Sample Category Title

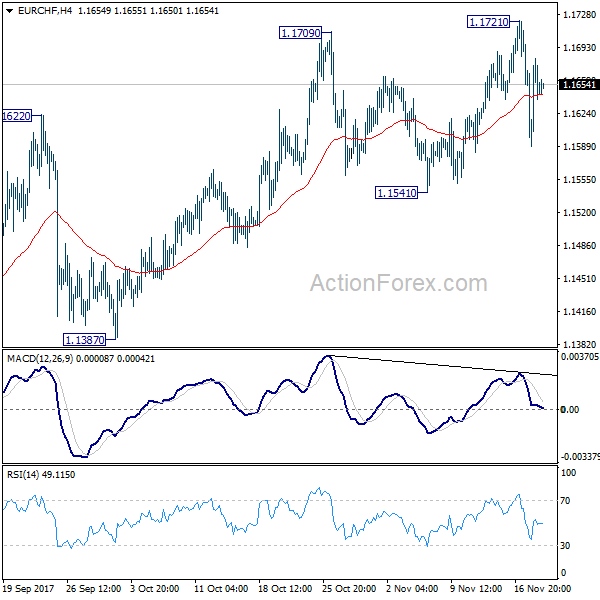

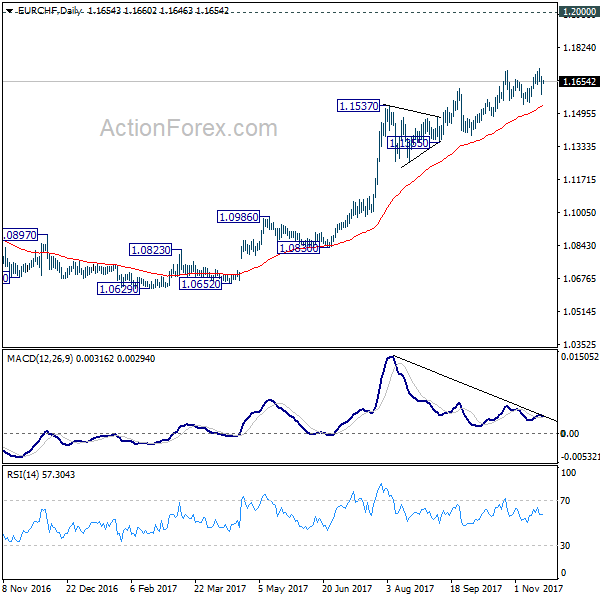

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1602; (P) 1.1642; (R1) 1.1694; More...

EUR/CHF's fall from 1.1721 was held well above 1.1541 support and quickly recovered. Intraday bias is turned neutral first. On the downside, considering bearish divergence condition in 4 hour MACD and daily MACD, decisive break of 1.1541 will confirm topping and turn near term outlook bearish for 1.1355 key support. Nonetheless, on the upside, break of 1.1721 resistance will resume recent up trend towards 1.2 key level.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1158) and possibly below.

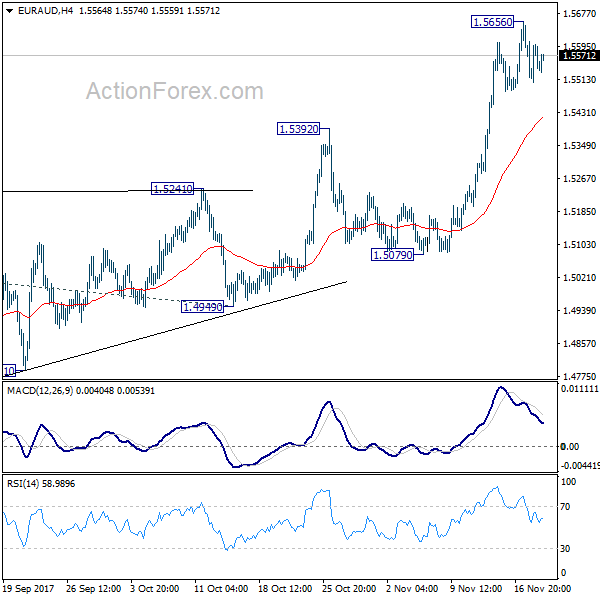

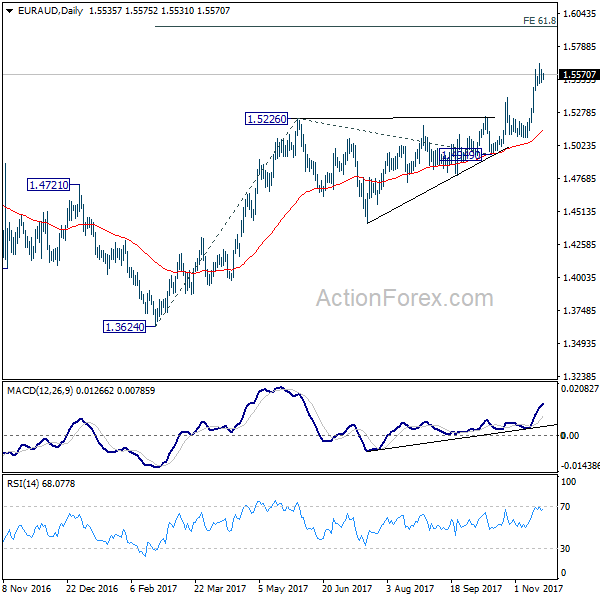

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5494; (P) 1.5548; (R1) 1.5592; More....

Intraday bias in EUR/AUD remains neutral for consolidation below 1.5656 temporary top. Downside of retreat should be contained by 4 hour 55 EMA (now at 1.5390) and bring rise resumption. Above 1.5656 will extend the rally from 1.3624 and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. Nonetheless, sustained break of 4 hour 55 EMA will bring deeper fall back towards 1.5079 support instead.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

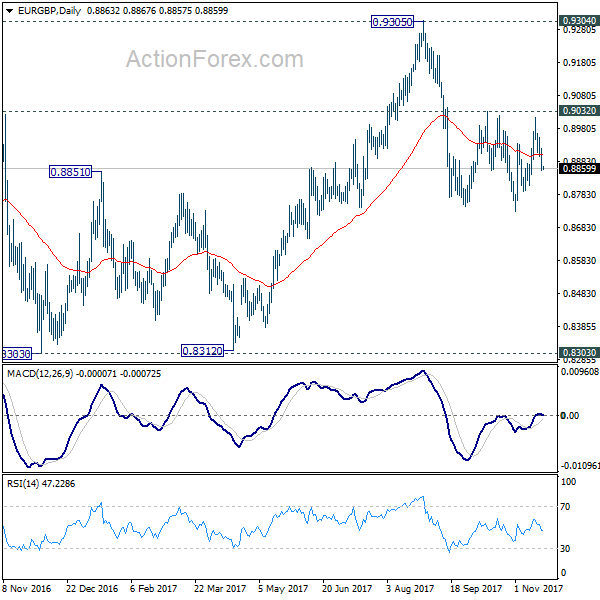

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8839; (P) 0.8880; (R1) 0.8905; More...

Intraday bias in EUR/GBP remains neutral as the cross is staying in range of 0.8732/0.9032. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the fall from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Euro Stays Weak on Germany Uncertainty but Loss Limited, Aussie Lower after RBA Minutes

Euro remains the weakest major currency for the week so far on political uncertainty in Germany. In addition, dovish comments from ECB President Mario Draghi is also weighing down the common currency. But after all, loss is limited, in particular against Dollar. EUR/USD is holding well above 1.1677 minor support and maintains near term bullish outlook. EUR/JPY breached 131.38 key near term support yesterday but quickly recovered. That's also helped by weakness in Yen, which pulled back on risk appetite and rebound in treasury yields. Dollar stays mixed as the rally attempt lacks follow through momentum. Australian Dollar weakens in Asian session as RBA minutes suggest interest rate to stay low for longer.

German President Steinmeier: Pause and reconsider your positions

After meeting with Chancellor Angela Merkel, German President Frank-Walter Steinmeier said that "we are now facing a situation that has never happened before in the history of the Federal Republic of Germany, that is for almost 70 years." After the coalition talk between CDU, FDP and Greens collapsed Steinmeier rejected the idea of new elections, but urged political parties to "pause and reconsider their positions". Words used were strong as Steinmeier said "the mission to form a government remains. You can not just hand back responsibility to the electorate." And, "all political parties elected to parliament must act for the common good. I expect a demonstration of readiness to form a government in the near future."

For now, the coalition talks will enter into extra time. But still, worst come to worst, a new election would be called if there is no progress in the negotiations. Recent survey shows that the outcome of another election would not be much different from the one held in September. Meanwhile, although Merkel pledges to run as a candidate again should there be a new election, the latest poll suggests that her popularity has slumped after the talks collapse. The Die Welt poll shows that 61.4% of people believe that she should not be the chancellor again. Apart from a minority government, new election and a return of FDP, a grand coalition is also an option. However, the price the SPD would ask for working with CSU/CDU again would be huge. Merkel not being the chancellor can be a pre-requisite for them to enter the negotiation.

ECB Draghi: Stimulus still need to to secure a sustained return of inflation

ECB President Mario Draghi said that time is still needed for the improvements in labor market to "translate" into "more dynamic wage growth. And he emphasized the "re-calibration" of monetary policy is meant to "preserve the degree of monetary stimulus that is still necessary to secure a sustained return of inflation." ECB announced in October meeting to half the monthly size of asset purchase to EUR 30b, and extend the program to September next year.

Broad agreement among UK minutes to raise divorce offer

BBC reported that after discussions in a cabinet meeting, there is broad agreement among ministers in UK for the government to raise the divorce bill offer to EU. However, there was no substantial discussion on the amounts to be raised. There were reports that UK would double the GBP 20b offered to GBP 40b but Downing Street has rubbished such rumors. European Council President Donald Tusk has set a deadline of completing the sufficient progress before December 14/15 summit, for moving on to trade agreements. And EU chief negotiator Michel Barnier has already be clear that UK has to "settle the accounts accurately" before starting trade talks.

RBA warned of "considerable uncertainty" over wage growth.

RBA signaled in the November meeting minutes that interest rates will remain at current historical level, maybe longer than originally expected. In particular, the central bank warned of "considerable uncertainty" over wage growth. It noted that "although unemployment rates had continued to fall, wage growth had been slow to increase in many economies and core inflation had remained low." And, retreat price inflation had remained subdued as competitions "continued to restrain price rises". Overall, "members noted that the outlook for inflation would be influenced by the persistence of heightened competitive pressures, the outlook for wage growth and the speed with which wage costs might flow through to higher prices."

Fed chair Yellen will step down from Board next year

Fed chair Janet Yellen announced yesterday that she will step down from the Federal Reserve Board of governors in February, after her role as chair ends. Originally, she could stay in the board until 2024. Yellen said in her resignation letter that "I am gratified that the financial system is much stronger than a decade ago. And she added that "I am also gratified by the substantial improvement in the economy since the crisis." There are now altogether four spots in the seven-member board to be filled. And that is seen as a golden opportunity for President Donald Trump to reshape monetary policy direction of the US.

Looking ahead

The economic remains light today. A main focus will be on UK inflation hearing. Swiss will release trade balance in European session. UK will release public sector net borrowing and CBI trends total orders. Canada will release wholesale sales. US will release existing home sales.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8839; (P) 0.8880; (R1) 0.8905; More...

Intraday bias in EUR/GBP remains neutral as the cross is staying in range of 0.8732/0.9032. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the fall from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | RBA Minutes Nov | ||||

| 04:30 | JPY | All Industry Activity Index M/M Sep | -0.40% | 0.10% | ||

| 07:00 | CHF | Trade Balance Oct | 3.21B | 2.92B | ||

| 09:30 | GBP | Public Sector Net Borrowing Oct | 6.6B | 5.3B | ||

| 11:00 | GBP | CBI Trends Total Orders Nov | 3 | -2 | ||

| 13:30 | CAD | Wholesale Trade Sales M/M Sep | 0.40% | 0.50% | ||

| 15:00 | USD | Existing Home Sales Oct | 5.42M | 5.39M |

Market Morning Briefing: The Aussie Has Surprised By Trying To Break Below Immediate Support Levels

STOCKS

The Stock indices are all trading slightly higher today. Sideways consolidation is possible in the near term if not a immediate rise to higher levels.

Dow (23430.33, +0.31%) is almost stable. But while above 23200, there is some scope of eventually rising towards 23600. Sideways consolidation is likely to continue just now.

Dax (13058.66, +0.50%) is holding well above immediate support near 12900 and could at least trade sideways within 13000-12900 (max extension of 100points on either side), if not rising sharply above 13100 just now. A sustained break above 13100 could initiate a fresh rally back towards 13200-13300 in the near term.

Nikkei (22488.38, +1.02%) has got some support near 22200 and the bounce from there yesterday may sustain this week. Trade within 22800-22000 is likely in the next couple of sessions.

Shanghai (3408.64, +0.48%) tested levels near 3337 yesterday before closing near 3400. The sharp bounce from the low yesterday is indicative of near term bullishness and the index could head towards 3450 and higher in the near term.

Nifty (10298.75, +0.15%) could rally towards 10400-10500 in the coming sessions while above 10200. Note that 10200 is a decent medium term support and is likely to hold for now.

COMMODITIES

Gold (1279.87) has come off on slight rise in the US Dollar Index. If the Dollar Index continues to rise towards 94.50, there could be some more downside in Gold in the near term.

Brent (62.33) and WTI (56.50) are trading higher and look bullish for the near term. Brent could move up towards 63-64 while WTI is likely to head towards 58-59 levels.

Copper (3.0835) is now testing the earlier support turned resistance at 3.10 and while that holds, it could push the price back towards 3.05-3.00 levels in the near term.

FOREX

Dollar Index (94.05) has near term channel support near 93.50/60 and while that holds, the downside looks limited just now. While above 93.50/60, the index could gradually move up towards 94.50-95.00 soon. Near term looks bullish.

EURO (1.1735) could come off towards 1.1700 where a decent support could push it back to levels near 1.175-1.180, preventing a fall to 1.1650 just now. Either the price breaks below 1.17 to open up lower levels of 1.1650-1.1620 or bounces back from 1.17 itself, targeting higher levels of 1.18 in the medium term.

Dollar-Yen (112.538) moved up after testing 111.88 on the downside. While there is some scope of the US-Japan 10Yr yield spread (2.33%) to rise towards 2.36%, some rise in Dollar Rupee is possible in the near term with an eventual fall towards 111.

The Pound (1.3246) is headed towards 1.33 as expected. Near term looks bullish. A rejection from 1.33 or slightly higher levels is expected in the medium term.

The Aussie (0.7538) has surprised by trying to break below immediate support levels. But while above 0.75, there is still some hope of a bounce back towards 0.76-0.77 in the coming sessions.

Dollar-Rupee (65.1150) could test 65.25 on the upside. Overall broad trade region could be expected within 64.90-65.25 levels.

INTEREST RATES

The US yields are all testing support. There has been a slight bounce in the yields compared to yesterday’s levels, while the support holds, some more rise is on the cards. The 5Yr (2.09%), 10Yr (2.36%) and the 30Yr (2.78%) are trading higher and looks bullish in the near term.

The US-Japan 10Yr (2.33%) surprisingly bounced back instead of heading to lower levels. However, the current rise could be temporary as the medium term resistance near 2.36% may hold and push the yield spread back towards 2.25% and lower in the sessions to come. For now, while the yield spread is up, Nikkei and Dollar Yen could see interim rises in an overall medium term bearish scenario.

The German-US 10Yr (-2%) could test medium term support near -2.05% and while that holds a bounce back in both the yield spread and Euro is possible maybe by the end of the week.

EUR/GBP Intraday Price Action Offering Something For The Shorts

Continuing with the EUR/GBP short side narrative that we have been following, I wanted to highlight the textbook price action that we saw during yesterday's trading session.

But first up, I have to include the higher time frame, EUR/GBP daily chart for context. It's almost the same as yesterday's blog, so if you've been following along or clicked the link above, you can skip right ahead!

EUR/GBP Daily:

The daily resistance zone that I've marked is pretty self explanatory. With some of the wicks going through it like that, you could probably draw it a little wider to the upside if you please.

But as it's a higher time frame level that we are using to gauge direction rather than entries, it doesn't really matter. The level has held and that's all that matters when it comes to day trading around these types of higher time frame zones.

Now let's get to the juicy part for the traders, with a look at an intraday, EUR/GBP 15 minute chart.

EUR/GBP 15 Minute:

After the higher time frame resistance zone holds, it becomes all about looking for shorts on the intraday charts. Any short term support that can be retested as possible resistance gives a nice entry that keeps you in tune with the ebbs and flows of the market.

To And Fro , Here We Go

To and Fro, here we go

Firming US yields overnight contributed to a stronger USD outperformance with the DXY breaching the 94 resistance level. While economic data drivers were few and far between dealer’s were left to chew on remarks by European Central Bank Mario Draghi, German Politics and of course the market’s fascination with yield curve developments

The Euro

Mario Draghi didn’t mention anything particularly penetrating but continues to signal that the Eurozone is still dependant on a healthy measure of monetary stimulus given the lack of inflation. This was enough to convince traders that 1.1800 was not a happy place to be caught long and the EUR subsequently slid lower through most of the NY session

Uncertainty over the Jamacia accord continues to weigh on near-term sentiment but given the outcome could be more positive pro-European-Union, ultimately until something permanently snaps the noise is only mildly EUR negative. But frankly, there was nothing positive priced into the market for a Jamaica coalition, so this should not be a reliable driver for EUR sentiment although it will likely weigh on top side progress near term.

In fact, those of us that trade the single currency are desensitised to Monday morning EU political noise as given the adroit negotiating skills of European politicians, cooler heads always seem to prevail. With that in mind, dealers will continue to focus on ECB expectations and continental growth as the critical drivers in Eur sentiment.

The Japanese Yen

USDJPY rallied from the NY open, climbing from ¥112.09 to ¥112.70, snapping a one-week downtrend. While there was no specific news other than to guess that investors are expecting an early holiday present in the form of tax reform, A moderately better risk tone and rising US Treasury yields supported the dollar momentum

Overall Wall Street finished in the green and for all intensive purposes ignored Trump calling North Korea a “state sponsor of terrorism” and promising new sanctions while exhibiting little emotion to Janet Yellen resignation

The Australian Dollar

The Australian dollar continues to trade in no man’s land as the RBA monetary policy meeting minutes failed to ignite any significant action despite tacking to a more dovish course. Again, and without sounding like a broken record, I suspect the next big move for the Aud will be US dollar driven so I think we could be back on fed watch.

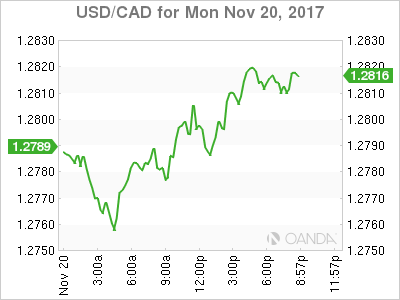

USD/CAD Canadian Dollar Lower Ahead Of Short Trading Week

The Canadian dollar depreciated on Monday versus the US dollar. Oil prices fell as higher production from the US is putting downward pressure on prices ahead of the Organization of the Petroleum Exporting Countries (OPEC) meeting on November 30. The production cut agreement between the OPEC and other major producers has added stability to oil prices, but has also opened up the opportunity for Brazil, Canada and the US to increase production.

NAFTA talks are ongoing in Mexico City with comments circling that the talks are close to a standstill as the US is not budging from its America First demands and Canada and Mexico will not introduce a counter proposal to the increase in US content in North American autos. The US could end up losing 24,000 jobs if it stick to its higher US content demands, and it could even be a worse loss if NAFTA is terminated, but that hasn’t stoped American negotiators to stick to their guns.

The loonie started the week under pressure with low oil prices and NAFTA negotiations devoid of any progress. The failure of the German Chancellor to form a coalition set off a sell off in the single currency during the Asian session. Angela Merkel has brushed off her resignation and instead is focused in a new round of elections instead of opting for a minority government.

The USD/CAD gained 0.33 percent on Monday. The currency pair is trading at 1.2812 at the start of a trading week that will be shortened by the American thanksgiving holiday starting Thursday. There are two big Canadian data releases this week. Canadian wholesale sales will be released on Tuesday, November 21 at 8:30 am and later in the week retail sales will be published on Thursday, November 23 at 8:30 am EST.

The U.S. Federal Reserve will publish the minutes form its November meeting on Wednesday, November 22 at 2:00 pm EST. There will be more clues on where certain policy makers stand regarding inflation, but the market is still pricing in a 99 percent probability of a US rate hike in December.

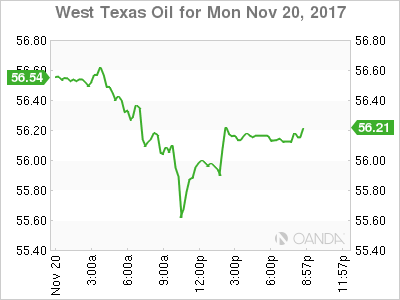

Oil prices fell on Monday. West Texas Intermediate prices are trading at $56.18 after opening at around $56.54 in the Asian session. Higher than expected US weekly inventories have offset comments of an extension to the crude output agreement cut by OPEC and other major producers. The current deal expires in March and while Russia has been supportive they have remained noncommittal which is why the meeting next week is so important to see where all producers stand on an extension.

The rise of the USD triggered by German coalition uncertainty was a negative for crude. Saudi Arabia was not in the spotlight this weekend after the events of the past two weeks have consolidated the power of Crown Prince Mohammed bin Salman. Russia and Saudi Arabia remain the core of the production cut agreement and compliance. If Russia pledges an extension to the deal, it is expected the OPEC members and the other 10 non-OPEC will follow suit.

Market events to watch this week:

Monday, November 20

7:30 pm AUD Monetary Policy Meeting Minutes

Tuesday, November 21

4:05 am AUD RBA Gov Lowe Speaks

6:00 pm USD Fed Chair Yellen Speaks

Wednesday, November 22

8:30 am USD Core Durable Goods Orders m/m

8:30 am USD Unemployment Claims

10:30 am USD Crude Oil Inventories

2:00 pm USD FOMC Meeting Minutes

4:45 pm NZD Retail Sales q/q

Thursday, November 23

4:30 am GBP Second Estimate GDP q/q

8:30 am CAD Core Retail Sales m/m

11:30 am CHF SNB Chairman Jordan Speaks

Gold Volatility Continues Over Tax Reform Prospects

Gold has posted sharp losses in the Monday session. In North American trading, the spot price for an ounce of gold is $1277.84, down 1.2% on the day. On the release front, the sole event is CB Leading Index. The indicator gained 1.2%, well above the forecast of 0.6%. On Tuesday, the US will publish Existing Home Sales. As well, US Federal Reserve Chair Janet Yellen will speak at an event in New York City.

There was good news from US construction numbers on Friday. Building Permits for single-family homes jumped to 1.30 million, above the estimate of 1.25 million. The annualized pace of 839,000 building permits in October was the fastest since September 2007. Housing Start also sparkled, accelerating to 1.29 million, compared to an estimate of 1.19 million. The catalyst for the strong numbers were hurricanes Harvey and Irma, which caused massive damage in the southern part of the US. With rebuilding efforts well underway, construction numbers should remain strong in the fourth quarter.

As investors keep a close eye on tax reform, gold prices continue to fluctuate. Gold prices jumped 1.2% on Friday, only to surrender those gains on Monday. President Trump won a major victory on Thursday, as the House of Representatives passed its version of the tax bill, by a vote of 227-205. However, with the vote largely based on party lines, Republicans will have a tougher battle passing the Senate version of the bill, as the Republicans have a slim majority of 52-48. The tax legislation provides major tax relief and cut corporate taxes from 35% to 20%, and if Congress does enact a new tax code, the US dollar could make strong gains, at the expense of gold.

The Quiet Trade

Everything else equal, what's the trade? That's the question we pose as markets drift in a holiday-shortened week. The pound was the top performer while the euro lagged. The RBA meeting minutes are up next. A 2nd EUR trade was issued today with 3 charts & notes as part of the "EUR Tactical Set-up".

German politics will likely remain the major headline-maker in a week with a light economic calendar and with US Congress on break. Merkel and her potential coalition partners have reached an impasse and are talking about a fresh election. The President is attempting to broker a deal and Merkel said she doesn't want to try to govern with a minority.

Expect some twists and turns but none of the potential scenarios are likely to leave a major mark on the euro. Initially, EUR/USD slumped 70 pips on the headlines but it recovered. Later in the day, EURUSD sagged again but that was part of a broader climb in the US dollar boosted by stronger than expected US LEI report.

And that brings us to the quiet trade. Risk assets have benefitted in nearly every environment over the past decade but the best backdrop has been the days with little-to-no news. That was the story on Monday and it's likely to be the same (especially in New York trading) for the rest of the week.That could help to underpin a minor rebound in the yen crosses and a creep higher in Treasury yields.

Expect higher volatility in Asia and Europe. The Aussie could be on the move when the RBA meeting minutes are released at 0030 GMT. Commentary about wages and financial stability is key along with insights about lower inflation projections.

Another event to watch is the 0430 GMT Japanese all industry activity index. It's forecast to fall 0.4% m/m.