Sample Category Title

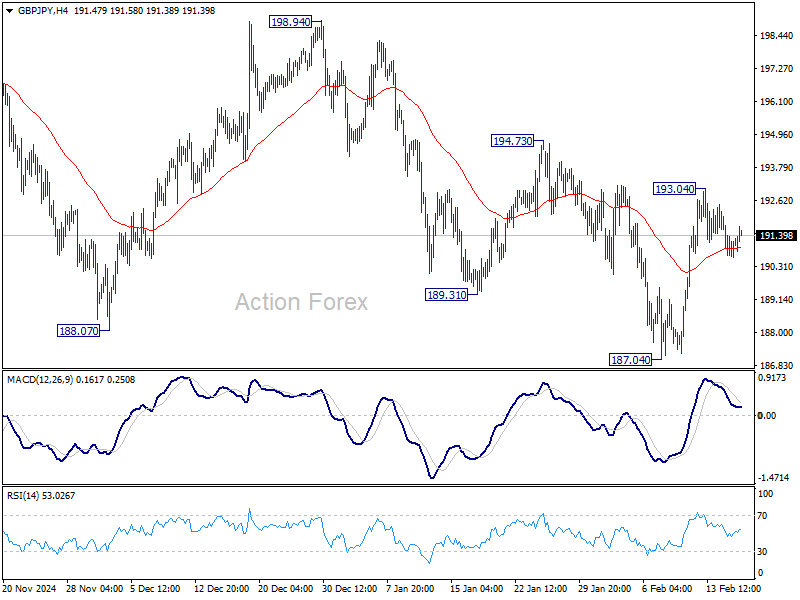

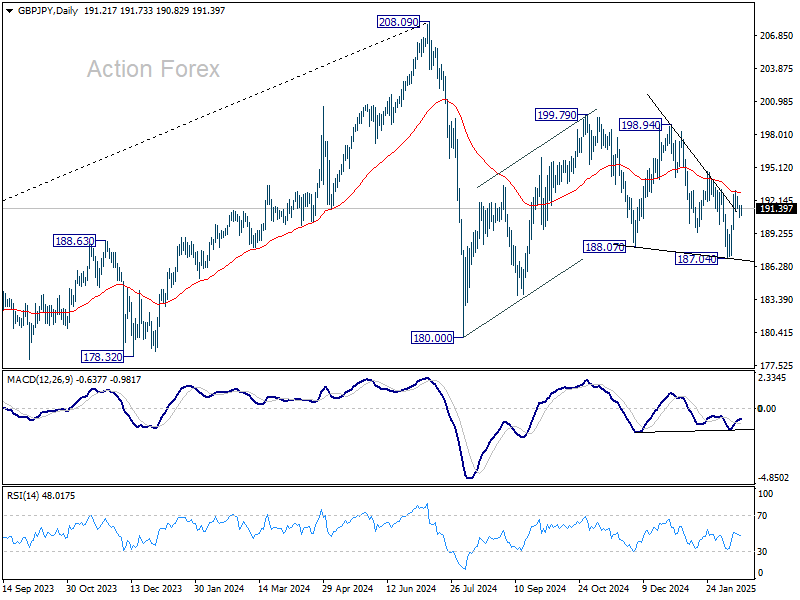

GBP/JPY Daily Outlook

Daily Pivots: (S1) 190.69; (P) 191.23; (R1) 191.83; More...

Intraday bias in GBP/JPY remains neutral at this point. Outlook is unchanged that corrective pattern from 180.00 is extending, possibly with rebound from 187.04 as another upleg. Above 193.04 will target 194.73 resistance first. Firm break there will solidify this case and target 198.94 next.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 208.09 to 180.00 from 199.79 at 171.70, even still as a correction.

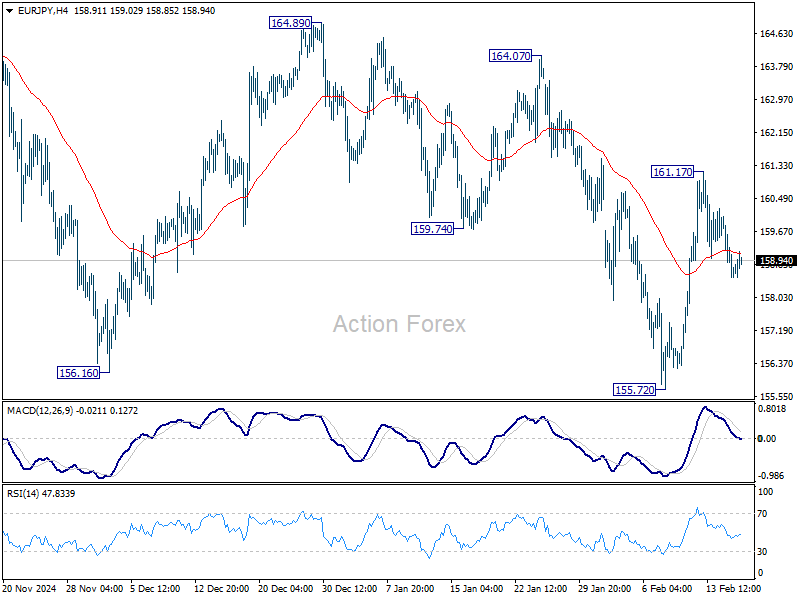

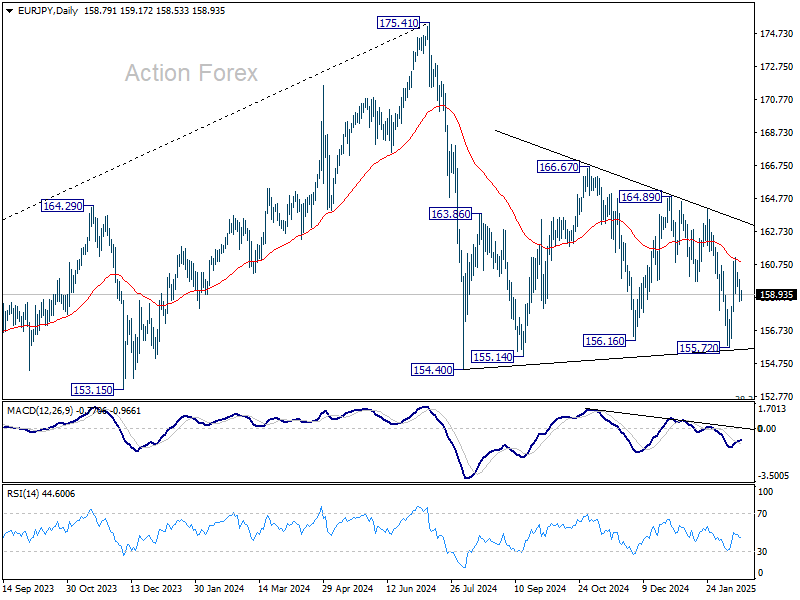

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.31; (P) 159.07; (R1) 159.61; More...

Intraday bias in EUR/JPY stays neutral at this point. Outlook is unchanged that sideway pattern from 154.40 is still extending with another upleg. On the upside, above 161.17 will target 164.07 resistance and then 164.89.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

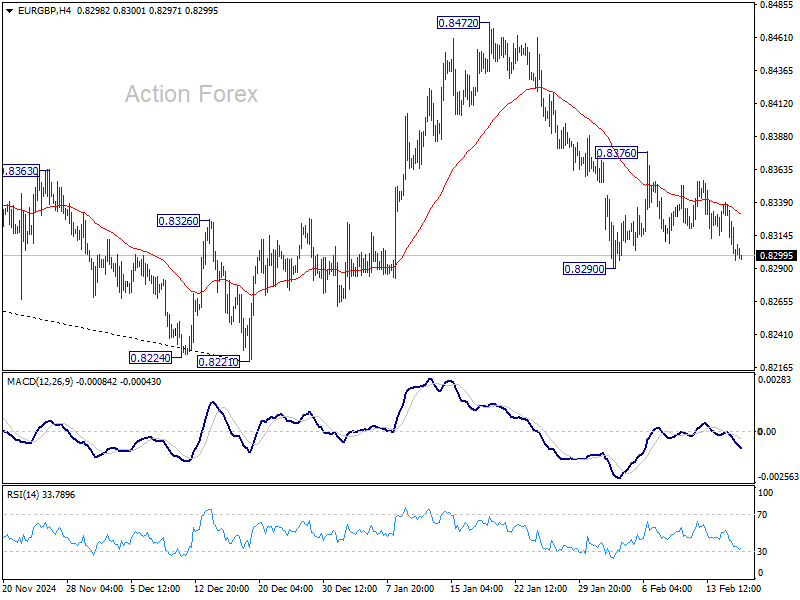

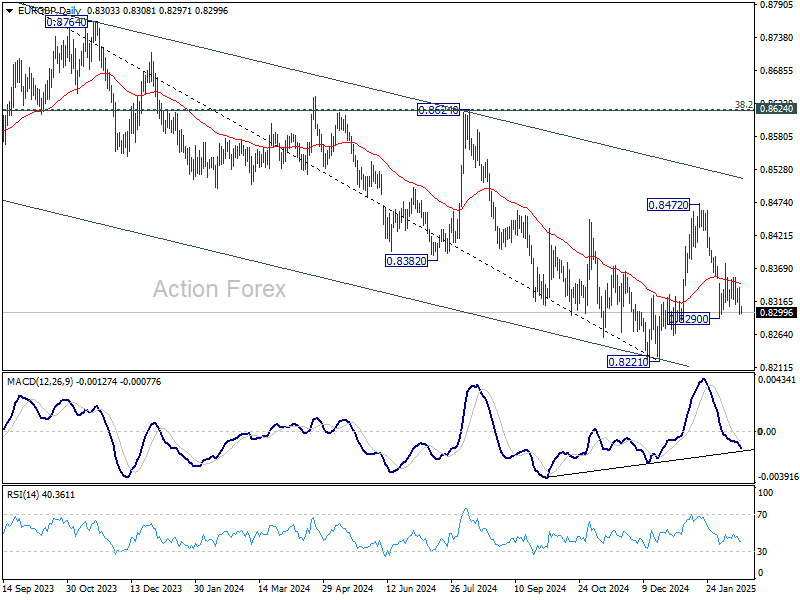

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8288; (P) 0.8313; (R1) 0.8330; More...

Intraday bias in EUR/GBP stays neutral for the moment. Near term outlook is mixed. On the downside, break of 0.8290 will resume the fall from 08472 to retest 0.8221 low. On the upside, above 0.8376 minor resistance will bring stronger rally towards 0.8472.

In the bigger picture, rebound from 0.8221 medium term bottom could extend higher through 55 W EMA (now at 0.8435). However, medium term outlook will be neutral at best as long as 0.8624 cluster resistance zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621) holds. Another decline through 0.8221 would remain mildly in favor.

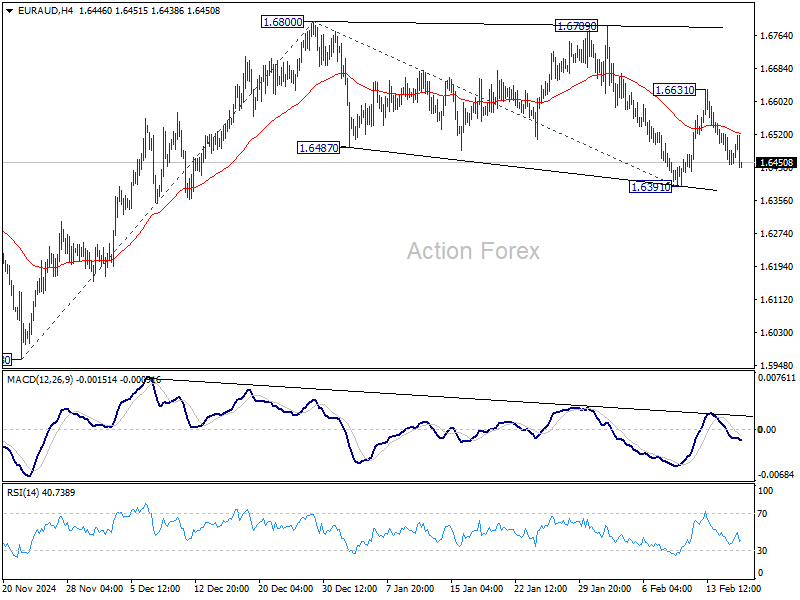

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6445; (P) 1.6493; (R1) 1.6538; More...

Intraday bias in EUR/AUD stays neutral at this point. The favored case remains that consolidation pattern from 1.6800 has completed at 1.6391 already. On the upside above 1.6631 will bring retest of 1.6800 first. Firm break there will resume the rally from 1.5963 to 61.8% projection of 1.5693 to 1.6800 from 1.6391 at 1.6908. However, firm break of 1.6391 will invalidate this view and bring deeper fall.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

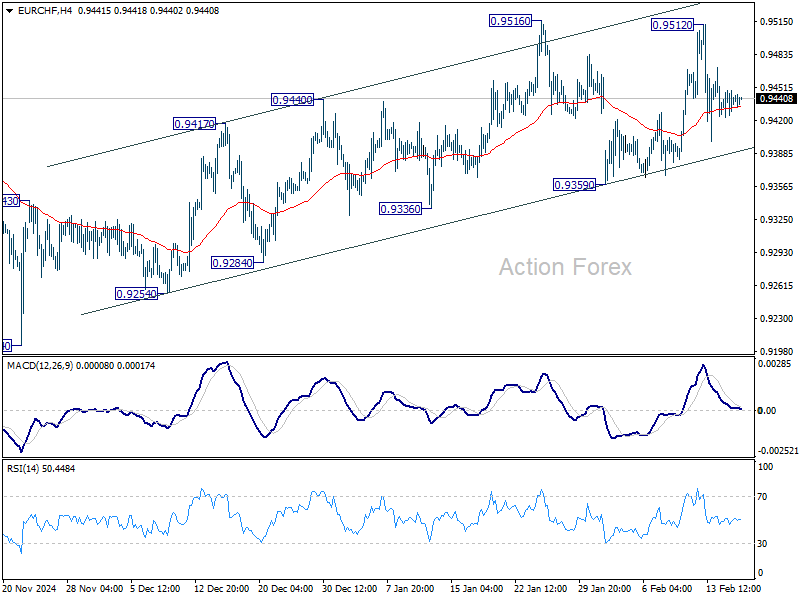

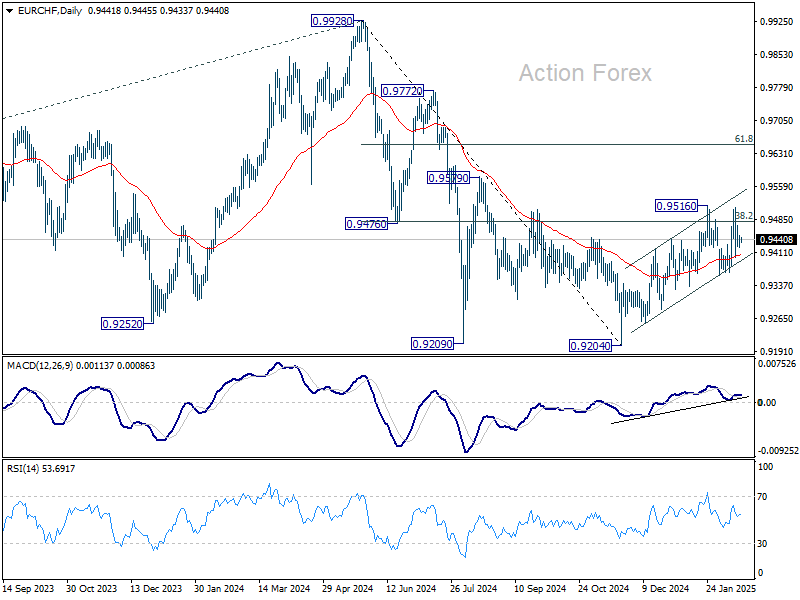

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9421; (P) 0.9436; (R1) 0.9458; More....

Range trading continues in EUR/CHF and intraday bias remains neutral. On the downside, break of 0.9359 support will revive the case that choppy rise from 0.9204 is merely a correction and has completed. Deeper fall should then be seen back to retest 0.9204 low. However, firm break of 0.9516 and sustained trading above 0.9481 fibonacci level will carry larger bullish implication and extend the rise from 0.9204.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204.

And So It Begins… RBA Cuts Cash Rate 25bp to 4.1%

As expected, RBA cuts cash rate 25bp to 4.1%. But a hawkish tone in the forecasts and rhetoric cements our view that RBA will move slowly from here.

As was widely expected, the RBA cut the cash rate today, by 25bp, to 4.1%. Inflation has declined faster than the RBA’s previous forecasts implied, with underlying inflation running at an annual rate consistent with the 2–3% target over the second half of 2024. Getting inflation sustainably back down to target was the Board’s highest priority. Given these data and the likely near-term outcomes they imply, it would be difficult to say that the goal is off-track. In fact, the RBA’s revised forecasts now have trimmed mean inflation constant (dare we say ‘sustained’) at 2.7% out to mid 2027. The post-meeting statement also acknowledges that inflation could be declining a bit faster than earlier expected.

Following today’s cut, the RBA assesses policy to still be restrictive. It recognised the progress made on getting inflation to target. It also acknowledged that upside risks to inflation had eased and that ‘there are signs that disinflation might be occurring a little more quickly than earlier expected.’

In a hawkish move, though, the press statement highlighted that there was a risk of easing ‘too much too soon’, in which case disinflation would ‘stall’ and inflation would ‘settle above the midpoint of the target range’ – exactly what their forecasts show trimmed mean inflation doing. The Board attributed this to ‘lingering tightness’ in the labour market. The prior easing in the labour market had ‘stalled’ over the second half of last year.

The hawkish tone is also an outworking of the 2023 RBA Review. Recall that the RBA Review recommended, and the latest Statement on the Conduct of Monetary Policy adopted – a framing of the inflation target that requires the RBA to set policy ‘such that inflation is expected to return to the midpoint of the target’, even though ‘all outcomes within the target range are consistent with the Reserve Bank Board’s price stability target’. The Board will therefore be more discomfited by the revised forecasts for trimmed mean inflation than they would have been prior to the Review. It also explains why in the post-meeting press conference, the Governor emphasised that people still needed to be patient to get inflation down – down by a whole 0.2ppts.

These forecasts are predicated on the cash rate following a path traced out by market expectations at the time of the forecast review for three rate cuts by year-end. In the post-meeting press conference, the Governor made it quite clear that the Board thinks that this is ‘far too confident’. We can therefore rule out back-to-back cuts and continue with our existing view that they will hold rates steady at the next meeting in April. But, just as inflation surprised the RBA on the downside recently, it could do so again.

A key driver of the hawkish tone is the RBA’s view of the labour market. The unemployment forecasts were revised down to level out at 4.2%. While the Governor declined to provide an estimate of the unemployment rate that is consistent with full employment, the structure in the forecasts suggests that the staff are still working on the assumption of a NAIRU around 4½%. The RBA’s framework (appropriately) goes beyond this single number and considers other variables such as underemployment and vacancies. The labour market has been tighter than expected, and yet inflation has fallen faster than the RBA expected. In the media conference, the Governor expressed hope that maybe Australia could sustain a lower unemployment rate with inflation at target. But the RBA is not willing to bet on such an outcome, even though a number of peer economies had a similar experience in the years leading up to the pandemic, with NAIRU estimates being revised down repeatedly.

Some other elements of the forecasts also appear quite hawkish. Forecasts for public demand growth were revised up, driven by recent state and federal budget updates. Consumption growth was revised down, but only a little and to a profile that looks to be still well above consensus. Overall growth was characterised as ‘returning to its trend rate’. But even allowing for the slower expected population growth, actual GDP forecasts look a little softer than past assumptions of potential output. The fragility of the labour market outlook to an early turn down in the current strong growth in employment in the healthcare and social assistance industry – the subject of an SMP Box – was barely acknowledged.

By explicitly characterising the stance of policy following the cut as restrictive, the Board is implicitly suggesting that, as long as inflation keeps declining, further rate cuts are on the cards. But they are not promising anything and expect it will be a long road still before they can declare victory on that last few tenths of a percentage point of inflation. The final paragraph of the post-meeting statement was unchanged.

Overall, this was a hawkish set of communications. While the inflation and labour cost data have turned out a bit better lately (and we will know more about the latter tomorrow), there was not a further evolution in the RBA’s thinking around the supply side. A moderate, almost grudging, path of easing is likely from here.

Elliott Wave View: EURUSD Looking to Extend Higher in 5 Waves

Short term Elliott Wave in EURUSD suggests rally from 1.13.2025 low is unfolding as a zigzag structure. Up from 1.13.2025 low, wave A ended at 1.0533 and pullback in wave B ended at 1.021. Wave C higher is in progress with internal subdivision as a 5 waves. Up from wave B, wave (i) ended at 1.035 and pullback in wave (ii) ended at 1.0269. Wave (iii) higher ended at 1.043 and pullback in wave (iv) ended at 1.0399. Wave (v) higher ended at 1.0442 which completed wave ((i)) in higher degree.

Pullback in wave ((ii)) unfolded as a zigzag structure. Down from wave ((i)), wave (a) ended at 1.035 and wave (b) rally ended at 1.041. Wave (c) lower ended at 1.0278 which completed wave ((ii)) in higher degree. Pair has resumed higher in wave ((iii)). Up from wave ((ii)), wave (i) ended at 1.0385 and pullback in wave (ii) ended at 1.031. Wave (iii) higher ended at 1.0514. Expect dips in wave (iv) to correct cycle from 2.12.2025 low before it resumes higher. Near term, as far as pivot at 1.0204 low stays intact, expect dips to find support in 3, 7, 11 swing for further upside.

EURUSD 60 Minutes Elliott Wave Chart

EURUSD Video

https://www.youtube.com/watch?v=5TPvTnPRF-4

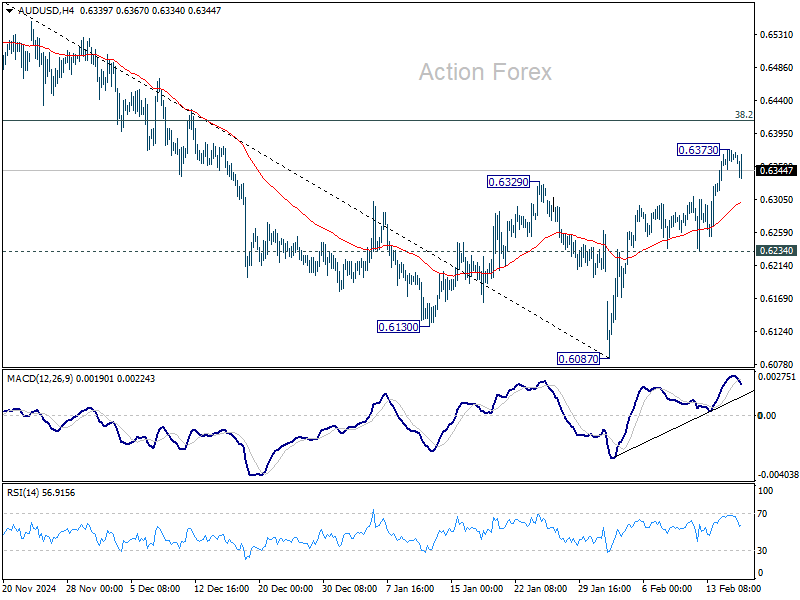

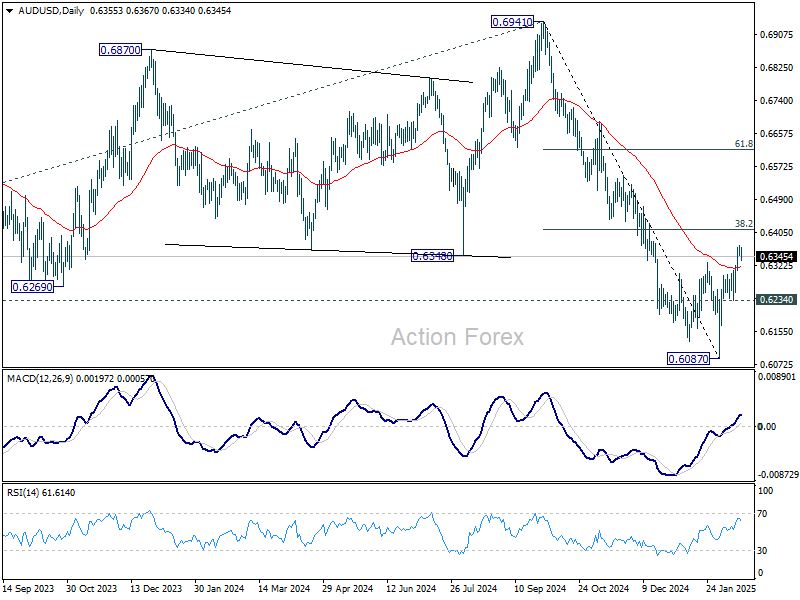

AUD/USD Daily Report

Daily Pivots: (S1) 0.6345; (P) 0.6359; (R1) 0.6372; More...

Intraday bias in AUD/USD is turned neutral as rebound from 0.6087 lost moment, as seen in 4H MACD, after hitting 0.6373. On the downside, break of 0.6234 support will suggest that the rebound has completed as a correction, and turn bias back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 38.2% retracement of 0.6941 to 0.6087 at 0.6413, will pave the way back to 61.8% retracement at 0.6615.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6504) holds.

RBA’s Cautious Easing Leaves AUD Supported, USD/JPY Ready for a Bounce?

Australian Dollar initially dipped after RBA's widely expected rate cut, but the move was short-lived as the currency quickly stabilized. RBA’s cautious tone on further easing provided underlying support for the Aussie. The central bank made it clear that while policy easing has begun, it is not committing to a rapid or continuous rate-cut cycle.

The updated economic projections justify RBA's cautious stance. Trimmed mean CPI is expected to stay at 2.7% throughout the forecast horizon, remaining above the midpoint of the RBA’s 2-3% inflation target. Meanwhile, the unemployment rate forecast was lowered to 4.2% and is expected to hold steady, indicating a persistently tighter-than-expected labor market.

RBA’s own cash rate assumptions suggest a drop to 3.60% by the end of 2025, implying just two more cuts before a prolonged pause. This guidance is against expectations for an aggressive easing cycle and could help limit AUD downside in the near term.

In the broader currency market, Dollar leads as the strongest performer of the day so far, recovering some of last week’s losses. Loonie follows as second, while Aussie holds third place. In contrast, Kiwi is the weakest, followed by Yen and Euro. Swiss Franc and Sterling are hovering in the middle of the pack.

Market focus now shifts to key upcoming economic data releases, including UK GDP, German ZEW economic sentiment, and Canadian CPI.

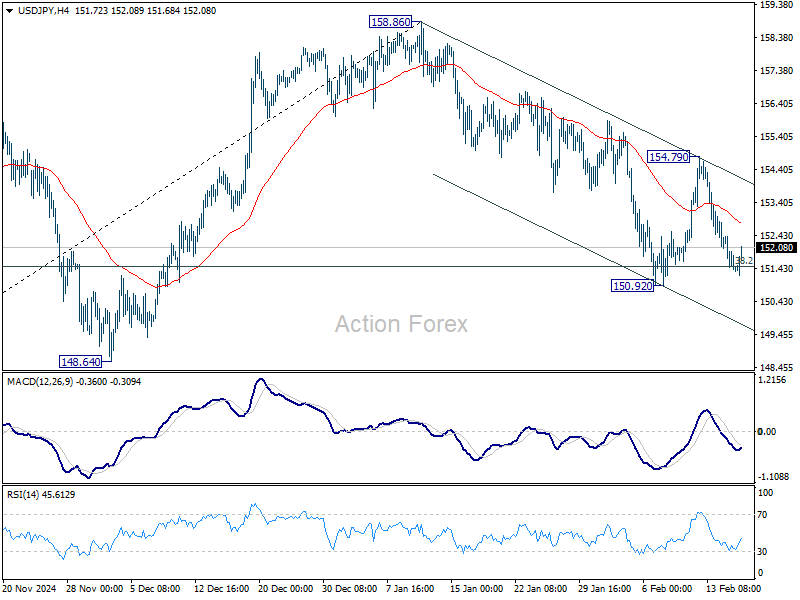

Technically, a main focus for today is whether USD/JPY could stage an extended rebound after drawing support from 38.2% retracement of 139.57 to 158.86 at 151.4 for the second time. Firm break of 55 4H EMA (now at 152.08) will be the first signal of bottoming. Firm break of 154.79 resistance will revive near term bullishness for resuming the rally from 139.57 at a later stage.

In Asia, at the time of writing, Nikkei is up 0.68%. Hong Kong HSI is up 1.94%. China Shanghai SSE is up 0.29%. Singapore Strait Times is up 0.25%. Japan 10-year JGB yield is up 0.0158 at 1.408.

RBA cuts rates, but warns against easing too much too soon

RBA lowered its cash rate target by 25bps to 4.10%, as widely anticipated, but signaled a cautious approach to further easing.

In its statement, the central bank emphasized that monetary policy will remain restrictive even after today’s reduction, warning that if rates are “eased too much too soon”, disinflation progress could stall and inflation could settle above the midpoint of the target range.

RBA acknowledged that some upside risks to inflation “appear to have eased”, and disinflation may be unfolding “a little more quickly than earlier expected”. However, it maintained that “risks on both sides” remain.

While today’s cut reflects the central bank’s confidence in recent progress, policymakers remain “cautious about the outlook”, reinforcing the idea that future easing will be data-dependent rather than pre-committed.

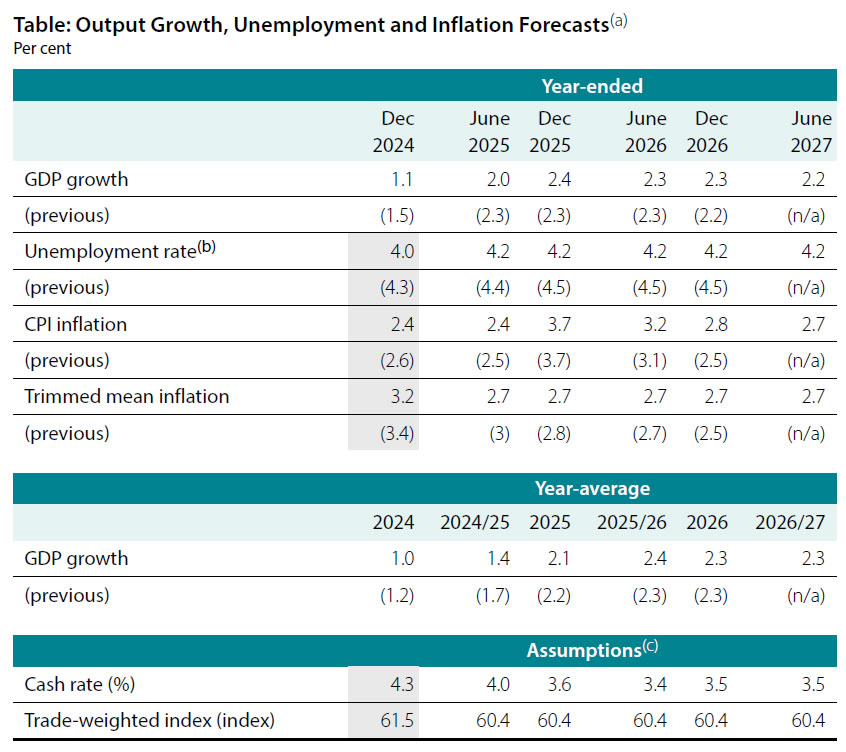

In the new economic projections:

- Headline CPI is now projected to rise to 3.7% by the end of 2025, before gradually easing to 2.8% by the end of 2026 (raised from 2.5%), and settling at 2.7% by mid-2027.

- Trimmed mean CPI is expected to remain at 2.7% throughout 2025, 2026, and mid-2027.

- Unemployment rate forecast was lowered to 4.2% across the projection horizon

- Year-average GDP growth was revised down by 0.1% to 2.1% for 2025, while 2026 remains unchanged at 2.3%, with growth expected to hold steady at 2.3% into 2026/2027.

- Cash rate assumptions suggest an average rate of 3.6% in 2025, followed by 3.5% in 2026.

Fed's Waller downplays tariff impact, warns against policy paralysis

Fed Governor Christopher Waller downplayed concerns that tariffs would have a significant, lasting impact on inflation, stating that their effect is likely to be “modest” and “non-persistent.” As a result, he favors “looking through” these effects when setting policy.

In a speech overnight, he emphasized that while economic uncertainty remains, Fed cannot afford to fall into a “recipe for policy paralysis” by waiting for absolute clarity regarding the administration's policies.

However, he conceded that tariffs could have a larger impact than expected, depending on their size and implementation. At the same time, he pointed out that other policies under discussion could have positive supply-side effects, helping to ease inflationary pressures.

Waller defended Fed’s decision to hold rates steady in January, arguing that the current economic data “are not supporting a reduction in the policy rate at this time.”

He left the door open for future rate cuts, stating that “if 2025 plays out like 2024, rate cuts would be appropriate at some point this year.”

Looking ahead

UK employment data is the main focus in European session, along with German ZEW economic sentiment. Later in the data, attention will be on Canada CPI. US will release Empire state manufacturing index and NAHB housing index.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6345; (P) 0.6359; (R1) 0.6372; More...

Intraday bias in AUD/USD is turned neutral as rebound from 0.6087 lost moment, as seen in 4H MACD, after hitting 0.6373. On the downside, break of 0.6234 support will suggest that the rebound has completed as a correction, and turn bias back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 38.2% retracement of 0.6941 to 0.6087 at 0.6413, will pave the way back to 61.8% retracement at 0.6615.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6504) holds.

RBA cuts rates, but warns against easing too much too soon

RBA lowered its cash rate target by 25bps to 4.10%, as widely anticipated, but signaled a cautious approach to further easing.

In its statement, the central bank emphasized that monetary policy will remain restrictive even after today’s reduction, warning that if rates are “eased too much too soon”, disinflation progress could stall and inflation could settle above the midpoint of the target range.

RBA acknowledged that some upside risks to inflation “appear to have eased”, and disinflation may be unfolding “a little more quickly than earlier expected”. However, it maintained that “risks on both sides” remain.

While today’s cut reflects the central bank’s confidence in recent progress, policymakers remain “cautious about the outlook”, reinforcing the idea that future easing will be data-dependent rather than pre-committed.

In the new economic projections:

- Headline CPI is now projected to rise to 3.7% by the end of 2025, before gradually easing to 2.8% by the end of 2026 (raised from 2.5%), and settling at 2.7% by mid-2027.

- Trimmed mean CPI is expected to remain at 2.7% throughout 2025, 2026, and mid-2027.

- Unemployment rate forecast was lowered to 4.2% across the projection horizon

- Year-average GDP growth was revised down by 0.1% to 2.1% for 2025, while 2026 remains unchanged at 2.3%, with growth expected to hold steady at 2.3% into 2026/2027.

- Cash rate assumptions suggest an average rate of 3.6% in 2025, followed by 3.5% in 2026.