Sample Category Title

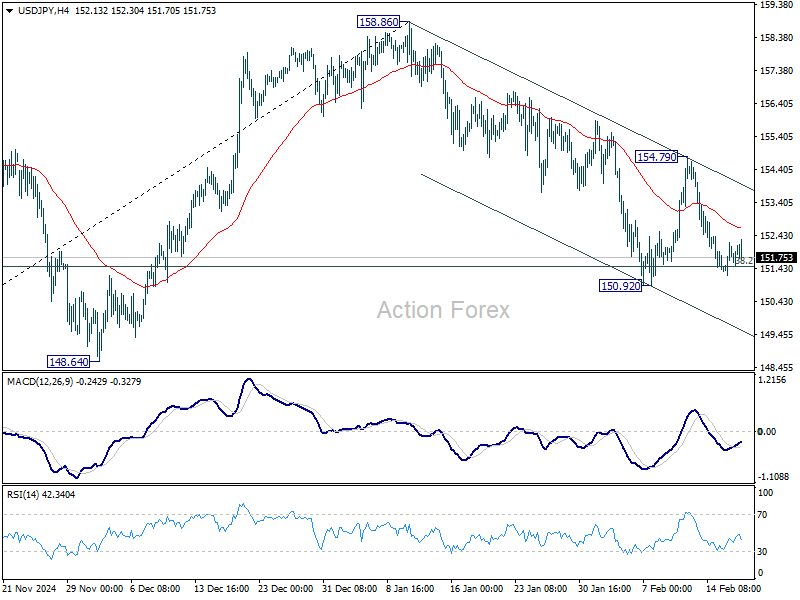

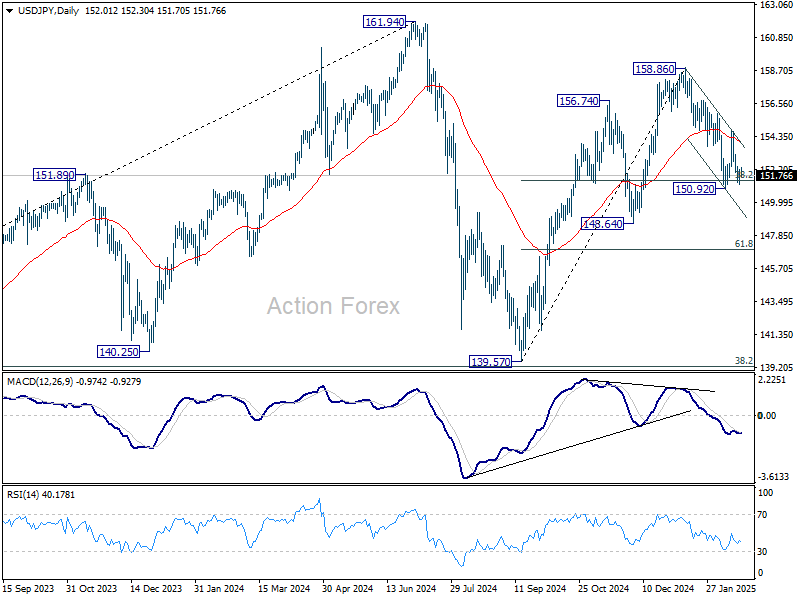

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.47; (P) 151.84; (R1) 152.45; More...

Intraday bias in USD/JPY stays neutral at this point. Attention remains on 38.2% retracement of 139.57 to 158.86 at 151.4. Strong rebound from there will maintain near term bullishness. On the upside, break of 154.79 will revive the case that correction from 158.86 has completed at 150.29. Further rise should be seen to retest 158.86 high. However, break of 150.92 and sustained trading below 151.49 will raise the chance of trend reversal, and target 148.64 support instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

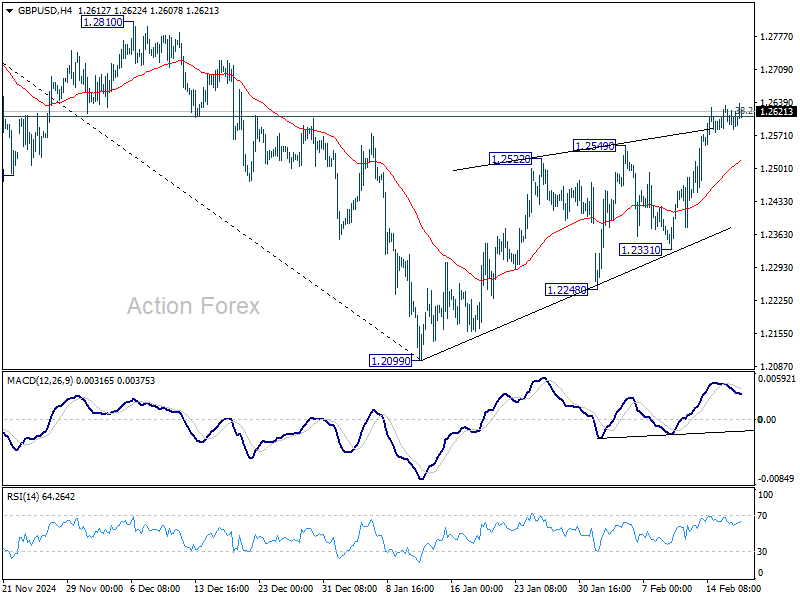

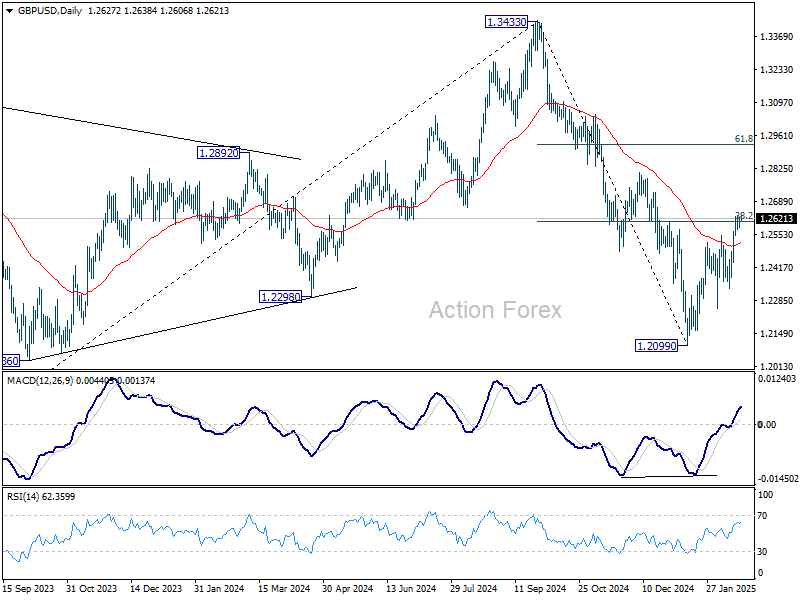

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2587; (P) 1.2609; (R1) 1.2637; More...

Intraday bias in GBP/USD remains neutral with focus on 38.2% retracement of 1.3433 to 1.2099 at 1.2609. Rejection by this level will keep near term outlook bearish. Break of 1.2331 support will suggest that the rebound from 1.2099 has completed as a correction, and bring retest of 1.2099 low. However, firm break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

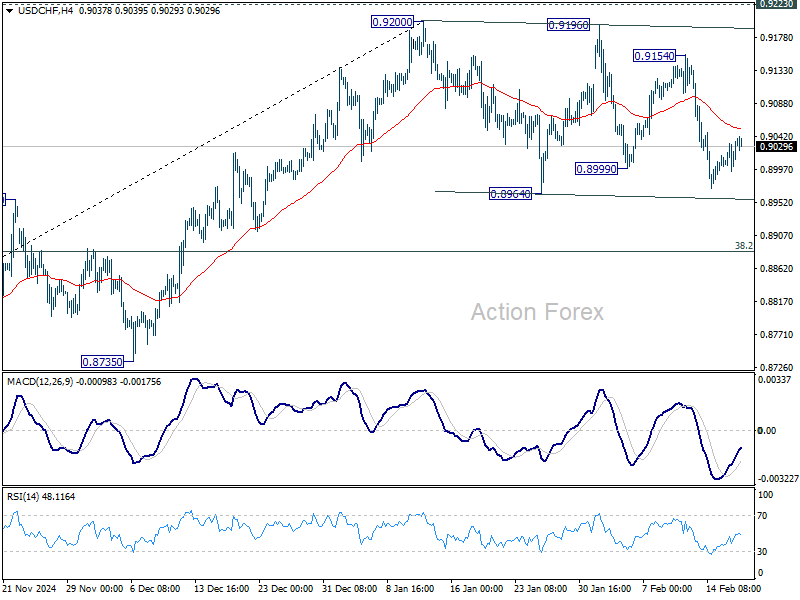

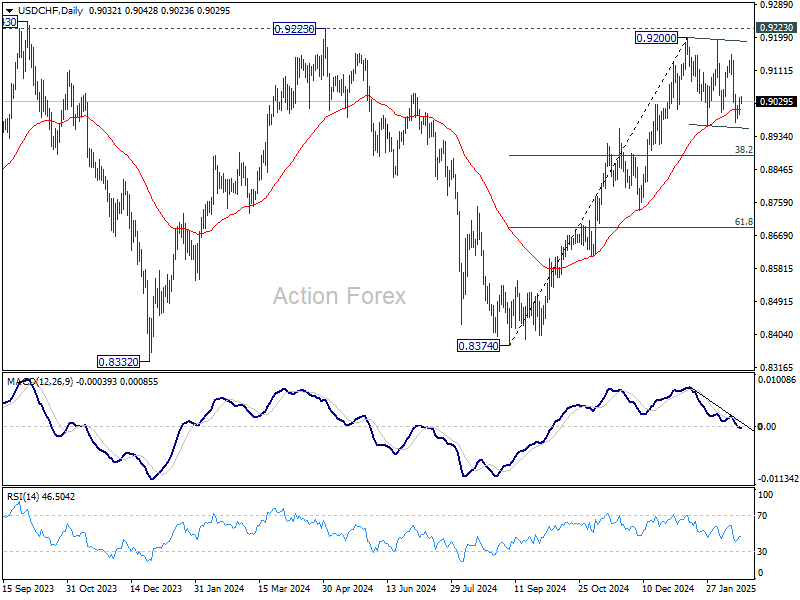

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9006; (P) 0.9024; (R1) 0.9051; More…

USD/CHF is staying in consolidation from 0.9200 and intraday bias remains neutral. While deeper pull back might be seen, outlook will stay mildly bullish as long as 38.2% retracement of 0.8374 to 0.9200 at 0.8884 holds. On the upside, firm break of 0.9223 key resistance will carry larger bullish implication. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

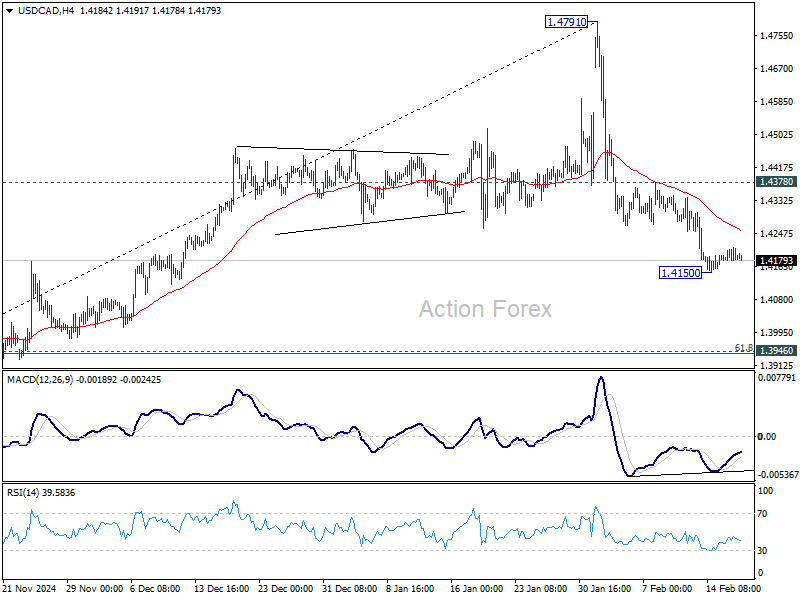

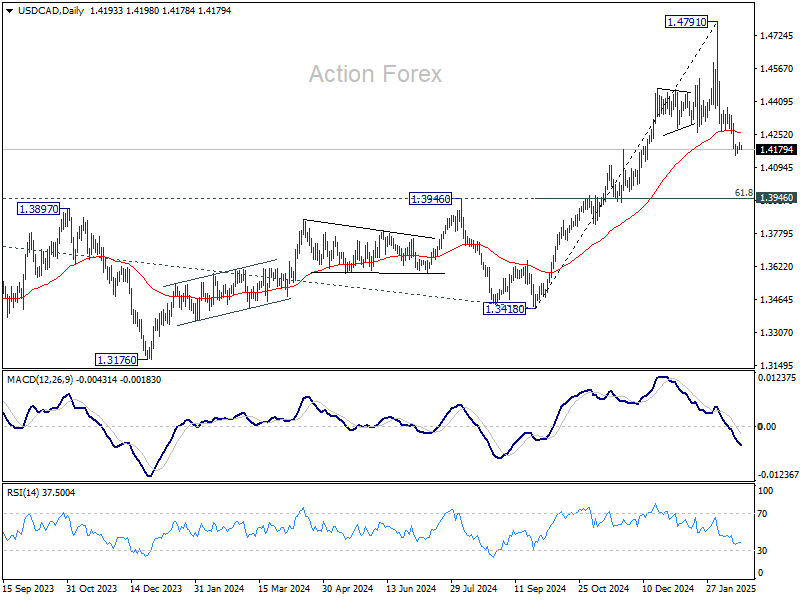

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4177; (P) 1.4195; (R1) 1.4212; More...

Intraday bias in USD/CAD remains neutral as consolidations continue above 1.4150 temporary low. Deeper decline is expected as long as 1.4378 resistance holds. Fall from 1.4791 is correcting whole rise from 1.3418. Break of 1.4150 will target 1.3946 cluster support (61.8% retracement of 1.3418 to 1.4791 at 1.3942).

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

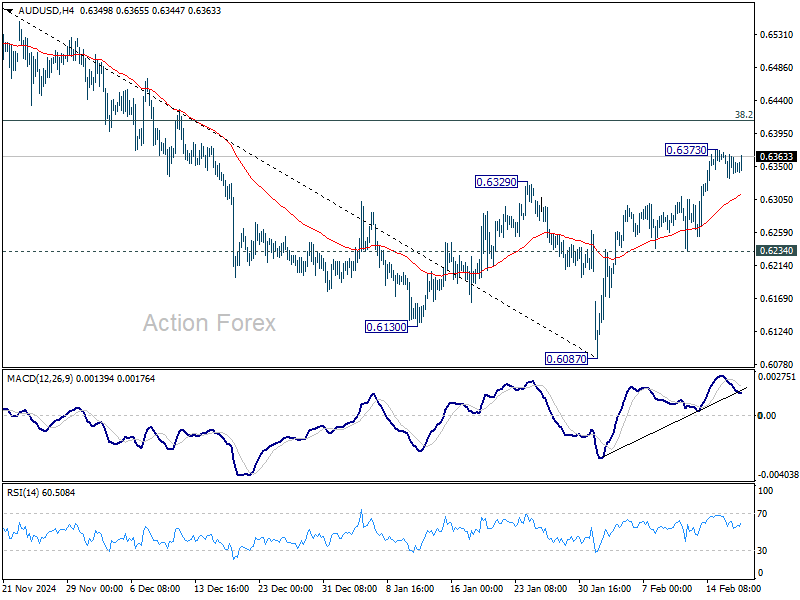

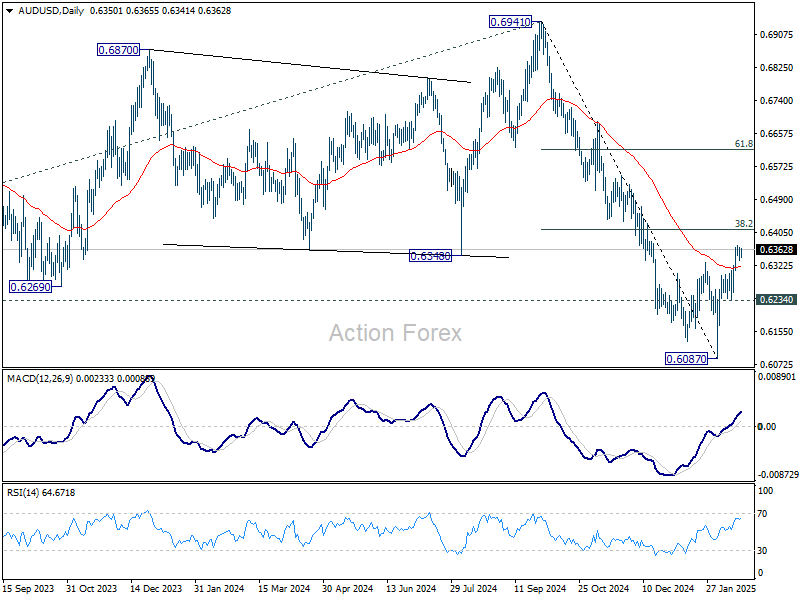

AUD/USD Daily Report

Daily Pivots: (S1) 0.6335; (P) 0.6352; (R1) 0.6368; More...

Intraday bias in AUD/USD stays neutral for consolidations below 0.6373 temporary top. Rebound from 0.6087 is seen as a correction to the fall from 0.6941. In case of another rise, upside should be limited by 38.2% retracement of 0.6941 to 0.6087 at 0.6413. On the downside, break of 0.6234 support will suggest that the rebound has completed as a correction, and turn bias back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 0.6413, will pave the way back to 61.8% retracement at 0.6615.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6504) holds.

Kiwi Wobbles After RBNZ Cut, Markets Eye UK CPI and FOMC Minutes

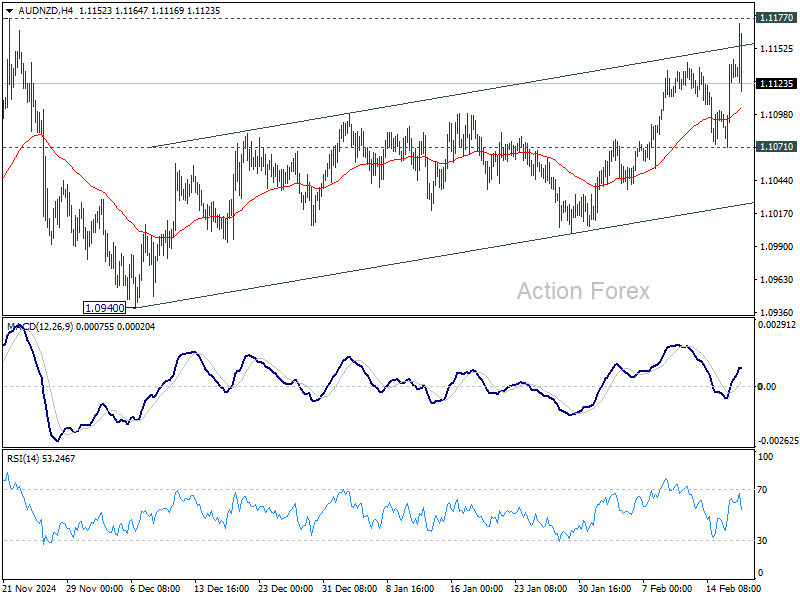

New Zealand Dollar initially weakened following RBNZ's 50bps rate cut today, but quickly regained ground as Governor Adrian Orr indicated that the pace of easing will slow in the coming months. Orr suggested that the central bank is likely to implement just more 25bps cuts, in April and May, provided that economic conditions unfold as expected. However, the Kiwi’s upside remains limited, as RBNZ revised its terminal rate forecast downward to 3.1% by year-end, slightly below November’s projection of 3.2%.

Technically, we'd maintain the view that AUD/NZD's choppy rise from 1.0940 is a corrective move. So upside should be limited by 1.1177 resistance to bring near term reversal. Break of 1.1071 support will argue that the pattern from 1.1177 has started the third leg, and should decline towards 1.0940 support next.

Outside of NZD-driven moves, the broader forex market remains subdued, with a lack of major catalysts. Dollar is the weakest performer of the day so far, as the momentum from this week’s recovery has faded. Traders are now looking ahead to FOMC minutes, though they are unlikely to provide new insights, instead reaffirming that Fed remains cautious and in no hurry to cut rates again.

British Pound is also under pressure, ranking as the second weakest currency, as investors await the release of UK CPI data. A hot inflation print could diminish expectations for a consecutive BoE rate cut in March, potentially offering some relief to the currency. Swiss franc rounds out the three weakest performers, showing broad softness.

On the stronger side, New Zealand Dollar leads the market. Yen follows, benefiting from continued speculation over future BoJ policy hikes, while the Australian Dollar also holds firm. Euro and Canadian Dollar are positioning in the middle.

In Asia, at the time of writing, Nikkei is down -0.38%. Hong Kong HSI is down -0.28%. China Shanghai SSE is up 0.54%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is up 0.002 at 1.439. Overnight, DOW rose 0.02%. S&P 500 rose 0.24%. NASDAQ rose 0.07%. 10-year yield rose 0.072 to 4.544.

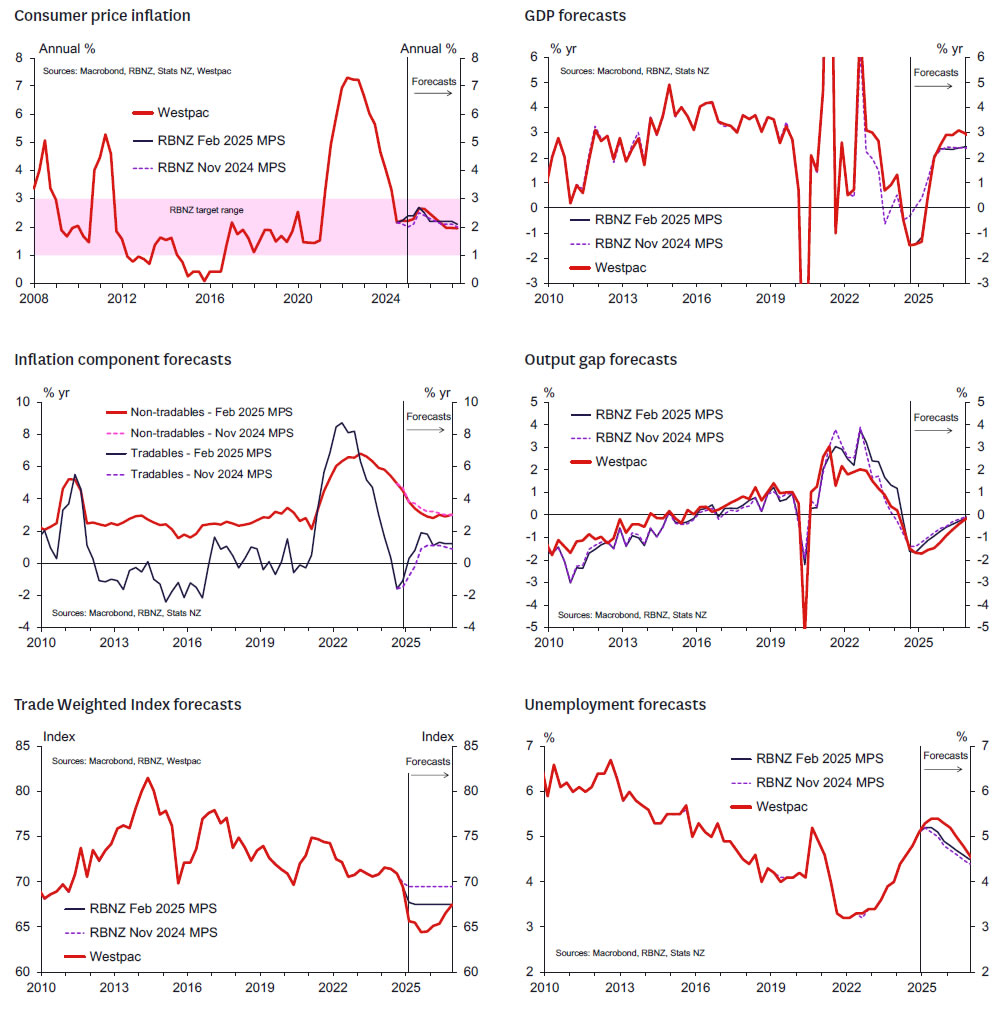

RBNZ cuts by 50bps, signals further easing through 2025

RBNZ cut the Official Cash Rate (OCR) by 50bps to 3.75%, as widely expected, while maintaining a clear easing bias.

The central bank stated that "if economic conditions continue to evolve as projected, the Committee has scope to lower the OCR further through 2025." According to the latest projections, the OCR is expected to decline to 3.1% by year-end and remain at that level until early 2028.

RBNZ acknowledged that economic activity remains subdued, though it expects growth to recover in 2025, driven by lower interest rates encouraging spending. However, elevated global economic uncertainty is likely to weigh on business investment. The bank also noted that inflation is expected to be volatile in the near term, influenced by a weaker exchange rate and higher petrol prices.

Regarding global risks, the RBNZ flagged concerns and warned that higher global tariffs could slow growth in key trading partners, dampening demand for New Zealand exports and weakening domestic economic momentum over the medium term.

However, the impact on inflation is "ambiguous", depending on factors such as trade diversion, supply-chain adjustments, and financial market reactions.

Australian wages growth slow 0.7% qoq, pressures easing

Australia’s wage price index rose 0.7% qoq in Q4, marking a slowdown from 0.9% qoq and missing expectations of 0.8% qoq. This matches the lowest quarterly growth since March 2022, reinforcing signs that wage pressures are easing, albeit still elevated.

On an annual basis, wages increased 3.2% yoy, making it the slowest pace since Q3 2022. Private sector wage growth came in at 3.3% yoy, the weakest since Q2 2022. Public sector wages rose 2.8% yoy, falling below 3% for the first time since Q2 2023.

BoJ’s Takata: Gradual policy shifts should continue beyond January hike

BoJ Board Member Hajime Takata emphasized the need for the central bank to continue to "implement gear shifts gradually, even after the additional rate hike decided in January 2025", to mitigate the risk of rising prices and financial market overheating.

Takata noted in a speech today that as "positive corporate behavior" persists, BoJ should consider a “further gear shift” in policy.

He highlighted three key risks that could drive prices above BoJ’s baseline scenario: a stronger wage-price cycle, inflationary pressures from domestic factors, and market volatility, especially in the exchange rates, stemming from a recovery in the US economy.

Nevertheless, due to uncertainties surrounding the US economy and the challenge of identifying the neutral interest rate, Takata advocated for a “vigilant approach”.

Japan’s trade deficit widens as imports surge, exports to China drop

Japan’s trade deficit expanded sharply in January, reaching JPY -2.759T, the largest shortfall in two years, as imports surged 16.7% yoy, far exceeding the expected 9.3% yoy gain.

Meanwhile, exports rose 7.2% yoy, falling slightly short of the 7.7% yoy forecast, with strong shipments to the U.S. (+18.1% yoy) offset by a -6.2% yoy decline in exports to China.

On a seasonally adjusted basis, exports declined -2.0% mom to JPY 9.253T, while imports climbed 4.7% mom to JPY 10.109T, leading to a JPY -857B trade deficit.

Looking ahead

UK CPI is the main focus in European session. EUrozone will release current account. Later in the day, main focus is on FOMC minutes while US will also publish building permits and housing starts.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6335; (P) 0.6352; (R1) 0.6368; More...

Intraday bias in AUD/USD stays neutral for consolidations below 0.6373 temporary top. Rebound from 0.6087 is seen as a correction to the fall from 0.6941. In case of another rise, upside should be limited by 38.2% retracement of 0.6941 to 0.6087 at 0.6413. On the downside, break of 0.6234 support will suggest that the rebound has completed as a correction, and turn bias back to the downside for retesting 0.6087 low. Nevertheless, sustained break of 0.6413, will pave the way back to 61.8% retracement at 0.6615.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6504) holds.

RBNZ Cuts the OCR to 3.75%

- As widely anticipated, the RBNZ cut the OCR by 50bps to 3.75%.

- The RBNZ signalled a high chance of 2-3 further cuts in 2025, including 25bp cuts at the April and May meetings.

- The RBNZ’s tone remains dovish albeit without any obvious intent to do another 50bp cut in the near term.

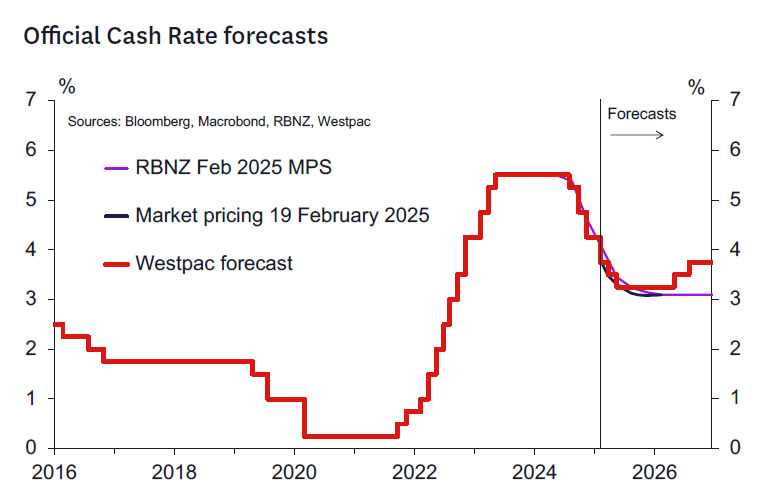

- Our OCR forecast remains unchanged. We see two further 25bp cuts in April and May and the end of the cycle at 3.25%.

Key takeout: RBNZ cuts OCR 50bps to 3.75%, signals further easing in April and May.

The RBNZ cut the OCR by 50bps to 3.75% as widely expected. This decision had been foreshadowed by the RBNZ at its late November meeting and was reached by consensus. It seems that there has been little on balance to shift the RBNZ’s thinking since the November meeting.

The RBNZ projects the OCR to end 2025 at 3.1%. This end- 2025 level was revised down from 3.55%, with the key adjustments taking place in the near-term profile which now looks consistent with Westpac’s forecasts of two further 25bp cuts in the April and May meetings.

The discussion surrounding the projections remains dovish. The MPC remains confident that inflation will remain well-contained – even though the headline CPI will temporarily rise to 2.7% in the September quarter of this year. These forecasts are exactly in line with Westpac’s forecasts.

The RBNZ has not significantly adjusted its short-term growth forecasts and sees recent indicators as broadly consistent with the expected return to growth from the December 2024 quarter. The RBNZ has, like us, not taken much from the large falls in GDP in mid-2024. There is a modest upgrade in their assessment of excess capacity in the economy – but it's very much at the margin. The forecast downturn in the unemployment rate occurs a quarter later than projected in November.

Risks.

The RBNZ points primarily at global developments which are seen as presenting downside risks to global growth and NZ exporters’ incomes. Tighter financial conditions from higher global interest rates are noted as something that could undermine global growth.

Tariffs and trade disputes similarly are seen as presenting downside risks to growth. The RBNZ hasn’t drawn any firm conclusions on how these global trade risks will pan out. The RBNZ echoes the RBA’s message from yesterday that the uncertainty might impact on business investment.

The RBNZ notes that while growth outcomes might be undermined, the impact on inflation is indeterminate – and it will be the impact of medium-term inflation pressures that will drive any policy response. Notably, the RBNZ acknowledges that the exchange rate will likely bear the brunt of foreign trade shocks. However, the commentary on the exchange rate impacts on the outlook is not prominent.

The RBNZ has made a significant downgrade to its house price forecasts (from 7.1% growth for 2025 to 3.8% in the new forecasts). While the recent strengthening-butstill- modest momentum may justify the direction of this adjustment, some forward indicators look positive. Mortgage approvals are now running at their highest levels since 2021 when house prices were rising very strongly. While we don’t think house prices will behave anything like they did in 2021, we see upside risks to the RBNZ’s assessment on this score. If realised, this could reduce the MPC’s ardour in cutting the OCR by mid-year.

Westpac’s OCR call.

We see the RBNZ cutting the OCR by 25bp increments at the April and May meetings, leaving the OCR at 3.25%. We think the RBNZ will pause at this point as by then there will be tangible signs of a return to trend growth, while inflation will still be in the top half of the 1-3% target range. This combination may test the MPC’s confidence in how anchored inflation is by then.

Key domestic data to watch ahead of the RBNZ’s 9 April Review.

The next RBNZ policy review will take place in seven weeks on 9 April. On the domestic front the most important data releases between now and then are as follows.

- The Q4 GDP report (20 March): The outcome of this report will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap and perhaps also its view on near-term growth momentum.

- The February Selected Price Indexes (14 March): This will provide the last indication of the likely outcome of the Q1 CPI report, which will be released on 17 April.

- The Q1 QSBO survey (8 April): This key report will be released publicly just the day prior to the policy announcement (although the RBNZ will likely see this earlier). The focus will be on indicators of Q1 activity and cost/inflation pressures. It will also be interesting to see to what extent confidence, hiring and investment indicators are continuing to lift.

In addition to the above, key monthly activity indicators such as the BusinessNZ manufacturing and services indexes and the ANZ Business Outlook survey will also be of interest, as will developments in retail spending and housing indicators (the latter could be especially instructive as we move into what is typically the busiest time of the year for housing market activity).

Outside of New Zealand, interest will centre on any clarity that emerges regarding the implications of the Trump presidency for New Zealand’s export sector. On that score, we note that President Trump has signalled an intention to apply ‘reciprocal’ tariffs to countries that apply value-added taxes – which would presumably include New Zealand’s GST. Associated developments in financial conditions – longer-term interest rates and the exchange rate – will also factor into the next OCR review.

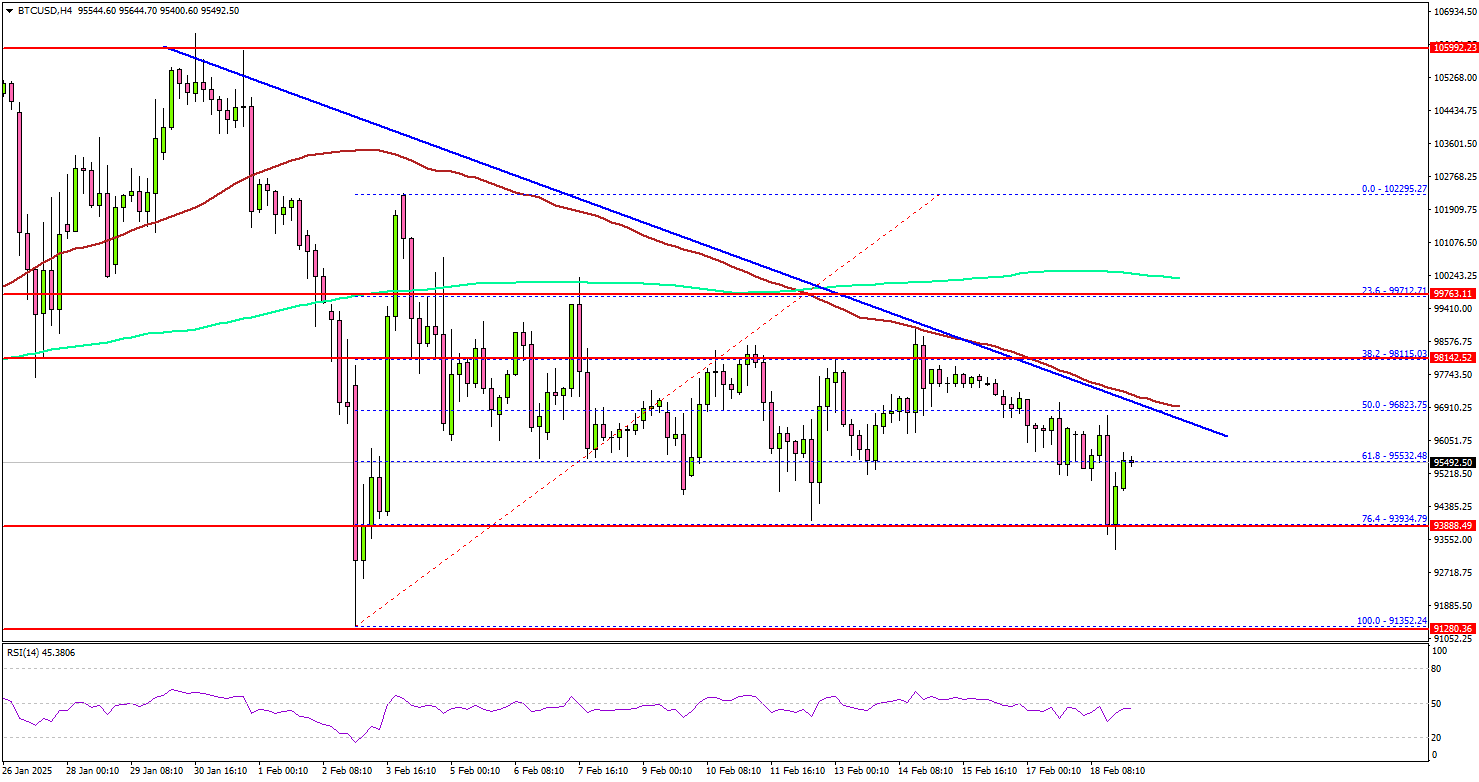

Bitcoin Fights To Break Free—Can It Rise Above Key Levels?

Key Highlights

- Bitcoin price is consolidating above the $94,000 support zone.

- BTC is facing hurdles near a key bearish trend line with resistance at $97,250 on the 4-hour chart.

- Ethereum price is struggling to gain pace for a move above $2,850 and $3,000.

- GBP/USD aims for a move above the 1.2630 and 1.2650 levels.

Bitcoin Price Technical Analysis

Bitcoin price made a couple of attempts to settle above $100,000 against the US Dollar. However, BTC bears remained active and prevented a steady increase.

Looking at the 4-hour chart, the price remained stable above the 76.4% Fib retracement level of the upward move from the $91,352 swing low to the $102,295 high, but it is also below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

On the upside, the price could face resistance near the $97,500 level and the 100 simple moving average (red, 4-hour). There is also a key bearish trend line forming with resistance at $97,250 on the same chart.

The next key resistance is $100,000 and the 200 simple moving average (green, 4-hour). A successful close above $100,000 might start another steady increase. In the stated case, the price may perhaps rise toward the $105,000 level.

Immediate support is near the $95,500 level. The next key support sits at $94,000. A downside break below $94,000 might send Bitcoin toward the $92,000 support. Any more losses might send the price toward the $91,200 support zone.

Looking at Ethereum, there was a recovery wave above $2,650 but the bears remained active near the $2,850 resistance zone.

Today’s Economic Releases

- US Housing Starts for Jan 2025 (MoM) – Forecast 1.40M, versus 1.499M previous.

- US Building Permits for Jan 2025 (MoM) – Forecast 1.460M, versus 1.482M previous.

BoJ’s Takata: Gradual policy shifts should continue beyond January hike

BoJ Board Member Hajime Takata emphasized the need for the central bank to continue to "implement gear shifts gradually, even after the additional rate hike decided in January 2025", to mitigate the risk of rising prices and financial market overheating.

Takata noted in a speech today that as "positive corporate behavior" persists, BoJ should consider a “further gear shift” in policy.

He highlighted three key risks that could drive prices above BoJ’s baseline scenario: a stronger wage-price cycle, inflationary pressures from domestic factors, and market volatility, especially in the exchange rates, stemming from a recovery in the US economy.

Nevertheless, due to uncertainties surrounding the US economy and the challenge of identifying the neutral interest rate, Takata advocated for a “vigilant approach”.

RBNZ cuts by 50bps, signals further easing through 2025

RBNZ cut the Official Cash Rate (OCR) by 50bps to 3.75%, as widely expected, while maintaining a clear easing bias.

The central bank stated that "if economic conditions continue to evolve as projected, the Committee has scope to lower the OCR further through 2025." According to the latest projections, the OCR is expected to decline to 3.1% by year-end and remain at that level until early 2028.

RBNZ acknowledged that economic activity remains subdued, though it expects growth to recover in 2025, driven by lower interest rates encouraging spending. However, elevated global economic uncertainty is likely to weigh on business investment. The bank also noted that inflation is expected to be volatile in the near term, influenced by a weaker exchange rate and higher petrol prices.

Regarding global risks, the RBNZ flagged concerns and warned that higher global tariffs could slow growth in key trading partners, dampening demand for New Zealand exports and weakening domestic economic momentum over the medium term.

However, the impact on inflation is "ambiguous", depending on factors such as trade diversion, supply-chain adjustments, and financial market reactions.