Sample Category Title

Weekly Economic and Financial Commentary: Looking Good Going into the Holiday Season

U.S. Review

Gobble, Gobble till You Wobble

- There was a light schedule of economic reports released ahead of the Thanksgiving holiday.

- Existing home sales rose solidly in October, with overall sales rising 2 percent. Inventories fell further and the median price of an existing home has risen 5.5 percent over the past year.

- Advance orders for durable goods came in below expectations but nearly all the shortfall was in the highly volatile commercial aircraft component. Orders for the prior month were revised higher and the longer-term trend remains solidly positive.

Looking Good Going into the Holiday Season

The economy looks like it has strong momentum going into the holiday season and consumers, retailers and businesses should all be in a fairly festive mood this year. This week's limited schedule of economic reports included just four major indicators: existing home sales, advance durable goods orders, weekly unemployment claims and the University of Michigan's Index of Consumer Sentiment. All of the reports are consistent with the economy throttling back a bit from the 3 percent plus pace averaged during the prior two quarters. In fact, revisions to previously published data suggest that third quarter real GDP growth will be revised higher to 3.2 percent.

Data on existing home sales came in slightly above expectations. Overall sales rose 2.0 percent in October, rising to a 5.48 million unit pace, following a smaller than initially reported 0.4 percent increase in September. Those two gains followed three consecutive monthly drops during the summer months that have raised some concerns that the housing recovery is running out of steam. On a year-to-year basis, existing home sales are running 0.9 percent below their year-ago level.

The apparent weakness in existing homes sales does not appear to be due to a lack of demand. Homes are selling quickly and home prices are rising solidly. The National Association of Realtors noted that the typical home sold in just 34 days and that 47 percent of existing homes sold in one month or less. Homes that are priced around the median of $247,000 or less are also selling very quickly and there are very few homes available at lower price points. The median price of an existing home has risen 5.5 percent over the past year.

The inventory of homes available for sale at the end of October fell 3.2 percent from the prior month to just 1.80 million units. There is just a 3.9 month supply of homes available for sale at the current sales pace, down from 4.4 months one year ago. The number of homes available for sale has tumbled 10.4 percent over the past year, while sales have fallen 1 percent. With inventories down more than 10 times as much as sales, the shortage of homes appears to be the likely culprit of any pullback in sales.

Advance orders for durable goods fell 1.2 percent in October and orders for the key nondefense capital goods component also fell during the month, albeit by a much smaller 0.5 percent, marking their first decline since June. Most of the drop in overall orders was due to an 18.6 percent pullback in orders for nondefense aircraft. That highly volatile component had risen 33 percent or more during each of the past two months and appears to be primed for another big up month, given the strength in orders reported by Boeing and Airbus at the Dubai Air Show.

While nondefense capital goods orders slipped, the longer run trend in orders remains solidly positive. The category provides a good approximation for investment in capital equipment. Orders over the past three months have risen at a 14.5 percent average annual rate and shipments have increased at a 13.1 percent pace, which helps get the fourth quarter off to a strong start.

U.S. Outlook

Consumer Confidence Index • Tuesday

Consumer confidence continued its tear in October, rising 5.3 points to 125.9, marking the highest level for consumer confidence since December 2000. The Consumer Confidence Index measures the breadth of confidence rather than its magnitude. The 24.9 percent rise over the past year means more consumers are feeling optimistic about the economy than one year ago. Over this period, consumers' assessment of the present situation has risen 22.7 percent, while their expectations for economic conditions over the next six months has risen 26.9 percent. This suggests consumers feel more optimistic about the current state of the economy and its future prospects.

We expect consumer confidence to pull back slightly in November but to remain near cycle-high levels.

Previous: 125.9 Wells Fargo: 124.9 Consensus: 124.0

Personal Income & Spending • Wednesday

Real personal spending finished Q3 on a high note, rising 0.6 percent in September and marking the second-fastest monthly growth rate of the past three years. Real consumer spending is up a solid 2.7 percent on the year, where it has hovered for most of 2017.

Personal income growth disappointed again, however, with just a 0.4 percent nominal gain. September's weak job growth likely weighed on income growth, and we may get a rebound in October. Through the monthly noise, the soft income growth seen in recent months has meant that consumers continue to draw down their saving rate. The saving rate fell to 3.1 percent in September from 3.6 percent during the first two months of Q3, down from as high as 6.0 percent two years ago.

Members of the FOMC will be watching the October print for a rebound in core PCE inflation. Some upward momentum heading into 2018 would bode well for continued fed funds hikes next year.

Previous: 0.4% Wells Fargo: 0.4% Consensus: 0.3% (Month-Over-Month, Income)

ISM Manufacturing Index • Friday

The ISM manufacturing index retreated slightly in October from its unusually strong September reading. The supplier deliveries subcomponent is still providing an artificial boost to the index, and this effect is likely to fade further in the November reading.

The underlying trend continues to be positive. The six-month averages for the production and new orders subcomponents are above 60, and the employment subcomponent has averaged a respectable 57.7 over the same period. The hard data have backed up the survey, with core capital goods orders rising at a 14.5 percent three-month average annualized rate through October.

We look for the ISM manufacturing index to pull back slightly in November to 58.4. With encouraging fundamentals in place, we expect the slow but steady improvement in the U.S. factory sector to continue in the coming months.

Previous: 58.7 Wells Fargo: 58.4 Consensus: 58.4

Global Review

In Germany, Political Uncertainty Sets In

- The German economy is booming at present with the yearover- year GDP growth rate standing at a six-year high and unemployment at its lowest rate in the post-reunification period.

- However, Germany is entering into a period of political uncertainty. Negotiations to form a new governing coalition collapsed this week, which could lead to a potentially unstable minority government. Not only could political uncertainty have a knock-on effect on the German economy, but it also makes it harder to pursue further integration in Europe.

In Germany, Political Uncertainty Sets In

This has been a rather quiet week in terms of foreign economic data releases, so we focus on recent political and economic developments in Germany. Following the German general election on September 24, Chancellor Merkel and her Christian Democratic Union (CDU) entered into negotiations with the Free Democrats (FDP) and the Green Party on forming the next government. The collapse of the coalition negotiations that was announced on Sunday is not a huge surprise given the ideological differences among the center-right CDU, the economically liberal FDP and the environmentally-conscious Greens.

So what happens now? There appears to be three options. First, the CDU has been governing Germany in coalition with the center-left Social Democrats (SPD) since the last general election in 2013. In theory, the CDU could form a new "grand coalition" with the SPD, but the latter has ruled out that option. Second, the CDU could govern as a minority government. Because the CDU does not have a majority of seats in the Bundestag, the lower house of the German parliament, it would need to pass legislation with other parties on an ad hoc basis. However, minority governments tend to be unstable because they can easily be brought down by no confidence motions. Third, the federal president could call for a new election. However, President Steinmeier seems reluctant to call new elections, at least at this point, because of the risk that fringe parties could garner even more votes than they did in September. In short, Germany seems set for a period of political uncertainty.

If voters cared only about pocketbook issues the CDU would have been returned overwhelmingly to power in the September elections, because the German economy is booming at present. Real GDP was up 2.8 percent in Q3-2017, the strongest year-overyear rate of growth in six years. Moreover, growth is broad-based at present with consumer spending, investment spending and exports all contributing positively to the overall rate of real GDP growth. Growth in real retail sales has strengthened markedly this year (top chart), and unemployment has declined to the lowest rate in the post-reunification era (middle chart). The Ifo index of German business sentiment stood at an all-time high in October (bottom chart), suggesting that growth has remained buoyant thus far in the fourth quarter.

But pocketbook issues are not the only considerations that motivate citizens to vote for individual candidates or political parties, and Germany has not been immune to the populist/nativist voices that have affected elections in other western countries in recent years. Political uncertainty could have a marginal negative effect on the German economy in the near term, although it is not likely to derail the expansion that is underway in Germany. However, Chancellor Merkel was weakened by the election results, and she will be weakened further if she needs to govern via a minority government. There could also be implications for Europe from the inability to form a coalition. A weakened Merkel will find it harder to persuade other German politicians to agree to the deeper European integration proposals that French President Macron has proposed.

Global Outlook

Germany Retail Sales • Monday

The global economy, the week will start with the release of October retail sales for Germany. The index printed a strong 0.5 percent in September, the first positive reading in three months. On a yearearlier basis, the index was also strong, up 4.1 percent in September, the third consecutive year-over-year improvement.

Meanwhile, markets will also get the GfK consumer confidence index for December. The GfK hit a series high of 10.9 in September while coming down to print 10.7 in November. It will be interesting to see how or if the failure of Angela Merkel to form a governmental coalition has affected consumer confidence in the largest economy in the Eurozone.

Previous: 0.5% (Month-Over-Month)

China Manufacturing PMI • Wednesday

Manufacturing activity in China has held steady over the past several months as shown by the manufacturing PMI. In the October reading, the index printed 51.6, down from 52.4 in September. On Wednesday, markets are going to take a look at the November reading. This is the manufacturing PMI that includes large, normally state-owned enterprises.

The services PMI is also going to be released on Wednesday. The index was at 54.3 in October after hitting 55.4 in September. Meanwhile, the Caixin manufacturing PMI, which includes small and medium-sized manufacturing firms that are typically not covered by the official manufacturing PMI will hit the newswires on Thursday. After hitting a series high of 51.9 in December of last year, the index remained at 51.0 in September and October.

Previous: 51.6

Brazil Q3 GDP • Friday

Brazil will release Q3 GDP on Friday. The year-over-year result for Q2 was 0.3 percent, the first positive year-over-year increase since the first quarter of 2014. Our expectation is for the economy to have posted another increase in the third quarter.

According to the index of economic activity, which is a proxy for the performance of the Brazilian economy, the economy grew 1.4 percent during the third quarter of the year, year over year. Much of the improvement in the economy reflects stronger consumer spending. The appreciation of the currency and the disinflationary process plus the reduction in interest rates over the last year has strengthened the ability of Brazilians to increase consumption.

Previous: 0.3% (Year-Over-Year)

Point of View

Interest Rate Watch

What is up With the Yield Curve?

The yield curve continued to flatten this past week, sparking interest from financial market participants and people looking for a diversion from thinking about the holidays. The spread between the yield on the 10-year Treasury and 2-year Treasury note has shrunk to around 60 basis points, which is the tightest that spread has been since November 2007. The flattening of the yield curve has revived interest in what a flattening yield curve implies for the financial markets and broader economy.

The yield curve's track record on predicting recessions has been very good, particularly when the curve inverts. An inverted yield curve is a red flag that a recession is less than one year away. The flattening in the yield curve we have seen in recent weeks does not appear to be a precursor to an inversion. Instead, the flattening appears to be driven by technical concerns, including liquidity needs ahead of year-end that are possibly compounded by the increased likelihood of significant tax reform. There is also a near universal conviction among market participants that the Fed will raise rates in December. In addition, Treasury issuance has increased at the short end of the curve but remained somewhat muted at the long end.

Long-term bonds remain in high demand, driven by an aging population in the developed world and voracious appetite from pension funds, insurance firms and other large long-term savers. The yield on the 30-Year Treasury has fallen about 16 basis points over the past four weeks to 2.78 percent, while the yield on the 10-year has fallen about 7 basis points. By contrast the yield on the 2-year Note has risen about 17 basis points over the past four weeks to 1.75 percent.

The technical factors driving the flatter yield curve may have a bit more to run, but we doubt the curve will completely flatten or invert. Aside from outright inversions, the shape of the yield curve has a spotty record of predicting economic growth. In fact, we expect the relationship to go the other way, with stronger economic growth, tightening labor markets and higher inflation leading to a steeper yield curve during the coming year.

Credit Market Insights

Consumers Content on Credit Access

The New York Fed asks consumers about their experiences in the credit market every four months, and this week, released results for the October iteration. In keeping with the results of other subjective surveys this year, consumers were upbeat about access to credit.

The application rate was in-line with its series average for credit cards and auto loans but rose slightly for mortgages. The uptick in the mortgage application rate was driven by middle-aged (40 to 60 years) and mid-credit score (680 to 760) borrowers. The rate of rejection declined for each type.

Fewer consumers responded that they were too discouraged to apply even though credit was needed. Just 4.9 percent of the sample was too discouraged to apply which is a low point for the series that started in 2013.

Expectations for needing to apply for credit in the next year held steady for each credit type. Improvement on the expectations front came from fewer consumers saying that they expected their credit applications to be denied should the need arise.

The New York Fed asked a specific question about financial fragility, asking consumers if they could come up with $2,000 to cover an unexpected expense, and 70 percent of respondents answered yes.

The takeaway from this survey was that consumers are quite comfortable with their ability to obtain credit if needed. That is an important source of financial security.

Topic of the Week

2017 Holiday Sales Outlook

Consumer confidence is currently at its highest level since December 2000. Improved expectations coupled with a persistently positive attitude toward consumers' present economic situation, point to an optimistic outlook for consumer demand this holiday season. We highlight that improved confidence figures have not translated to an expected uptick in personal consumption. Real personal consumption expenditures (PCE) have downshifted over the past few years, which has likely in part been an effect of a lack of income growth.

Our forecast for holiday sales this year is for an increase of 4.0 percent on a seasonally adjusted basis compared to only 3.0 percent for last year (top graph). According to the National Retail Federation media release, American consumers are planning to spend, on average, $967.13 during this holiday season, which is up 3.4 percent from what the survey indicated they were planning to spend last year (bottom graph). Fundamentals point to relatively strong consumer demand this season.

The projected uptick in sales is in-line with strong retail sales figures for October, which suggest solid momentum for spending headed into the fourth quarter. Likewise, the labor market remains supportive of relatively strong holiday spending, with the unemployment rate at just 4.1 percent and a continued rise in the demand for workers. We highlight that average hourly earnings have slowed slightly, although we expect firming in coming months due to the continued strength of the labor market.

Improved confidence in the future has outweighed the lack of income growth of the consumer. Confidence has brought down the saving rate at the same time as Americans have continued to borrow to complement income growth, helping keep PCE on a relatively stronger path than income growth would normally suggest. Strong confidence, coupled with high expectations of tax reform, could translate to an even larger bump in holiday sales than expected. We are projecting risks to our holiday sales forecast to be tilted to the upside this holiday season. For a more detailed analysis of our outlook, please read our full report here: 2017 Holiday Sales Outlook.

USD Continues to Struggle. EU News Supports Euro

- European equities shrugged off sharply lower Chinese equity indices in Asia overnight and eked out modest gains with utilities, telecommunication the frontrunners in the EuroStoxx. The US market closure (Thanksgiving) affected trading volumes across markets.

- The ECB's top officials rallied around the idea of extending its asset purchase programme into a fourth year, but at half the current rate, minutes of the October 26 meeting show. There was "broad agreement" that an ample degree of monetary stimulus was still needed for inflation to reach the ECB's target."

- The South African Reserve Bank left its benchmark rate at 6.75% after September's surprising decision to leave rates on hold instead of cutting them. The big test comes tomorrow, when key ratings agencies are due to announce whether they will downgrade the country's debt - a move that could shove South Africa out of major bond indices.

- The Turkish lira failed to sustainably gain ground after Cemil Ertem, economic adviser to president Erdogan, said the central bank could raise rates "any time". President Erdogan has for years set his face against higher interest rates, a position that has left investors to question the independence of the central bank.

- The beleaguered UK retail sector got a month of respite in November, according to the CBI survey. Almost 40% retailers surveyed said sales volumes were higher than a year ago, with a similar number optimistic that volumes would pick up again next month. Only 13% said sales were down in November, with fewer expecting a drop in Dec.

- Businesses in the eurozone reported their best month of activity in more than 6 years in November with job growth at a 17-year high, according to the Markit surveys. The headline PMI index for the euro area rose from 56 to 57.5, with multi-year highs for all the main indicators of output, demand, employment and inflation

Rates

Uneventful sideways bond trading

German bonds traded uneventful in the absence of US traders (Thanksgiving). Equities and the euro held a sideways trading range as well. The Bund opened slightly higher, but never caught a strong directional bid. As the upside was blocked, traders tried it on the downside. Selling dried soon up though despite strong euro area PMI business sentiment (see headlines). The intraday trading range amounted to 20 ticks divided evenly around the Wednesday's close (162.99). In the afternoon, the accounts of the October ECB meeting were published. They showed some interesting features, but nothing really new and important (see below). At the time of writing, German yields are marginally higher (flat to +0.7 bps). On intra-EMU bond markets, 10-yr yield spreads versus Germany widened 1 to 2 bps, reversing yesterday's decline.

The ECB accounts of the last ECB meeting revealed that there was broad agreement on the extent of the bond buying cut (from €60B to €30B). It was still deemed necessary for inflation to reach the ECB inflation target. The slower pace of purchases signaled growing confidence though that inflation would eventually rise. Several alternative solutions were put forward and discussed including a longer extension and one having a clear end date for QE, but the large majority agreed that it was prudent to keep the program flexible. "Several" policy makers also said that the current ECB guidance linking asset purchases to an improving inflation outlook should eventually be replaced" with a reference to the monetary policy stance, in all its dimensions.

The private sector programmes would not be adjusted in strict proportion to the overall scaling down of the APP bond buying. Purchases of these bonds (corporate, ABS and covered bonds) would remain sizeable and scaled back more slowly. Because of the flexibility to spread out reinvestments, the published monthly purchase amounts would likely become more volatile.

Currencies

USD continues to struggle. EU news supports euro.

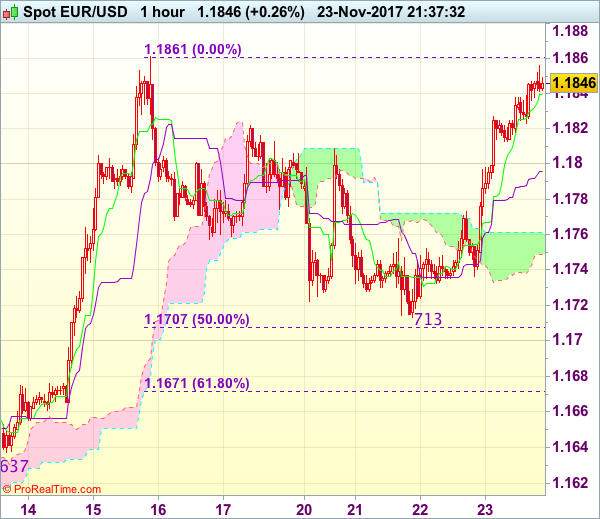

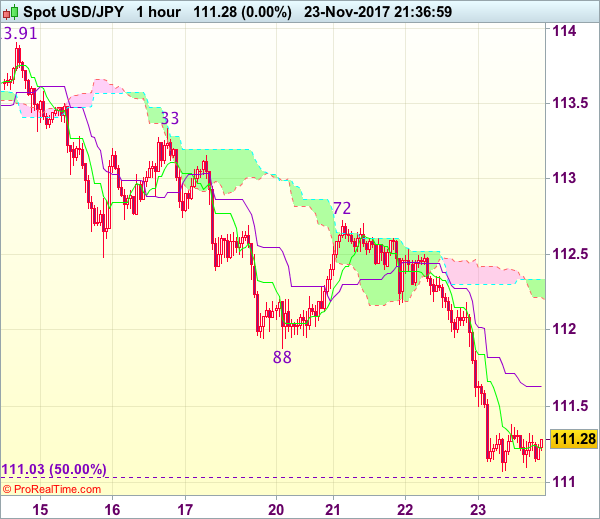

Global/FX trading shifted into a lower gear today as US markets are closed in observance of the Thanksgiving holiday. The dollar remained in the defensive after yesterday's soft Fed minutes. At the same time, the euro was slightly supported by strong EMU PMI's. EUR/USD came close to the 1.1861/80 resistance, but a real test didn't occur. USD/JPY hovers in the 111.25 area.

Overnight, Asian equity markets traded mixed to lower. Japanese markets were closed. Chinese markets underperformed. Losses mounted up to 3%, amongst others on fear from more credit regulation. EUR/USD held well north of 1.18. This was mainly due to overall USD softness. Speculation on a new grand coalition in Germany was a slight additional supportive for the euro. USD/JPY hovered in the lower half of the 111 big figure.

EUR/USD maintained a cautiously positive bias during the European morning session. Investors still avoided USD longs after yesterday's 'soft' Fed minutes. At the same time, EMU PMI's were substantially stronger than expected, indicating that EMU Q4 growth might even surpass Q3's 0.6% quarterly growth. EUR/USD filled offers in the 1.1855 area early in the afternoon session. A real test of the 1.1861/1.1880 resistance didn't occur yet. Investors are apparently reluctant to take such a 'big step' without guidance from the US. The minutes of the October ECB meeting brought the different views that resulted in the ECB policy decision on APP. However, they didn't bring really new insights. There was no noticeable reaction of the euro. EUR/USD trades currently in the 1.1850 area. USD/JPY hovers near 112.25. The USD sell-off slows, but there is no sign of a turnaround yet.

EUR/GBP returns to 0.89 area

UK Q3 GDP growth was confirmed a 0.4% Q/Q and 1.5% Y/Y today. Consumer spending remained the main driver for growth (0.6% Q/Q). Investments (gross fixed capital formation) was soft (0.2% Q/Q). Later in the session, the CBI November retail data printed much stronger than expected, both for the current sales and for expected sales, indicating that the UK consumer keeps spending going into the holiday season despite negative pressure on the disposable income. The data had hardly any impact on the UK currency. The focus for sterling trading remains on Brexit. UK and EU negotiators are said to work behind closed doors to prepare a document on the progress in the run-up the December EU summit. However, for now there is no concrete news on specific topics. EUR/GBP trades in the 0.89 area This move is at least partially the result of the EUR/USD rally. Cable (1.3310) trades slightly off the overnight top, but remains well bid on USD softness.

Canadian Retail Spending Volumes Edged Down again in September

Highlights:

- September retail sales inched up 0.1% but only because prices rose

- Volume sales declined 0.6% - a third straight monthly drop. Sale volumes dipped lower in Q3 as a whole for the first time since Q2 2016.

- E-commerce sales (not all of which are included in the retail sales totals) were up 16.7% over the past year ending in September. That was much faster than the 6% increase in overall retail sales but still down from 40%+ readings in earlier months

Our Take:

Retail sales inched up 0.1% in September but only because of a price-led 2.6% increase in sales at gasoline stations. Statistics Canada noted that sales at stores typically thought to be sensitive to housing purchases and home renovation bounced back after declining in August but sales at clothing stores fell by 2.8%. Controlling for the impact of prices, sale volumes declined for a third straight month with a 0.6% dip in September. They declined by 1.4% at an annualized rate in Q3 as a whole. Of course, the data is often volatile and the drop in Q3 retraces little of the average 8% per-quarter increase from Q4/16 to Q2/17 — the strongest 3-quarter stretch since 2004. The data does, however, provide further confirmation that the economy as a whole came off the boil in Q3/17. The dip in September retail sale volumes points to some downside risk to our prior expectation that overall GDP inched up 0.1% in the month and also modest downside to our call for a 1.7% Q3 gain. Looking through monthly/quarterly volatility, we think the economy should continue to grow at a slightly 'above-potential' pace but likely closer to 2% than the outsized 4% growth per-quarter over the first half of the year.

Canada: Retail Sales Volumes Slide Again in September

Following two months of declines, retail sales edged up 0.1% in September. However, in real terms, the declines continued, with sales volumes down 0.6% during the month.

The key driver behind the overall increase in September was higher sales at gasoline stations (+2.6%), due to rising prices caused by Hurricane Harvey. Volumes of gas station sales were actually down 2.5%. Elsewhere, sales tied to housing activity including furniture (+2.3%) and building material and garden equipment (+2.6%) stores were up, while most other industries recorded a decline during the month.

Regionally, the story was a mixed bag, with sales up in half the provinces. Ontario (+0.5%) recorded the largest gain in dollar terms thanks to higher gas station sales, while BC (+0.4%), Alberta (+0.3%) New Brunswick (+2.1%) and Newfoundland and Labrador (+1.8%) were also up during the month.

Key Implications

After a strong first half of the year, consumers took a breather in the third quarter, with retail sales volumes down 0.4% over the three month period. This suggests a deceleration GDP growth during the quarter from its earlier breakneck pace, with our tracking currently sitting below 2%. The soft handoff also reduces momentum heading into the fourth quarter.

Consumer spending has been a key driver of economic growth this year and while a more sustainable rate of growth is likely, it should remain a key support going forward. Indeed, some improvement in retail sales could be in the cards, in line with the uptick in housing market activity and a strong labour market.

Today's data is in line with the slowing in economic activity expected by the Bank of Canada. We continue to expect the Bank to remain on hold in December, before taking rates higher in early-2018.

Euro Boosted by Stellar PMIs, Canadian Dollar Pressured after Poor Retail Sales

Euro strengthens broadly today as supported by solid PMI data that indicates strong Q4 growth. Nonetheless, the common currency remains in negative territory against all major currency except Dollar and Loonie, Canadian Dollar suffers some selling after much softer than expected retail sales data. Overall, trading is relatively quiet today as US is on holiday. Subdued trading could carry on for the rest of the week.

Eurozone PMI: Q4 to round off best year for a decade

PMI data out of Eurozone are generally positive. Eurozone PMI manufacturing rose to 60.0 in November, up from 58.5, above expectation of 58.2. Eurozone PMI services rose to 56.2, up from 55.0, above expectation of 55.2. Germany PMI manufacturing rose to 62.5, up from 60.6 and above expectation of 60.3. Germany PMI services rose slightly to 54.9, up from 54.7, missed expectation of 55.0. France PMI manufacturing rose to 57.5, up from 56.1, beat expectation of 55.9. France PMI services rose to 60.2, up from 57.3 and beat expectation of 57.0.

Markit noted that "growth kicked higher in November to put the region on course for its best quarter since the start of 2011." And, "the PMI is so far running at a level signalling a 0.8% increase in GDP in the final quarter of 2017, which would round-off the best year for a decade."

Also released from Europe, German GDP was finalized at 0.8% qoq in Q3. UK GDP was unrevised at 0.4% qoq in Q3. Total business investment rose 0.2% qoq. Index of services rose 0.4% 3mo3m. CBI reported sales jumped sharply to 26 in November.

ECB accounts showed "broad agreement" on asset purchase cut

The accounts of ECB October meeting showed that there was "broad agreement" among policymakers to cut the asset purchase program next year. The account added that "the envisaged purchase horizon served to underline the Governing Council's commitment to its price stability objective and also entailed a prolonged market presence in view of possible future shocks."

Meanwhile, there were concerns that "the open-ended nature of the asset purchase program might generate expectations of further extensions as the intended end date of the program approached." And the idea was put forth for a "clear end date" to the program. But the general consensus was to "keep the flexibility to extend the programme further if necessary."

Elsewhere

Canada retail sales rose 0.1% mom in September, well below expectation of 1.0% mom. Ex-auto sales rose 0.3% mom, below expectation of 1.1% mom. New Zealand retail sales rose 0.2% qoq in Q3, core retail sales rose 0.5% qoq, both below expectation. Eurozone PMI will be a main feature in European session.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Retail Sales Q/Q Q3 | 0.20% | 0.40% | 2.00% | 1.80% |

| 21:45 | NZD | Retail Sales Core Q/Q Q3 | 0.50% | 0.90% | 2.10% | 1.90% |

| 07:00 | EUR | German GDP Q/Q Q3 F | 0.80% | 0.80% | 0.80% | |

| 08:00 | EUR | France Manufacturing PMI Nov P | 57.5 | 55.9 | 56.1 | |

| 08:00 | EUR | France Services PMI Nov P | 60.2 | 57 | 57.3 | |

| 08:30 | EUR | Germany Manufacturing PMI Nov P | 62.5 | 60.3 | 60.6 | |

| 08:30 | EUR | Germany Services PMI Nov P | 54.9 | 55 | 54.7 | |

| 09:00 | EUR | Eurozone Manufacturing PMI Nov P | 60 | 58.2 | 58.5 | |

| 09:00 | EUR | Eurozone Services PMI Nov P | 56.2 | 55.2 | 55 | |

| 09:30 | GBP | GDP Q/Q Q3 P | 0.40% | 0.40% | 0.40% | |

| 09:30 | GBP | Total Business Investment Q/Q Q3 P | 0.20% | 0.30% | 0.50% | |

| 09:30 | GBP | Index of Services 3M/3M Sep | 0.40% | 0.40% | 0.40% | 0.50% |

| 11:00 | GBP | CBI Reported Sales Nov | 26 | 5 | -36 | |

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | CAD | Retail Sales M/M Sep | 0.10% | 1.00% | -0.30% | -0.10% |

| 13:30 | CAD | Retail Sales Ex Auto M/M Sep | 0.30% | 1.10% | -0.70% | -0.40% |

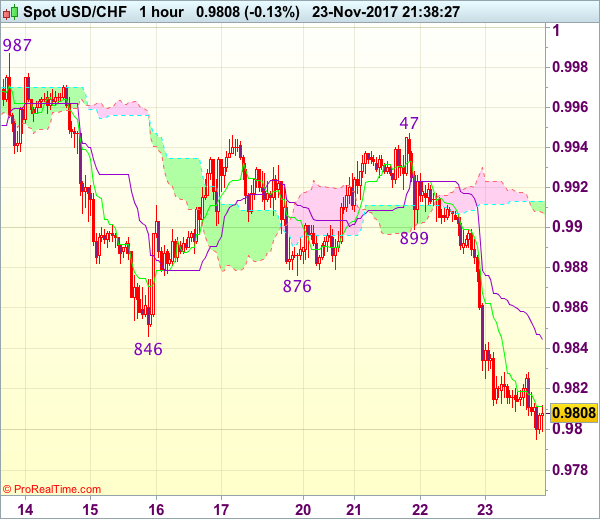

Trade Idea Wrap-up: USD/CHF – Sell at 0.9865

USD/CHF - 0.9811

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9812

Kijun-Sen level : 0.9845

Ichimoku cloud top : 0.9913

Ichimoku cloud bottom : 0.9907

Original strategy :

Sell at 0.9865, Target: 0.9765, Stop: 0.9900

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9865, Target: 0.9765, Stop: 0.9900

Position : -

Target : -

Stop : -

Dollar’s decline accelerated yesterday after breaking previous support at 0.9876 and 0.9846, adding credence to our bearish view and downside bias remains for the decline from 1.0039 top to extend further weakness to 0.9790-95, then 0.9770, however, oversold condition should prevent sharp fall below 0.9740-50 and bring rebound later.

In view of this, we are looking to sell dollar again on recovery as 0.9875-80 should limit upside and bring another decline. Above 0.9900 would defer and suggest low is possibly formed, bring rebound to 0.9920-25 burt resistance at 0.9947 should remain intact, bring another decline.

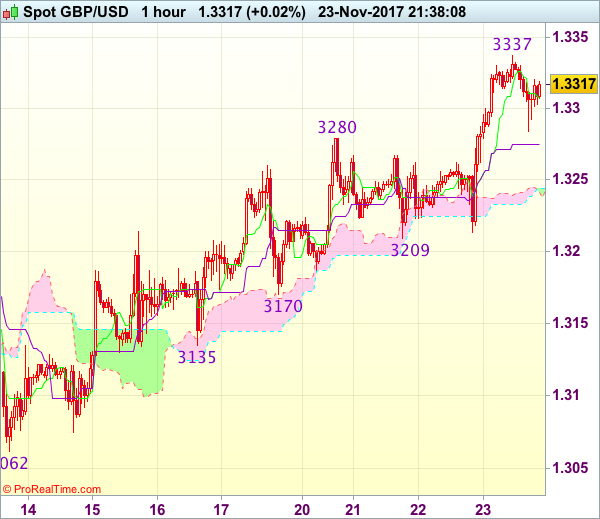

Trade Idea Wrap-up: GBP/USD – Buy at 1.3255

GBP/USD - 1.3308

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3307

Kijun-Sen level : 1.3275

Ichimoku cloud top : 1.3244

Ichimoku cloud bottom : 1.3242

Original strategy :

Buy at 1.3270, Target: 1.3370, Stop: 1.3235

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3255, Target: 1.3355, Stop: 1.3220

Position : -

Target : -

Stop : -

As cable has surged after holding above support at 1.3209 and the breach of 1.3280 resistance (now support) confirm recent upmove from 1.3039 is still in progress and may bring a test of previous resistance at 1.3338, however, break there is needed to retain bullishness and signal an upside break of recent established broad range, bring subsequent rise to 1.3370 and later towards 1.3400 but resistance at 1.3425 should hold from here.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as 1.3250-60 should limit downside. Below the lower Kumo (now at 1.3242) would defer an suggest top is possibly formed, risk test of said support at 1.3209.

Trade Idea Wrap-up: EUR/USD – Buy at 1.1780

EUR/USD - 1.1844

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1840

Kijun-Sen level : 1.1796

Ichimoku cloud top : 1.1761

Ichimoku cloud bottom : 1.1749

Original strategy :

Buy at 1.1780, Target: 1.1880, Stop: 1.1745

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1780, Target: 1.1880, Stop: 1.1745

Position : -

Target : -

Stop : -

As the single currency has rallied after finding renewed buying interest at 1.1713 and broke above 1.1809 resistance, signaling the correction from 1.1861 (last week’s high) has ended and retest of this level would be seen, however, break there is needed to retain bullishness and confirm recent upmove has resumed for headway to 1.1880 resistance, then 1.1900-10 but near term overbought condition should limit upside to 1.1940-50.

In view of this, we are looking to buy euro on pullback as 1.1775-80 should limit downside and bring another rise later. Below the lower Kumo (now at 1.1749) would abort and signal the rebound from 1.1713 has ended instead, bring retest of this level later.

Trade Idea Wrap-up: USD/JPY – Sell at 111.85

USD/JPY - 111.29

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.22

Kijun-Sen level : 111.63

Ichimoku cloud top : 112.34

Ichimoku cloud bottom : 112.21

Original strategy :

Sell at 111.85, Target: 110.85, Stop: 112.20

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.85, Target: 110.85, Stop: 112.20

Position : -

Target : -

Stop : -

Yesterday’s anticipated selloff adds credence to our bearish expectation for recent decline to resume and as price has remained under pressure, downside bias remains for recent fall from 114.74 top to extend further weakness to 111.00-05 (50% Fibonacci retracement of 107.32-114.74) but near term oversold condition should limit downside to 110.70 and reckon 110.40-50 would hold from here.

In view of this, we are looking to sell dollar on recovery as 111.88 (previous support now resistance) should limit upside and bring another decline later. Above 112.00-10 would defer and risk test of the upper Kumo (now at 112.34) but price should falter below resistance at 112.72, bring another decline later.

Canadian Dollar Ticks Higher, Retail Sales Next

The Canadian dollar has ticked higher in the Thursday session. Currently, USD/CAD is trading at 1.2679, down 0.13% on the day. On the release front, Canada releases retail sales reports. Retail Sales and Core Retail Sales are both expected to rebound to 0.9% in September, after posting declines a month earlier. US banks are closed for the Thanksgiving holiday, and there are no US events on the schedule.

The Federal Reserve released the minutes of its most recent meeting on Wednesday. Policymakers expect the US economy to continue showing strong growth, and predicted that interest rates will be raised in the "near term". Although policymakers did not provide further hints about the timetable of a rate hike, the markets remain convinced that additional rates are imminent. The odds of a rate hike in December are 91%, and the odds a January raise are at 89%.

The NAFTA trade agreement appears in trouble, which could bode badly for the Canadian economy. A fifth round of talks over NAFTA failed to lead to significant progress, prompting the US to send an ominous warning to Canada and Mexico. The US wants to raise the North American content of vehicles from 62.5% to 85% and require that 50% of content come from the US. As well, the US wants to put restrictions on Canadian and Mexican agriculture. Unsurprisingly, Mexico and Canada have rejected these proposals. Negotiators are hoping to wrap up a new deal by March 2018, but the US chief negotiator warned that "absent rebalancing, we will not reach a satisfactory result".