look over their shoulder at a potential Shale production swell. Invariably we end up back it this inflexion point time and time again which continues to undercut OPEC reduction momentum.

Also, there could be some year-end decision at play as trading the " turn" can be full of liquidity surprises.

Asia FX

The Good, Bad, and Ugly for regional currencies as idiosyncratic narratives are driving trading decisions

The Malaysian Ringgit ( The Good)

A fantastic 24 hours for the Ringgit as yesterday's PMI, hitting 43 months high at 52 supports the hawkish BNM narrative. The Malaysian Centeral Bank has sounded overtly hawkish of late and appears more open to a stronger currency to ward off potential inflation.

Given the market is baking in January rate hike with a likely Q2 or 3 follow up, so the MYR will become much more sensitive to economic data for the next few months. And this is what happened yesterday as the Ringgit surged on very supportive data.

However, a follow-up rate hike in Q2 or 3 well l is 100% data dependent suggesting we will continue to see see the Ringgit trade more sensitive to Growth and Inflation headlines for the next few months.

Also, foreigners were noted buyers on local equity markets which added to the frothy MYR conditions

The market remains underweighted on MYR so despite more naysayers jumping on the wagon, there still lots of room on the party bus.

Korean Won ( The Bad)

The USDKRW has continued to trade dollar bid in the wake of the dovish BoK hike. Investor propensity to move out of tech into to financial stocks dulls KOSPI sentiment.And this morning risk aversion blip on Japans defence system headlines isn't helping KRW risk this morning.

The Philippine Peso ( The Ugly)

A horrible 24 hours for the local currency as both the PSEi and the Peso cratered. Whatever tactical shorts were entered last week on the regional wave of positivity gave way to more aggressive USD buying post-US tax reform.

To put the local equity market move in perspective Philippine stocks suffered one of the most significant 2-day drop this year!

But this reinforces the view that their remains substantial structural differences at play in the Peso relative to regional peers. Last week there was little if any sizable stock or bond inflow to drive or sustain momentum which left the PHP extremely susceptible to a stronger USD narrative.

Market Musings

Why isn't the dollar trading higher?

- Extremely unclear what the actual GDP impact will be relatively Budget woes.

- Political risk will forever be baked into the USD narrative so long as President Trump remains in office

- The dollar momentum is more about Fed funds rate and inflation rather than tax reform

Canadian Dollar Flat After Loonie Rally Loses Steam

The Canadian dollar fell slightly on Monday after the optimism surrounding the US tax reform has wavered as concerns about the debt load sapped the USD of momentum. The loonie was boosted on Friday by a massive Canadian jobs report for November. The economy added 79,500 jobs and the unemployment rate fell to 5.9 percent. Gross domestic product (GDP) also come in above forecast, but less impressive at a 0.2 percent monthly gain. The surprise increase in employment took the CAD from deep in the red to ending the week ahead of the USD despite the US Senate tax bill chances of passing being high.

The GDP validated the slowdown of the economy in the third quarter but with strong employment data the Canadian economy could make an improvement sooner rather than later. The Bank of Canada (BoC) hiked interest rates twice in 2017 back to the 1.00 percent level. Governor Poloz had cut twice in 2015 to avoid a deeper negative impact of falling oil prices. The actions of the Organization of the Petroleum Exporting Countries (OPEC) and other major producers to band together in agreement to cut production has stabilized oil prices. The weaker Canadian dollar also helped boost exports and attracted investment jolting the economy to a surprise GDP gain of 4.5 percent, the best pace in six years. The third quarter report in contrast shows a gain of 1.7 percent in annual terms.

The loonie posted a five week high after the strong jobs and improved third quarter GDP. Some of the gains were taken back by the rise in the USD after the weekend's vote on the Senate tax bill. A Reuters survey of 103 economists revealed that three US interest rate hikes are expected in 2018. The poll also showed that the December rate hike has a high probability and will come in at 25 basis points, the third rate hike of 2017. The rest of the week will be dominated by US jobs data (ADP and NFP reports) and the Bank of Canada (BoC) rate statement on Wednesday.

The USD/CAD lost 0.7 percent on Monday. The currency pair is trading at 1.2675 after the loonie retraced after the US Senate passed its version of the tax bill over the weekend. Geopolitics continue to keep the USD in check as the Trump Administration is fielding multiple investigations into their presidential campaign and a crowdsourced effort by citizens threatens to derail the promised tax reforms. Since both the House and the Senate passed their own versions they now need to be merged into a cohesive bill in order to pass.

The Bank of Canada (BoC) is not expected to modify its benchmark rate on Wednesday, December 6 at 10:00 am EST. The overnight rate is 1.00 after the last 25 basis points hike in September and given the slowdown of economic growth economists do not foresee a hike until next year. US interest rate moves are highly anticipated with the December decision near 100 percent probability but already priced into the dollar. The Reuters poll keeps a hawkish forecast on the Fed that will get a new Chair in February as Fed Chair Janet Yellen steps down.

Canadian Prime Minister Justin Trudeau is in China on with the intention to build a plan B on trade in case NAFTA ends up disappearing. While not exactly a perfect replacement a deal with China could diversify Canada's reliance on its neighbour to the south, but given the long negotiation periods for this type of deals it could be a decade before it is signed. The meeting between Trudeau and Chinese Premier Li Keqiang was positive with China showing an open attitude.

Energy prices started the week on a down note. The price of West Texas Intermediate is trading at $57.34. Crude prices have been trading in a tight range at the start of the week with all the spotlight on the US ahead of the release of employment data. Dollar strength has hurt commodities and for some investors was a signal for profit taking. The announcement of the 9 month extension of the production cut agreement between Organization of the Petroleum Exporting Countries (OPEC) and other major producers took WTI to near $58.60 per barrel. Oil prices will be awaiting Tuesday's afternoon API's stock data and the official Energy Information Administration (EIA) weekly crude inventories released on Wednesday at 10:30 am EST.

Market events to watch this week:

Monday, December 4

- 7:30pm AUD Current Account

- 7:30pm AUD Retail Sales m/m

- 10:30pm AUD Cash Rate

- 10:30pm AUD RBA Rate Statement

Tuesday, December 5

- 4:30am GBP Services PMI

- 8:30am CAD Trade Balance

- 10:00am USD ISM Non-Manufacturing PMI

- 7:30pm AUD GDP q/q

Wednesday, December 6

- 8:15am USD ADP Non-Farm Employment Change

- 10:00am CAD BOC Rate Statement

- 10:00am CAD Overnight Rate

- 10:30am USD Crude Oil Inventories

- 7:30pm AUD Trade Balance

Thursday, December 7

- 8:30am USD Unemployment Claims

- 11:00am EUR ECB President Draghi Speaks

Friday, December 8

- 4:30am GBP Manufacturing Production m/m

- 8:30am USD Average Hourly Earnings m/m

- 8:30am USD Non-Farm Employment Change

- 8:30am USD Unemployment Rate

*All times EDT

Pound Yawns as Construction PMI Beats Expectations

The British pound has ticked higher in the Monday session. In North American trade, GBP/USD is trading at 1.3455. On the release front, British Construction PMI in November looked sharp, accelerating to 53.1 points, above the forecast of 51.2 points. This marked the highest level since June. In the US, Factory Orders declined 0.1%, the first decline since July. Still, this beat the forecast of -0.3%. On Tuesday, the UK releases Services PMI, which is forecast to dip to 55.2 points. The US publishes ISM Non-Manufacturing PMI, with the markets expecting the indicator to slow to 59.2 points.

After sweetening the British offer over its Brexit bill last week, Prime Minister Theresa May is anxious to change the focus of the Brexit negotiations and talk trade with Europe. Prime Minister May and European Commission President Jean-Claude Juckner met earlier on Monday in Brussels, hoping to move closer to wrapping up the first phase of the talks. May has moved closer to the European's demands on a divorce bill of around EUR 50 billion, but two items have yet to be resolved. One is the border between the UK (Northern Ireland) and Ireland, which is a member of the EU. The UK will clearly not remain in a customs union with the EU, but Ireland is insistent that there not be a hard border. The second issue is whether the European Court of Justice will have a role protecting European citizens in the UK. The EU is in favor of a role for the court, while many British lawmakers feel that such a move would impinge on British sovereignty.

President Trump has asked lawmakers in Washington for a tax reform bill for Christmas, and Congress, at least on the Republican aisle, appears to be in a giving mood. After a false start and some anxious hours on Friday, the US Senate passed a tax reform bill on the weekend. The vote was a squeaker, with 51 Republicans voting yes, against 48 Democrats and 1 Republican. The Senate vote is a big win for President Trump, as tax reform would mark his first major legislative bill in office, after a stinging defeat in trying to pass a new health care bill. The Senate and House must now reconcile their two tax bills, and the new uniform bill will then have be passed in both houses. Investors are pleased with the legislation, and the dollar and the stock markets could continue to gain as a result of positive market sentiment.

Gold Slips as Factory Orders Beats Estimate

Gold has started the week with losses, erasing the gains seen in the Friday session. In the Monday North American session, the spot price for an ounce of gold is $ 1274.23, down 0.50% on the day. In the US, Factory Orders declined 0.1%, the first decline since July. Still, this beat the forecast of -0.3%. On Tuesday, the US publishes ISM Non-Manufacturing PMI, with the markets expecting the indicator to slow to 59.2 points.

President Trump has been pressing for a major legislative win before the end of the year, and it looks like he'll get tax reform all wrapped up in time for Christmas. The Republicans have pushed through tax legislation through the House and the Senate at breakneck speed. After a false start on Friday, the US Senate passed a tax reform bill on the weekend. The 51-49 vote was a squeaker, with 51 Republicans voting yes, against 48 Democrats and 1 Republican. Republican lawmakers hope to have Trump sign a bill before the end of the year. The Senate and House must now reconcile their two bills, and the new uniform bill will then have be passed in both houses. Investors are pleased with the bill, and the US dollar has responded to the vote with broad gains.

Gold could be marked by volatility in the upcoming weeks. Gold prices are inversely linked to interest rate hikes, and with the markets widely expecting rate hikes in December and January, traders should be prepared for some movement from gold. As well, there are major changes taking place at the Federal Reserve, as Jerome Powell is set to replace Janet Yellen as Fed chair in February. Powell didn't make any waves at his confirmation hearing last wee, although his comments on relaxing regulations for smaller banks did send global stock markets higher. Powell inherits a strong US economy, and this could mean several rate hikes in 2018, if the economy maintains its current pace. Still, inflation remains stubbornly low, and with Fed policymakers divided on whether to keep the 2 percent inflation target, the markets will be keeping close tabs on how Powell deals with inflation when he takes over the helm of the Fed.

Yen Steady, Japanese Inflation Report Ahead

The Japanese yen has inched lower in the Monday session. In North American trade, USD/JPY is trading at 112.74. On the release front, Japanese Consumer Confidence increased to 44.9, edging above the estimate of 44.8 points. Although the Japanese consumer remains pessimistic, this marked the strongest reading since September 2013. In the US, Factory Orders declined 0.1%, the first decline since July. Still, this beat the forecast of -0.3%. On Tuesday, the BoJ releases Core CPI, which is expected to remain unchanged at 0.5%. The US publishes ISM Non-Manufacturing PMI, with the markets expecting the indicator to slow to 59.2 points.

President Trump has been pressing for a major legislative win before the end of the year, and it looks like he'll get tax reform all wrapped up in time for Christmas. The Republicans have pushed through tax legislation through the House and the Senate at breakneck speed. After a false start on Friday, the US Senate passed a tax reform bill on the weekend. The 51-49 vote was a squeaker, with 51 Republicans voting yes, against 48 Democrats and 1 Republican. Republican lawmakers hope to have Trump sign a bill before the end of the year. The Senate and House must now reconcile their two bills, and the new uniform bill will then have be passed in both houses. Investors are pleased with the bill, and the US dollar has responded to the vote with broad gains.

Bank of Japan Governor Haruhiko Kuroda spoke at the Europlace financial forum in Tokyo on Monday, but there was nothing new in his message about where the BoJ is headed. Kuroda reiterated that the Bank would maintain its ultra-accommodative monetary policy in order "to achieve the 2 percent inflation target as soon as possible". The BoJ has been forced to constantly lower its inflation projections, yet the Bank has stubbornly stuck to the 2 percent target. Although the labor market remains tight, this has not translated into higher wages for workers, and nervous consumers have held tight to their purse strings, further contributing to a lack of inflation. Kuroda noted that global economic growth had improved, although he sounded a note of concern about President's Trump isolationist policy, saying that he hoped that global trade would be conducted under the multilateral trading system.

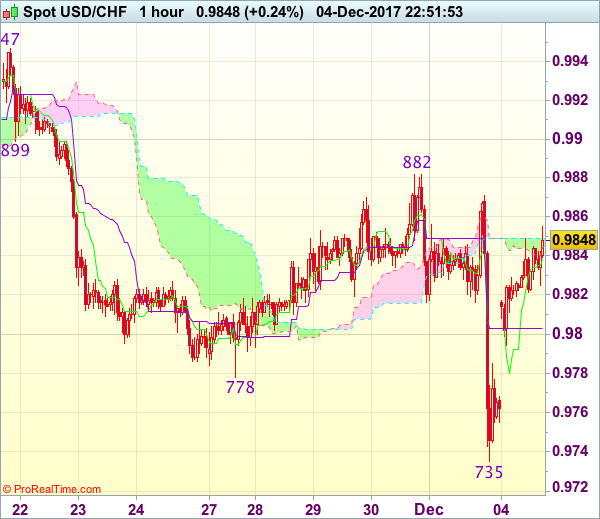

Trade Idea Wrap-up: USD/CHF – Buy at 0.9785

USD/CHF - 0.9845

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9838

Kijun-Sen level : 0.9803

Ichimoku cloud top : 0.9849

Ichimoku cloud bottom : 0.9846

Original strategy :

Buy at 0.9785, Target: 0.9885, Stop: 0.9750

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9785, Target: 0.9885, Stop: 0.9750

Position : -

Target : -

Stop : -

Although the greenback dropped sharply to as low as 0.9735 on Friday, the subsequent reversal on dollar’s broad-based strength suggests low is formed there and consolidation with upside bias is seen for gain to last week’s high at 0.9882, however, a sustained breach above this level is needed to confirm this view and bring at least a retracement of recent decline to 0.9900 and later towards resistance at 0.9947.

In view of this, we are looking to buy dollar on dips as 0.9775-85 should limit downside and bring another rebound. Below 0.9750 would risk a retest of said last week’s low at 0.9735 but only break there would signal the decline from 1.1038 top has resumed for weakness to 0.9705 support.

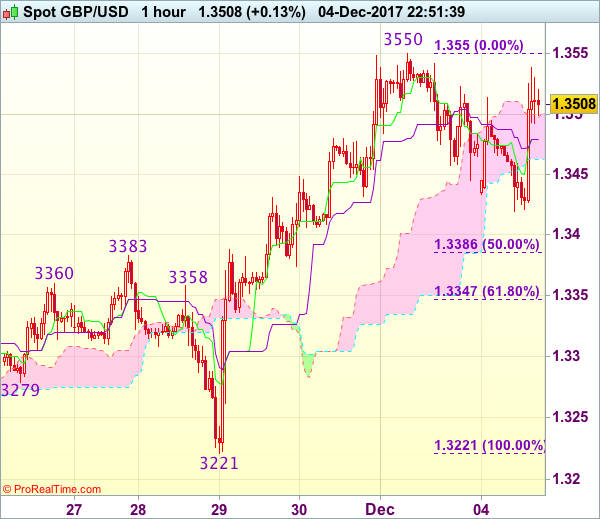

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.3500

GBP/USD - 1.3519

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3479

Kijun-Sen level : 1.3479

Ichimoku cloud top : 1.3501

Ichimoku cloud bottom : 1.3462

Original strategy :

Sold at 1.3500, Target: 1.3400, Stop: 1.3535

Position : - Short at 1.3500

Target : - 1.3400

Stop : - 1.3535

New strategy :

Hold short entered at 1.3500, Target: 1.3400, Stop: 1.3535

Position : - Short at 1.3500

Target : - 1.3400

Stop : - 1.3535

Although cable has rebounded after finding support at 1.3419 and further consolidation would be seen, reckon upside would be limited to 1.3530-35 and bring retreat later, below said support at 1.3419 would bring retracement of recent rise for weakness to 1.3400, however, reckon downside would be limited to 1.3380-85 (50% Fibonacci retracement of 1.3221-1.3550) and bring rebound to 1.3500 but upside should be limited to 1.3515-25, bring another corrective decline later.

In view of this, we are holding on to our short position entered at 1.3500. Above 1.3535-40 would signal the retreat from 1.3550 has ended, bring retest of this level, then 1.3575-80 but reckon 1.3600-10 would hold. Below 1.3345-50 (61.8% Fibonacci retracement of 1.3221-1.3550) would abort and signal top has been formed at 1.3550, bring further fall towards 1.3300-10.