Sample Category Title

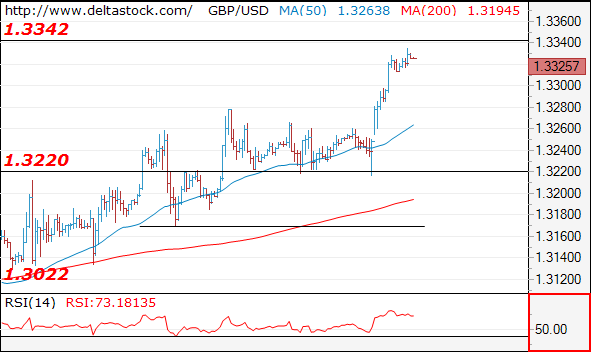

Cable Breaks Significant Resistance At 1.3280

Key Highlights

- The British Pound traded higher recently and broke the 1.3280 resistance against the US Dollar.

- There was a break above two crucial bearish trend lines with resistance near 1.3280 on the 4-hours chart of GBP/USD.

- The US Durable Goods Orders in Oct 2017 declined 1.2% whereas the market was looking for a 0.3% rise.

- The UK GDP figure for Q3 2017 will be released today, which is forecasted to increase by 0.4% (QoQ).

GBPUSD Technical Analysis

The British Pound after forming a base near 1.3100 against the US Dollar started an upside move. The GBP/USD pair broke a key resistance near 1.3280 to set the pace for more gains.

The pair is now well above 1.3250 and the 100 simple moving average (red, 4-hour), signaling an uptrend. During the recent upside move, there was a break above two crucial bearish trend lines with resistance near 1.3280 on the 4-hours chart.

The pair is currently trading around the last swing high of 1.3320. It might continue to move higher and trade towards the 1.236 extension of the last decline from the 1.3320 high to 1.3041 low at 1.3386.

On the downside, the broken resistance at 1.3280 is now a decent support in the short term.

US Durable Goods Orders

Recently in the US, the Durable Goods Orders report for Oct 2017 was released by the US Census Bureau. The forecast was slated for a rise of 0.3% in the Durable Goods Orders compared with the last increase of 2.2%.

However, the actual result was disappointing, as there was a decline of 1.2% in orders in Oct 2017. The last reading was revised to 2.2%. Moreover, the Durable Goods Orders ex Transportation were up by 0.4%, but less than the forecast of +0.5%.

The report added that:

New orders for manufactured durable goods in October decreased $2.8 billion or 1.2 percent to $236.0 billion. Excluding defense, new orders decreased 0.8 percent. Transportation equipment, also down following two consecutive monthly increases, drove the decrease, $3.5 billion or 4.3 percent to $77.1 billion.

Economic Releases to Watch Today

Germany's Manufacturing PMI for Nov 2017 (Preliminary) – Forecast 60.4, versus 60.6 previous.

Germany's Services PMI for Nov 2017 (Preliminary) – Forecast 55.0, versus 54.7 previous.

Euro Zone Manufacturing PMI Nov 2017 (Preliminary) – Forecast 58.3, versus 58.5 previous.

Euro Zone Services PMI for Nov 2017 (Preliminary) – Forecast 55.1, versus 55.0 previous.

UK GDP for Q3 2017 (QoQ) – Forecast +0.4% versus +0.4% previous.

Canadian Retail Sales Sep 2017 (MoM) – Forecast +0.9%, versus -0.3% previous.

Canadian Retail Sales ex Autos Sep 2017 (MoM) – Forecast +1.0%, versus -0.7% previous.

USD Also Weakened Pushing EUR/USD Above 1.18 Again

Market movers today

Yesterday we published a presentation on the Swedish housing market: What if Swedish house prices dropped 15-20%? While SEK has adjusted we believe Swedish rates have yet to adjust to the weaker housing market in Sweden.

In the euro area the PMI figures for November are due for release. Manufacturing PMI rose steadily throughout 2017 and reached 58.5 in October from 58.1 in September. It is now st rikingly close to the 59.0 post -crisis peak reached in February 2011. While survey expectat ions indicators point towards further increases with rising consumer confidence and high Ifo and ZEW expectat ions, we expect only a moderate increase as the euro appreciation in 2017 could have started to act as a drag on export orders. Thus, we expect manufacturing PMI to increase to 58.7 and service PMI to increase to 55.2.

The ECB minutes from the October meet ing are also due for release today. At the October meet ing, the ECB extended its QE programme for another nine months in 2018 but scaled down the monthly purchases to EUR30bn (see also ECB Review: ECB opts for ‘lower-forlonger’ QE extension, 26 October). In the minutes, focus will be on the Governing Council's discussions regarding whether to put a definite end date to the QE programme, which might give insights regarding the likelihood of a possible tapering start ing in Q4 18.

In addit ion, German revised Q3 GDP are due for release today.

In Norway the Q4 oil investment survey could t urn out t o be t he week's most important release.

Selected market news

US bond markets rallied strongly last night following dovish minutes from the latest FOMC meet ing. The USD also weakened pushing EUR/USD above 1.18 again. The minutes revealed that the Fed is on t rack to deliver the third hike this year at its meeting next month. However, the minutes were a bi t dovi sh in th e sense th at 'several' FOMC participants are becoming increasingly concerned about inflation running below 2% target, which, in our view, is a dovish signal that the Fed might not hike as much as they indicate themselves (3 hikes). We st ick to our view that the Fed is going to deliver two hikes next year although uncertainty is high given that we get a completely new FOMC next year with new Chair and new members. The FOMC members cont ribute the lower-than-expected inflat ion to a flat ter Phillips curve, more slack left in the labour market and possibly also lower inflat ion expectations (we have argued for the lat ter for a while).

In China the crackdown on shadow banking and renewed deleveraging push continues to hi t the bond market. Corporate bond yields (AAA) yesterday rose to the highest level in three years and is now up more than 200bp since late 2016. The fight on financial risks is posit ive in the long run but poses short term downside risk to Chinese growth.

Euro consumer confidence (released yesterday afternoon) rose to the highest level since 2000 point ing to cont inued strong private consumption growth.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

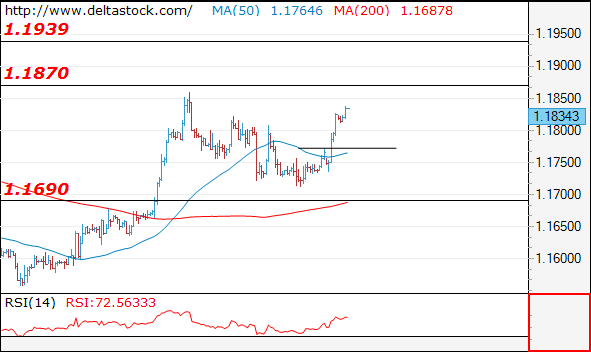

EUR/USD

Current level - 1.1834

The rise above 1.1806 high shows a completion of the whole slide from 1.1860 and the intraday bias is positive above 1.1770, for a continuation towards 1.1870 and 1.1940.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1870 | 1.1940 | 1.1770 | 1.1690 |

| 1.1940 | 1.2090 | 1.1690 | 1.1550 |

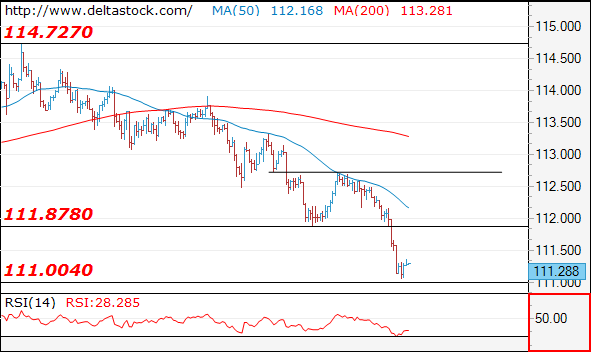

USD/JPY

Current level - 111.28

The sell-off has reached 111.00 support area and the latter is expected to provoke a rebound towards 111.90 intraday resistance. Crucial on the upside is 112.70 and only a violation of that area will signal a reversal of the slide from 114.70.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 111.90 | 112.70 | 111.00 | 109.50 |

| 112.70 | 114.70 | 109.50 | 107.30 |

GBP/USD

Current level - 1.3325

The rise here has reached the resistance at 1.3340 and the overall bias remains positive, with an initial support at 1.3280 and crucial low at 1.3220. My outlook is rather counter-trend, for a reversal and slide towards 1.3220. Next major resistance beyond 1.3340 is 1.3460.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3340 | 1.3340 | 1.3280 | 1.3220 |

| 1.3460 | 1.3460 | 1.3220 | 1.3020 |

UK GDP Figures Eyed As Growth Forecasts Take A Hit

- DAX Set to Underperform Again as Political Uncertainty Weighs;

- Revised UK GDP Figures Eyed as OBR Lowers Forecasts;

- ECB Accounts and Eurozone PMIs Also in Focus.

DAX Set to Underperform Again as Political Uncertainty Weighs

European equity markets are poised to open a little lower on Thursday, with the DAX underperforming its peers as political uncertainty weighs on the German index.

Germany has been the one area of stability in the eurozone since the global financial crisis, even when the region appeared on the brink of collapse but it would appear it has come at a cost. Chancellor Angela Merkel has been striving to form a “Jamaica coalition” with the Greens and the FDP since the election but this appeared to fall apart at the weekend.

The SPD has insisted that it would prefer to go into opposition rather than form another grand coalition with Merkel's party, with the previous partnership appearing to have come at a political cost. This leaves Merkel with few options in the absence of a change of heart from the other parties, increasing the probability of another election and more uncertainty. This appeared to weigh on the DAX late on Wednesday and looks to be doing the same ahead of the open this morning.

While the European session itself won't be particularly quiet with plenty of economic data being released throughout the morning, the Thanksgiving holiday in the US will likely have a significant impact on trading volumes and make for a quieter afternoon session.

Revised UK GDP Figures Eyed as OBR Lowers Forecasts

The ONS will release second quarter GDP data for the UK this morning, which is expected to be unrevised from last month's preliminary reading of 1.5%. If the OBR's forecasts – as revealed by Chancellor Philip Hammond in yesterday's Autumn – are to be believed, we should get used to only moderate growth in the coming years, with significant downward revisions being driven by lower productivity and business investment.

ECB Accounts and Eurozone PMIs Also in Focus

We'll also get manufacturing and services PMIs this morning from the eurozone, Germany and France, as well as the accounts from the last ECB meeting, at which policy makers agreed to halve and extend the asset purchase program by nine months. I don't expect much from the minutes though as the move was fully priced in at the time and there's unlikely to be significant clues about the next step, even if it would currently appear to be quite obvious.

Market Update – Asian Session: Markets Quiet With Holidays In Japan And US

Headlines/Economic Data

General Themes: Asian equity markets trade mixed amid thin trading conditions on US and Japan holidays

Energy and Materials sectors add on to Wednesday’s gains

Looking ahead: US markets closed for Thanksgiving holiday

Japan

Tokyo Stock Exchange closed in observance of Labour Thanksgiving Day

Nikkei 225 Futures -0.2%

USD/JPY consolidates losses seen following FOMC minutes

(JP) Japan metalworkers to push for a ¥3,000 ($26.90) minimum increase in monthly base pay for the 5th straight year – Nikkei

(JP) Japan said to be ready to start debate on Constitution reform - financial press

Looking Ahead: Japan prelim Nov Man PMI due to be released on Friday

Korea

Kospi opened flat and has since moved lower: LG Electronics -1.4%, Samsung Electronics -1.1%, Hynix -2% (tracks declines in US chipmakers)

Korean Won (KRW) opened at over 2 year highs versus US dollar; has since pared gains

South Korea FX Official: Some offshore speculators are failing to notice government's willingness to stabilize financial markets

South Korea Q3 Short Term External Debt: $119.8B v $117.3B prior; Debt/FX reserves ratio 31.1% v 30.8% prior

Geopolitics: North Korea Foreign Ministry: US designation deemed a severe provocation (responds to move by US to name the country a state sponsor of terrorism)

South Korea and China to cooperate on stopping North Korea provocation – South Korea Press

China/Hong Kong

Hang Seng opened +0.1%; Materials Index +3% (Chalco +7%)

Shanghai Composite opened -0.2% and has extended losses led by appliance makers and wine cos; while banks outperform even with continued talk on tighter regulations; Small-cap Chinext index -1.5%

Automakers trade mixed: China may reduce EV subsidies by 20% in 2018 versus originally plan for 2019 – Chinese Press

Nexgo [300130.CN] cancels planned micro loan unit following suspension of approval by China government – US financial press

(CN) China Banking Regulatory Commission (CBRC) official calling for stricter monetary management - Chinese press

(CN) S&P: China's wealth product rules are game changing and could be a break to credit

(CN) China planning to set up a more than CNY100B fund for support to mixed-ownership reform of State Owned Enterprises (SOE) - Chinese press

(CN) PBOC Deputy Gov Fan Yife; Financing difficulties remain for some small technology companies - China press

Shorter-term Offshore yuan money market rates ease after Wednesday’s rise: (HK) Offshore yuan Overnight HIBOR rate -3.22ppts to 2.75967%; 1-week HIBOR -47bps to 4.52286

(CN) PBoC OMO: Injects CNY270B v CNY190B injected in 7,14 and 63-day reverse repos prior; Net injects CNY100B v CNY0B prior

Offshore Yuan (CNH) +0.1%

(CN) PBoC sets yuan reference rate at 6.6021 v 6.6290 prior (strongest level since Oct 18th)

Australia/New Zealand

S&P ASX 200 opened -0.1%, closed flat; Utilities index -0.9% (follow-through selling) Consumer Discretionary Index -0.6%; Resources Index +0.8%

TAP.AU Issues letter to shareholder regarding Risco – filing; -20%

ASX 200 Financials Index -0.4%: Australia Treasurer Morrison summoned the chairs of the big banks to a series of urgent meetings; banks have said they will hold their opposition to in inquiry - Australian press

NZX 50 closes flat

Aussie and Kiwi slightly lower during session

(NZ) NEW ZEALAND Q3 RETAIL SALES (EX-INFLATION) Q/Q: 0.2% V 0.1%E (smallest gain since Q2 2015); Y/Y: 5.4% V 5.1%E

(AU) JPMorgan: In 2018, the Australia/US 10-year bond yield spread may turn negative

(AU) Moody’s: Sees stable outlook for corporates in Australia in 2018; Sees moderate levels of debt maturities over the next 18 months

(AU) Australia sells A$500M in Feb 2018 notes, avg yield 1.7244%, bid to cover 4.46x

(AU) Australia sells A$394.5M in RMBS at auction (resumed as of today)

(NZ) New Zealand sells NZ$150M in 3.5% 2033 bonds, avg yield 3.1338%, implied bid to cover 2.48x

(NZ) New Zealand Former Labour Finance Minister will head group to consider changes that would improve the structure, fairness and balance of the tax system

(NZ) New Zealand immigration minister wants to tighten work visa rules - NZ press

Looking ahead: New Zealand Oct Trade Balance due for release on Friday.

Australia to sell A$500M in 2.00% Dec 2021 bonds

Other Asia

Singapore

Straits Times Index opened +0.3%; has since pared gains

Q3 GDP revised higher: SINGAPORE Q3 FINAL GDP Q/Q: 8.8% V 7.8%E; Y/Y: 5.2% V 5.0%E

Singapore sees 2018 GDP growth slowing to 1.5-3.5%, while 3.0-3.5% is expected for 2017

Singapore Central Bank (MAS) official: 2017 monetary policy remains appropriate

SINGAPORE OCT CPI M/M: -0.3% V -0.1%E; Y/Y: 0.4% V 0.5%E; Core CPI Y/Y: 1.5% v 1.5%e

North America

US equities closed mostly lower: Dow -0.3%, SP500 -0.1%, Nasdaq +0.1%, Russell2000 -0.1%

S&P500 Financial Sector -0.5%

(US) FOMC MINUTES FROM NOV 1 MEETING: MANY FED POLICYMAKERS SAW NEAR-TERM RATE HIKE AS WARRANTED; SOME OPPOSED NEAR-TERM HIKE DUE TO WEAK INFLATION; A few Fed officials concerned hikes would undermine credibility; Several on Fed concerned about low inflation expectations

US Treasury yields ended lower amid release of FOMC minutes

(US) DOE CRUDE: -1.9M V -1.5ME

M&A: 21st Century Fox (FOXA) said to remain engaged in prelim talks with suitors including Comcast and Disney; Broadcom (BRCM) reportedly considering higher offer for Qualcomm (QCOM) by offering more shares (press); Davita (DVA) said to consider sale of medical group unit which might be valued at ~$4B (press);

Looking Ahead: NYSE is closed on Thursday in observance of Thanksgiving holiday. An early close (at 13:00 GMT) is seen for Friday;

Canada Sept Retail Sales to be released later today

Europe

(DE) Germany Oct Tax Rev +0.5% y/y, suggesting continued economic expansion – Ministry

(EU) EU's Tusk: EU needs to discuss how to move forward with a banking union; Euro summit on Euro zone future will go ahead as planned

(DK) Denmark PM Rasmussen’s Liberal Party suffered losses in local elections – financial press

Looking ahead: Second readings of Q3 GDP expected out of Germany and the UK; European Nov prelim PMI data; ECB Account of Monetary Policy Meeting

Levels as of 01:00ET

Nikkei closed, Hang Seng +0.1%; Shanghai Composite -1.1%; ASX200 +0.6%, Kospi +0.0%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.0%, Dax -1.5%; FTSE100 +0.0%

EUR 1.1838-1.1813; JPY 111.38-111.07; AUD 0.7623-0.7604;NZD 0.6884-0.6867

Dec Gold -0.2% at $1,289/oz; Jan Crude Oil -0.2% at $57.88/brl; Dec Copper +0.0% at $3.14/lb

Aussie Trading A Tad Lower In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.51% against the USD and closed at 0.7617.

LME Copper prices rose 0.7% or $44.5/MT to $6872.5/MT. Aluminium prices rose 1.1% or $23.0/MT to $2085.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7616, with the AUD trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7573, and a fall through could take it to the next support level of 0.7529. The pair is expected to find its first resistance at 0.7642, and a rise through could take it to the next resistance level of 0.7667.

With no macroeconomic releases in Australia today, investor sentiment would be determined by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Consumer Confidence Jumped To Its Highest Since 2001 In November

For the 24 hours to 23:00 GMT, the EUR rose 0.72% against the USD and closed at 1.1821, after a reading on the Euro-zone consumer sentiment came in better-than-expected in November.

Data showed that the Euro-zone's preliminary consumer confidence index advanced to a level of 0.1 in November, jumping back into the positive territory and surging to a nearly 17-year high level, suggesting that upbeat growth prospects across the Euro-area are further lightening the region's consumer morale.

The index had recorded a reading of -1.0 in the previous month, while investors had envisaged for a rise to a level of -0.8.

The US Dollar fell against most of the major currencies, after minutes of the Federal Reserve's (Fed) November meeting revealed lingering concerns over tepid US inflation.

According to minutes, officials proffered an upbeat assessment on the US economy and indicated that an increase in interest rates would be warranted “in the near term”. However, policymakers had some disagreements on the pace of inflation as many felt that tightness in the labour market would likely fuel higher inflation in the medium term while others expressed concerns over the inflation outlook. Also, board members fretted that asset prices are out of balance and could pose a threat to the economy.

Macroeconomic data released in the US showed that preliminary durable goods orders unexpectedly dropped 1.2% in October, after three straight months of strong gains, pulled down by declining orders for commercial aircraft. Market participants had anticipated durable goods orders to rise 0.3%, after advancing 2.0% in the previous month. Moreover, the nation's final Reuters/Michigan consumer sentiment index declined to a level of 98.5 in November, while the preliminary figures had indicated a drop to a level of 97.8. The index had registered a level of 100.7 in the previous month.

Other data revealed that initial jobless claims in the US eased to a level of 239.0K in the week ended 18 November, more than market expectations for a fall to a level of 240.0K. In the prior week, initial jobless claims had registered a revised level of 252.0K. Additionally, the nation's MBA mortgage applications registered a rise of 0.1% in the week ended 17 November, following a gain of 3.1% in the previous week.

In the Asian session, at GMT0400, the pair is trading at 1.1834, with the EUR trading 0.11% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1767, and a fall through could take it to the next support level of 1.1699. The pair is expected to find its first resistance at 1.1870, and a rise through could take it to the next resistance level of 1.1905.

Trading trend in the Euro today is expected to be determined by the release of minutes of the European Central Bank's recent meeting, due later in the day. Moreover, investors would keenly monitor the flash Markit manufacturing and services PMIs for November across the Euro-zone.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

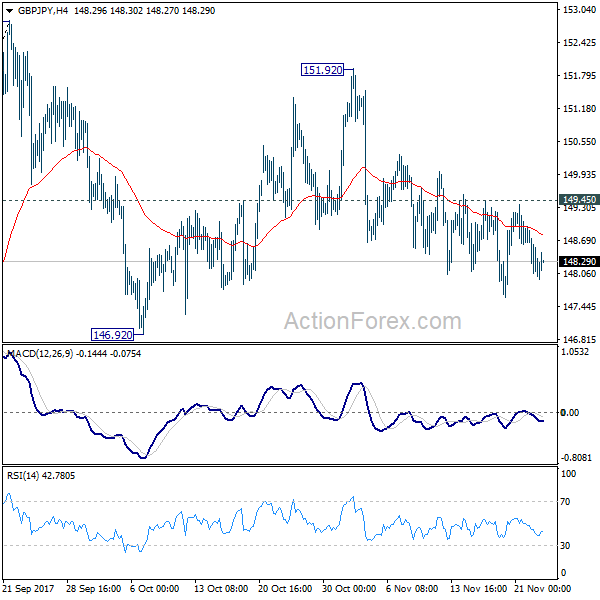

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.80; (P) 148.37; (R1) 148.75; More...

With 149.45 minor resistance intact, deeper fall is mildly in favor in GBP/JPY. Corrective pattern from 152.82 is still in progress and could extend through 146.92 support. But we'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, break of 149.45 minor resistance will turn bias back to the upside for 151.92/152.82 resistance zone.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

British Government Slashes Growth Projections, Sets Aside £3.0 Billion For Brexit: Autumn Budget

For the 24 hours to 23:00 GMT, the GBP rose 0.66% against the USD and closed at 1.3326.

Yesterday, the British Finance Minister, Philip Hammond, in his Autumn Statement announced that the Office for Budget Responsibility (OBR) downgraded UK’s economic growth outlook and anticipated that the nation will need to borrow sharply over the coming years.

The OBR now expects the economy to post a growth of just 1.5% this year before slipping to 1.4% in 2018, revised down from a previous estimate of 2.0% and 1.6%, respectively. Further, Hammond vowed to set aside £3.0 billion over the next two years for Brexit contingency plans.

In the Asian session, at GMT0400, the pair is trading at 1.3330, with the GBP trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3250, and a fall through could take it to the next support level of 1.3171. The pair is expected to find its first resistance at 1.3373, and a rise through could take it to the next resistance level of 1.3417.

Moving ahead, market participants would draw their attention towards the release of UK’s flash 3Q GDP numbers, to gauge the strength in the British economy.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 1.1% against the JPY and closed at 111.20.

In the Asian session, at GMT0400, the pair is trading at 111.31, with the USD trading 0.1% higher against the JPY from yesterday’s close.

The pair is expected to find support at 110.80, and a fall through could take it to the next support level of 110.30. The pair is expected to find its first resistance at 112.08, and a rise through could take it to the next resistance level of 112.86.

As Japanese markets are closed on account of public holiday, Yen investors would focus on global macroeconomic releases for further direction.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.