Sample Category Title

The Central Bank Decision Is Due

Market movers today

It is a very light day in terms of data releases; hence market focus is likely to be on the evolving political stand still in forming a new government in Germany after SPD left the coalition talks over the weekend.

In Hungary, the central bank decision is due and we expect unchanged rates along with concensus expecations. The central bank may continue its dovish signals despite fast wage growth and strong economic activity.

Statistics Denmark publishes employment data for September. The number of people in work rose in August after a slight fall in July, and we expect a further improvement in September.

Selected market news

In Germany snap elections moved closer yesterday as Chancellor Angela Merkel stated that she favours a new poll over a minority government. With SPD having ruled out a new ‘grand coalition' and Merkel ruling out a minority government the only option left seems to be a new election. A new government is not likely to be formed until well into 2018 delaying any potential Eurozone reforms.

Fed Chairman Janet Yellen yesterday announced she will not continue at the Fed when Jerome Powell takes over as Chairman after Yellen's term ends in February, see Bloomberg. Her decision leaves Donald Trump with a fourth spot to fill on the Federal Reserve Board.

The US leading indicator from Conference Board jumped back in October rising 1.2% m/m (consensus 0.8% m/m). September was revised up to 0.1% m/m from -0.2% m/m. The data underlines the strong picture of the US economy currently. US 2-year yields rose to a new high yesterday flat tening the US yield curve further. The flattening has received much at tention lately in relation to Fed policy with some arguing it worries the Fed as it is a signal of an economic slowdown. However, a San Francisco Fed paper yesterday argues that the low long-term yield is justified by a lower ‘normal rate', risk of persistently low inflation and fiscal and geopolitical uncertainty, see paper.

Asian stock markets were strong overnight with gains across the board defying signs of a Chinese slowdown. China's Tencent grabbed the headlines yesterday as they joined the ranks of Apple and Facebook breaking the USD500 bn mark in market value. Tencent is the maker of the Chinese social media We Chat with close to one billion users. Chinese company Alibaba might be next in line as they currently have a market value of USD 474 bn.

Yesterday we published an update on the latest Chinese measures to crack down on shadow banking announced Friday last week. We also released travel notes from US trip visiting political analysts, think tanks, economists and journalists, see US travel note Tax cuts are coming but will be watered down.

Trade Idea : EUR/USD – Buy at 1.1680

EUR/USD - 1.1738

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1740

Kijun-Sen level : 1.1769

Ichimoku cloud top : 1.1772

Ichimoku cloud bottom : 1.1765

Original strategy :

Buy at 1.1700, Target: 1.1800, Stop: 1.1665

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1680, Target: 1.1780, Stop: 1.1645

Position : -

Target : -

Stop : -

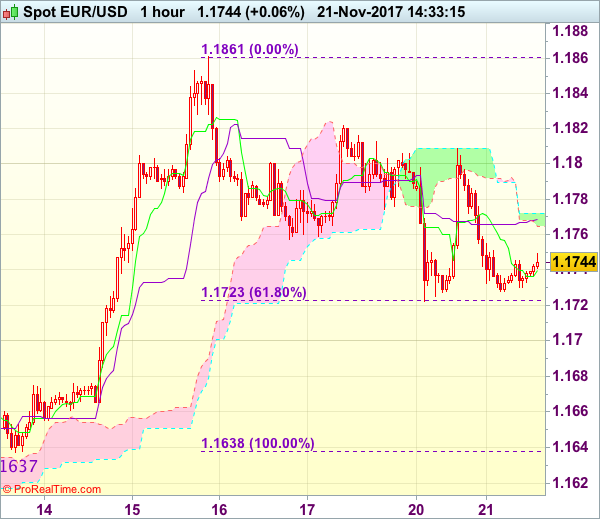

As the single currency has retreated again after meeting resistance at 1.1809, suggesting near term downside risk remains for the erratic fall from 1.1861 top to bring retracement of recent rise, hence initial fall to 1.1700 cannot be ruled out, however, reckon downside would be limited to 1.1671-78 (61.8% Fibonacci retracement of 1.1554-1.1861 or previous resistance) and bring rebound later to 1.1809 but break of resistance at 1.1822 is needed to signal the pullback from 1.1861 (last week’s high) has ended, bring retest of said resistance later.

In view of this, we are looking to buy euro on next decline as 1.1671-78 should limit downside and bring rebound later. Only below 1.1650 would defer and signal top has been formed instead, bring a stronger retracement of recent rise to previous support at 1.1637 first.

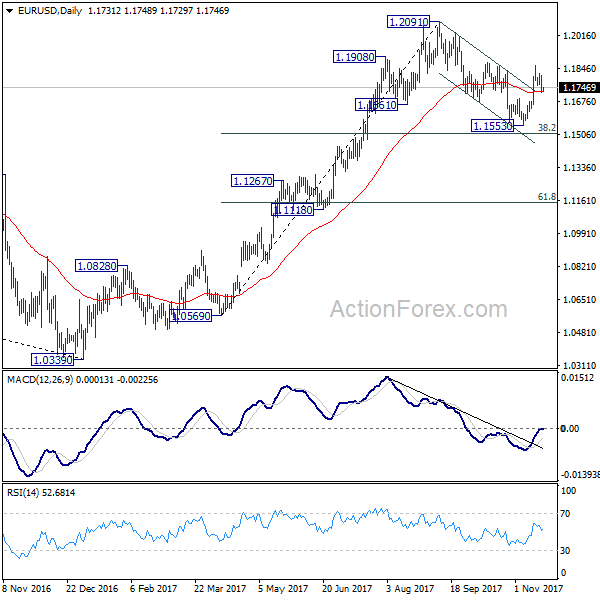

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1699; (P) 1.1753 (R1) 1.1786; More....

Intraday bias in EUR/USD remains neutral at this point. With 1.1677 minor support intact, further rally is expected. As noted before, corrective fall from 1.2091 has completed at 1.1553 already, ahead of 38.2% retracement of 1.0569 to 1.2091 at 1.1510. Above 1.1860 will turn bias to the upside for retesting 1.2091 high. However, break of 1.1677 will dampen this bullish view and turn focus back to 1.1553 low instead.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1373) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

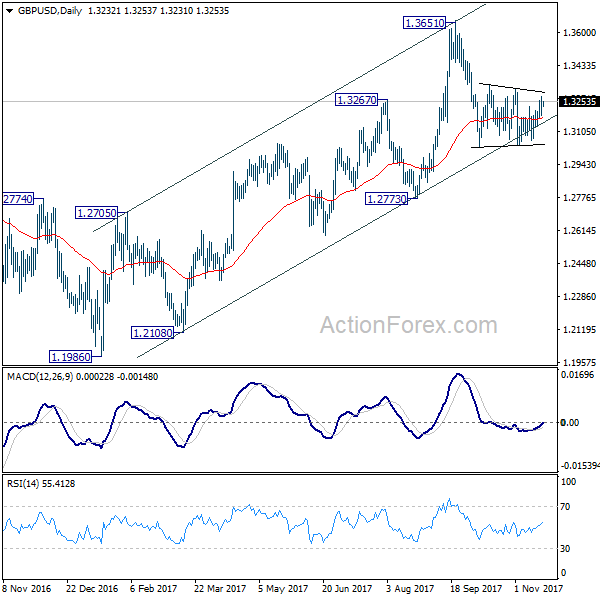

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3186; (P) 1.3232; (R1) 1.3279; More....

GBP/USD continues to be bounded by range of 1.3026/3337. Intraday bias remains neutral at this moment. Upside of recovery should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

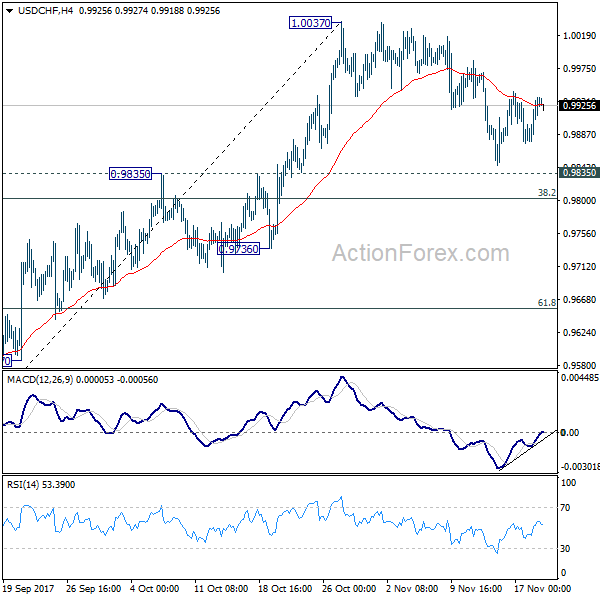

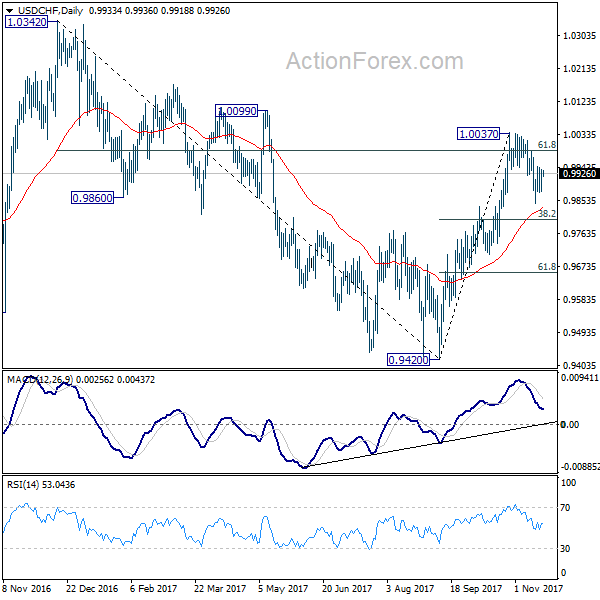

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9896; (P) 0.9916; (R1) 0.9955; More....

Intraday bias in USD/CHF remains neutral for the moment. On the upside, firm break of 1.0037 resistance will extend the rise from 0.9420 and target 1.0342 high. However, sustained break of 0.9835 resistance turned support will argue that whole rebound form 0.9420 is completed and turn outlook bearish. In that case, USD/CHF should target 61.8% retracement of 0.9420 to 1.0037 at 0.9565 and possibly below.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could be a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

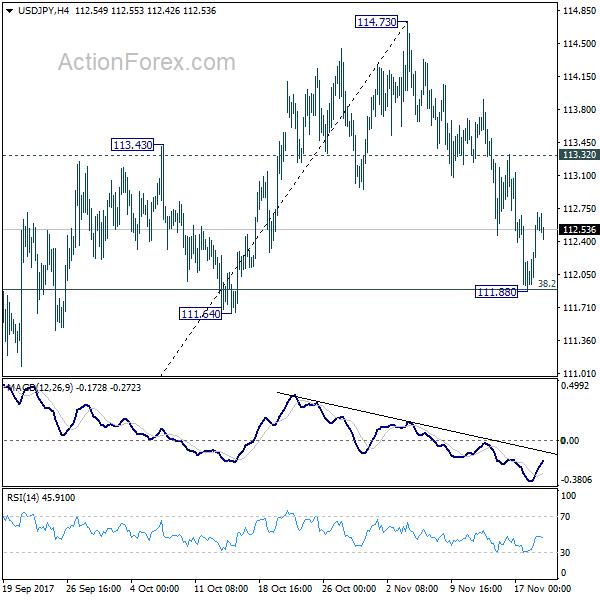

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.09; (P) 112.40; (R1) 112.92; More...

USD/JPY recovers after dipping to 111.88, hitting 38.2% retracement of 107.31 to 114.73, ahead of 111.64 support. Intraday bias is turned neutral first. On the upside, break of 113.32 will revive near term bullishness and turn bias to the upside for 114.73. On the downside, however, decisive break of 111.64 support will argue that whole rebound from 107.31 has completed. In that case, deeper fall would be seen to 61.8% retracement of 107.31 to 114.73 at 101.14 and below.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

Elliott Wave Analysis: Mid-Term On AUDUSD Looks Bearish

AUDUSD is showing us a potentially completed higher degree three-wave recovery as in an A-B-C manner. We see final wave C of IV completed at the 0.81234 level and recent sharp reversal that followed can be start of a new bearish cycle. We see wave 1) in progress, that can search for a low near the 0.7562 former swing low and from there make a new corrective three-wave rally into wave 2). Once wave 2) fully unfolds, more weakness into upcoming wave 3) can follow.

AUDUSD, Daily

Crude Oil Price Remains In Uptrend Above $55.00

Key Highlights

- Crude oil price recently traded as high as $57.84 against the US dollar before starting a downside correction.

- There are two bullish trend lines forming with supports at $55.50 and $55.00 on the 4-hours chart of XTI/USD.

- The 100 simple moving average (red, 4-hour) is also positioned at $55.50 to provide support.

- Today, the US Existing Home Sales Change will be released for Oct 2017 which is forecasted to increase by 0.7% (MoM).

Crude Oil Price Technical Analysis

Crude oil price traded nicely in November 2017 so far and recently traded as high as $57.84 against the US dollar. It is currently correcting lower but remains supported above $55.00.

The price recently traded towards the $55.00 support area where the 100 simple moving average (red, 4-hour) prevented declines. Looking at the 4-hours chart of XTI/USD, there are two bullish trend lines in place with supports at $55.50 and $55.00.

On the upside, there is a connecting bearish trend line with current resistance at $56.60 on the same chart. Should there be a close above $56.60, the price will most likely retest $57.80.

On the downside, only a close below $55.00 and the mentioned 100 simple moving average could open the doors for losses may be toward $54.00 or even $52.00. An intermediate support is around $53.30 and the 200 simple moving average (green, 4-hour).

Economic Releases to Watch Today

UK’s Public Sector Net Borrowing Oct 2017 – Forecast £6.600B, versus £5.326B previous.

US Existing Home Sales for Oct 2017 (MoM) – Forecast +0.7%, versus +0.7% previous.

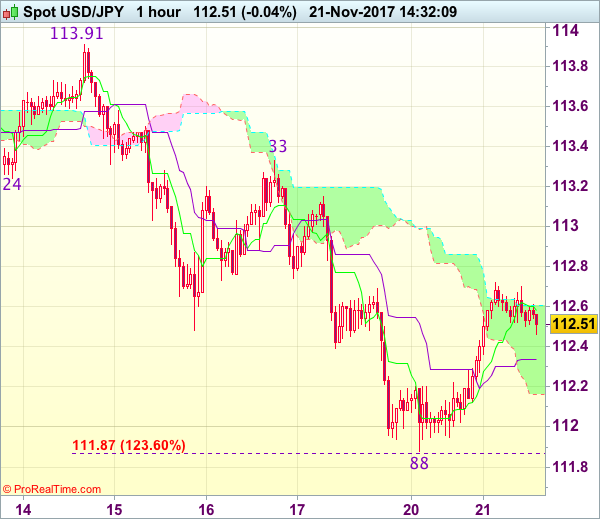

Trade Idea : USD/JPY – Hold short entered at 112.60

USD/JPY - 112.48

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.58

Kijun-Sen level : 112.34

Ichimoku cloud top : 112.61

Ichimoku cloud bottom : 112.16

Original strategy :

Sold at 112.60, Target: 111.60, Stop: 112.95

Position : - Short at 112.60

Target : - 111.60

Stop : - 112.95

New strategy :

Hold short entered at 112.60, Target: 111.60, Stop: 112.75

Position : - Short at 112.60

Target : - 111.60

Stop : - 112.75

Although the greenback rebounded after falling to 111.88, reckon upside would be limited to 112.27-75 and bring retreat later, below 112.10-15 would bring retest of said support at 111.88 (yesterday’s low), break there would extend recent decline from 114.74 top to previous support at 111.65, break there would bring further fall to 111.45-50, however, near term oversold condition should limit downside and reckon 111.00-05 would hold from here.

In view of this, we are holding on to our short position entered at 112.60. Above 112.85-90 would risk test of previous support at 113.09 but only break there would abort and signal low is formed instead, bring a stronger rebound to 113.33 resistance first.

Market Update – Asian Session: Risk Appetite Returns With Bond Yields Lower

Headlines/Economic Data

Japan

Nikkei 225 opened +0.9%;

Automakers track Monday’s gains in US auto sector; Toyota +1.6%

Steelmakers track recent gains in shares of US Steel; JFE +1%

Mega Banks and Topix Securities Brokers index gain (rebound from prior session’s losses)

Toshiba +4% (closed -5.8% on Monday), Softbank +1.3%, Fast Retailing +0.8%

(JP) Japan Finance Min Aso: Tax changes need to consider work reform and an aging society; one time depreciation is a big encouraging investment

(JP) Japan Defense Min Onodera unable to rule out more North Korea ‘provocations’ - Japanese Press

Korea

Kospi opened +0.2%

LG Display +4% (South Korea to decide on planned investment in China), Hynix +1.5% (Micron +3.2%); Hanwha Life -3% (stake sale)

(KR) South Korea Nov (20 days) Exports Y/Y: 9.7% v 6.9% prior; Imports Y/Y: 14.0% v 3.1% prior

Won reversed yesterday’s losses as risk appetite returns

(KR) Local South Korea think tank: Expect the won to remain strong in 2018

(US) Pres Trump: US to designate North Korea as a state sponsor of terrorism

034220.KR South Korea said to hold meeting related to planned investment in China - South Korean Press; +5.7%

China/Hong Kong

Shanghai Composite opened -0.3%, Hang Seng +0.4%

Hang Seng Information Technology Index +3.5% (Tencent +3.9%, market cap moves above Facebook’s)

Hang Seng Financials Index +1%; Insurers gain amid rise in China 10-year bond yield

Hang Seng Consumer Goods Index +0.8% (L’Occitane +2.5% after reporting final Q3 earnings); Property Index -0.5%

(CN) China Energy Investment Group and China National Coal Group will keep their 2018 coal contract prices at CNY535/t, flat y/y - financial press

(CN) China NDRC Vice Chairman Lian Weiliang says coal prices are currently relatively high and should be guided downward – Chinese Press

USD/CNY (CN) PBoC sets yuan reference rate at 6.6356 v 6.6271 prior

(CN) PBoC OMO: Injects CNY180B v CNY100B injected in 7,14 and 63-day reverse repos prior; Net injects CNY10B v CNY20B prior

Australia/New Zealand

ASX 200 opened +0.2%;

Graincorp -5% (FY17 profits below ests; CEO sees challenging year ahead)

AUD trades at 5-month low: Morgan Stanley (MS) said to forecast the Aussie to trade at $0.65 (timing uncertain)

The pass-through to inflation could be delayed by many factoring including retail competition, consumption growth likely to be lower in Q3 versus Q2, says the Reserve Bank of Australia (RBA) Nov Meeting Minutes.

(AU) Australia banking regulator, APRA, Chairman Byres: Have concerns over housing and lending standards

(AU) Australia PM Turnbull: considering tax cuts for low and middle income earner, in addition to lowering the corporate rate to 25% from 30% - speaking to Business Council of Australia

RBA Gov Lowe to speak during European morning

Australia Q3 Construction work done to be released on Wednesday’s session

ATM.NZ Reports FY18 first 4-months EBITDA NZ$78.4M; Rev NZ$262.2M – AGM; +4.3%

Other Asia

(TW) Taiwan Gov sells NT$25B in 30-yr bonds, avg yield 1.667% v 1.7%e; bid-to-cover 1.54x

North America

US equity indices ended Monday broadly higher: Dow +0.3%, S&P 500 +0.1%, Nasdaq +0.1%, Russell 2000 +0.7%; Financials and Industrials outperformed

After Market Movers: Intuit (INTU) Reports Q1 $0.11 adj v $0.05e, Rev $886M v $855Me; -2.4% afterhours Palo Alto Networks (PANW) Reports Q1 $0.74 v $0.68e, Rev $505.5M v $489Me; Promotes Bonanno as CFO; +7.3% afterhours; Urban Outfitters (URBN) Reports Q3 $0.41 v $0.33e, Rev $893M v $857Me; +3.1% afterhours

M&A: US DoJ seeking to block merger between Time Warner Inc and AT&T; Nestle said to show bidding interest in Hain Celestial (press report); CVS may reportedly come to definitive agreement to acquire Aetna by end of Nov (press report)

Debt Issuance: Weight Watchers International priced $300M in high yield 2025 senior notes (offering downsized from $500M)

Little news seen regarding US tax reform.

(US) Janet Yellen to resign from Fed Board of Governors, effective upon the swearing in of her successor as Chair

BABA Muddy Waters in a report calls Alibaba's Singles Day numbers "obviously fake"

Europe

(DE) German Chancellor Merkel: new elections would be better than a minority govt; goal is still to form a stable govt - TV interview

(DE) CDU Parliamentary Leader Kauder: we seem to be on the course for new elections in Germany

(EU) Reportedly ECB expected to make small, incremental changes next year in discussing QE exit - press

(UK) UK panel reportedly considering move to £40B (€45B) Brexit offer - UK press

(UK) Unnamed source in PM May's office says nothing is agreed upon in the Brexit until everything is agreed - financial press

(UK) EU Chief Brexit Negotiator Barnier reportedly informs EU27 that more clarity is needed on the Brexit bill; believes bill cannot be tied to trade agreement

(UK) BOE's Dep Gov Ramsden: UK economy in a weaker growth period for some time to come; domestic CPI is below the rate consistent with 2% goal

Levels as of 00:00ET

Nikkei +1.0%, Hang Seng +1.22%; Shanghai Composite +0.4%; ASX200 +0.4%, Kospi +0.1%

Equity Futures: S&P500 +0.0%; Nasdaq100 +0.1%, Dax +0.0%; FTSE100 0.0%

EUR 1.1745-1.1730; JPY 112.70-112.51; AUD 0.7558-0.7532;NZD 0.6819-0.6789

Dec Gold +0.4% at $1,280/oz; Dec Crude Oil +0.1% at $56.45/brl; Dec Copper +0.1% at $3.09/lb