Sample Category Title

USD Market Isn’t Impressed by Renewed (Car, Pharma & Chip) Import Tariff Threat

Markets

The first high-level in-person talks between the US and Russia since the 2022 invasion in Riyadh went well according to the parties involved but offered nothing concrete. The talks were merely explanatory. The fact they happened without Ukraine and the EU sparked outcry from both and prompted a handful of EU leaders into a crisis meeting on Monday to discuss upgrading the European defense capacity. Polish PM Tusk said that (funding) measures would be presented in time for an upcoming March 20-21 summit. We wouldn’t be surprised if something came up sooner given the sense of urgency, provided German coalition building goes smoothly after this Sunday’s elections. French president Macron has called a second meeting for today, involving several EU and non-EU states. Negotiations center around having a UN-mandated “peace-keeping operation” in Ukraine to uphold any future ceasefire/peace deal. The war theme stays at the center of attention but markets are wary to frontrun on any outcome for the time being. Monday’s slide by European bonds in anticipation of significantly increased defense spending eased yesterday. German rates gapped higher at the open but pared gains afterwards to close virtually unchanged. UST’s caught up during their first trading day of the week by adding between 4.7-7.5 bps across the curve yesterday. The US dollar held the upper hand. EUR/USD fell to 1.0446, DXY bounced back to 107. Sterling appreciated on an across-the-board beat by the labour market report. EUR/GBP lost 0.83 and withstood overall USD strength (GBP/USD 1.261). Next up in the UK: CPI. Headline inflation only dropped 0.1% m/m, pushing up the yearly figure to a quicker-than-expected 3%. Core CPI jumped to 3.7% from 3.2% and services inflation to 5% from 4.4%. Bank of England governor Bailey flagged the inflation spike in a speech yesterday and warned not to read too much into it. It explains this morning’s muted GBP reaction. UK money market pricing barely changed and sticks to just two rate cuts for all of 2025.

Aside from the running war theme, Trump’s tariff policy comes back to front as well. The FX ex. USD market isn’t impressed by a renewed (car, pharma & chip) import tariff threat by Trump late-yesterday though. The president said an announcement could come April 2, offering time to hammer out a deal. The greenback trades on the backfoot against all G10 peers. The eco calendar further contains the January Fed meeting minutes. The slew of policymakers since that gathering that came to cement the long pause suggests a broad consensus and means the minutes probably have little surprising or new to offer. We assume technically inspired FX and FI trading.

News & Views

The Reserve Bank of New Zealand today reduced the policy rate further by 50 bps to 3.75%. The move was largely expected. CPI inflation remains near the midpoint of its 1-3% target band (0.5% Q/Q and 2.2% Y/Y in Q4). Firms’ inflation expectations are at target and core inflation continues to fall towards the target midpoint. The economic outlook remains consistent with inflation remaining in the band over the medium term. Economic activity remains subdued and spare productive capacity and domestic inflation pressures continue to ease. Price and wage setting is adapting to a low-inflation environment. The RBNZ expects economic activity and employment growth to recover this year, but there is a high degree of uncertainty, amongst others due to trade. The RBNZ governor indicated that the RBNZ might ease policy a bit faster than indicated earlier, with follow-up rate cuts (25 bps) in April and May. The Monetary policy report sees the policy rate on average near 3.1% in Q4. The NZ 3-y bond yield initially dropped after the decision but current trades little changed near 3.85%. The kiwi dollar made a similar move, reversing an earlier decline after governor Orr’s press conference, currently even trading slightly higher at NZD/USD 0.573.

BoJ Board member Takata in a speech today advocated that the bank should continue to consider gradual further rate hikes to contain upside inflation risks. With long-term inflation expectations rising and companies more actively passing on costs, conditions for further policy normalization are falling into place. Maintaining expectations for interest rates to stay low for a prolonged period of time might overheat the economy and financial activity. He indicated that it is difficult to estimate a neutral policy rate and finds it problematic for the Bank to announce a certain level of the neutral policy rate. It could be seen as pre-committing and would reduce the bank’s policy flexibility. At 1.435%, the 10-y Japanese government bond yield this morning touched the highest level since 2009.

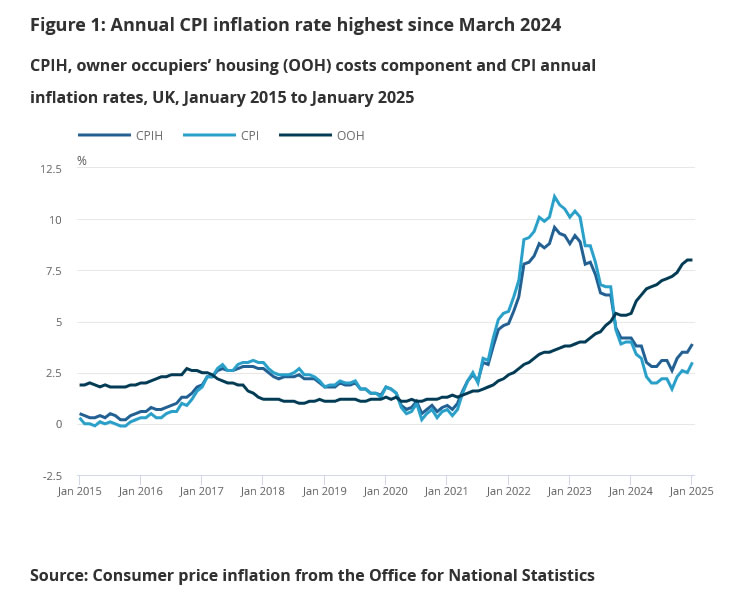

UK CPI surges to 3.0%, highest since March 2024

UK headline CPI accelerated to 3.0% yoy in January, up from 2.5% yoy and exceeding market expectations of 2.8% yoy. This marks the highest inflation level since March 2024, reinforcing concerns that price pressures remain persistent.

Core inflation also surged, with CPI excluding energy, food, alcohol, and tobacco rising to 3.7% yoy, up from 3.2% yoy in December.

Meanwhile, CPI goods inflation edged higher from 0.7% yoy to 1.0% yoy, while CPI services inflation climbed from 4.4% yoy to 5.0% yoy.

Trump Announces Sweeping Tariffs on Autos, Steel and Chips

In focus today

In Sweden we get the results from the Inflation Expectation Survey conducted by the Origo Group (previously Prospera). The Riksbank emphasises the importance of having the long (5y) inflation expectations well anchored at the 2% inflation target, which has been the case since the start of 2024 (between 1.9% and 2.1%). We do not expect to see any large deviations this time either.

In the UK, focus turns to inflation data for January, where consensus expects a rise in both headline and core terms driven by fuel prices and education. Service inflation is expected to tick up to 5.1% compared to the BoE's expectation of 5.0%. This will be the final CPI release ahead of the March meeting, where markets price low likelihood of a cut. We see the bar as high for delivering a cut in March and expect the next cut in May.

This morning China releases new home prices, which is an important gauge of the state of the housing markets. Prices have declined at a slowing pace in recent months in line with other indicators suggesting moderate improvement in housing demand. We look for prices to be around flat in January compared to December marking a halt to the decline in home prices.

Economic and market news

What happened overnight

In the US, President Trump said he would impose tariffs starting at 25% on automobiles, pharmaceuticals and semiconductor chips. No date was announced, although he plans to increase the tariffs to force companies to invest in the US. At the same time, he announced a March 12 start date for the 25% tariffs on steel and aluminium. Markets will presumably attempt to evaluate the sincerity of the statements throughout today.

What happened yesterday

Regarding the war in Ukraine, officials from the US and Russia met in Saudi Arabia for a first meeting on ending the war in Ukraine - without Ukraine represented. Both sides agreed to "lay the groundwork for future co-operation" with US national security adviser Mike Waltz commenting that the war needs to be ended permanently, and a discussion of territory and security guarantees will take place. Yuri Ushakov, Putin's foreign policy adviser, said that the US and Russia are collaborating to set the stage for a meeting between Trump and Putin.

In Sweden, the detailed CPI report for January came in just below expectations at 0.9% y/y (cons: 1.0% y/y) and 0.0% m/m (cons: 0.0% m/m). CPIF ex. Energy matched the surprising flash reading at 2.7% y/y, which could be a worrying sign of a broader inflation pressure.

In the UK, the labour market report for December/January came in with data slightly stronger than expected. The unemployment rate remained steady at 4.4 % in December and payrolls likewise came in higher than expected in January with positive revisions for December, although this can be largely attributed to the public sector. Overall, yesterday's report highlights that the BoE will most likely continue to stick to its "careful and gradual" approach to easing monetary policy.

In Germany, the ZEW index rose more than expected in February. The assessment of the current economic situation increased to -88.5 (cons: -89.4, prior: -90.4), which is the highest level in four months, and expectations increased to 26.0 (cons: 20.0, prior: 10.3). The ZEW index suggests that the positive surprises in German indicators (ZEW, Ifo, PMI) we saw in January continued in February. The indicators remain at very low levels, and we expect the economy to continue stagnating in the near term, but the stabilisation is finally a non-negative signal for the German economy.

Equities: Equities continued higher, driven equally by Europe and US, despite US being closed for holiday on Monday. Interesting to see big tech lagging notably without killing the party. Small caps and equal weighted equity indexes fared better, with energy, metals and semiconductor companies among the stronger groups. European banks adding 2% aided by higher yields. Asian markets are strong this morning as well, with South Korea rising 2%. The buzz is centred on Europe, but Korea have also added a dazzling 10% YTD. US futures are higher this morning.

FI: European rates traded mostly sideways through the trading session amid little news. The lack of driver led to an outperformance by the usual low-volatility performing trades (carry trades), best captured by the BTPs-Bund spread, which is now just at 105bp, which is the tightest since 2021. Tonight, FOMC minutes are released from the January meeting.

FX: Yesterday was another relatively quiet session, with broad USD strength across the G10 space. EUR/USD remains rangebound in the mid-1.04 to 1.05 area, while USD/JPY continues to trade around the 152-mark. USD/CAD held steady near 1.42 after Canada's January CPI print aligned with consensus. EUR/GBP ended the day below 0.83 following a slightly stronger-than-expected UK labour market report for December/January. In the Scandies, EUR/SEK trended slightly lower to 11.20, while EUR/NOK edged higher to 11.65.

Elliott Wave View: S&P 500 (SPX) Breaking to New All-Time High

Short term Elliott Wave in S&P 500 (SPX) suggests that pullback to 5774.1 ended wave ((4)). The Index has resumed higher in wave ((5)) and broken above previous wave ((3)) peak. Wave ((5)) is in progress as a 5 waves impulse Elliott Wave structure. Up from wave ((4)), wave ((i)) ended at 5871.9 and pullback in wave ((ii)) ended at 5805.4. Wave ((iii)) higher ended at 5964.69 and pullback in wave ((iv)) ended at 5930.72. Final leg wave ((v)) ended at 6128.18 and this completed wave 1 in higher degree.

Pullback in wave 2 unfolded as a zigzag Elliott Wave structure. Down from wave 1, wave ((a)) ended at 5962.92 and rally in wave ((b)) ended at 6120.91. Wave ((c)) lower ended at 5923.9 which completed wave 2 in higher degree. The Index has resumed higher again in wave 3. Up from wave 2, wave ((i)) ended at 6101.28 and pullback in wave ((ii)) ended at 6003. Up from there, wave (i) should end soon, and the Index should pullback in wave (ii) to correct cycle from 2.12.2025 low before it resumes higher. Near term, as far as pivot at 5774.1 low stays intact, expect pullback to find buyers in 3, 7, or 11 swing for further upside.

S&P 500 (SPX) 60 Minutes Elliott Wave Chart

SPX Video

https://www.youtube.com/watch?v=1_SsYDsGGFc

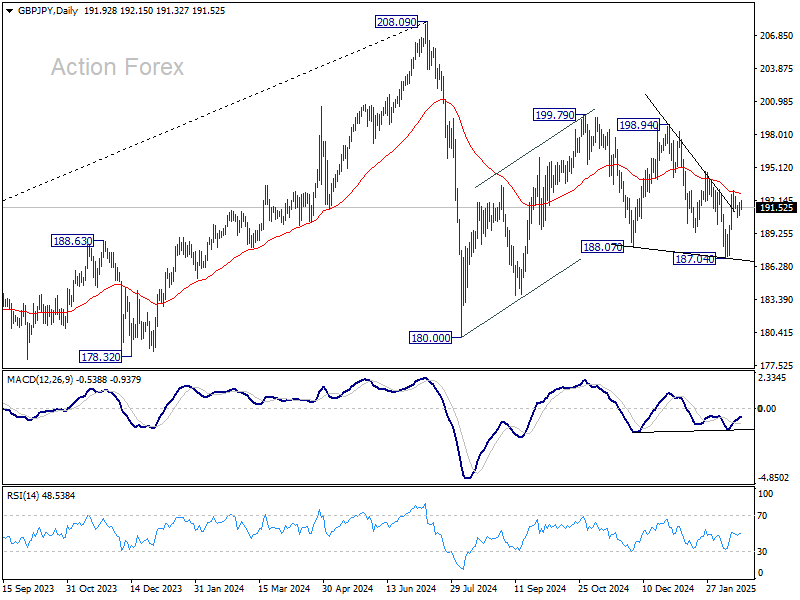

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.12; (P) 191.53; (R1) 192.22; More...

Intraday bias in GBP/JPY remains neutral for the moment. Outlook is unchanged that corrective pattern from 180.00 is extending, possibly with rebound from 187.04 as another upleg. Above 193.04 will target 194.73 resistance first. Firm break there will solidify this case and target 198.94 next.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 208.09 to 180.00 from 199.79 at 171.70, even still as a correction.

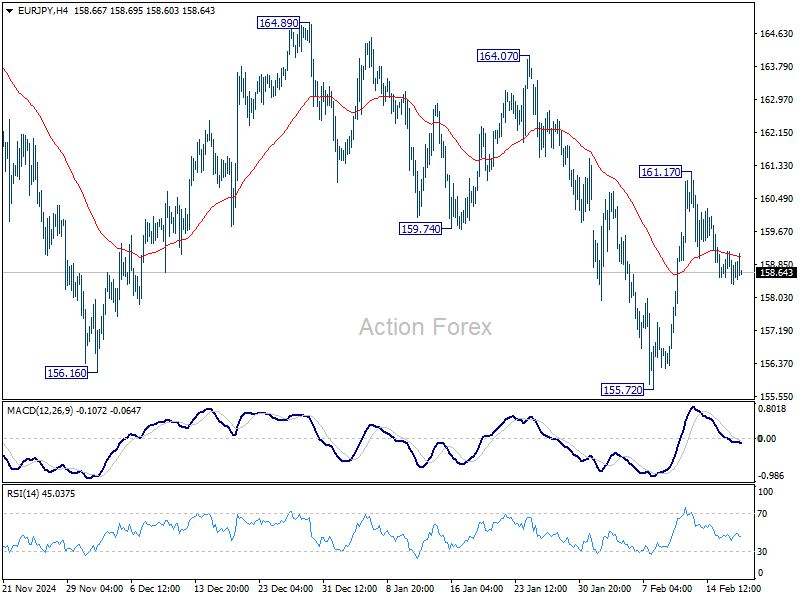

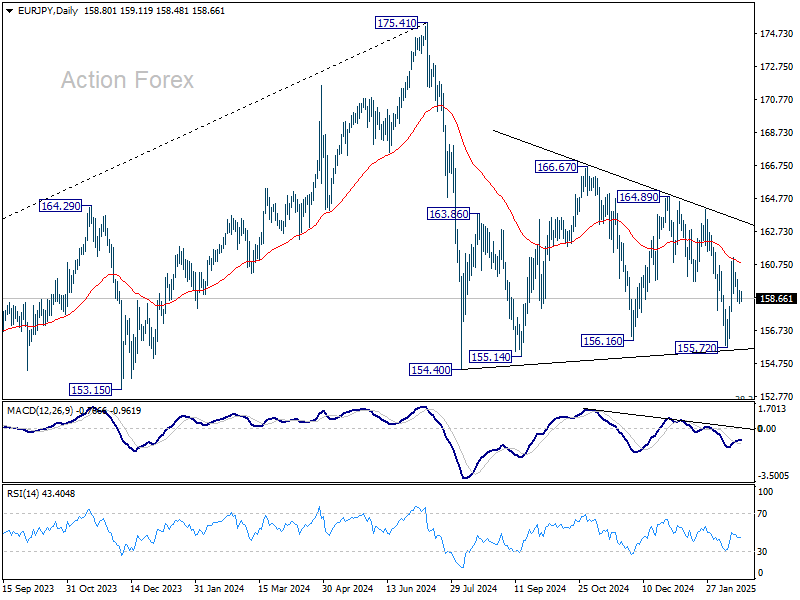

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.41; (P) 158.81; (R1) 159.24; More...

Intraday bias in EUR/JPY stays neutral for the moment. Outlook is unchanged that sideway pattern from 154.40 is still extending with another upleg. On the upside, above 161.17 will target 164.07 resistance and then 164.89.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

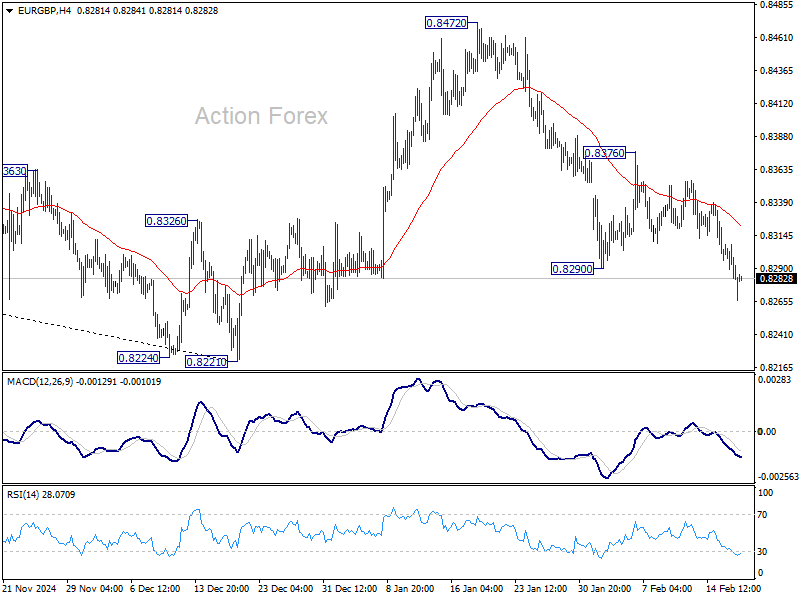

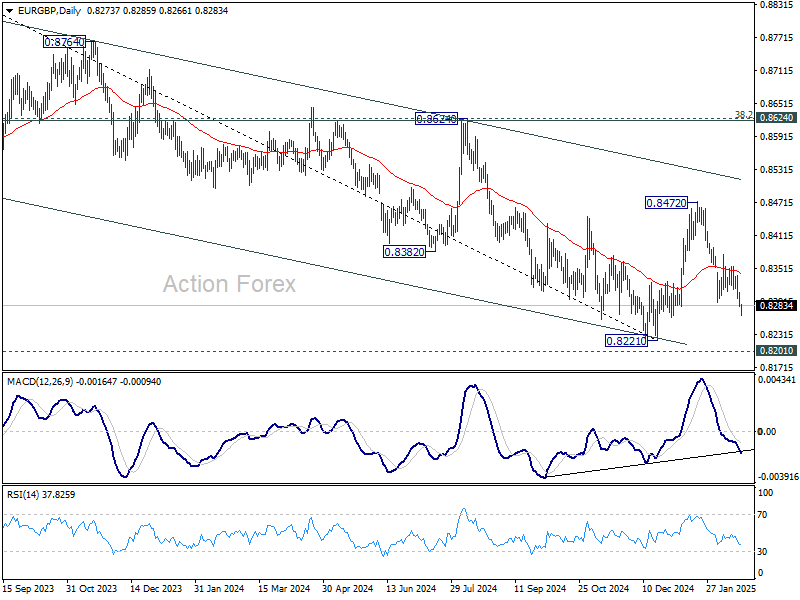

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8271; (P) 0.8291; (R1) 0.8300; More...

EUR/GBP's fall from 0.8472 resumed by breaking through 0.8290 support. Intraday bias is back on the downside for retesting 0.8221 low. For now, risk will remain on the downside as long as 0.8376 resistance holds, in case of recovery.

In the bigger picture, rebound from 0.8221 medium term bottom could extend higher through 55 W EMA (now at 0.8435). However, medium term outlook will be neutral at best as long as 0.8624 cluster resistance zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621) holds. Another decline through 0.8221 would remain mildly in favor. Firm break of 0.8221 will resume whole down trend from 0.9267 (2022 high) and carry larger bearish implications.

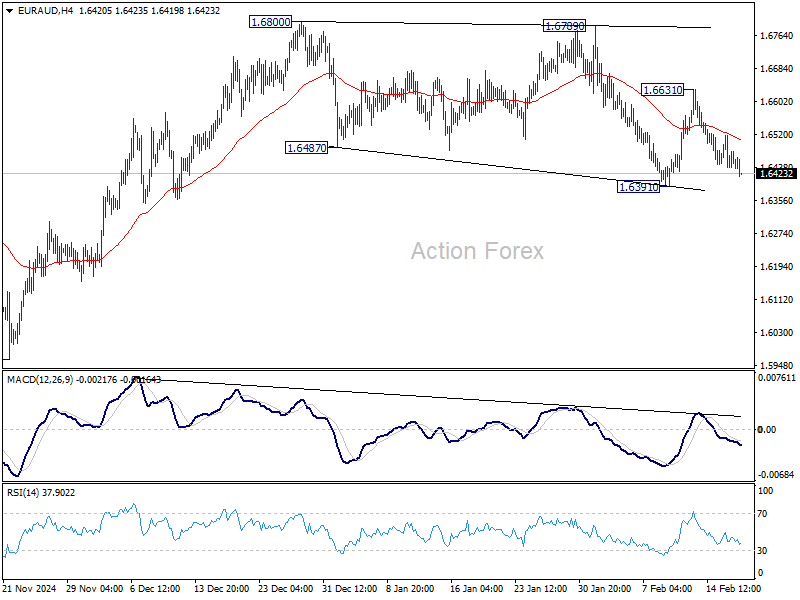

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6416; (P) 1.6468; (R1) 1.6498; More...

Intraday bias in EUR/AUD stays neutral for the moment. On the upside, break of 1.6631 resistance will reaffirm the case that consolidation from 1.6800 has completed at 1.6391. Retest of 1.6800 high should be seen next and firm break there will resume the rally from 1.5963. However, firm break of 1.6391 will invalidate this view and bring deeper fall.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

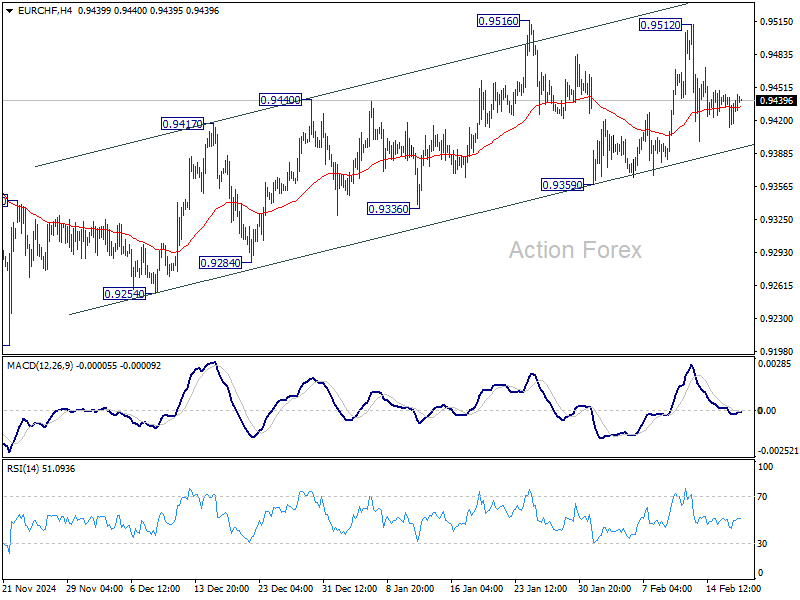

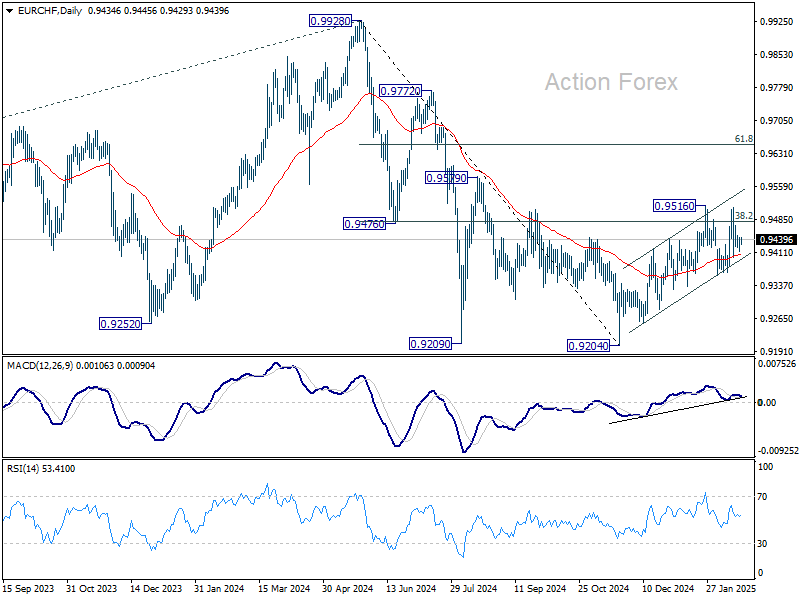

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9418; (P) 0.9434; (R1) 0.9453; More....

EUR/CHF is staying in range trading below 0.9516 and intraday bias stays neutral. On the downside, break of 0.9359 support will revive the case that choppy rise from 0.9204 is merely a correction and has completed. Deeper fall should then be seen back to retest 0.9204 low. However, firm break of 0.9516 and sustained trading above 0.9481 fibonacci level will carry larger bullish implication and extend the rise from 0.9204.

In the bigger picture, sustained trading above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204.

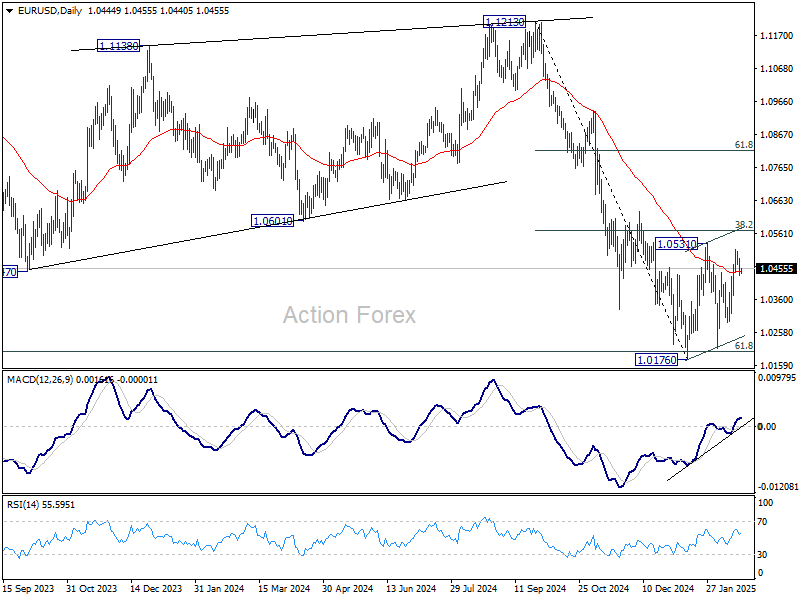

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0425; (P) 1.0456; (R1) 1.0477; More...

EUR/USD is staying in consolidation from 1.0176 and intraday bias stays neutral. Stronger rebound might be seen but outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.