Sample Category Title

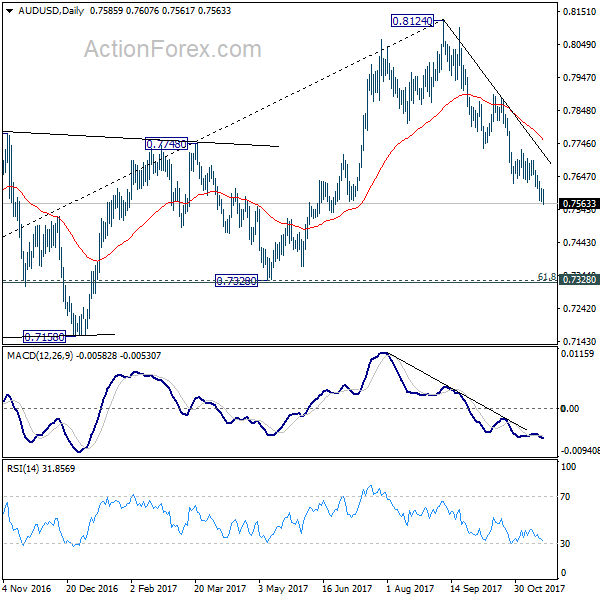

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7564; (P) 0.7586; (R1) 0.7610; More...

AUD/USD's decline continues today and intraday bias remains on the downside. Current fall from 0.8124 is expected to target next key cluster level at 0.7322/8. On the upside, above 0.7607 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 0.7729 resistance holds.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

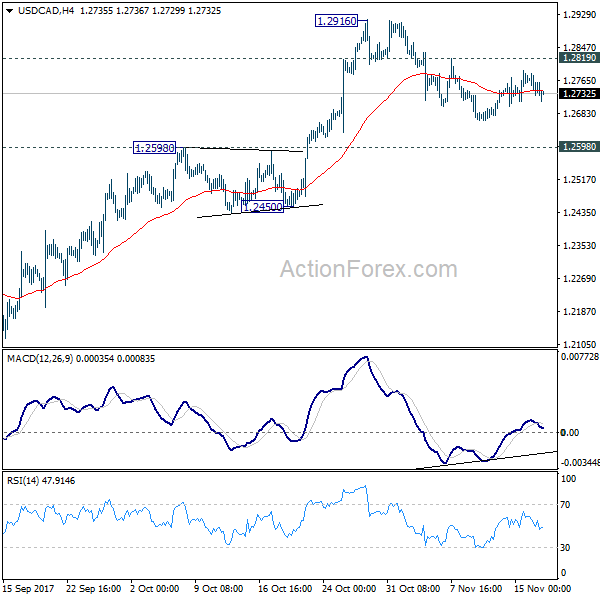

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2728; (P) 1.2755; (R1) 1.2783; More....

Intraday bias in USD/CAD remains neutral and near term outlook stays bullish as long as 1.2598 resistance turned support holds. On the upside, above 1.2819 minor resistance will turn bias back to the upside for 1.2916 high first. Break there will extend the rise from 1.2061 to 38.2% retracement of 1.4689 to 1.2061 at 1.3065. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2916). Near term outlook will be turned bearish in this case.

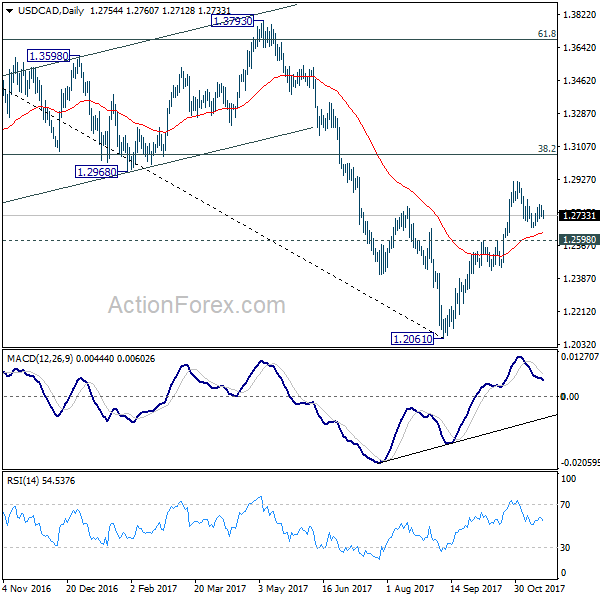

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

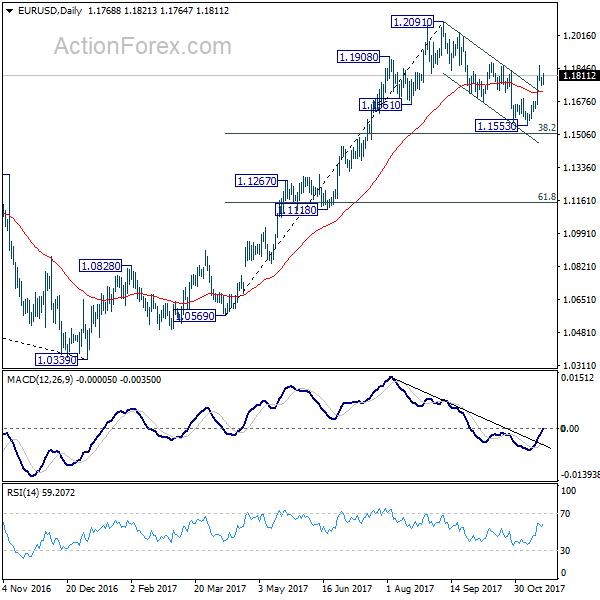

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1749; (P) 1.1774 (R1) 1.1793; More...

Intraday bias in EUR/USD remains neutral for consolidation below 1.1860 temporary top. Outlook is unchanged that correction from 1.2091 has completed at 1.1553 already. Further rise is expected. Above 1.1860 will target 1.2091 high. However, break of 1.1677 support will turn focus back to 1.1553 low instead.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1346) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

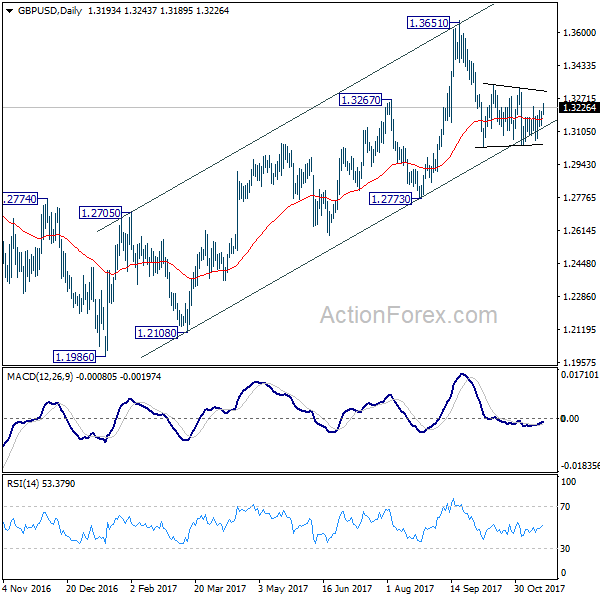

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3148; (P) 1.3178; (R1) 1.3221; More....

GBP/USD is still bounded in range of 1.3038/3337 and intraday bias stays neutral at this point. In case of further rise, upside should be limited below 1.3337 resistance to bring fall resumption. Break of 1.3038 will now resume decline from 1.3651 to 1.2773 key support level. However, decisive break of 1.3337 will indicate that pull back from 1.3651 is completed and medium term rise from 1.1946 is resuming.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Current development is starting to favor that corrective rebound from 1.1946 low has completed at 1.3651. Decisive break of 1.2773 will confirm this bearish case and target a test on 1.1946 low next, with prospect of resuming the low term down trend. Nonetheless, break of 1.3320 resistance will restore the rise from 1.1946 for 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

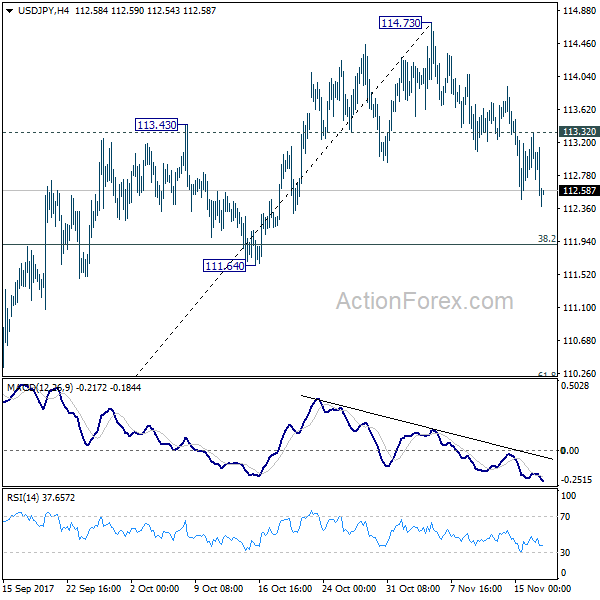

US Dollar Pressured Vs Japanese Yen Below 113.50

Key Highlights

- The US Dollar started a new downside wave from the 114.70 swing high against the Japanese Yen.

- There is a key contracting triangle forming with resistance at 113.50 on the 4-hours chart of USD/JPY.

- The US Initial Jobless Claims for the week ending Nov 11, 2017 posted a rise from 239K to 249K.

- Today in the US, the Building Permits figure for Oct 2017 will be released which is forecasted to register a change of +2.0%.

USDJPY Technical Analysis

The US Dollar is in a slow and steady downtrend below 113.50 against the Japanese Yen. The USD/JPY pair is likely to remain under pressure as long as it is below 113.50.

Looking at the 4-hours chart, there was a sharp decline from 113.90 to 112.49. Later, the pair started an upside correction, but it faced resistance near the 50% Fib retracement level of the last decline from 113.90 to 112.49.

It seems like there is a key contracting triangle forming with resistance at 113.50. Above the triangle resistance, the 100 simple moving average (red, 4-hour) is positioned at 113.65.

Therefore, the 113.50 and 113.65 levels are important resistances for an upside move in USD/JPY. As long as the pair is below 113.50, it remains at a risk of a downside reaction toward 112.50 or lower.

US Initial Jobless Claims

Recently in the US, the Initial Jobless Claims figure for the week ending Nov 11, 2017 was released by the US Department of Labor. The forecast was slated for a decrease from the last reading of 239K to 235K.

However, the actual result was on the lower side as there was an increase in claims from 239K to 249K. With this, the 4-week moving average now stands at 237,750, which is 6,500 more than the last 231,250.

The report added:

The advance number for seasonally adjusted insured unemployment during the week ending November 4 was 1,860,000, a decrease of 44,000 from the previous week’s revised level. This is the lowest level for insured unemployment since December 29, 1973 when it was 1,805,000.

Overall, the USD/JPY pair will most likely remain in the bearish zone as long as the 113.50 resistance is intact in the near term.

Economic Releases to Watch Today

Euro Zone Current Account for Sep 2017 – Forecast €30.2B versus €33.3B previous.

US Housing Starts Oct 2017 (MoM) – Forecast 1.185M, versus 1.127M previous.

US Building Permits Oct 2017 (MoM) – Forecast 1.247M, versus 1.215M previous.

Canadian Consumer Price Index Oct 2017 (MoM) – Forecast +0.1%, versus +0.2% previous.

Canadian Consumer Price Index Oct 2017 (YoY) – Forecast +1.4%, versus +1.6% previous.

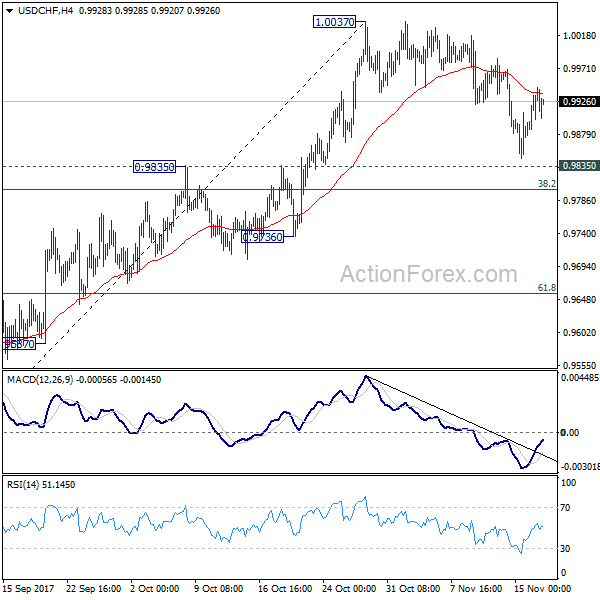

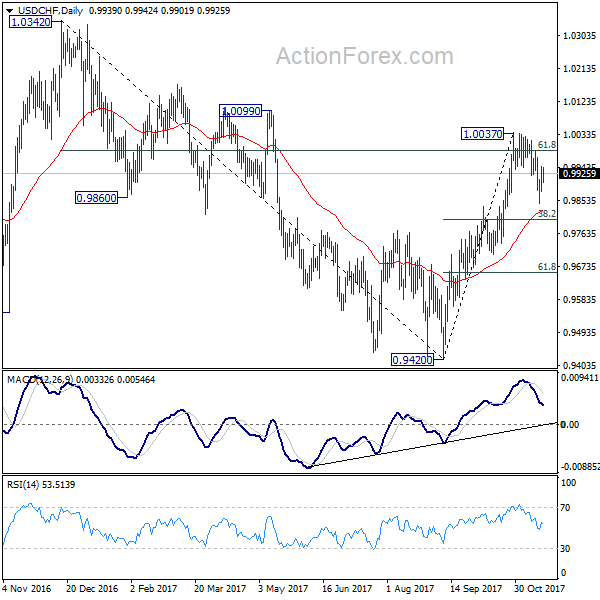

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9899; (P) 0.9922; (R1) 0.9966; More....

Intraday bias in USD/CHF remains neutral for the moment. The rebound ahead of 0.9835 support retained near term bullishness and favors further rally. On the upside, firm break of 1.0037 resistance will extend the rise from 0.9420 and target 1.0342 high. However, firm break of 0.9835 will argue that whole rebound form 0.9420 is completed and turn outlook bearish. In that case, USD/CHF should target 61.8% retracement of 0.9420 to 1.0037 at 0.9565 and possibly below.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could is a medium term up move and should target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9736 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Market Update – Asian Session: BoJ Cuts Purchases In Daily JGB Operation

Headlines/Economic Data

Japan

The Nikkei opened +1.1%, but has since pared gains: Fast Retailing +0.8%, Sony +0.9%; Softbank -1%

USD/JPY lower by over -0.3%

BOJ cut planned purchases of 1-3 year JGBs in daily operation (first cut since April); Cuts planned purchases of 1-3 year JGBs to ¥250B from ¥280B; Raised planned purchases of Treasury bills to ¥500B v ¥100B prior

Australia

The S&P ASX 200 opened +0.5%; Financials Index +0.6% Consumer Discretionary Index +0.5%, Utilities Index -0.4%; Virgin Australia (says not aware of any unannounced information), Santos Energy +1%

(AU) Australia sold A$400M in 2033 Bonds, avg yield 2.8774%, bid to cover 2.84x

China

Shanghai Composite Opened -0.2%, Hang Seng opened +0.7%; Hang Seng Information Technology Index +1.7%, Hang Seng Financials Index +0.8%, Hang Seng Materials Index -1.3%; Tencent +1.5% (all-time high)

PBOC reduces injected amount in daily open market operation: CNY30B v CNY330B injected in 7,14 and 63-day reverse repos prior; Net drain CNY10B v CNY310B injection prior; Weekly net injection CNY810B v CNY230B drain w/w

MOF sold 50-year bonds at lower than expected yield: Sold 50-year bonds: Avg yield 4.37% v 4.46%e

MOF also sold 3-month bills at avg yield of 3.7644%

(CN) PBOC set yuan reference rate at 6.6277 v 6.6286 prior (Prior close: 6.6283)

(CN) State Owned Enterprises (SOEs) in Shanghai planning CNY800B/per year in new investments as part of plan to accelerate restructuring of these companies – China Daily

Other Asia:

India

Indian assets rally following sovereign upgrade at Moody’s: Sensex +1%; Indian Rupee (INR) +0.6%; 10-year bond yield down over 10bps.

(IN) MOODY'S RAISED INDIA SOVEREIGN RATING TO BAA2 FROM BAA3; Outlook revised to Stable from Positive: Moody's rating for India is now above the BBB- ratings (lowest level of investment grade) that both S&P and Fitch have for the country.

South Korea

The Kospi index opened +0.2% and traded at intraday record high earlier today; Samsung +0.9%, Hynix +0.8%

Korean Won (KRW) flat and pares earlier gain amid warning from Bank of Korea (BoK)

Won has appreciated ‘fast’ in a short time; reiterates FX authorities closely monitoring markets, said an unnamed BoK official

On Thursday’s session, the Korean Won rallied by more than 1% to trade at the highest levels since Sept 2016 versus the US dollar.

Malaysia

Q3 Y/Y GDP beat estimates supported by private spending, along with the services and manufacturing sector, says Malaysia’s Central Bank: (MY) MALAYSIA Q3 GDP Y/Y: 6.2% V 5.7%E

Ringgit (MYR) +0.1%

Singapore

Straits Times equity index opened +0.7%

Oct Non-Oil Domestic Exports above estimates supported by China: (SG) Singapore Oct Non-Oil Domestic Exports M/M: 12.5% v 7.7%e; Y/Y: 20.9% v 11.9%e; Non-oil Domestic Exports to China +53.3% y/y

US

S&P 500 Futures -0.1%, Nasdaq Futures flat

Afterhours Movers: FOXA (21st Century Fox) Comcast reportedly approached Fox over possible bid; not clear if Comcast sought all of Fox or only some assets; +8.5% afterhours; ROST (Ross Stores) Reports Q3 $0.72 v $0.67e, Rev $3.33B v $3.27Be; Raises FY17 $3.24-3.28 v $3.22e (prior FY17 $3.16-3.23); +7.8% afterhours; WSM (Williams-Sonoma) Reports Q3 $0.79 v $0.84e, Rev $1.30B v $1.29Be; Guides Q4 $1.49-1.64 v $1.66e, Rev $1.61-1.68B v $1.64Be; -8.1% afterhours

Fed Speak: (US) Fed Williams (moderate, non-voter): Reiterates 4 rate hikes by end-2018 'reasonable' guess for policy; Open to raising rates in Dec 2017 or holding steady

Tax Reform: (US) Senate Finance Committee advances Republican tax legislation by vote of 14 to 12; full Senate expected to consider the measure during the week of Nov 27th; The revised tax proposal by the Senate is said to target the carried interest break, according to a separate press report

During the NY afternoon on Thursday, House of Representatives passed GOP tax reform bill (as expected)

Politics: (US) In mid-Oct, Special counsel Robert Mueller said to have issued subpoena to President Trump’s election campaign in relation to documents on Russia – US press

Levels as of 00:30ET

Nikkei +0.1%, Hang Seng +0.7%; Shanghai Composite -0.6%; ASX200 +0.2%, Kospi +0.1%

Equity Futures: S&P500 -0.1%; Nasdaq100 flat; Dax -0.2%; FTSE100 -0.3%%

EUR 1.1766-1.1822 ; JPY 112.40-113.15; AUD 0.7569-0.7608 ;NZD 0.6842-0.6884

Dec Gold +0.4% at 1,283/oz; Dec Crude Oil +0.2% at $55.27/brl; Dec Copper +0.3% at $3.062/lb

The US Equity Market Rebounded Yesterday

Market movers today

Today, we have a very light data calendar with no global market movers being released.

ECB President Mario Draghi will be speaking again, followed by Bundesbank President Jens Weidmann later in the day. They are scheduled to deliver keynote addresses at the Frankfurt European Banking Congress and markets will again watch out for any clues about ECB policy during this otherwise relatively unevent ful day.

The Netherlands is up for review by S&P. The Netherlands is ‘AAA/stable' and we do not expect any change to either the rating or the out look.

Selected market news

The US equity market rebounded yesterday as the odds of a corporate tax cut are rising after the House of Representatives passed its version of the tax bill. This is a key milestone for President Trump in changing the tax code. There are still tough challenges ahead as it needs to pass in the Senate, where the Republicans only have a two-seat majority.

The 10Y US Treasuries came under pressure on the back of the tax plan and 10Y US Treasury yields rose more than 5bp, while the USD strengthened relative to EUR and JPY.

The positive sentiment in the equity market has continued in Asia this morning with a rise in stock prices across the region.

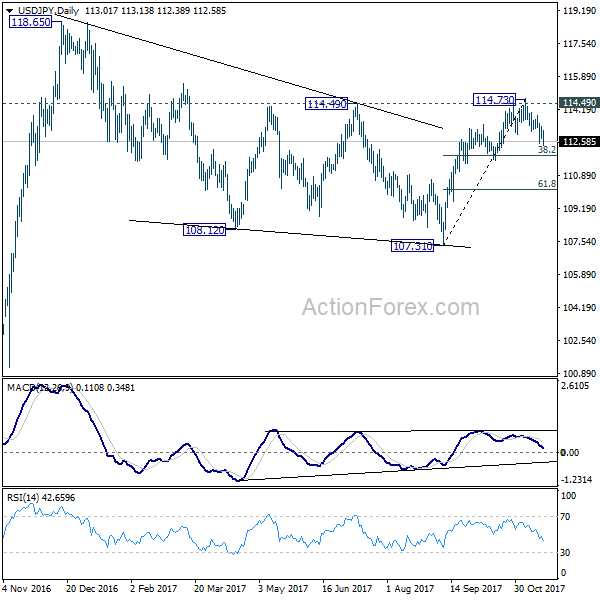

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.75; (P) 113.03; (R1) 113.34; More...

USD/JPY's fall from 114.73 continues today and intraday bias stays on the downside for 38.2% retracement of 107.31 to 114.73 at 111.89 first. Sustained break of 111.64 support will now argue that rise from 107.31 has completed. In that case, USD/JPY should target 61.8% retracement at 101.14. On the upside, break of 113.32 minor resistance is needed to confirm completion of the fall. Otherwise, near term outlook will now stay cautiously bearish.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

US Stocks Surged as Tax Bill Passed in House and Senate Finance Committee, Dollar Stays Soft

The US markets responded positively to the passage of the tax bill in House and in Senate Finance Committee. DOW jumped 187.08 pts, or 0.8% to close at 23458.36. Technically, it defended 23251.1 key near term support and maintained bullishness. Focus is back on historical high at 23602.1. NASDAQ has indeed made new record at 6806.67 before closing at 6793.29, up 1.3%. 10 year yield also showed some resilience and ended up 0.026 at 2.361, keeping itself well above 2.304 key support. In the currency markets, Dollar remains generally soft, though, except versus Aussie and Kiwi. Euro and Yen would probably end the week as the strongest ones.

House passed tax bill by 227-205

The House passed its version of tax reform bill with a 227-205 vote. The outcome had been widely anticipated as Republicans control 240 out of 435 seats there. Despite the passage of the bill, there were 13 Republicans who did not vote for the bill. Many of them defected as they were dissatisfaction with the elimination of some tax deduction. The House bill eliminates the deduction for state and local income taxes, but preserves the deduction for property tax up to US$ 10k. Yet, the partial preservation was not sufficient for the policymakers from high-tax states such as New York and New Jersey, and California and North Carolina.

Senate Finance Committee passed tax bill by 14-12

The House is presumably the easier hurdle for the tax reform bill. The next is the Senate. The Senate Finance Committee also approved the their version of tax bill yesterday, with 14-12 vote. The bill is expected to be considered on floor the week after Thanksgiving. Given the slim majority of Republicans in the senate, there is little margin for error. They could only afford to see two defections, one filled up by Ron Johnson already. Susan Collins has also expressed some concerns. Meanwhile, it should also be noted that there are some major differences between the House's version and the Senate's version. And the reconciliation effort is huge.

San Francisco Fed Williams urged monetary policy rethink

San Francisco Fed President John Williams continued his push for rethinking global monetary policies. He noted that the major economies of the world are all facing slower growth and lowest interest rates. And there is a need to expand to toolkits to prepare for the time when stimulus is needed. He said that "we will all be better able to contain the next economic recession if we develop approaches that succeed even when many countries are simultaneously constrained by the lower bound." Interest rate was the traditional convention tool. Then there were asset purchases and forward guidance, widely used in recent recession. Some countries adopted negative interest rates. And Williams also tried to push so called price-level targeting and also nominal-income targeting. He said that "each of these alternatives has significant advantages and disadvantages, which need further careful study and discussion."

Regarding the current situation, Williams support another hike in December. He said that "my view is that a perfectly reasonable path for policy would be one more increase this year, and three next year."

Dallas Fed Kaplan "very open-minded" about December hike

Dallas Fed President Robert Kaplan said his is "very open-minded" about "considering taking a next step in removing accommodation at upcoming meetings." He pointed out that unemployment at 4.1% is expected to fall further in a "deviation" from Fed's full employment mandate. And, "if the deviation on the full employment gets big enough that would be, for me, enough of reason to still remove accommodation, take another step." And, "prudent risk management means some action to remove accommodation gradually and patiently". He also emphasized that "it's not that you have see you are meeting both, then you move", regarding Fed's dual price and employment mandate.

ECB Villeroy de Galhau: Follow the path of gradual normalization

ECB Governing Council member Francois Villeroy de Galhau said that "we will clearly follow this path of gradual normalization, with caution but combining the whole range of our instruments - and there shouldn't be excessive focus on the net purchases of assets." He added that "monetary policy cannot be the only game in town, and therefore we should not overburden it,"

UK Brexit Secretary Davis: Incredibility unlikely for no-deal Brexit

UK Brexit Secretary David Davis said that it's "incredibly unlikely" there will be a no-deal Brexit. And he hopes that the next round of negotiation with EU will start before Christmas. But he also warned not to "politics above prosperity" in the post Brexit relationship with EU. Davis would want to seek a "deep and comprehensive free trade agreement" with EU. And continue "continued close cooperation in highly regulated areas such as transport, energy and data".

On the data front

New Zealand business manufacturing index dropped to 57.2 in October. PPI input rose 1.0% qoq in Q3, PPI output rose 1.0% qoq too. Eurozone current account is the only feature in European session. Canada will release CPI while US will release housing starts later in the day.

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.75; (P) 113.03; (R1) 113.34; More...

USD/JPY's fall from 114.73 continues today and intraday bias stays on the downside for 38.2% retracement of 107.31 to 114.73 at 111.89 first. Sustained break of 111.64 support will now argue that rise from 107.31 has completed. In that case, USD/JPY should target 61.8% retracement at 101.14. On the upside, break of 113.32 minor resistance is needed to confirm completion of the fall. Otherwise, near term outlook will now stay cautiously bearish.

In the bigger picture, medium term rise from 98.97 (2016 low) is not completed yet. It should resume after corrective fall from 118.65 completes. Break of 114.49 resistance will likely resume the rise to 61.8% projection of 98.97 to 118.65 from 107.31 at 119.47 first. Firm break there will pave the way to 100% projection at 126.99. This will be the key level to decide whether long term up trend is resuming. However, firm break of 111.64 support will dampen this view and turn focus back to 107.31 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Oct | 57.2 | 57.5 | 57.6 | |

| 21:45 | NZD | PPI Input Q/Q Q3 | 1.00% | 1.20% | 1.40% | |

| 21:45 | NZD | PPI Output Q/Q Q3 | 1.00% | 1.40% | 1.30% | |

| 9:00 | EUR | Eurozone Current Account (EUR) Sep | 30.2B | 33.3B | ||

| 13:30 | CAD | CPI M/M Oct | 0.10% | 0.20% | ||

| 13:30 | CAD | CPI Y/Y Oct | 1.40% | 1.60% | ||

| 13:30 | CAD | CPI Core - Common Y/Y Oct | 1.50% | |||

| 13:30 | CAD | CPI Core - Trim Y/Y Oct | 1.50% | |||

| 13:30 | CAD | CPI Core - Median Y/Y Oct | 1.80% | |||

| 13:30 | USD | Housing Starts Oct | 1.19M | 1.13M | ||

| 13:30 | USD | Building Permits Oct | 1.25M | 1.23M |