Sample Category Title

Aussie Dollar Flash

Aussie Dollar Flash

Seller exhaustion was apparent in the lead up to the FOMC minutes, as shorts continued to unwind. While selling pressure has re-emerged this morning at .7620-.7625, one does get the sense that the FOMC minutes was the last kick of can for the Aussie bears heading into 2018. And given the dovish Fed overtones, for those fortunate to have been riding shorts since the convincing downtrend emerged in mid-Sept, traders will now be more inclined to cover shorts which should temper any near-term downside momentum. And while commodity correlations have weakened of late, Dalian Iron ore is up over 3.5 %, as the Pboc continues to inject cash in an attempt fine-tune their deleveraging act, it still underpins the Aussie dollar sentiment to a degree.

FOMC Participants’ Positive Economic Assessment Reaffirms the Case for a December Hike

The minutes of the Federal Open Market Committee's (FOMC) last meeting showed participants looking through the temporary impact of hurricanes, with many seeing "the economy... operating at or above full employment."

Some participants continue to fret about the persistence of weak inflation and worry that ongoing Fed tightening whilst inflation is below target could push inflation expectations down further and make the target harder to achieve.

Interestingly, a few participants considered whether the Fed should adjust its framework for achieving stable inflation to something akin to a price level target, requiring periods of weak inflation to be followed by stronger inflation in order to keep the overall price level growing at around 2%.

Finally, the minutes emphasized FOMC members' satisfaction with the balance sheet normalization program. Further, "members generally agreed that the statement following this meeting needed to contain only a brief reference to the program and that subsequent statements might not need to mention the program."

Key Implications

With economic data showing a firming in growth through the latter half of 2017 and potentially the longest string of quarterly growth over 3% (annualized) since 2004/2005, a December rate hike is close to a sure thing.

The debate continues to rage amongst Fed participants around when and if inflation will move toward target. Participants' willingness to discuss other possible frameworks toward inflation shows that they are taking recent misses seriously and will react to further deviations from their goal.

Including Janet Yellen's resignation, there are now four Federal Reserve board of governor seats up for grabs. This has the potential to dramatically change the tone and composition of the Federal Reserve and the future course of monetary policy and should be watched closely by investors.

In Yellen We Trust

In Yellen we trust

The market spent the better part of Wednesday paring back USD exposure ahead of the FOMC minutes after Dr Yellen soft pedalled the reflation rhetoric all but signalling to the markets that absentee US inflation remains a substantial concern amongst Fed members. This year the Fed’s top dogs have time and time gain restated their confidence that inflation will revive despite their preferred price measure slipping to 1.3 percent, well below the 2-percent target. But this morning release of FOMC October minutes indicates the board’s ship is listing towards inflation concerns or the lack thereof to be more specific.

Speaking of listing ships, the USD price action is echoing the Markets concerns over inflation. But frankly, the minutes did little more than embody what we’ve heard in recent Fedspeak. However the statement does clear the air of one raging debate, and that’s 2018 rate hikes unambiguously depend more pressingly on inflation than on growth.This apparent shift suggests policy normalisation may be less perceptive to US economic performance than the dollar bulls were anticipating.

Despite the fact that the dollar sold off rather aggressively overnight, APAC currency markets have a ” gone fishing ” feel this morning exhibiting few concerns about the slide. However, with few looking to press the USD issue one way or another, the markets have that distinct holiday feel about them.

Not to sound like the eternal USD bull, I can’t help but think the Feds are looking over their shoulder concerned that if asset prices keep going higher the fear of the asset bubble eruption my outweigh concern about inflation.

Speaking of which, US equity markets to continue to surge reaching Amazonian proportions. The high tech-laden Nasdaq notched out another record high after Amazon share rose 1 % after a deal with their cloud-based unit and Cerner was inked. But Wall Street closed mixed in a low volume day. The Dow Jones Industrial Average and the S&P 500 were a tad softer while the NASDAQ was slightly higher.

The Japanese Yen

USDJPY was under pressure in the lead-up tot he FOMC but experience a cascading effect lower as stop-loss selling intensified on a break of the 111.60 support line after the minutes were released. How much liquidity conditions undermined the dollar weakness is tough to gauge, but the dovish FOMC rhetoric is not.

The Euro

Besides the FOMC minutes catalyst, the Euro is getting a bonus bounce from reports that the EU and UK will come to terms with the Brexit divorce bill

Asia FX

Its all aboard the ASEAN party bus USDTWD, USDKRW USDMYR and USDTHB are hitting fresh year lows.

The Korean Won

In addition to the weaker USD narrative, supportive inflows, strong domestic Macro conditions and BoK rate expectations bolstering the Won, the latest bounce comes on the back of long dollar hedge unwinds as geopolitical risk abates.

Malaysian Ringgit

Besides the Macro bounce supporting the MYR the weaker USD post FOMC minutes will continue to support over the short-term

And while the only thing that does matter for oil prices is the month end OPEC meeting, WTI oil prices managed to hang on to yesterday’s gains. Prices were supported by an oil leak in the Keystone pipeline and the EAI report of a decline in US Crude inventories. This does add to the positive MYR narrative

But the primary catalyst for the stronger MYR over the past 24 hours is surging Bond and Equity inflows which are accelerating real demand for the Ringgit

Philippine Peso

Like the regional peers, the Peso is expected to reap the benefits from US inflation dilemma and softening USD. But the core driver remains a boisterous regional equity rally that is benefiting from capital inflows, solid economic fundamentals and the de-escalation of regional geopolitical tension.

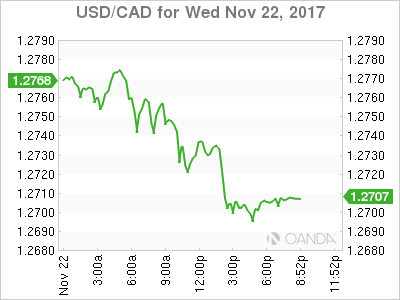

USD/CAD Canadian Dollar Rises On Weak US Data

The Canadian dollar appreciated on Wednesday boosted by US dollar weakness. Oil prices rose to a 2 year high with drawdowns in weekly inventories. The US dollar fell after durable goods orders disappointed with a 1.2 percent fall, although the core reading met expectations at 0.4 percent gain.

The main event in the US before the Thanksgiving holiday was the publication of the Federal Open Market Committee (FOMC) minutes from the November meeting. The market is already pricing in a rate hike in December, but further evidence of the internal debates regarding US inflation were expected. The minutes did not disappoint as there seems to be a strong contingent of Fed voting members who are concerned with weak inflation. That anxiety is not likely going to affect the coming rate hike, but will dampen the pace of rate hikes in 2018.

The NAFTA talks ended the fifth round without much progress and US representative called out Mexico and Canada for not engaging on the provisions that will lead to a rebalanced agreement. This rebalancing refers mainly to the US demands to increase the threshold for autos from 62.5 percent to 85 percent. Other US officials were more optimistic and that progress was made, but more on gelling than actually closing.

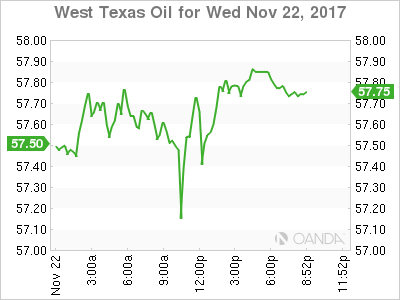

Oil prices rose on Wednesday as US weekly inventories showed a larger drawdown than expected as well as comments around an extension to the Organization of the Petroleum Exporting Countries (OPEC) agreement that has stabilized prices. Saudi Arabia is said to be pushing for a 9 month extension to the deal that ends in March and will try to rally the other major producers to agree to it on their November 30 meeting. Russia has not committed to such an agreement, but there are rumours that they would prefer a 6 month extension.

The USD/CAD lost 0.54 percent on Wednesday. The currency is trading at 1.2700 after the release of the November Federal Open Market Committee (FOMC) minutes. Fed voting members are likely to raise US interest rates at the December meeting, but there are concerns that some of them would like to see inflation improve. Given that the market is pricing that eventuality at near 100 percent it already has been fully priced in, so any anxiety about inflation is more likely to affect the future path of rates in 2018.

Fed Chair Janet Yellen will end her term as Chair in February and she will also step down as a Governor of the central bank as was expected when she was the Trump’s administration nominee to remain in the position. Chair Yellen favoured a hike now, inflation later approach that seems to be inline with her successor (appointment pending) Jerome Powell. Dovish voices have risen within the Fed as inflation remains stagnant, but with strong growth data and a central bank willing to normalize monetary policy the Fed is more likely to keep tightening in 2018.

The Bank of Canada (BoC) hiked twice in 2017, but that only put the Canadian benchmark rate back to 1 percent where it was when Governor Poloz cut the rate twice to boost the economy ahead of the fall of oil prices. The loonie will face more pressure as the Fed continues its monetary policy tightening pace, while the BoC will be more cautious as it monitors rising household debt.

The NAFTA renegotiations have not gone according to plan, unless the plan was to not have any progress. The dream of wrapping up negotiations before the end the year is already dead and Mexico and the United States will have to sit down to the table, while electoral noise could disrupt proceedings. Mexico will hold Presidential elections in 2018 and the US primaries will take place next year and if the few elections this year are any indications it could signal a backlash for the Republican establishment.

The price of oil rose on Wednesday. The price of West Texas Intermediate is $57.86 as the USD took a tumble ahead of the US Thanksgiving holiday. Oil touched a two year high after the US weekly inventories dropped by 1.9 million barrels. The market was forecasting a lower drawdown, but after the massive drop in API inventories on Tuesday and disruptions in North America, crude continued its way upward. Global supply is lower, thanks to the Organization of the Petroleum Exporting Countries (OPEC) and other major producers agreement to cut production levels and other disruptions to supply around the world.

The OPEC will meet with major producers on November 30 to seek an extension to the deal that takes them beyond the current March deadline.

Market events to watch this week:

Thursday, November 23

4:30 am GBP Second Estimate GDP q/q

8:30 am CAD Core Retail Sales m/m

11:30 am CHF SNB Chairman Jordan Speaks

On The Latest US Dollar Weakness

The main catalyst for US dollar bulls over the past 2 months has been tax reform, but that could also be the catalyst for the bears as Ashraf indicated here and here. The yen was the top performer Wednesday while the US dollar lagged. New Zealand retail sales beat estimates in early Asia-Pacific trading. The Premium Insights took 90-pip gain on 1 of the 2 EURUSD trades. 6 of the existing Premium trades are currently in the green.

For months various markets have been pricing in changes to the US tax code. It's impossible to say exactly what's priced in but it's clear that passing something is more likely than ever. So why the US dollar weakness?

We've been writing this week about the divergence between stock markets and USD/JPY. In the past , there has been a solid correlation between the pair and equity prices. Recently, however, the S&P 500 and Nikkei have soared while USD/JPY has languished.

One theory is that traders are wary of 'selling the fact' and getting out of the way early. Perhaps that's true. Another is that the Fed is increasingly getting worried about low inflation. Today's release of the FOMC minutes showed some members want to hit the pause button after a December hike and wait for inflation to get closer to target. There is probably some truth in that as well.

Back to the tax story. The dollar is selling because of the tax plan. More specifically, the details of the plan. It's increasingly clear this isn't a broad-based tax cut. It's heavily skewed to corporations and the top earners, while offering little to the vast majority of Americans. See Ashraf's notes on the disappointing tax holiday for US multinationals and rising cost of debt in the aforementioned pieces.

Maybe the market is saying that this plan isn't going to boost incomes, wages, investment or growth. Instead it will add to the deficit and lead to spending cuts down the road. What it will do is boost corporate profits and that explains the rosy reaction in stocks.

Whatever the reason for the dollar selling, the USD/JPY chart sent a major signal Wednesday. It broke the 100-day and 200-day moving averages, along with the October low in a 125 pip drop. It was part of a broad dollar rout. It's tempting to brush aside because of the US holidays but this move is too big and long-lasting to ignore.

Looking ahead, the Asia-Pacific calendar is light. Early in trading the Q3 New Zealand retail sales report showed a 0.2% rise excluding inflation. That's better than the +0.1% expected and the kiwi caught a small bid on the release.

Pound Falls after Hammond Downgrades Economic Outlook; Euro Rebounds as Eurozone Consumer Confidence Surprises to the Upside

The British Budget for 2018 was the main focus during today's European trading session, while a strip of economic releases out of the US also attracted some attention. The pound posted short-lived losses after British official budget forecasters downgraded the country's economic outlook, while the dollar dipped into losses after strong flash readings on eurozone confidence activated euro bulls.

The British Finance Minister, Philip Hammond, delivered the UK's budget statement for 2018 in the Parliament on Wednesday, announcing that official GDP forecasts were lowered for the next four years. Particularly, he said that the Office for Budget Responsibility is now estimating that GDP will grow by 1.5% in 2017 compared to the 2.0% expected in March. For 2018, growth forecasts were reduced from 1.6% to 1.4%, while an expansion by 1.3% is projected for both 2019 and 2020, below the previous projections of 1.7% and 1.9%. With the economy growing slowly, Hammond will struggle to raise taxes and support public finances at a time when the country is preparing to exit the EU. Pound/dollar lost ground in the wake of the announcement but managed to rebound to 1.3291 in the face of a weaker dollar. On the day, the pair gained 0.40%.

The euro erased earlier losses after flash estimates on Eurozone confidence surprised to the upside. Eurozone consumer confidence rose to its highest in almost 17 years to stand at 0.1 according to November flash estimates by the European Commission. This is the first positive reading for the index since early 2001 and compares to expectations for a reading of -0.8 and October's downwardly revised -1.1 (from the previous -1.0). Euro/dollar reacted positively following the data release, eventually rising to the day's high of 1.1796. The pair last traded close to the aforementioned high (+0.48% on the day).

On the monetary policy front, the ECB is said to delay any policy movements at its December's meeting according to sources familiar with the matter. The central bank decided in October to scale back economic stimulus by halving its asset purchases and extending the asset purchase scheme by nine months, pushing out any prospect of a rate hike until 2019. Although the ECB chief, Mario Draghi said that some decisions may be left for December, sources claimed that they do not "expect any substantial discussion before March or possibly mid-year".

Meanwhile, in the US, new orders for capital goods made in October, declined unexpectedly for the first time after two months of advancing. Analysts had forecasted a smoother rise of 0.3% m/m, but the actual reading came in negative at -1.2%. In September, new orders increased by 2.2% m/m. Excluding volatile items, durable goods orders expanded by 0.4% m/m, below the 0.5% expected and the 1.1% tracked in September.

In other US data, initial jobless claims for the week ending November 17 declined by 12,000 to 239,000 applicants as expected after two weekly consecutive increases. The four-week average gauge, though, inched up to 239,750 as previous marks were revised upwards. The Michigan Consumer Sentiment index beat expectations, rising by 0.9 points in November to 98.5.

The dollar index slipped to 93.53 (-0.43%) on the back of a stronger euro. Investors were also worried about a flattening yield curve which could be a sign of a possible economic downturn. Dollar/yen and dollar/swissie sank by 0.80% to 111.51 and 0.9824 respectively. Gold surged by 0.83% to $1,291.20 per ounce.

Later in the day, the FOMC meeting minutes due at 1900GMT might bring further volatility to the market.

Looking at energy markets, oil prices pared some of their gains earned during the Asian session after touching a two-year high early on Wednesday despite the EIA report confirming a decline in US crude oil inventories. The EIA numbers showed that US crude oil stocks decreased by 1.855 million barrels compared to a fall of 1.545 million expected by analysts. However, gasoline production rose by 0.580 million barrels, posting the highest increase since February. WTI crude slipped to $57.39 per barrel but remained 1.0% up on the day. Brent moved down to $57.42 a barrel, gaining 0.14%.

Gold Improves on Dismal Durable Goods Orders

Gold has posted considerable gains in the Wednesday session. In North American trading, the spot price for an ounce of gold is $1290.71, up 0.79% on the day. On the release front, durable goods reports were a mix. Core Durable Goods Orders gained 0.4%, matching the forecast. However, Durable Goods Orders declined 1.4%, well of the forecast of a 0.4% gain. The UoM Consumer Sentiment report came in at 98.5, above the forecast of 98.2 points. Later in the day, the Federal Reserve releases the minutes of its November policy meeting.

The markets are keeping an eye on the Federal Reserve, which will release the November minutes later in the day. In October, the Fed announced that it would taper its balance sheet, and those reductions of $10 billion commenced around the time of the November meeting. The odds of upcoming rate hikes remains very high, with fed futures priced in at 91% and 89%, respectively. If the minutes reinforce the market perception that more markets are just around the corner, the US dollar could gain ground.

As President Trump's tax reform bill winds it way through Congress, gold prices have been fluctuating and traders can expect this to continue when the Senate votes on its version of the bill after Thanksgiving. On Monday, gold prices jumped 1.4%, erasing the losses seen on Friday. President Trump won a major legislative victory when the House of Representatives passed a tax reform bill. However, with the vote largely based on party lines, Republicans will have a tougher battle passing the Senate version of the bill, as the Republicans have a slim majority of 52-48. The tax legislation provides major tax relief and cut corporate taxes from 35% to 20%, and if Congress does enact a new tax code, the US dollar could make strong gains, at the expense of gold.

Pound Higher Despite Lower UK Growth Forecast

The British pound has posted gains in the Wednesday session. In North American trade, GBP/USD is trading at 1.3283, up 0.35% on the day. On the release front, the UK presented the Autumn Budget. In the US, durable goods reports were a mix. Core Durable Goods Orders gained 0.4%, matching the forecast. However, Durable Goods Orders declined 1.4%, well of the forecast of a 0.4% gain. The UoM Consumer Sentiment report came in at 98.5, above the forecast of 98.2 points. Later in the day, the Federal Reserve releases the minutes of its November policy meeting.

British Finance Minister Philip Hammond released the August Budget, which was noteworthy for a large contingency fund for Brexit. Hammond announced he was setting aside GBP 3 billion pounds over the next two years, beefing up the contingency fund of GBP 700 million. Meanwhile, the Office for Budget Responsibility (OBR) downgraded Britain's GDP for 2017, from 2% to 1.5%. The OBR also revised downwards productivity growth and business investment, further signs that the economy could be headed for a down-spin.

There was positive news from British CBI Industrial Order Expectations on Monday, an important barometer of activity in the manufacturing sector. The indicator surged to 17 points in October, rebounding from the September release of -2 points. Manufacturing indicators continue to point upwards, boosted by strong global demand and a weak British pound. Export order books are at their highest levels since 1995, and the markets are predicting that the export and manufacturing sectors will continue to shine in the fourth quarter.

The markets are keeping an eye on the Federal Reserve, which will release the November minutes later in the day. In October, the Fed announced that it would taper its balance sheet, and those reductions of $10 billion commenced around the time of the November meeting. The odds of upcoming rate hikes remains very high, with fed futures priced in at 91% and 89%, respectively. If the minutes reinforce the market perception that more markets are just around the corner, the US dollar could gain ground.

Activity Declines Due to Thanksgiving Celebration

The EUR/USD price keeps consolidating thanks to a short trading week in the US due to the Thanksgiving Day celebration. Investors are also reluctant to open new positions ahead of tomorrow's release of the ECB monetary policy meeting minutes. Some pressure on the greenback came from the durable goods orders report in the US, according to which the indicator decreased by 1.2% in October against forecasted growth of 0.4%. At the same time, the core durable goods orders increased by 0.4% which was in line with the expected figure. The attention of the market today will turn to the FOMC meeting minutes' publication at 19:00 GMT. We should note that Janet Yellen will be leaving the chair and the hawkish sentiment on the market will be hit by the uncertainty concerning the future inflation figures forecasts by the Fed, which have become less certain after the last speech by Mrs. Yellen.

The British pound was negatively affected by the finance minister, Philip Hammond's speech during which he announced that forecasts of economic growth in the UK had worsened due to lower labour force productivity. Tomorrow, investors should pay attention to the preliminary report on British GDP growth for the third quarter.

The aussie quotes grew amid investors uncertainty regarding the US dollar. News on the MI leading index increasing by 0.1% in September had little impact on traders. Activity until the end of the week will be low due to the holiday in the US, but we do not exclude sharp moves due to lower trading volumes.

EUR/USD

The EUR/USD returned to the support line at 1.1730 but was not able to break through it. The next target in case of rising dynamics will be 1.1825. On the other hand, we do not exclude the price fixing below 1.1730 which may become a trigger for a sharp decline to 1.1620 or even to 1.1500.

GBP/USD

The GBP/USD has shown a sharp rise in volatility after some consolidation near 1.3250. The gradual decline in the amplitude of price fluctuations, increases the possibility of a powerful impulse in either direction. In case of the price fixing under the inclined support line, the immediate goals will be at 1.3150 and 1.3050. The growth within the next days is likely to be limited at the 1.3400 mark.

AUD/USD

The AUD/USD restored some of the previously lost positions and may continue the rising dynamics to 0.7600 and 0.7635. The RSI on the 15-minute chart is approaching the overbought zone which points to a possible price correction. The MACD signal line on the 15-minute chart just crossed the zero line which is an additional stimulus for the price to continue growing.

Yen Hits 8-week High as US Durable Goods Decline

The yen has posted considerable gains in the Wednesday session. In North American trade, USD/JPY is trading at 111.64, down 0.71% on the day. The yen is at its highest level against the dollar since late September. Japanese banks are closed for a holiday, and there are no Japanese events on the schedule. In the US, durable goods reports were a mix. Core Durable Goods Orders gained 0.4%, matching the forecast. However, Durable Goods Orders declined 1.4%, well of the forecast of a 0.4% gain. The UoM Consumer Sentiment report came in at 98.5, above the forecast of 0.4%. Later in the day, the Federal Reserve releases the minutes of its November policy meeting.

The markets are keeping an eye on the Federal Reserve, which will release the November minutes later in the day. In October, the Fed announced that it would taper its balance sheet, and those reductions of $10 billion commenced around the time of the November meeting. The odds of upcoming rate hikes remains very high, with fed futures priced in at 91% and 89%, respectively. If the minutes reinforce the market perception that more markets are just around the corner, the US dollar could gain ground.

US construction numbers continue to beat expectations. On Monday, it was the turn of Existing Home Sales, which climbed to a 4-month high. On Friday, Building Permits and Housing Starts impressed the markets. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Starts also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.