Sample Category Title

Trade Idea: USD/CAD – Sell at 1.2720

USD/CAD - 1.2682

Trend: Near term up

New strategy :

Sell at 1.2720, Target: 1.2570, Stop: 1.2780

Position: -

Target: -

Stop:-

The greenback ran into heavy selling pressure at 1.2837 earlier this week and has dropped sharply, suggesting the rebound from 1.2665 has ended there and consolidation with downside bias remains for another test of said support, however, break there is needed to signal another leg of decline from 1.2917 top is underway for weakness to support at 1.2636, below there would bring stronger correction of recent rise to 1.2600 and later towards 1.2550-60

In view of this, we are looking to sell the pair on recovery as 1.2720-30 should limit upside and bring another decline later. Above 1.2780-90 would dampen this bearish view and prolong consolidation, risk another bounce to said resistance at 1.2837 but only break there would signal correction from 1.2917 has ended instead, bring further gain to 1.2880 first.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Hammond Plans for Post-Brexit Britain; Pound Lifted above $1.33

The UK Chancellor of the Exchequer, Philip Hammond, unveiled his 2017 budget in parliament on Wednesday, which put the focus on investing for the future as Britain readies to leave the European Union. With the Conservative government still trying to bring under control a financial crisis era debt hangover, Hammond had little room for big giveaways. Instead, Hammond used his first budget after the disastrous June elections to plan for the future, with the housing market and business investment taking centre stage.

After an embarrassing U-turn on plans to raise national insurance for self-employed individuals in his Spring Budget statement, Hammond could not afford another blunder, with his unpopularity among the Brexiteers within the cabinet adding to the pressure. But it's not just the finance minister's credibility at stake with this budget as May's government badly needs a win with British voters following the dramatic rise in popular appeal of the Labour leader, Jeremey Corbyn, during the election campaign. Also at stake is the UK's economic credibility internationally as the country's reputation has come under scrutiny following the 2016 referendum decision to exit the EU.

The budget got off to a negative start in forex markets as the pound fell after the Chancellor revised down the government's forecasts for UK growth for 2017 and the next five years. The Office for Budget Responsibility (OBR) lowered its forecast for 2017 growth from 2% to 1.5% and for 2018 from 1.6% to 1.4%. The downward revisions were mainly on the back of weaker productivity growth in the UK, which have failed to recover after falling during the financial crisis.

Despite the reduced growth forecasts, Hammond has been given a bit of a boost from lower-than-expected government borrowing in the current fiscal year to date. The Chancellor's first giveaway was to set aside an extra £3 billion to prepare the UK for all possible outcomes of Brexit. Business measures were high on the agenda as he allocated £500 million for a range of initiatives, such as the development of 5G mobile network and fibre broadband, and £540 million to support electric cars. There was also a £2.3 billion investment boost for research and development and a £20 billion fund for technology industries to help start-ups.

Transport projects also received more money with the creation of a £1.7 billion transforming cities fund and £300 million set aside to connect the High Speed 2 rail link with future rail projects in the North of England. Other winners included the devolved governments for Scotland, Wales and Northern Ireland, which were allocated extra funding, and there are plans to devolve more power to the West Midlands. The National Health Service also got a boost with an extra £2.8 billion announced for the NHS in England and a £10 billion capital investment package for hospitals.

There were some tax increases too, with owners of older diesel cars taking a hit, additional measures to reduce tax avoidance, and a plan to charge income tax on UK sales of multinational digital companies that are based in low-tax jurisdictions.

Hamond's main headline grabber however, is the massive boost for the housing market. The government has come under pressure in recent years for not doing enough to support people climb on to the property ladder when average house prices have become unaffordable for many buyers. The government is committing £44 billion of capital funding for the housing market and new incentives to guarantee the construction of 300,000 new homes per year by the mid-2020s. The biggest surprise of the budget though was the announcement to abolish stamp duty for all first-time buyers of up to £300,000.

The UK's leading share index, the FTSE 100, hit an intra-day high of 7460.91 (up 0.7%) after the budget speech, before heading lower due to a weak Wall Street to close up by just 0.1%. The pound recovered from a dip to $1.3211 on the weaker growth forecasts before climbing towards six-week highs above $1.33, as investors saw the budget as being overall positive for UK growth without comprising the government's deficit commitment.

According to the OBR, the UK's debt will peak at 86.5% of GDP in 2017 and will start declining in 2018. A balanced budget remains a long way off though given the negative impact of Brexit on growth and the government's finances. Hammond's predecessor, George Osbourne, was forced to abandon his target of eliminating the deficit by 2020 following the Brexit vote, but the deficit remains on track to being reduced to 1.1% GDP in 2022-23.

The forecasts and Hammond's cautious spending plans should help the UK avoid any further downgrades to its credit rating. However, the projections are subject to the outcome of the Brexit talks as a crash exit from the EU could result in a further deterioration of public finances.

The Brexit negotiations did not get off to a very good start and the UK and the EU are currently in a deadlock, with the EU demanding that the UK settle the divorce terms before the talks proceed to discussing trade and a transition deal. There have been some optimistic signs recently amid reports that the prime minister, Theresa May, is now prepared to raise her offer of the Brexit bill from £20 billion to about £38 billion. This has raised hopes that a deal on the divorce terms could be reached in three weeks ahead of the EU summit in December.

The lack of breakthrough in December could send the pound tumbling again. The British currency has made an impressive recovery this year, gaining almost 8% versus the US dollar. It hit a 15-month high of $1.3656 in September but has been consolidating since amid the stalemate in the Brexit negotiations and the Bank of England following up its hawkish rhetoric with only a dovish rate hike. Yesterday's budget is seen as slightly increasing the odds of further rate hikes over the next 2-3 years and might reassure investors about the UK government's management of the economy.

However, the medium-term outlook will very much depend on what happens at the EU summit on December 14-15 as a further delay to an agreement for a transition period would only extend the uncertainty for businesses and further dampen confidence in the economy. Insufficient progress at the December summit could push the pound back towards $1.28, which is near the 50% retracement of the 2017 uptrend. A positive outcome on the other hand could bring the $1.40 handle into scope.

DAX Yawns Despite Stellar German Manufacturing PMI

The DAX index is showing limited movement in the Thursday session. Currently, the DAX is at 13,001.00, down 0.10%. On the release front, German Final GDP accelerated to 0.8%, matching the forecast. German and Eurozone Manufacturing PMIs beat their estimates, with readings of 62.5 and 60.0, respectively. Later in the day, the ECB releases the minutes of its October policy meeting. On Friday, Germany releases Ifo Business Climate.

German manufacturing data continues to point upwards, and there was more good news on Thursday, as German Manufacturing PMI improved to 62.5, above the forecast of 60.4 points. This marked its highest level since 2010. Eurozone Manufacturing PMI also kept pace, climbing to 60.0, compared to an estimate of 58.3 points. Manufacturing sectors in Germany and the eurozone have been buoyed by an increase in global demand and stronger domestic consumption.

The ECB releases the minutes of the October policy meeting, and the markets will be looking for clues regarding future monetary policy. At the meeting, the ECB took the long-awaited step of tapering its asset-purchase program, announcing that monthly asset purchases would be cut from EUR 60 billion to EUR 30 billion. At the same time, the ECB extended the program to September 2018. The markets viewed this as a dovish statement, and if the minutes reinforce this view, the euro could lose ground.

With Germany in political paralysis, there are concerns whether this will affect the robust German economy. In the short-term, the economy should be able to weather the crisis, but future growth could be in jeopardy if the political deadlock continues. The euro and German stock markets have remained steady since the coalition talks fell apart last week, indicating that investors remain upbeat about the German economy.

AUDUSD – Recovery Faces Strong Headwinds from Trendline Resistance

Recovery rally from Tuesday's low at 0.7530 extends into third consecutive day and faces strong headwinds at 0.7540 zone. Resistance is provided by 20SMA/bear-trendline from 20 Sep 0.8102 peak and marks key obstacle for near-term recovery. Corrective action should be ideally capped here to keep underlying bears intact for fresh extension lower. Stronger signal of recovery stall would be generated on close below broken 10SMA (0.7602) and would turn focus towards targets at 0.7547 (20-d lower Bollinger band) and key 0.7530 support (21 Nov 5 1/2 month low). On the other side, sustained break above trendline resistance would signal recovery extension and expose 200 SMA at 0.7694.

Res: 0.7638; 0.7665; 0.7694; 0.7726

Sup: 0.7602; 0.7547; 0.7530; 0.7516

GBPUSD Bullish ABove 1.3307 Level

The British pound has moved sharply higher against the greenback, as the U.S dollar index falls to its weakest trading level in over a month, following the FOMC Meeting Minutes on Wednesday. The GBPUSD pair has traded as high as 1.3330 in intraday trading, before pulling back slightly to test overall demand around the 1.3300 handle. Earlier, GDP data showed that the UK grew at a pace of 0.4 percent in the third fiscal quarter, with annual GDP growth also coming in-line with initial estimates, at 1.5percent.

The GBPUSD pair remains intraday bullish while trading above the 1.3307 level, further upside towards 1.3360 and 1.3400 levels is now expected.

Any decline below the 1.3307 level, may see sellers push-price action back towards the 1.3268 and 1.3230 levels.

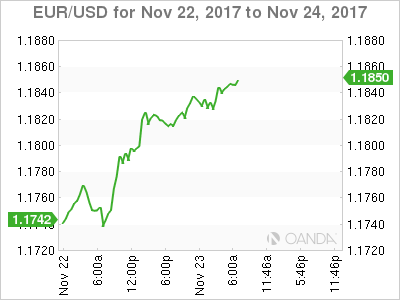

EURUSD Rally to Continue Above 1.1807

The euro continues to advance against the U.S dollar during the European trading session, hitting 1.1850, showing no signs of an imminent price-correction, following yesterday's strong upside rally. Price-action on the EURUSD pair currently trades at 1.1845, which is just below the former monthly high traders set at 1.1862. With markets in the United States being away for Thanksgiving holidays, traders now the look to the release of the Meeting Minutes from the European Central Bank's last policy meeting, as the main risk event on Thursday.

The EURUSD pair remains strongly bullish while trading above the 1.1807 technical level. Further upside towards the 1.1860 and 1.1910 levels appears increasingly likely.

Any decline below the 1.1807 level should spark an immediate sell-off towards the 1.1755 support region.

Gobble Gobble – Dollar In Trouble

Thursday November 23: Five things the markets are talking about

While investors believe the Fed will raise rates in December, many are trying to gauge how aggressively the central bank will tighten monetary policy next-year.

Yesterday's FOMC minutes showed that most Fed policy makers saw a near-term rate hike as appropriate. Some members were opposed citing weak inflation; with several others noted that a move was hinged on data. Most participants continued to think tighter labor markets would ultimately produce higher inflation

This 'dovish' sentiment is leading markets to reduce their expectations for interest rate increases next year. Growing consensus is beginning to expect only two rate increases in 2018, instead of the three hikes implied by the dot plot.

The dollar has steadied after tumbling yesterday in the wake of the more dovish sentiment. This may weigh further on the USD, especially if we start to see a broader correction develop in U.S rates markets.

Note: The U.S is out for Thanksgiving today, so liquidity is expected to be significantly lower into the weekend.

German politics continues to hog the spotlight, with the Social Democrats ready to talk with Chancellor Merkel and are prepared to offer her limited support for a fourth-term.

1. Stocks see red

The biggest slump in Chinese stocks in almost two-years is taking some of the shine off another record high in the global equity bull-run.

Tighter liquidity enforced by the Chinese government stepping up 'deleveraging'is causing the massive swings in Chinese asset classes.

Note: Japan was closed for a bank holiday.

Overnight in China, consumer and healthcare firms led the fall and dragged the CSI300 index down sharply by -2.93%, its biggest fall in percentage terms since June 2016. The broader Shanghai Composite Index lost -2.26%, its worst day since December.

In Hong Kong, stocks also ended sharply lower, pressured by the mainland's soured sentiment. The Hang Seng index fell -1.0%, while the China Enterprises Index lost -1.9%, to its lowest level in a month. Investors took profit in sectors including financials, IT and consumer goods.

In Europe, regional indices are trading off their lows, with most indices in the 'black' following strong PMI data in Europe where manufacturing PMI's registered a near 18-year high in the Eurozone (see below). Trading activity is light as the U.S markets are closed today.

Indices: Stoxx600 -0.2% at 386.5, FTSE -0.3% at 7397, DAX -0.1% at 13004, CAC-40 +0.2% at 5366, IBEX-35 +0.4% at 10058, FTSE MIB +0.3% at 22385, SMI flat at 9293, S&P 500 Futures flat

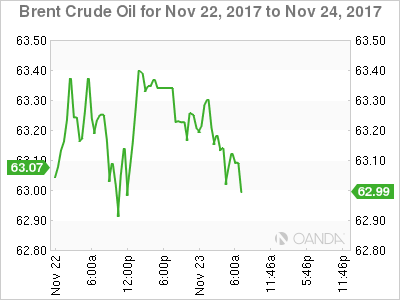

2. U.S oil prices ease from highs on oversupply worries, gold lower

U.S oil prices have eased back from their two-year high, as concerns about oversupply outweighed the impact of a pipeline shutdown in the U.S.

U.S light crude (WTI) is trading down -17c at +$57.85 a barrel, slipping from its highest level since mid-2015 reached yesterday of +$58.15. Brent crude is at +$62.98 per barrel, or down -34c from yesterday's close.

U.S crude had been boosted by the shutdown of the +590k bpd Keystone pipeline – it was closed last week due to an oil spill.

EIA data this week shows that U.S output has risen by +15% since mid-2016 to a record +9.66m bpd. The U.S, previously the world's biggest importer of crude oil, is now one of its biggest exporters, behind Russia and Saudi Arabia.

Note: OPEC meets next week, Nov. 30, to discuss policy, with Saudi Arabia lobbying for an extension to the cuts. However, Russia has sent mixed messages on its position, believing that cuts had hit its economy.

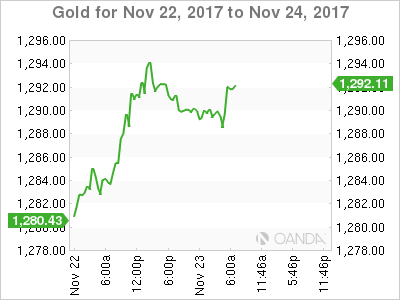

Gold prices are lower overnight, with investors taking profits after gains of nearly +1% in the previous session on weaker U.S data and concerns among some Fed members over lower inflation. Spot gold is down -0.2% at +$1,289.88 per ounce.

3. U.S yield curve steepens

While a move in December by the Fed to between +1.25% and +1.5% is still almost fully priced in, Fed fund futures are rallying to show rates at just +1.75% by the end of 2018.

The Fed's dovish turn yesterday has helped break the sell off in short-term U.S Treasuries, with yields on the two-year note falling almost -5 bps to +1.727% – the sharpest daily drop since early September.

Borrowing costs in the euro area are also creeping higher ahead of the ECB's October meeting minutes this morning (07:30 am EDT).

Germany's 10-year Bund yield has climbed less than +1 bps to +0.35%, while in the U.K the 10-year Gilt yield has decreased -1 bps to +1.263%, the lowest yield in more than two-weeks.

4. Dollar under pressure

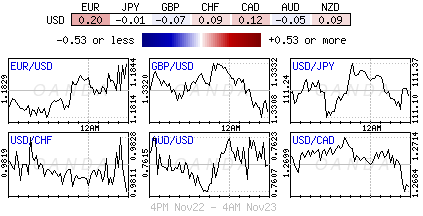

The EUR (€1.1841) and GBP (£1.3303) are trading well versus the USD, but this has been more to do with broader USD weakness in the aftermath of yesterday's FOMC minutes.

The EUR is further aided by much better manufacturing PMI data for France, Germany and the Eurozone. The data suggests that the regional economy is running on all cylinders. The pair tested a week high trading atop of €1.1850 area. If Germany can develop a 'grand coalition', should see the EUR benefit even further.

GBP/USD may see its eight-day winning streak come under pressure as Q3 Preliminary GDP came in-line with expectations (+0.4%) and showing a slowdown taking effect as the Brexit negotiation continue. GBP is a tad lower hovering ahead of support levels just below £1.3300 area.

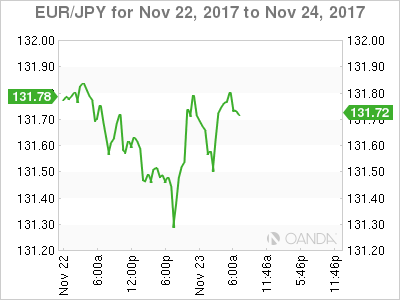

USD/JPY has posted a new two-month lows to test below ¥111.10 in the overnight session.

Dollar 'bears' believe that until there's considerable progress on U.S tax reform, the dollar is likely to stay pressured by a stronger EUR and rising Asian currencies.

5. Eurozone data point to strengthening recovery

Data this morning showed that the composite Purchasing Managers Index for the eurozone rose to 57.5 this month from 56.0 in October, reaching its highest level in more than six-years.

The strong print suggests the eurozone economy will grow at a quarter-to-quarter rate of +0.8% in the final three months of the year, which would mark a pickup from +0.6% in the three months through September.

France was the main source of surprise, recording its highest reading since the middle of 2011. That surge was led by its services sector.

Note: France's economy has been growing over half a percentage point a quarter for a year, fuelled by a strong recovery in business investment and steady consumer spending growth. Still, employment remains a weak spot in France's economic recovery.

Germany's stats Thursday also confirmed that its economy grew at a quarter-to-quarter rate of +0.8% in the three months through September, making it the strongest of the G7 developed countries in that period.

Market Update – European Session: Major European PMI Manufacturing Data Suggest The Regional Economy Is Running On All Cylinders

Notes/Observations

Major European Manufacturing PMI registers strong beats (Euro Zone near a 18-yer high with France and Germany at roughly 7-year highs to 6 ½ year highs

Pressure was growing within Germany's Social Democratic Party to at least discuss the possibility of forming a new government with Chancellor Merkel's conservatives

Europe:

EU official: Have seen willingness for UK PM May to act; hope she could deliver on key conditions but not clear what room she had for maneuver

German Finance Ministry Oct Monthly Report: indicators suggested upward economic trend to continue in the coming months

UK Citi/Yougov Nov 12-month inflation expectations: 2.6% v 2.8% prior

Americas:

FOMC Nov Minutes: Many policy makers saw near-term rate hike as appropriate. Some members were opposed citing weak inflation with several others noting that a move was hinged on data. Most participants continued to think tighter labor markets would ultimately produce higher inflation

Energy:

Venezuela Oil Min Del Pino: OPEC production cut extension should be agreed upon by consensus. Six OPEC ministers to informally discuss production cuts at meetings in Bolivia to help form consensus before OPEC meeting

Economic Data:

(DE) Germany Q3 Final GDP Q/Q: 0.8% v 0.8%e; Y/Y: 2.8% v 2.8%e; GDP NSA Y/Y: 2.3% v 2.3%e

(DE) Germany Q3 Private Consumption Q/Q: -0.1% v +0.2%e, Government Spending Q/Q: 0.0% v 0.2%e, Capital Investment Q/Q: 0.4% v 1.4%e, Construction Investment Q/Q: -0.4% v -0.3%e, Domestic Demand Q/Q: 0.4% v 0.6%e, Exports Q/Q: 1.7% v 1.0%e, Imports Q/Q: 0.9% v 0.8%e

(FR) France Nov Business Confidence: 111 v 109e; Manufacturing Confidence: 112 v 111e, Production Outlook: 31 v 33e, Own-Company Production: 16 v 17 prior

(TW) Taiwan Oct Industrial Production Y/Y: 2.9% v 4.0%e v

(FR) France Nov Preliminary Manufacturing PMI: 57.5 v 55.9e (14th month of expansion and highest since Apr 2011), Services PMI: 60.2 v 57.0e, Composite PMI: 60.1 v 57.2e

(DE) Germany Nov Preliminary Manufacturing PMI: 62.5 v 60.4e (36th month of expansion and highest since Feb 2011), Services PMI: 54.9 v 55.0e, Composite PMI: 57.6 v 56.7e

(GR) ECB lowers emergency liquidity assistance (ELA) cap for Greece banks from €26.9B to €25.8B

(EU) Euro Zone Nov Preliminary Manufacturing PMI: 60.0 v 58.2e; (52nd month of expansion and highest since Apr 2000), Services PMI: 56.2 v 55.2e, Composite PMI: 57.6 v 56.0e

(UK) Q3 Preliminary GDP (2nd reading) Q/Q: 0.4% v 0.4%e; Y/Y: 1.5% v 1.5%e

(UK) Q3 Preliminary Private Consumption Q/Q: 0.6% v 0.4%e; Govt spending Q/Q: 0.3% v 0.3%e; Gross Fixed Capital Formation Q/Q: 0.2% v 0.4%e; Exports Q/Q: -0.7% v -0.7%e; Imports Q/Q: 1.1% v 0.9%e

(UK) Q3 Preliminary Total Business Investment Q/Q: 0.2% v 0.3%e; Y/Y: 1.3% v 1.4%e

Fixed Income Issuance:

(SE) Sweden sold SEK500M vs. SEK500M indicated in I/L 2027 Bonds; Avg Yield: -1.1900% v -1.1505% prior; Bid-to-cover: 5.49x v 2.09x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.2% at 386.5, FTSE -0.3% at 7397, DAX -0.1% at 13004, CAC-40 +0.2% at 5366, IBEX-35 +0.4% at 10058, FTSE MIB +0.3% at 22385, SMI flat at 9293, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices trade off the lower with most indices in the green, following strong PMI data in Europe where Manufacturing PMI registered a near 18 year high in the Eurozone.

Trading acitivity has been light as the US markets are closed today in observance of Thanks Giving Holiday.

In the UK Centrica trades sharply lower after warning Full year EPS will be below views, while Telit Comms trades over 10% lower after warnings on profits. In Germany ThyssenKrupp reported positive Full year results, while Remy Cointreau trades lower in France after slightly missing estimates.

On the M&A front Servelec trades higher after receiving a takeover offer, while Fingerprint Cards trades sharply higher after bid talk.

Equities

Consumer discretionary [ Mothercare [MTC.UK] -15% (Earnings) , Rovio [ROVIO.FI] -19% (Earnings), Remy Cointreau [RCO.FR] -2.8% (Earnings)]

Industrials: [ThyssenKrupp [TKA.DE] +1.3% (Earnings)]

Financials: [CMC Markets [CMCX.UK] +6.6% (Earnings)]

Technology: [Fingerprint Cards [FINGB.SE] +21% (Reports Beijing Watertek Information Tech preparing offer) , Servelec [SERV.UK] +20% (Receives takover offer) ]

Telecom: [Telit Communications [TCM] -12.7% (Profit warning)]

Energy: [Centrica [CNA.UK] -15.5% (FY17 adj EPS below views)]

Speakers

EU Commissioner Moscovici calls for a credible tax haven list from EU ministers by Dec 5th

Reports circulating that German SPD leader Schultz could resign in near future (as soon as today)

Italy Economy Min Podoan: 2017 GDP growth could exceed 1.5%, recovery seen sustainable in 2018-2019 period

Norway oil and gas investment survey: 2018 gas and investment seen at NOK144.3B v NOK141.7B prior view (Aug).

Norway Central Bank (Norges) Q4 Household Expectation Survey raised its 12-month expectations from 2.6% to 2.9% and maintained thes 2-3-year inflation outlook at 3.2%

Turkey President Chief Adviser Ertem: Central bank is not targeting foreign exchange; would not ‘drift to crisis’ with ‘FX attacks. Central bank had instrumental independence and free to take any step it saw necessary; could break the hands of speculators

Turkey President senior advisor Karahan: Central would tighten policy whenever it needed too. President Erdogan was sensitive about inflation and wanted it lower

Poland Dep PM Gowin: Opposition no-confidence vote could delay Cabinet reshuffle into Jan

Currencies

The USD maintained a soft tone in the aftermath of the Nov FOMC minutes which showed that some policymakers were unsure about raising interest rates due to low inflation

EUR/USD was further aided by much better Manufacturing PMI data for France, Germany and the Euro Zone. The data suggesting that the regional economy was running on all cylinders. The pair tested a 1-week high near 1.1850 area.

GBP/USD saw its 8-day winning streak under pressure as Q3 Preliminary GDP came in-line with expectations and showing a slowdown taking effect as the Brexit negotiation continued. GBP/USD lower by 0.1% and hovering around the 1.33 area.

USD/JPY posted 2-month lows to test below 111.10 in the session.

Fixed Income

Bund futures trade up 2 ticks at 163.00 despite strong PMI data out of Europe. Trading remains quiet with upside targeting 163.30 initially followed by 163.40. Downside sees analysts targeting 162.88 then 162.61.

Thursday's liquidity report showed Wednesday Excess liquidity rose to €1.835T from €1.832T prior. Use of the marginal lending facility increased to €291M from €284M prior.

Looking Ahead

(AR) Argentina Nov Consumer Confidence: No est v 51.1 prior

(BR) Brazil Nov CNI Industrial Confidence: No est v 56.0 prior

05:30 (HU) Hungary Debt Agency (AKK) to sell Bonds (3 tranches)

05:30 (PL) Poland to Sell Bonds

06:00 (UK) Nov CBI Retailing Reported Sales: +3e v -36 prior; Total Distribution: No est v 1 prior

06:00 (BR) Brazil Mid-Nov IBGE Inflation IPCA-15 M/M: 0.4%e v 0.3% prior; Y/Y: 2.8%e v 2.7% prior

06:00 (IL) Israel Oct Unemployment Rate: No est v 4.1% prior

06:00 (RO) Romania to sell 12-month Bills; Avg Yield: % v 0.79% prior

06:45 (US) Daily Libor Fixing

07:00 (FR) ECB’s Villeroy (France) in London

07:00 (HU) Hungary Premier Chief of Staff Lazar

07:30 (EU) ECB account of the monetary policy meeting (Nov Minutes)

07:30 (BR) Brazil Oct Current Account: -$0.9Be v +$0.4B prior; Foreign Direct Investment (FDI): $7.0Be v $6.3B prior

08:00 (ZA) South Africa Central Bank (SARB) Interest Rate Decision: Expected to leave Interest Rate unchanged at 6.75%

08:00 (PL) Poland Central Bank (NBP) Nov Minutes

08:00 (PL) Poland Oct M3 Money Supply M/M: 0.7%e v 0.5% prior; Y/Y: 5.5%e v 5.4% prior

08:00 (RU) Russia Gold and Forex Reserve w/e Nov 17th: No est v $426.4B prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Sept Retail Sales M/M: +1.0%e v -0.3% prior; Retail Sales Ex Auto M/M: +1.0%e v -0.7% prior

09:00 (BE) Belgium Nov Business Confidence: 0.8e v 0.5 prior

09:00 (MX) Mexico Sept Retail Sales M/M: 0.2%e v 0.2% prior; Y/Y: +0.8%e v -0.2% prior

09:00 (BR) Brazil to sell Fixed Rate 2023 and 2027 Bonds

09:00 (BR) Brazil to sell 2018, 2019 and 2021 LTN Bills

10:00 (MX) Mexico Central Bank (Banxico) Nov Minutes

11:30 (CH) SNB President Jordan speaks in Basel

13:00 ECB’s Coeure (France) in Paris

13:30 (FR) ECB’s Villeroy (France) at London School of Economics

14:00 (AR) Argentina Sept Economic Activity Index (Monthly GDP) M/M: No est v 0.3% prior; Y/Y: 4.5%e v 4.3% prior

14:00 (AR) Argentina Oct Trade Balance: -$0.7Be v -$0.8B prior

16:00 (KR) South Korea Nov Consumer Confidence: No est v 109.2 prior

16:45 (NZ) New Zealand Oct Trade Balance (NZD): -0.8Be v -1.1B prior

19:30 (JP) Japan Nov Preliminary Manufacturing PMI: No est v 52.8 prior

20:10 (JP) BOJ Outright Bond Purchase 10~25 Years; over 25 Years~

23:00 (MY) Malaysia Oct CPI Y/Y: 4.1%e v 4.3% prior

Euro Slightly Higher On Sharp Manufacturing PMIs

The euro has posted slight gains in the Wednesday session. Currently, EUR/USD is trading at 1.1844, up 0.18% on the day. On the release front, German Final GDP accelerated to 0.8%, matching the forecast. German and Eurozone Manufacturing PMIs beat their estimates, with readings of 62.5 and 60.0, respectively. Later in the day, the ECB releases the minutes of its October policy meeting. US banks are closed for the Thanksgiving holiday, and there are no US events on the schedule. On Friday, Germany releases Ifo Business Climate.

The political deadlock continues in Germany, as President Angela Merkel faces her toughest challenge since coming to power 12 years ago. With the Free Democratic Party pulling out of coalition talks on the weekend, Merkel appears unable to form a coalition government. Merkel has said she would rather hold another election than try to govern with a shaky minority government. President Frank-Walter Steinmeier has urged the parties to redouble their efforts in order to reach an agreement, warning that another election would cause uncertainty in German as well as Europe. The crisis in the eurozone’s largest economy could paralyze the European Union, as Merkel has become the unofficial leader of the bloc. Euro-supporters such as French President Emmanuel Macron have ambitious plans to strengthen European integration, but this will have to wait until Merkel can straighten out her domestic challenges.

With Germany in political paralysis, there are concerns whether this will effect the robust German economy. In the short-term, the economy should be able to weather the crisis, but future growth could be in jeopardy if the political deadlock continues. The euro and German stock markets have remained steady since the coalition talks fell apart last week, indicating that investors remain upbeat about the German economy. There was positive news on Thursday, as German Manufacturing PMI improved to 62.5, above the forecast of 60.4 points. This marked its highest level since 2010. Eurozone Manufacturing PMI also kept pace, climbing to 60.0, compared to an estimate of 58.3 points. The strong numbers point to strong manufacturing sectors in Germany and the eurozone, which have been boosted by an increase in global demand and stronger domestic consumption.

NZD/CHF 1H Chart: Kiwi Tests Two Channels

NZD/CHF is currently trading in three channels. The senior one was formed mid-September, while the other two emerged only in November. The Kiwi bounced off the senior channel circa 0.6710 last week and has since entered a slight consolidation period. The current situation shows that the rate is testing the boundaries of two opposing patterns which are likewise reinforced by the 55– and 100-hour SMAs. Thus, two scenarios are possible. In case the bearish momentum prevails, the Kiwi should edge lower but with limited momentum, as the senior pattern and the weekly S1 are likely to restrict this currency circa 0.6680. The pair might subsequently trade sideways prior to a period of appreciation. Conversely, the medium pattern might be breached already in this session; however, sharp increase could be hindered by the weekly PP and the 200-hour SMA circa 0.6790. A surge is likely to follow.