Sample Category Title

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

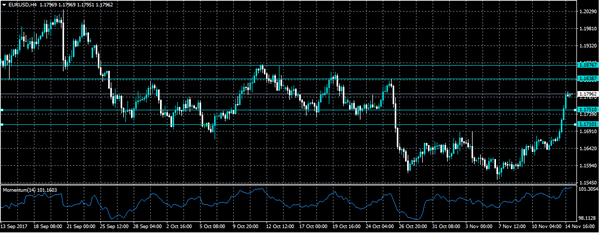

EUR/USD

Current level - 1.1793

The break through 1.1730 dynamic resistance signals a reversal of the whole downmove from 1.2090 and my outlook here is bullish, for a rise towards 1.1870 area. Initial support is found around 1.1775, followed by 1.1730 break-out area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1870 | 1.1870 | 1.1775 | 1.1690 |

| 1.2000 | 1.2090 | 1.1730 | 1.1550 |

USD/JPY

Current level - 113.10

The failure below 114.05 crucial resistance signals a bearish outlook, for a break through 113.00 area, towards 111.60 support. Crucial on the upside is the intraday high at 113.50.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.50 | 115.50 | 113.00 | 111.60 |

| 114.05 | 116.80 | 111.60 | 107.30 |

GBP/USD

Current level - 1.3150

Despite the failure at 1.3180 resistance, my outlook here is bullish above 1.3130, for a rise towards 1.3220 and 1.3340 later on.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3180 | 1.3220 | 1.3130 | 1.3020 |

| 1.3220 | 1.3340 | 1.3060 | 1.2760 |

Technical Outlook: EURUSD – Extension Of Strong Rally Penetrates Daily Cloud

The Euro holds firm tone on Wednesday following previous day’s strong rally when the single currency rallied 1.13%, boosted by upbeat German economic data and solid EU figures.

Fresh bullish extension in early European trading on Wednesday cracked key near-term barrier at 1.1815 (daily cloud base).

Cloud is spanned between 1.1815 and 1.1877 and marks solid resistance which may put strong near-term bulls on hold for corrective action. Scenario is signaled by strongly overbought slow stochastic on daily chart.

Broken 55SMA (1.1795) marks immediate support but dips may extend towards broken 100SMA (1.1736) before fresh attempts higher.

Firm bullish structure favors dip-buying strategy for further upside as 1.2092/1.1553 is completed and focus is turning higher.Break above daily cloud would generate strong bullish signal for extension towards 1.2000 zone.

Res: 1.1836, 1.1877, 1.1886, 1.1936

Sup: 1.1796, 1.1759, 1.1736, 1.1716

Dollar Struggles Ahead Of Inflation Figures, Aussie Takes A Knock After Wage Data

On Wednesday, the dollar performed poorly relative to its major counterparts in Asia, failing to recover on the back of a stronger euro and on continued concerns on the future of the US tax overhaul. Its Australian peer, however, was the worst performer during the session, as wage growth readings out of the country missed expectations.

The dollar index, which gauges the dollar's strength against six major currencies hovered around a three-week low of 93.56 (-0.25%) after stronger-than-expected GDP growth readings released out of Germany on Tuesday pushed the euro higher. Investors will now turn attention to CPI figures and retail sales due later today which could affect the Fed's rate decisions in the coming year. Consumer prices in October are anticipated to slow down by 0.2 percentage points to 2.0% y/y, while retail sales are forecasted to weaken by 1.5 percentage points to 0.1% m/m.

Meanwhile, the US House of Representatives is said to vote on their tax reform bill as soon as Thursday, while the Senate is also debating its version of the bill this week, with the Chamber desiring to approve the tax code after Thanksgiving. In other news, Senate Republicans decided to accomplish two policy mandates in a single piece of legislation, by embodying a key repealing component of Obamacare into their tax-cut plan.

Elsewhere, Japanese data on GDP growth, showed that the Japanese economy expanded for the seventh consecutive quarter (its longest expansion since 2001), growing by 1.4% y/y in the third quarter, slightly above the 1.3% forecasted but almost half the previous mark of 2.6% (upwardly revised from 2.5%). On a quarterly basis, the Japanese GDP rose in line with expectations by 0.3%, with a recovery in exports and business confidence offsetting the decline in consumption.

Dollar/yen was last trading at 112.97, 0.41% down on the day. However, the pair reacted little in the wake of the Japanese figures. Euro/dollar gained 0.11%, climbing to a fresh three-week high at 1.1816, as markets' optimism on eurozone's economy underpinned the currency.

In the UK, the debate of the Brexit bill which aims to determine the UK's strategy after it leaves the EU and therefore give some relief to business decision-makers is ongoing, with the European leaders, according to sources familiar with Brexit developments, signalling potential summits earlier next year and hence giving a second chance to the UK, as they see Brexit talks before December's summit failing.

Pound/dollar was mainly flat around 1.3169 ahead of UK labour data due to be released during the European trading hours.

The aussie tumbled by 0.63% during the session to a 4-month low of $0.7575 as Australian wages disappointed hopes for an improving labour market, hinting at downside risk to consumer spending and inflation. The numbers revealed that Australian wages increased steadily by 0.5% q/q, while projections were for a rise from 0.5% to 0.7%. The annual measure, though, inched up by 0.1 percentage points to 2.0% but fell short of expectations of 2.2% growth.

Turning to commodities, gold went up by 0.20% to $1,283.50 per ounce, whereas energy prices followed a downtrend after the API weekly report showed on late Tuesday an unexpected increase of 6.513 million barrels in US crude inventories (week ending November 10). Moreover, the IEA cut its oil demand growth forecast for 2017 and 2018, pressuring oil prices even further. WTI crude lost 0.95%, slipping to $55.17 per barrel and Brent fell by 0.92% to $61.63.

Global Stocks Lower, UK Jobs Data In Focus

A negative vibe was felt across financial markets during Tuesday's trading session, as the combination of tumbling oil prices and growing uncertainty over the outlook of the proposed U.S tax reforms affected risk sentiment. World stocks were under noticeable selling pressure yesterday, thanks to the absence of risk appetite, with investors now questioning the sustainability of the over-extended market rally.

Anair of caution has already infiltrated Asian markets this morning, with Asia Pacific equities in the red territory, following Wall Street's overnight decline. European stocks concluded Tuesday in a depressed fashion and may extend losses this morning amid, the lack of risk appetite.

Sterling wobbles ahead of UK jobs data release

The main risk event for the British Pound this morning will be September's U.K labour market report, which is widely expected to paint a similar picture to August's – record low unemployment,with a dash of subdued wage growth.

Although Britain's unemployment rate is at a 42-year low, the buzzkill remains, that little sign of rising pay growth continues to weigh heavily on sentiment. If average earnings struggle to pick up, consumers are likely to continue feeling the squeeze, especially when considering how inflation remains at a five-and-a-half year high, at 3%.

Sterling appreciated against the Dollar on Tuesday, but this has nothing to do with a change of sentiment towards the Pound;it is simply Dollar weakness. A disappointing U.K jobs report may inspire bears with enough inspiration to drag the GBPUSD back below 1.3150. From a technical standpoint, sustained weakness below the 1.3150 resistance level may encourage a further decline back towards 1.3050 and 1.3000, respectively. The daily bearish setup is a threat if bulls are able to break back above 1.3230.

Dollar trips on uncertainty

This is shaping up to be a painful trading day for the Dollar, as ongoing uncertainty over the proposed tax reforms weighs heavily on the currency.

The fact that the Dollar sharply depreciated on Tuesday, as growing concerns that U.S corporate tax cuts could be delayed, continues to highlight its sensitivity to expectations of proposed U.S tax reforms. Dollar bulls are currently lacking the inspiration to make a move, but could be motivated this afternoon, if U.S consumer inflation and retail sales data exceed market expectations. A rise in inflation and retail sales is likely to boost sentiment towards the U.S economy. ultimately supporting the Dollar.

Taking a look at the technical picture, the Dollar Index took a beating on Tuesday, as price tumbled towards 93.80. Sustained weakness below the 94.00 support level may encourage a further decline towards 93.50. In an alternative scenario, bulls need to push prices back above 94.50 to jump back into the game.

Commodity spotlight – Gold

Gold received a boost on Tuesday, thanks to a vulnerable U.S Dollar and depressed stock markets. With caution in the air as uncertainty lingers over the outlook for U.S tax reforms, investors may turn to safe-haven assets, which in turn should offer some support to Gold. From a technical standpoint, prices have broken above the $1280 resistance level. If bulls can maintain control above this level, then the next levels of interest will be at $1289 and $1300. Alternatively, a failure for bulls to secure control above $1280 may trigger a decline back towards $1267.

Global Stock Market Rout Continues

Japanese GDP growth approves BOJ's policies

Oil Traders await inventory data

UK wage number needs to keep up with inflation

US inflation data may have only one outcome

The Japanese economy has continued to show its sign of strength for the consecutive seven quarters. The GDP data released overnight has strengthened the Bank of Japan's position and affirmed that its monetary policies are sailing the ship in the right directions. The GDP number for the third quarter came at 1.4% which was ahead of the forecast of 1.3%. The robust Japanese export numbers are the primary driver for today's GDP number. Investors have discounted the feeble consumer spending as the economy is approaching its full employment level but this number is expected to improve in the future. The bank of Japan's biggest challenge has been fighting the sluggish inflation in the country, however, the improving export number and the higher capital expenditure should move the inflation in the bank's desired situation.

Commodities

Crude and Brent are both getting battered as the API data indicated that the US stockpiles have surged unexpectedly by 6.51 million barrels and the if the upcoming US crude inventory number also confirms the same message, we could see the US crude moving further lower. Adding to the trader's malaise, the IEA lowered its oil demand growth by 100K b/d for the next two years and Russia reasons it may be too soon to talk about output cuts. These negative developments have taken the wind out of the oil rally.

The price for the precious metal seems to be steady after hitting this week's low. The upcoming US consumer inflation data would have the potential to impact the gold price further. The dollar index looks firm ahead of this number and if the US consumer inflation number moves ahead of the forecast, it would move the dollar index further higher. The higher dollar would have the potential to push the gold price lower. A number of Fed members back the idea of another rate hike and improving consumer inflation and producer prices would strengthen their view for another rate hike in December. Under those circumstances, the dollar index may move more in the upwards direction which would take some more shine off the yellow metal.

Currencies

Back in the UK, Carney was able to save its ink and doesn’t need to write a letter to the Chancellor of the Exchequer after the inflation data came a little shy of the forecast. Now, the focus would be on the labour data and investors are going to see how much evidence exists in terms of a squeeze on the UK households. A modest pay rise would not solve the problem because the wage growth of 2.2% is not going to keep up with the inflation. In today's number, we do expect the unemployment number to show further enhancement and may print the number of 4.3%. It would be fascinating the hear the views of the BOE Deputy governor's view today who firmly voted for a 25 basis point hike at November meeting.

As for the US, it would be mostly about the U.S inflation number which matters the most. The game has transformed now and investors cannot say that they have their backs covered by the Fed. The Fed is on the monetary policy tightening path. Previously, a bad set of data was also considered as good news because the Fed would have pumped more liquidity in the market. But now, a bad set of economic data would be believed as a very negative progress because it would say that the Fed has made a mistake. Furthermore, a good set of economic number may not lift all the boats either because it would simply tell us that the Fed would remain firm about increasing the interest rate three more times next year.

AUDUSD Extends Decline, Bearish Outlook Now Stronger

AUDUSD is in a bearish phase as it extends its decline from the multi-year peak of 0.8124. The pair is now testing its lowest level since July. The bearish outlook was strengthened after prices fell below the 200-day moving average.

Key support failed at the 61.8% Fibonacci retracement level (0.7630) of the upleg from 0.7328 to 0.8124. This level has now turned to immediate resistance.

Indicators like RSI and MACD are in bearish territory although looking neutral at the moment, suggesting downside momentum has weakened. On a shorter time-frame, the market has entered a consolidation phase. Support levels are expected in the 0.7500 handle at previous daily lows (0.7571 and 0.7534) before re-testing the 0.7328 low.

A move above the 0.7900 level would ease downside pressure and a break back above 0.8000 would shift the focus back to the upside for a resumption of the prior uptrend from 0.7328.

While the 50 and 200-day moving averages remain bullishly aligned (shorter MA above longer period MA), the 50-day MA is now sloping down suggesting a possible bearish crossover is imminent.

USDJPY Pair Intraday Bearish Below 113.24 Level

The U.S dollar has moved sharply lower against the Japanese yen, hitting 113.03, after better than expected third quarter GDP figures from the Japanese economy. The Japanese yen has strengthened across the board, after official data showed the Japanese economy growing for a seventh consecutive quarter, led by strong export growth. The USDJPY pair currently trades around the 113.18 level, as intraday buyers continue to defend the key 113 level ahead of the European market open.

The USDJPY pair remains intraday bearish while trading below the key 113.24 technical level. Further declines can be expected towards the 112.98 and 112.28 levels, while price-action holds below the 113.24 level.

Should price-action move above the 113.24 level, USDJPY buyers will likely re-test the 113.68 and 113.92 resistance levels.

EURO Strongly Bullish Above 1.1710 Level

The euro has surged higher against the U.S dollar, hitting 1.1800, after the pair performed a major technical break-out on Tuesday. Investors also continue to move into the single currency after much better than expected German GDP growth figures. The EURUSD pair currently trades close to the highs of the week, as the U.S dollar index starts to decline across the board in early Wednesday trading. During the upcoming U.S session, we see the release of key Retail Sales and inflation figures from the U.S economy.

The EURUSD pair remains intraday bullish while trading above the key 1.1710 technical level. Further upside towards the 1.1838 and 1.1876 levels remains increasingly likely.

Should the EURUSD pair start to decline, intraday sellers will likely target the 1.1751 and 1.1710 technical support levels.

Ethereum Breakout Hits One-Month High

The value of Ethereum caught a tailwind on Tuesday, as a series of technical trades brought ETH/USD above critical resistance levels.

ETH/USD held firm in the early hours of Wednesday trading, where it was seen hovering around $336. The cross has added 6% over the past 24 hours on higher trade volumes. With the gain, ether climbed above key technical hurdles situated at $315 and $325, signaling continued upside for the pair.

At current levels, ether’s total market cap is valued at $32.13 billion, enough for second on the global cryptocurrency list. Ethereum briefly fell to third place on the list after Bitcoin Cash quadrupled in price over the weekend.

Ethereum has struggled in recent months, but appears poised to continue higher after this week’s technical breakout. The market remains well below record highs, which appear closer to $400.

The ether blockchain continues to be the platform of choice for token issuers. This is expected to continue as more companies adopt smart contracts.

Data Deluge Begins On Wednesday

Investors can expect to see a deluge of economic data on Wednesday, with highlights from both sides of the Atlantic. These data points are expected to fuel everything from stocks to currencies in mid-week trading.

Action begins at 07:45 GMT with French inflation data. The Eurozone's second-largest economy is expected to show annual CPI of 1.2% in October.

Shifting gears to the United Kingdom, the Office for National Statistics will report the latest jobs numbers at 09:30 GMT. The claimant count change is expected to rise by 2,300 for the month of October. The unemployment rate is expected to hold steady at 4.3% annually in the three months through September. Meanwhile, average hourly earnings including bonus are projected to rise 2.1% annually in July-September.

Later in the session, the European Commission's statistical agency will release the latest trade balance for the month of September. The Eurozone trade surplus is forecast to edge down to €21.4 billion from €21.6 billion.

In North America, government economists will release a pair of high-profile reports at 13:30 GMT, including retail sales and the consumer price index (CPI).

Receipts at retail stores are forecast to rise 2% annually in October, following a 1.6% increase the month before.

In terms of CPI, inflation is expected to climb 2% annually in October, following a 2.2% gain in September. Excluding food and energy, the CPI indicator is expected to come in at 1.7%.

In a separate release on Wednesday, the Federal Reserve Bank of New York will issue its Empire State Manufacturing Index for the month of November. The report is expected to show a drop of 4.2 points to 26.0.

In terms of monetary policy, Federal Reserve official Charles Evans will deliver a speech at 08:00 GMT. The Bank of England's Andrew Haldane and Peter Praet of the European Central Bank (ECB) are also scheduled to deliver remarks throughout the day.

EUR/USD

The euro is trading at fresh two-week highs against the dollar, with EUR/USD briefly trading above 1.1800 on Tuesday. The pair was last seen hovering just below that psychological level. The 14 November high of 1.1805 remains the key resistance barrier. On the flipside, support is located at 1.1765.

GBP/USD

Cable regained momentum on Tuesday, climbing to a session high of 1.3176. GBP/USD gave back most of its gains at the start of Wednesday, with the pair trading around 1.3138. That represents a decline of roughly 0.2%. Economic data will largely dictate the direction of the market in the short term.

USD/JPY

The USD/JPY declined on Wednesday, as the dollar weakened. The pair was last down 0.2% at 113.18. The bulls control the market at 114.00. Immediate support is located at the low 113.00 region.