Sample Category Title

Pound Gains Continue, British Inflation Report Eyed

The British pound has posted gains in the Monday session. In North American trade, GBP/USD is trading at 1.3239, up 0.18% on the day. On the release front, there are no British indicators on the schedule. In the US, the sole event is CB Leading Index. The indicator gained 1.2%, above the forecast of 0.6%. On Tuesday, the UK releases Public Sector Net Borrowing and the BoE Inflation Report Hearings. The US will publish Existing Home Sales. As well, US Federal Reserve Chair Janet Yellen will speak at an event in New York City.

There was good news from US construction numbers on Friday. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Start also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.

One of the main sticking points in the Brexit negotiations is the size of Britain's divorce bill. The European Union has demanded EUR 60 billion, while Britain has made an offer of EUR 20 billion. Prime Minister May apparently wants to compromise at EUR 40 billion, but senior ministers Boris Johnson and Michael Gove are reluctant to pay more without a clearer idea of what form a new trade relationship with Europe will take. The divisions within May's cabinet have only weakened May's hand. May hasn't been able present a coherent Brexit policy to the Europeans or to the voters at home, raising doubts as to whether she can deliver the goods on Brexit. With Britain scheduled to leave the EU in March 2019, there is pressure on both sides to begin trade talks before the end of 2018.

Euro Fails to Rebound after Draghi’s Dovish Words; Pound Gains on Brexit Hopes

Political noise in Germany continued to draw markets' attention during the European trading hours as the economic calendar was lacking major releases and any progress on the US tax reforms was expected only after the Thanksgiving holidays. The euro was on track to erase losses made in the previous session but dovish remarks by the ECB President pressured the currency. The dollar was in the green during the session while the pound drifter higher as hopes on Brexit negotiations moving forward appeared on the horizon.

Following a strong sell-off in Asia, the euro managed to recover from a two-month low as investors retained their confidence in the eurozone amid optimism on the block's relative economic momentum. Late on Sunday, the German Chancellor, Angela Merkel, had announced that coalition talks had failed to reach a three-way agreement after the FDP decided to pull out from the negotiations as the parties were unable to find a common solution to key issues. Later on Monday, the German President, Frank-Walter Steinmeier speaking to reporters after a meeting with Merkel, urged parties to resume negotiations prioritizing the nations' interests, signalling that he did not prefer new elections.

Meanwhile, in the monetary policy front, the ECB chief, Mario Draghi, testified before the European Parliament's economic committee in Frankfurt. Draghi highlighted that inflation has not shown self-sustained upward trend yet, while the labour market "still need time to translate into more dynamic wage growth", hinting that monetary stimulus is still necessary.

The euro touched an intra-day high of $1.1807 but it slipped back to 1.1750 after Draghi's dovish remarks, losing 0.36% on the day.

The dollar index gained 0.24%, rising to 93.88 but analysts admitted that dollar investments would be muted this week given the uncertainties surrounding the US tax overhaul. Markets believe that the Senate Republicans will face challenges to pass the tax bill when they return after a week off for the Thanksgiving holidays. Dollar/yen was up 0.21% to 112.30 and dollar/swissie jumped by 0.38% to 0.9923. Dollar/loonie rose by 0.27% to 1.2795.

The dollar-denominated gold extended its losses, falling by 0.65% to $1,285.90 per ounce.

The pound remained 0.24% up on the day, supported by expectations that the UK cabinet will back an increase in the Brexit divorce bill under certain conditions. Particularly, ministers predict that the offer could rise from the current 20 billion euros to 40 billion euros approaching the EU's estimate of 60 billion euros. Besides that, the EU Brexit negotiator, Michel Barnier, stated on Monday that the EU was willing to give Britain "its most ambitious trade deal" but only if it meets EU demands.

In other currencies, the aussie was weaker by 0.24% at $0.7547 ahead of the RBA monetary policy meeting minutes release early on Tuesday. Note, that RBA policymakers decided in October to hold interest rates at a record low level of 1.50% as expected, retaining their optimism on country's economic outlook.

The kiwi stood flat at $0.6816.

Looking at energy markets, oil prices retreated sharply on Monday as investors turned cautious ahead of next week's OPEC meeting where OPEC and non-OPEC members will discuss whether to keep restraining oil supply after the current deal expires in March 2018. Investors are widely anticipating that the deal will be extended until the end of 2018 but doubts are still growing about Russia's commitment. WTI declined by 1.57% to $55.66 per barrel and Brent fell by 1.79% to $61.60.

Yen Dips Despite Higher Trade Surplus

The yen has started the new trading week with slight gains. In North American trade, USD/JPY is trading at 112.35, up 0.24% on the day. On the release front, Japan's trade surplus jumped to JPY 0.32 trillion, crushing the forecast of JPY 0.21 trillion. Later in the day, Japan realizes All Industries Activity, with an estimate of -0.4%. In the US, the sole event is US CB Leading Index. The indicator gained 1.2%, above the forecast of 0.6%. On Tuesday, the US publishes Existing Home Sales. As well, US Federal Reserve Chair Janet Yellen will speak at an event in New York City.

US housing numbers ended the week on a positive note, easily beating expectations. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Start also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.

Japan's trade surplus improved in October, buoyed by strong demand for Japanese exports. China is showing some momentum after a recent slowdown, and Japanese factories are having a hard time keeping up with the demand for automobiles, electronics and machinery. The robust manufacturing and export sectors have fueled a moderate recovery, as Japan has now posted 16 consecutive quarters of growth, the longest economic expansion since 2001. However, Preliminary GDP for Q3 came in at 0.3%, weaker than the 0.6% gain in Final GDP for the second quarter. Although the economy has improved in 2017, but this has not translated into higher inflation levels. Inflation remains persistently below the inflation target of around 2 percent, but the Bank of Japan has no plans to change policy. Earlier in the week, BoJ Governor Haruhiko Kuroda acknowledged the inflation issue, saying "it is not easy to quickly dispel the deflationary mindset that has formed over the course of 15 years of deflation." Kuroda added that he expects inflation levels to rise, but in the meantime the BoJ would continue its massive monetary easing, a key component of the "Abenomics" program.

Dollar Set for Lacklustre Week as Focus Remains on Senate Tax Vote

There's expected to be few drivers for the US dollar this week, with investors likely to shrug off data releases and the FOMC minutes ahead of the Thanksgiving holiday, with the focus firmly on the tax plan, which is facing a crucial vote in the Senate.

The US Census Bureau will publish its monthly advance report on manufacturers' shipments, inventories and orders on Wednesday – a closely watched gauge of industrial activity that is seen as a good indication of future factory output. Orders of durable goods are expected to rise by 0.3% month-on-month in October, easing from a 2% surge in September. However, the data is not expected to see much of a reaction in forex markets as it is unlikely to alter the outlook for the US economy in the run up to the December FOMC meeting.

A rate hike by the Fed at its December 12-13 meeting appears to be a foregone conclusion, with market-implied odds of a 25-bps rate hike now running over 90% and several Fed officials signalling such a move in recent public remarks. Further indication of Fed action next month will likely come from the minutes of the October 31-November 1 meeting, which are published on Wednesday. The Fed will probably signal in the minutes that further tightening would be appropriate soon – in what would be the third rate increase this year.

A bigger concern for investors though in the near term is the fate of the US tax plan in the Senate. The tax bill passed its first major hurdle when it was approved by the House of Representatives last week. However, the Republicans have a much smaller majority in the Senate and could lose the vote if three or more Senators object to it. The Senate's version of the tax bill differs widely from the House version and is proving unpopular among some Senate Republicans.

A vote on the Senate's version of the tax legislation is not expected to come until the week after the Thanksgiving holiday at the earliest. The dollar could struggle to find upside momentum before then. It has already retreated sharply from the 8-month high of 114.72 yen set earlier this month as investors await Congress to give the tax reforms the green light before making fresh bets on the dollar.

With the near-term risk for dollar/yen tilted to the downside, immediate support should come from the 200-day moving average around 111.75, just below today's one-month low of 111.87. A breach of the 200-day moving average could see the next key support being formed around the 111 level.

Core Bonds Shrug off German Political Crisis

- European equities opened with losses following the collapse of German coalition talks, but managed to recover initial weakness to trade currently up to 0.5% higher. US stock markets started with marginal gains.

- Germany's President Steinmeier urged the country's political parties to return to the negotiating table and avoid the need for new elections. SPD-leader Schulz said new elections would be right following the collapse of the four-way coalition talks.

- The German economy is powering into the end of the year thanks to strong industrial activity and firms are increasingly struggling to find workers to satisfy orders, the country's central bank said.

- Italy's anti-establishment 5-Star Movement pummelled a centre-right coalition to govern Ostia, one of Rome's largest neighbourhoods, in a run-off vote that confirms the 5-Star's strength months away from a national election.

- EU chief Brexit negotiator Barnier told the UK to come up with a solution for the Irish border, making clear that an improved offer on the divorce bill might not be enough to unblock talks.

- There is a 50% chance the Czech central bank will raise interest rates again in December after hikes in August and November, though it is in no rush to tighten policy, the bank's Governor Jiri Rusnok said. Rusnok said any move would likely be by 25 bps, the same as the last hike on Nov. 2 which brought the main repo rate to 0.5%.

Rates

Core bonds shrug off German political crisis

In a data-poor opening session of the week, core bonds (and other markets) shrugged off the German political crisis triggered by the collapse of the coalition negotiations. In the afternoon, the German president urged parties to find a deal to avoid a new vote, as he is unprepared to call early elections. He will hold talks with the party leaders. Caretaker chancellor Merkel promised to do whatever it takes to give Germany a working government. It only affected markets very temporarily. The Dax opened weak, testing key support, but no break occurred, leading to short covering and modest daily gains.

The Bund opened higher (163.08), equities and the euro substantially lower, but the tide turned immediately. The Bund dropped to around Friday's closing level (162.87) where the selling dried up and the Bund started to move sideways. An attempt to rally again higher in early afternoon failed and by the time of closing our report the Bund trades again near Friday's closing levels. Similarly, the US T-Note moved higher in Asian trading before easing slightly during the European session. In early US dealing, US traders sold Treasuries, pushing them to modest losses.

At the time of writing, the US yield curve steepens slightly in bearish fashion with yields 1.3 bps (2-yr) to 2 bps (10-30-yr) higher. German yield changes varied between +0.5 bps (5-yr) and -0.5 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany ranged between -1 bp and +1 bp with Greece slightly underperforming (+4 bps).

Currencies

Impact of German crisis on the euro is short-lived

Trading in the major FX cross rates was confined to tight ranges today except for a temporary decline of the euro this morning due to the political stalemate in Germany. EUR/USD touched an intraday low in the 1.1725 area, but already returned to the 1.18 area early in Europe as global markets didn't draw any firm conclusions from German developments. Later in the session, the dollar gained a few ticks in technical trade. EUR/USD trades in the 1.1770 area. USD/JPY is changing hands in the 112.25 area.

Overnight, Asian markets opened in risk-off modus. Both regional and global themes were in play. Asian investors also pondered the potential impact of the collapse of the German coalition talks. EUR/USD dropped from the 1.18 area to the 1.1725 area. The pair traded slightly off the intraday lows at the start of the European trading session. USD/JPY suffered no substantial loss and hovered in the 112 area.

The German Bund contract jumped higher at the open, but European markets soon found their composure. Core bond yields rebounded. EUR/USD reversed the Asian losses as soon as it became clear that the German political uncertainty wouldn't cause a meaningful sell-off on European equities. EUR/USD returned to the 1.18 area. At noon, European equities even traded with marginal gains, but it had no big impact on FX trading anymore. EUR/USD settled closed to, but slightly below, 1.18. USD/JPY held an extremely tight sideways range in the low 112 big figure.

Early in the afternoon, the German President urged the parties in the coalition negotiations to find a deal to avoid a new vote. There was little impact on the euro. In technical trading, the dollar captured a cautiously positive bid. EUR/USD trades in the 1.1775 area. USD/JPY hovers around 112.25. Constrictive risk sentiment apparently puts a floor for the dollar. At the same time, German politics had no negative impact on the euro, but evidently, it is also no help.

Conflicting Brexit headlines block further GBP-gains

German political uncertainty weighed on the euro overnight, including on EUR/GBP. At the same time, UK policy makers indicated they might make further concessions on the amount of the UK Brexit Bill. EUR/GBP touched an intraday low in the 0.8875 area at the start of the European trading session. However, both stories again didn't last long enough to cause a protracted EUR/GBP trend-move. The euro soon reversed the Asian losses. The impact on EUR/GBP was initially limited as cable stayed well bid, hoping on positive Brexit news. Sterling sentiment eased later on, as EU's Barnier spoke tough on the conditions that need to be fulfilled to start trade negotiations. Aside from the financial bill, he stressed that the UK also needs to bring a workable solution for the Irish boarder. Cable drifted gradually off the intraday highs, pushing EUR/GBP back up to the 0.89 area (currently 0.8890). Cable trades currently in the 1.3245 area. Sterling eased off the intraday highs against the euro and the dollar. That said, underlying sentiment on the UK currency doesn't look too bad. Sterling stays away from the recent lows against euro and the dollar.

Elliott Wave Analysis: German DAX and AUDUSD

Good day traders. Here are qucik peeks on DAX and AUDUSD.

German DAX turned nicely up, as we expected and moved sharply back above 13k figure. We see an impulsive reaction from recent swing low so we think it's wave C which can run up into 13100-13150 area where upside can be limited this week since we think that recovery from 12846 is a correction. A reversal may be seen.

German DAX, 15Min

Recent minor rally on AUDUSD to 0.7574 is looking like a small correction, probably wave four within ongoing five waves of decline from 0.7618 that can extend down to 0.7500. We however think that sooner or later a higher degree correction will occur, but only if we see a break above 0.7600.

AUDUSD, 1H

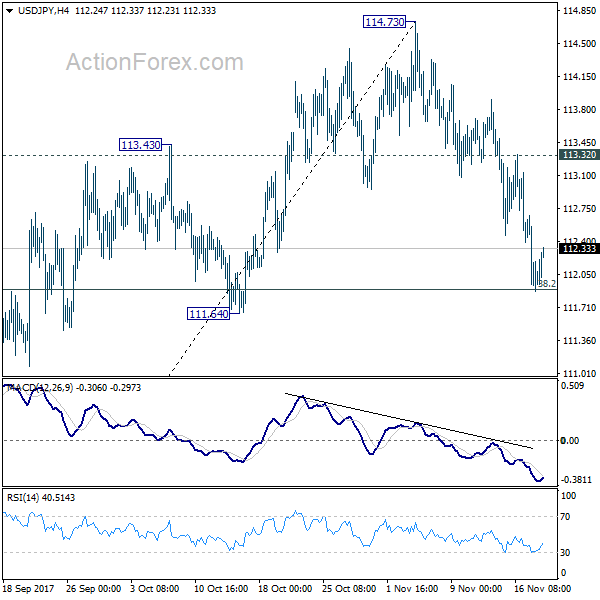

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.62; (P) 112.38; (R1) 112.82; More...

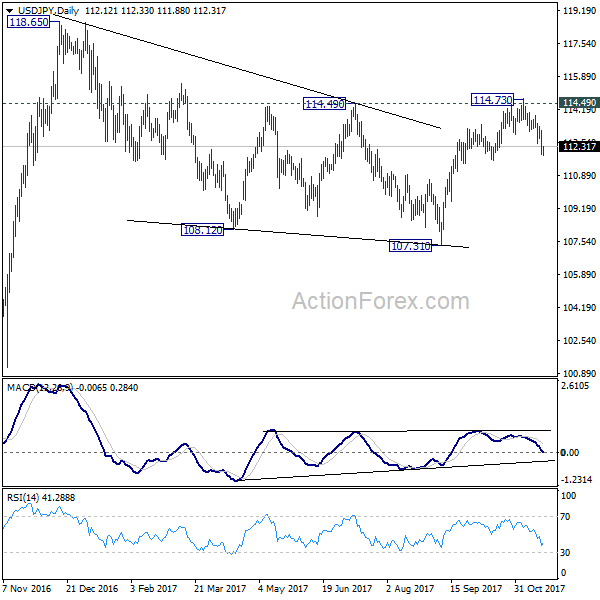

At this point, intraday bias in USD/JPY remains on the downside. Fall from 114.73 could extend lower. Decisive break of 111.64 support will argue that whole rebound from 107.31 has completed. In that case, deeper fall would be seen to 61.8% retracement of 107.31 to 114.73 at 101.14 and below. On the upside, though, break of 113.32 minor resistance will indicate that the pull back is completed and turn bias back to the upside.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

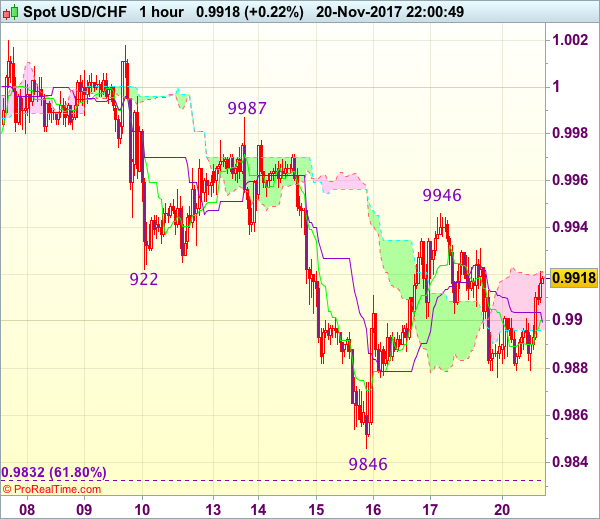

Trade Idea Wrap-up: USD/CHF – Hold short entered at 0.9935

USD/CHF - 0.9913

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9900

Kijun-Sen level : 0.9900

Ichimoku cloud top : 0.9921

Ichimoku cloud bottom : 0.9896

Original strategy :

Sold at 0.9935, Target: 0.9835, Stop: 0.9950

Position : - Short at 0.9935

Target : - 0.9835

Stop : - 0.9950

New strategy :

Hold short entered at 0.9935, Target: 0.9835, Stop: 0.9950

Position : - Short at 0.9935

Target : - 0.9835

Stop : - 0.9950

Although the greenback rebounded after finding support at 0.9876, as long as indicated resistance at 0.9946 holds, bearishness remains for another retreat, below said support at 0.9876 would add credence to our view that the rebound from 0.9846 has ended at 0.9946, bring further fall to 0.9860, then retest of 0.9846. Once this level is penetrated, this would signal the erratic decline from 1.0038 top has resumed for at least a retracement of early upmove to previous resistance at 0.9837, break below there would encourage for subsequent decline towards 0.9795-00.

In view of this, we are holding on to our short position entered at 0.9935. Above said resistance at 0.9946 would defer and risk test of 0.9970-75 but price should alter below resistance at 0.9987, bring another decline later.

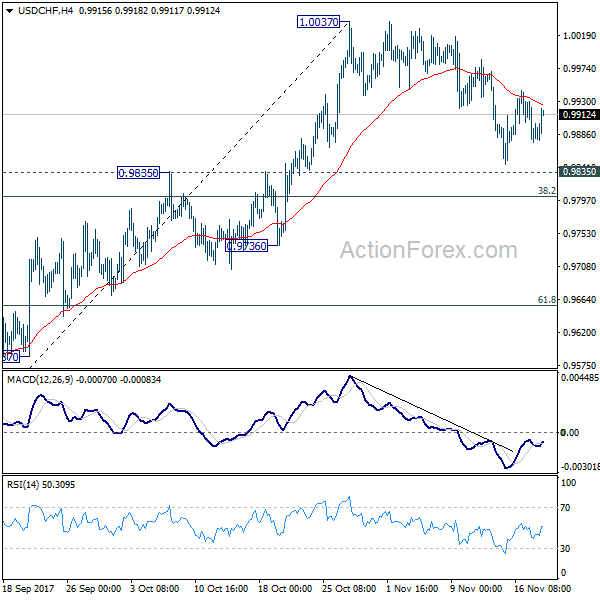

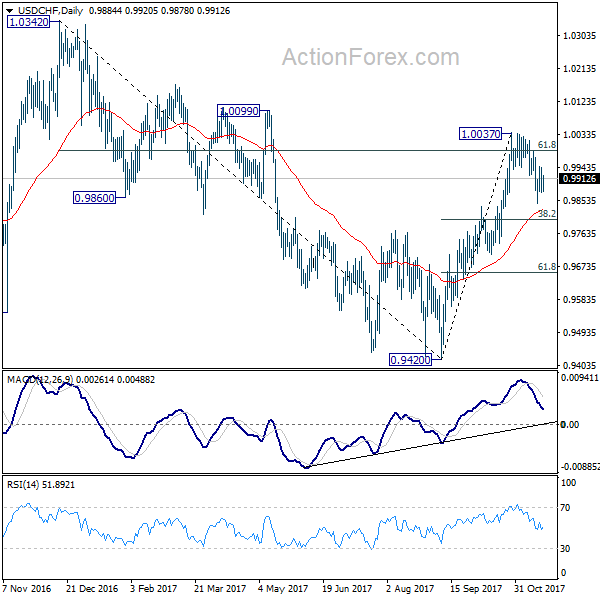

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9859; (P) 0.9901; (R1) 0.9926; More....

Intraday bias in USD/CHF remains neutral for the moment. On the upside, firm break of 1.0037 resistance will extend the rise from 0.9420 and target 1.0342 high. However, sustained break of 0.9835 resistance turned support will argue that whole rebound form 0.9420 is completed and turn outlook bearish. In that case, USD/CHF should target 61.8% retracement of 0.9420 to 1.0037 at 0.9565 and possibly below.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could be a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

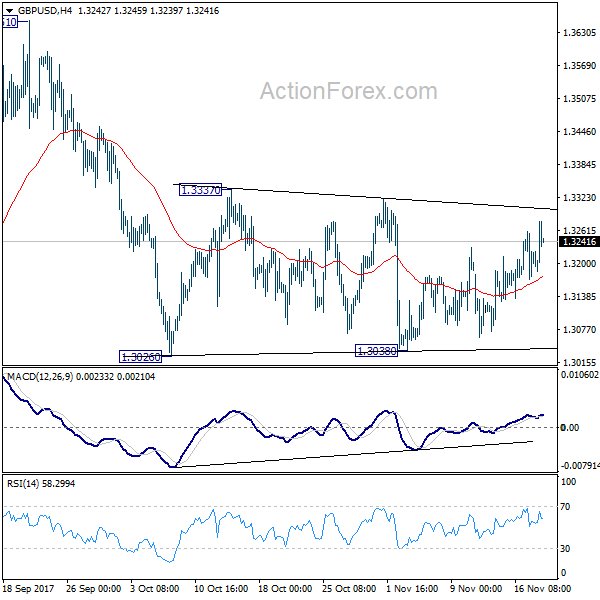

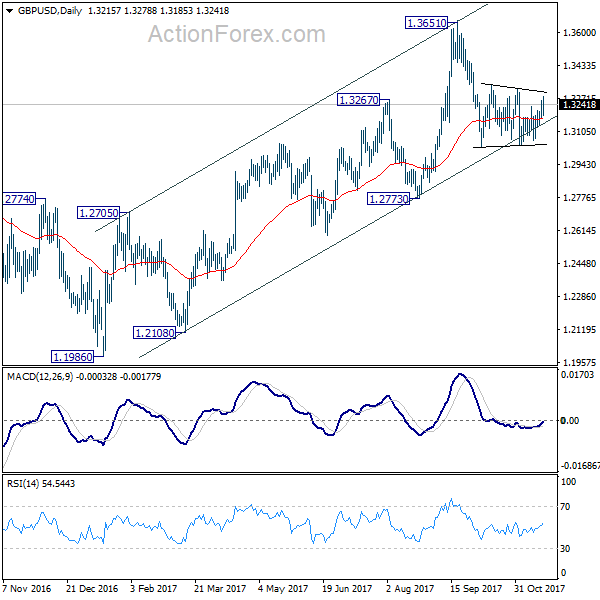

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3168; (P) 1.3213; (R1) 1.3258; More....

GBP/USD's choppy recovery from 1.3038 extends today but it's staying in range of 1.3026/3337 after all. Intraday bias remains neutral at this moment. Upside of recovery should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.