Sample Category Title

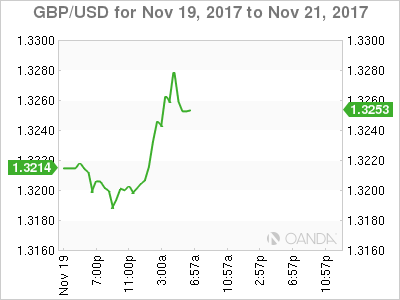

GBPUSD Intraday Bullish Above 1.3220

The British pound has moved sharply higher against the U.S dollar, hitting 1.3280 during today's European trading session. The pound has been one of the foreign exchange market's strongest performing pairs over the last few trading session, driven by German political fears. The GBPUSD pair currently trades around the 1.3245 level, with the 1.3268 level still remaining a major medium-term technical price hurdle for pound buyers.

The GBPUSD pair remains intraday bullish while holding above the key 1.3220 level. Further upside towards the 1.3307 and 1.3360 levels appears likely.

Should price-action decline below the 1.3220 level, sellers may push the pair towards the 1.3200 and 1.3168 technical levels.

GBP & EUR Moves

Sterling and euro are in the news for different reasons with the former gaining on imrpoved prospects of an agreement on the Brexit bill and the latter undergoing volatility in Asian trade after German coalition talks collapsed following the Free Democratic Party's walking out of the exploratory talks. More strikingly is the euro's recovery of all its 70-pip decline in London trade amid the realisation that any delayed would fail to derail the economic recovery in Germany and rest of the Eurozone.

Futures positioning showed increasingly vulnerable bets against JPY. USD/JPY opened the week near a one-month low after a slide in Treasury yields and stock markets on Friday. What's troubling is that sentiment was bolstered a day earlier by a positive vote in the US House on tax reform. One way to look at it is that now the good news for tax reform is priced in. It faces a tougher battle in the Senate and it could be more than a month before anything is passed. The market may be reflecting that worry.

Cable also deserves a closer watch. A weekend report in the FT said Theresa May could give the greenlight to increasing the Brexit bill on Monday. That would help to break a deadlock and move the talks forward.

Ultimately, the market is far less concerned with the tab, and far more concerned with the post-Brexit trade deal. If paying €40B or even €60B is what it takes to get something like a free trade deal, then that would count as a major win for the pound. Watch for more headlines Monday.

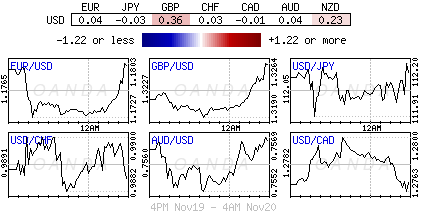

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +85K vs +85K prior

- GBP -4K vs -9K prior

- JPY -136K vs -128K prior

- CHF -28K vs -25K prior

- CAD +47K vs +51K prior

- AUD +44K vs +45K prior

- NZD -12K vs -11K prior

Yen shorts are at the most extreme since the end of 2014 but the market was caught offside by the rally Thursday. Despite all the bets on a climb in USD/JPY, the pair is close to the mid-point of the 2017 range. That's a sign of a vulnerable market.

Gold Bullish above 1290 in Near Term

Gold has shifted to a more bullish bias in the near-term after strong upside momentum last Friday pushed the metal above a key Fibonacci level. On the 4-hour chart, a bullish signal was given by the crossover of the 50-period moving average above the 200-MA.

On Friday, prices rallied after a break above the 23.6% Fibonacci (1283.47) of the downleg from 1357.47 to 1260.59. Momentum faded when the market reached overbought levels. The 4-hour RSI crossed above the 70 level and this is when prices pulled back. The rally also slowed down just ahead of resistance at the 38.2% Fibonacci (1297.58).

A daily close above immediate support at 1290 would help keep momentum to the upside but 1297.58 needs to be broken to strengthen the move up to target the key 1300 area soon. Alternatively, failure at 1290 support would take price back down to 1283.46 and from here the odds get stronger for a re-test of the 1260.59 low.

Since the end of October, prices have been making higher lows but in the bigger picture, the market still does not show a clear direction in the trend, which has mostly been neutral since the drop from 1357.47.

DAX Higher Despite Merkel Woes

The DAX index has started the week with gains. In the Monday session, the DAX is at 13,020.50, up 0.21% on the day. On the release front, German PPI remained unchanged at 0.3%, edging above the estimate of 0.2%. The markets will be keeping an eye on ECB President Mario Draghi, who is testifying before the European Parliament Economic and Monetary Affairs Committee. Draghi will be discussing ECB monetary policy, and the markets will be looking for clues regarding future policy moves.

Germany is in political crisis, as coalition talks have fallen apart. The Free Democratic Party (FDP) pulled out of talks on Sunday. Christian Lindner, head of the FDP, did not mince words, saying that there was no "basis of trust" to enter a government with Angela Merkel's CDU-CSU alliance and the Greens. The parties have been holding negotiations for a month, but have failed to bridge the gaps on issues such as immigration. So what happens next? Merkel has said in the past that she will not run a minority government, but if she holds fast to that stance, Germany would likely face another election. Some pundits are predicting that this could be the end of the Merkel era, which could usher in a period of political uncertainty in the largest economy in the eurozone.

Mario Draghi spoke at the Frankfurt European Banking Congress on Friday. Draghi was upbeat, noting the strong outlook for the eurozone economy. Draghi noted that GDP has risen for 18 consecutive quarters, and he expected the positive momentum to continue, pointing to positive global and domestic trends. The global economy has strengthened, and corporate and consumer debt continues to head lower.

The eurozone economy continues to perform well in the third quarter. German GDP accelerated to 0.8%, while Eurozone Flash GPD remained steady at 0.6%. However, inflation remains the fly in the ointment, with levels well below the ECB target of around 2 percent. Weak inflation has kept the ECB cautious regarding its monetary stimulus program. The ECB announced in October that it would chop asset-buying from EUR 60 billion to 30 billion each month, but added that it was extending the scheme until September 2018. Jens Weidmann and other senior policymakers want the ECB to act more aggressively, and have called on the ECB to announce a termination date to its stimulus program. However, Mario Draghi appears in no rush to wrap up the scheme, especially with no inflation pressures on the eurozone economy.

EUR Recovers After German Coalition Shock

Monday November 20: Five things the markets are talking about

The collapse of the German coalition talks over the weekend would suggest that Germany is no longer the role model of 'political' stability. Europe's strongest economy has the possibility of three options ahead, a minority government, a continuation of the current grand coalition or new elections.

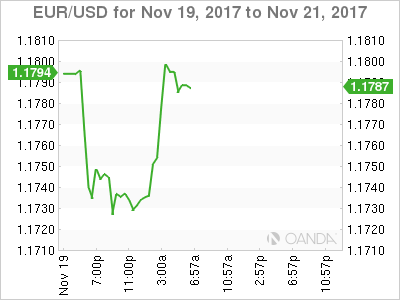

The EUR (€1.1795) has recovered to last trade up +0.68% outright having earlier dropped to its lowest in nearly a week at €1.1723 as the market reassessed how bad it is that Chancellor Merkel failed to form a coalition.

The majority expected a coalition to happen and the most probable scenario now is for Merkel to form a minority government with the FDP.

Note: Trading volumes are expected to be lower than average this week due to the Thanksgiving holiday in the U.S.

The week ahead, key data are the flash November PMI's in Europe (Nov. 23), Japan and the U.S. Germany posts updated Q3 GDP and the important November Ifo survey (Nov. 24). From Japan, key October merchandise trade data (Nov 24) will also be reported.

Minutes from the Reserve Bank of Australia's (RBA) November meeting are due Tuesday (Nov. 21), while those from the ECB's October meeting due out on Thursday (Nov. 23) could show dissent in the discussion about tapering.

The U.K. announces its budget Wednesday (Nov 23); that could see a significant economic downgrade amid a continued impasse in its negotiations with the E.U on Brexit.

Also on Wednesday, the Fed will publish the minute's form its November meeting (2:00 pm EST). There will be more clues on where certain policy makers stand regarding inflation, but the market is still pricing in a +99% probability of a U.S rate hike next month.

1. Stocks mixed results

In Japan, the Nikkei share average fell overnight amid losses stateside and a stronger yen (¥112.00), while semiconductor equipment manufacturers and financial stocks underperformed. The Nikkei ended -0.6%, while the broader Topix slipped -0.2%. Turnover also dropped to a one-month low.

Down-under, Australia's stock benchmark was pressured overnight by a pullback in the country's major banks after late-week gains. After rising the last two sessions, the S&P/ASX 200 settled down -0.2%.

In Hong Kong, stocks rose slightly overnight. The Hang Seng index rose +0.2%, and the China Enterprises Index lost -0.6%.

In China, stocks reversed early losses to end higher on Monday, aided by a rebound in banking shares even after Beijing set new guidelines to regulate asset management products. The blue-chip CSI300 index dropped as much as -1.5% in early trade but closed up +0.6%, while the Shanghai Composite Index ended -0.3% higher.

In Europe, regional equities opened lower, but turned around after digesting situation in Germany. Energy stocks are supported by oil prices, but commodity prices are underperforming, but not enough to significantly impact material stocks.

U.S stocks are set to open in the 'red' (-0.2%).

Indices: Stoxx50 -0.1% at 3,545, FTSE -0.2% at 7,366, DAX -02% at 12,970, CAC-40 flat at 5,320, IBEX-35 +0.1% at 10,019, FTSE MIB flat at 22,086, SMI +0.6% at 9,236, S&P 500 Futures -0.2%

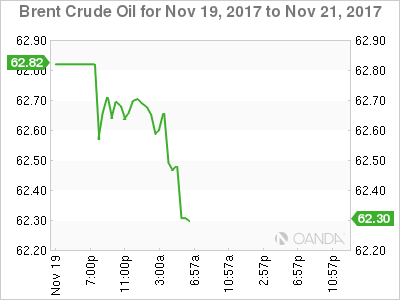

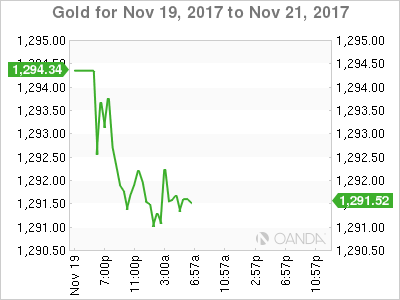

2. Oil markets tepid ahead of Nov. 30 OPEC meeting, gold prices steady

Oil markets are little changed as investors seem reluctant to take on big new positions ahead of an OPEC meeting at the end of the month, when producers are expected to decide whether to continue output cuts aimed at supporting prices.

Brent crude futures are at +$62.47 per barrel, down -25c or -0.4% from Friday's close, while U.S West Texas Intermediate (WTI) crude futures are at +$56.57 a barrel, up just +2c.

OPEC, along with a group of non-OPEC producers led by Russia, have been restraining output since the start of this year in a bid to end a global supply overhang and prop up prices. The deal expires in March 2018.

OPEC is expected to agree an extension, although there are doubts about the willingness of some participants to continue to restrain output.

Note: In the U.S, the number of rigs drilling for new oil production remained unchanged in the week to Nov. 17 at 738 (Baker Hughes).

Gold has dipped on a firmer dollar, but it's staying close to its one-month peak on uncertainty over progress on a potential overhaul of the U.S tax code. Spot gold is down -0.2% at +$1,291.44 per ounce.

3. Sovereign yields fall

Germany's 10-year Bund yield fell to its lowest level in two-weeks in the early Euro session, after weekend talks to form a coalition government failed and raised the risk of fresh elections.

The political crisis in Europe's biggest economy has pushed Germany's 10-year Bund yield down -1.5 bps to +0.35%, its lowest level since Nov. 9.

Elsewhere, the yield on U.S 10-year Treasuries fell -1 bps to +2.34%. In the U.K, 10-year Gilt yield has climbed +1 bps to +1.309%. In Japan, the 10-year JGB yield has increased less than +1 bps to +0.038%.

4. Dollar continues to struggle

Naturally, the focus in FX is on Germany with the current German coalition talks collapsing.

The EUR/USD tested €1.1722 during the Asians session. However, EUR 'bulls' noted that despite the political uncertainty in Germany, the domestic economic engine remained robust and thus would not need the help of near-term reform efforts to continue to boom. The 'single unit' (€1.1795) has reversed back the majority of its overnight losses on reports that FDP would support forming a minority government run by Merkel rather than new elections.

GBP (£1.3254) is higher on market optimism that the U.K would soon increase its offer for the Brexit financial settlement. The U.K budget Wednesday will greatly influence the pounds short-term direction.

5. German producer prices in October 2017

In October, the index of producer prices for German industrial products rose by +2.7% compared with the corresponding month of 2016. Compared with the preceding month September, the overall index rose by +0.3%.

Note: In September, the annual rate of change all over had been +3.1%.

Digging deeper, the price indices of all main industrial groups increased y/y – prices of intermediate goods rose by +4.1%, energy prices were up +2.8%. Prices of non-durable consumer goods rose by +2.8%, while prices of durable consumer goods increased by +1.2%, whereas prices of capital goods increased by +1.1%

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bullish momentum last week topped at 1.1860 but closed a little bit lower at 1.1786 and hit 1.1722 earlier today in Asian session. Overall price is still in a short-term bullish phase since broke above 1.1690 but still respects the trend line resistance as you can see on my H1 chart below and as long as stay below 1.1900 my major bullish outlook remains valid. The bias is bearish in nearest term testing 1.1690 support area. A clear break and daily close below that area would retest 1.1550 region this week. Immediate resistance is seen around 1.1800. A clear break above that area would expose 1.1860 – 1.1900 key resistance.

GBPUSD

The GBPUSD was indecisive last week. The bias is neutral in nearest term. Price has been moving sideways between 1.3330 – 1.3040 range area for the last six weeks now and we need a clear break from that range area to see clearer direction. Immediate support is seen around 1.3160 followed by 1.3115 but key support remains at 1.3000. Immediate resistance is seen around 1.3230. A clear break above that area could trigger further bullish pressure testing 1.3260 but key resistance remains at 1.3330. Overall I remain bullish.

USDJPY

The USDJPY had a bearish momentum last week bottomed at 111.94 and hit 111.88 earlier today in Asian session. The bias is bearish in nearest term testing 111.65 (daily EMA 200) as a part of the bearish pin bar scenario as you can see on my daily chart below. A clear break and daily close below that area would expose 110.65 region. Immediate resistance is seen around 112.50. A clear break above that area could lead price to neutral zone in nearest term testing 113.00 region. Overall I remain neutral.

USDCHF

The USDCHF had a bearish momentum last week bottomed at 0.9846 following a clear break below 0.9940 support area (now resistance) but closed a little bit higher at 0.9890. The bias is bearish in nearest term testing 0.9835. Immediate resistance is seen around 0.9940. A clear break back above that area could lead price to neutral zone in nearest term but would give the major bullish trend another chance retesting 1.0037 key resistance area.

Euro Under Pressure As German Coalition Talks Collapse

It's been a busy start to the week for EUR/USD. The pair lost ground in the Asian session, only to recover in European trade. Currently, EUR/USD is trading at 1.1789, down 0.04% on the day. In economic news, there are no major indicators in the eurozone or the US. German PPI remained unchanged at 0.3%, edging above the estimate of 0.2%. The markets will be keeping an eye on ECB President Mario Draghi, who will testify before the European Parliament Economic and Monetary Affairs Committee. Draghi will be discussing ECB monetary policy, and the markets will be looking for clues regarding future policy moves.

German coalition talks are in crisis, as the Free Democratic Party (FDP) pulled out of talks on Sunday. Christian Lindner, head of the FDP, did not mince words, saying that there was no “basis of trust” to enter a government with Angela Merkel's CDU-CSU alliance and the Greens. The parties have been holding negotiations for a month, but have failed to bridge the gaps on issues such as immigration. So what's next? Merkel has said in the past that she will not run a minority government, but if she holds fast to that stance, Germany would likely face another election. Some pundits are predicting that this could be the end of the Merkel era, which could usher in a period of political uncertainty in the largest economy in the eurozone.

US indicators ended the week on a high note, as housing data easily beat expectations. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Start also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.

Technical Outlook: WTI OIL – Recovery Is Consolidating Above 10SMA

WTI Oil price consolidates on Monday after Friday's strong rally which fully retraced last Tuesday's sharp $56.75/$54.80 fall.

Friday's close above 10SMA ($56.33, now again acting as initial support) was bullish signal.

Overall structure remains bullish as correction was contained by rising 20SMA, leaving higher low at $54.80 ahead of Friday's surge.

Bullish bias needs confirmation on repeated close above $56.72 (Fibo 61.8% of $57.90/$54.80 pullback) to $57.90 peak for retest.

Otherwise, extended consolidation above 10 SMA could be seen as likely near-term scenario.

Increased downside risk could be expected on close below 10SMA.

Res: 56.72, 57.17, 57.90, 58.46

Sup: 56.33, 55.82, 55.27, 54.80

Market Update – European Session: Optimism Remains For A Potential Minority Gov’t In Germany Run By Merkel

Notes/Observations

German coalition talks fall apart but optimism remains for a potential minority govt run by Merkel

Overnight

Asia:

China PBOC Q3 monetary policy implementation report: To maintain a prudent and neutral monetary policy and keep liquidity conditions stable, to fend off systemic risks. To improve its “twin pillar” framework by combining its monetary policy with macro-prudential assessment (MPA), while using multiple monetary policy tools to manage liquidity. Reiterated to the CNY currency (Yuan) stable while increasing the currency’s two-way flexibility.

China NDRC Deputy Sec Gen Fan Hengshan: Initial 2018 GDP growth seen at 6.5%

Japan Oct Trade Balance: ¥285.4B v ¥330.0Be; Exports y/y: 14.0% v 15.7%e (11th month of increase); Imports y/y: 18.9% v 20.2%e (highest annual pace since Jan 2014)

Moody’s forecasted G20 2017 and 2018 GDP growth slightly above 3% 2018 compared to 2.5% registered in 2016. Expected China GDP growth to slowly decelerate in 2018. Potential protectionist turn in US trade policy could pose risk to trade-reliant economies

Europe:

German Chancellor Merkel: Tried everything to make coalition talks work; regrets FDP’s decision. Main sticking point was immigration. To stay on as acting-Chancellor and inform German president on Monday, Nov 21st and would do everything possible to get Germany through difficult weeks

Chancellor of Exchequer Hammond (Fin Min): We are on the brink of serious progress in Brexit talks; UK to make proposals to EU in time for the December EU Leader Summit. Needed to get transition period in place as soon as possible, preferably within the next few months

UK Cabinet said to be ready to give UK PM a green light to increase Brexit divorce bill offer in an attempt to break deadlock in talks with Brussels

Americas:

OMB Director Mulvaney: President Trump would agree to removing repeal of Obamacare mandate from the Senate tax bill if it becomes an impediment to passage

US Special Prosecutor Mueller said to send request for documents to DoJ related to Russia probe

Economic Data:

(DE) Germany Oct PPI M/M: 0.3% v 0.3%e; Y/Y: 2.7% v 2.7%e

(JP) Japan Oct Convenience Store Sales Y/Y: -1.8% v 0.0% prior

(NG) Nigeria Q3 GDP Y/Y: 1.4% v 1.5%e

(TW) Taiwan Oct Export Orders Y/Y: 9.2% v 7.8%e

(TW) Taiwan Q3 Current Account: $20.5B v $16.8B prior

(IL) Israel Nov CPI 12-month Forecast: 0.8% v 0.6% prior

Fixed Income Issuance:

(SK) Slovakia Debt Agency (ARDAL) sells total €229.9M in 2026 and 2037 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.1% at 3,545, FTSE -0.2% at 7,366, DAX -02% at 12,970, CAC-40 flat at 5,320, IBEX-35 +0.1% at 10,019, FTSE MIB flat at 22,086, SMI +0.6% at 9,236, S&P 500 Futures -0.2%]

Market Focal Points/Key Themes: European stocks open lower but turned around after digesting situation in Germany; concern over German Chancellor Merkel potentially being unable to forma government dragged on risk sentiment, impacting German stocks at the start of the session; energy stocks supported by oil prices; commodity prices underperforming, but not enough to significantly impact material stocks; attention turning to events later in the week before Thanksgiving holiday; Argentina, Brazil and Mexico will be closed for holidays today; upcoming earnings in the US session include Cubic, Palo Alto Networks and Agilent

Equities

Consumer discretionary: Air France AF.FR +2.9% (analyst action), D'ieteren DIE.BE +7.8% (partnership), Elior ELIOR.FR -4.2% (analyst action)

Consumer staples: Dixy Group DIXY.RU -5.1% (potential delisting)

Energy: Petroleum Geoservices PGS.NO +9.7% (settlement in Brazil)

Financials: Bollore BOL.FR +2.0% (continuation following results), Julius Baer BAER.CH +1.1% (results)

Healthcare: Ablynx ABLX.BE +5.4% (analyst action), DBV Technologies DBV.FR +12.4% (positive study results), Galapagos GLPG.BE +4.3% (positive data), Roche ROG.CH 4.2% (positive study results)

Industrials: Gaussin ALGAU.FR +6.3% (awarded order)

Materials: DSM DSM.NL +1.8% (acquisition)

Technology: Xaar XAR.UK -17.7% (trading update)

Telecom: Altice ATC.NL +10.7%(not planning capital issue), Mediaset MS.IT +3.9% (CFO comments over weekend)

Speakers

German FDP parliamentary whip Marco Buschmann: Would support a minority govt lead by Angela Merkel

Netherlands Min Zijlstra: EU expecting a substantial offer from UK on its Brexit offer and its must be concrete and on the table

Former Italy PM Monti saw difficult elections in Italy. Believed that Gentiloni or Tajani could be PM; unlikely for Renzi or Berlusconi

Poland Central Bank's Osiatynski: Interest rate hike might needed to maintain macroeconomic stability as country could not sustain GDP growth of 4.5-5.0% range

UAE Oil Min Mazrouei saw logic in having OPEC extend the current phase of production cuts. He saw OPEC extending but not deepening the production cuts

Iran Oil Min Zanganeh: Most OPEC members favor extending the current round of production cuts

Currencies

Focus in FX markets was on Germany with the current German coalition talks collapsing. The EUR/USD tested 1.1722 during the Asians session. Some analysts noted that despite the political uncertainty in Germany the domestic economic engine remained robust and thus would not need the help of near-term reform efforts to continue to boom. The EUR/USD clawed back the majority of its losses on reports that FDP would support forming a minority government run by Merkel (rather than new elections. EUR/USD hovering aeound 1.18 area just ahead of the NY morninrg.

The uncertainty in Germany initially weighed upon the EUR/JPY cross and trickled over into the USD/JPY pair as the JPY currency firmed. Both pairs managed to move higher on optimism that Merkel could remain as Chancellor in a minority govt

GBP/USD was higher as optimism bubbled that the UK would soon bump up its offer for the Bexit financial settlement. GBP/USD higher by almost 0.5% at 1.3275

Fixed Income

Bund futures trade 163.00 up 14 ticks, coming off the earlier highs as equity markets rebound from earlier weakness as German coalition talks fall apart. Continued upside sees 163.40 then 163.63. A reversal targets 162.50 then 162.38.

Monday's liquidity report showed Friday's excess liquidity rose €1B to €1.849T. Use of the marginal lending facility declined to €214M from €235M prior.

Corporate issuance saw ~$29B issued for the week via 50 traches. November volume now tops $84B, while 2017 volume approaches $1.3T.

In Europe €31.4B came to market, led by multi tranche deals from Vodafone and BT. 50 issuers came to market via 59 tranches.

Looking Ahead

(SA) Saudi Arabia Sept Oil production: No est v 9.951M prior - JODI

05:25 (BR) Brazil Central Bank Weekly Economists Survey

05:30 (BR) Brazil Sept Economic Activity Index (Monthly GDP): M/M: +0.4%e v -0.4% prior; Y/Y: 1.4%e v 1.6% prior

05:30 (BE) Belgium canceled planned Bond Auction

05:30 (NL) Netherlands Debt Agency (DSTA) to sell €2.0-4.0B in 3-month and 6-month Bills

06:00 (PT) Portugal Reports Monthly Economic Survey

06:00 (IL) Israel to sell 2021, 2027 and 2045 bonds (4 tranches)

06:00 (RO) Romania to sell 5.95% 2021 Bonds

06:30 (CL) Chile Q3 GDP Q/Q: 1.5%e v 0.7% prior; Y/Y: 2.2%e v 0.9% prior

06:30 (CL) Chile Q3 Current Account: -$1.0Be v -$1.6B prior

06:45 (AT) ECB's Nowotny (Austria) speaks at Central Bank Conference in Vienna

06:45 (US) Daily Libor Fixing

07:15 (DE) ECB’s Lautenschlaeger (Germany) in Frankfurt

07:30 (AT) Central European Central Banks governors participate on Panel in Vienna

08:00 (PL) Poland Oct Sold Industrial Output M/M: 3.1%e v 6.0% prior; Y/Y: 9.9%e v 4.3% prior, Construction Output Y/Y: 23.9%e v 15.5% prior

08:00 (PL) Poland Oct PPI M/M: 0.2%e v 0.4% prior; Y/Y: 2.9%e v 3.1% prior

08:00 (PL) Poland Oct Retail Sales M/M: +3.5%e v -0.3% prior; Y/Y: 8.5%e v 8.6% prior, Real Retail Sales Y/Y: 7.5%e v 7.5% prior

08:00 (RU) Russia Oct Unemployment Rate: 5.1%e v 5.0% prior

08:00 (RU) Russia Oct PPI M/M: 0.8%e v 2.4% prior; Y/Y: 6.8%e v 6.8% prior

08:00 (RU) Russia Oct Real Retail Sales M/M: +1.2%e v -0.7% prior; Y/Y: 3.9%e v 3.1% prior

08:00 (DE) German President Steinmeier statement on govt coalition talks

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions

08:05 (UK) Baltic Dry Bulk Index

08:50 (FR) France Debt Agency (AFT) to sell combined €5.0-6.2B in 3-month, 6-month and 12-month Bills

09:00 (EU) ECB chief Draghi in Brussels

09:00 (IN) India announces details of upcoming bond sale (held on Fridays)

09:15 (PT) ECB’s Constancio (Portugal) in Frankfurt

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (US) Oct Leading Index: 0.7%e v -0.2% prior

11:00 (EU) ECB chief Draghi in capacity as European Systemic Risk Board (ESRB) chair

11:30 (US) Treasuries to sell 3-Month and 6-Month Bills

16:00 (US) Weekly Crop Progress Report

Oil’s Fireworks Friday Suggest The Worst Is Over

Oil's impressive rally on Friday has changed the technical picture completely suggesting we could see attempts at new highs this week.

After the fireworks of Friday, crudes price action in Asia has been tepid, to say the least. Both Brent and WTI remain almost unchanged from their respective New York closes.

The same couldn't be said for Friday's session with Brent climbing a respectable 2.20% and WTI soaring 2.40% with both contracts tracing out some very bullish technical price action. There was no one driver for the rallies; rather we feel oil benefited from a general rotation out of U.S. dollars. The worst of the corrective sell-off would appear to be over now as well with the weak long positioning flushed out. Traders seem to be turning their attention now to the OPEC/Non-OPEC meeting on the 30th of November and an extension of the production cut deal to cover all of 2018.

Brent crude is unchanged at 62.25 and has traced out a bullish outside reversal day on Friday, having made a marginal new low and then forged higher to close substantially above the previous days high. The triple bottom at 61.25 is now a quadruple bottom after Friday and will provide formidable support to any pullbacks now. Resistance is currently at 63.30 ahead of the challenging double tops at 64.40 and 64.85.

WTI spot trades at 56.55 as we await the start of the European session. It held its 6-week trend line support impressively on Friday with the low of 55.15 being the line itself before rallying to 56.55. Today this line comes in at 55.275 and is followed by support at 54.50. The charts are now clear for another challenge of the November highs at 57.80.