Sample Category Title

DAX – Break Below Key Supports at 12900 Zone Signals Further Downside

DAX is in firm bearish mode and accelerated further down after opening with gap lower on Wednesday.

Fresh strength of the Euro keeps the index under increased pressure as today's weakness broke key short-term supports at 12906/12892 (25 Oct trough / Fibo 38.2% of 11862/13530 ascend).

Close below here would generate fresh bearish signal for extension of pullback from 13530 (07 Nov all-time high), as formation of daily Tenkan-sen / Kijun-sen bear-cross additionally pressures the price.

Next support lies at 12803 (55SMA) with further bearish acceleration capable of travelling towards 12666 (top of rising daily cloud / 138.2% Fibo projection of the downleg from 13530).

Bears could be interrupted in coming sessions by corrective action on oversold studies.

Res: 12906; 12991; 13104; 13186

Sup: 12842; 12803; 12753; 12666

The Dollars Demise

Wednesday November 15: Five things the markets are talking about

Market risk-off continues to dominate capital market moves; both European and Asian stocks have seen 'red' in their sessions while bonds and gold prices advanced.

The dollar has fallen to its lowest level in nearly three weeks overnight, reflecting the diminishing expectations that Republicans will be able to push through a tax overhaul this year.

Investors attention now turns to data coming out of the U.S this morning – consumer prices and retail sales (08:30 am EDT) should provide clues on the strength of the world's largest economy after the 'flattest' U.S Treasury yield curve in a decade is raising concern that growth will slow.

1. Stocks see 'red'

In Japan, the Nikkei share average fell to a new two-week low overnight, with all sectors in negative territory as investors took profits following a two-month rally that pushed the index up by about +20%. The index ended down -1.6%, while the broader Topix closed -2% to seal its longest streak of losses since September 2016.

Down-under, Australia's S&P/ASX 200 Index declined -0.6% and the Kospi index in Seoul was down -0.3%.

In Hong Kong, stocks followed other Asian markets lower, dragged down by resources and industrial firms, amid worries over China's economic growth after sluggish economic data. The Hang Seng index fell -1.0%, while the China Enterprises Index lost -1.6%.

In China, stocks extended their losses, hurt by resources shares amid signs of a slowdown in industrial production. The blue-chip CSI300 index fell -0.6%, while the Shanghai Composite Index dropped -0.8%.

In Europe, regional indices trade lower across the board following on from weakness in Asia. Softer commodity prices are weighing on miners after weaker Japanese GDP (+0.3% vs. +0.4%) and downbeat Chinese economic data.

In the U.S, stocks are set to open in the 'red' (-0.5%).

Indices: Stoxx600 -0.8% at 380.8, FTSE -0.5% at 7375, DAX -1.0% at 12898, CAC-40 -0.5% at 5287, IBEX-35 -0.8% at 9911, FTSE MIB -1.0% at 22084, SMI -0.7% at 9065, S&P 500 Futures -0.5%

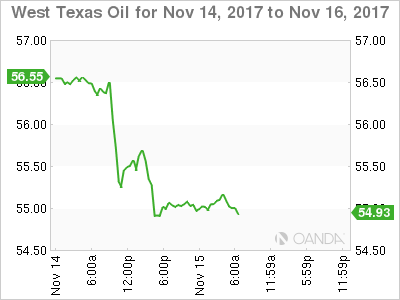

2. Oil prices slide after IEA casts doubt over demand outlook, gold higher

Oil prices fell by -1% overnight, continuing yesterday's slide after the IEA cast doubts over the past few months' narrative of tightening fuel markets.

Brent crude futures are at +$61.61 per barrel, down -60c, or -1% from yesterday's close. U.S West Texas Intermediate (WTI) crude is at +$55.14 per barrel, down -56c, or -1%.

Note: Crude prices are now down by around -5% since hitting 2015 highs last week, ending a +40% rally between June and early November.

Yesterday, the IEA cut its oil demand growth forecast by -100k bpd for this year and next, to an estimated +1.5m bpd in 2017 and +1.3m bpd in 2018.

U.S crude inventories are also weighing on prices. API data yesterday showed that U.S crude inventories rose by +6.5m barrels in the week to Nov. 10 to +461.8m.

Note: U.S government inventory data (EIA) is due later this morning (10:30 am EDT).

Ahead of the U.S open, gold prices have edged higher as the dollar slipped ahead of the release of inflation data and retail sales that could provide hints on the Fed's monetary tightening policy. Spot gold is up +0.3% at +$1,284.30 per ounce.

Note: On Tuesday, gold touched +$1,270.56, its lowest since Nov. 6, before rallying to close +0.2% higher.

3. Sovereign yields fall

Global yield curves have returned to a 'flattening' trend and have pushed the U.S benchmark spread (2/30) back below +70 bps.

From here, sovereign yields are expected to range trade for the remainder of this year now that the Fed's rate increase for December is almost fully priced, and while the ECB has set its course for most of 2018.

Overnight, the yield on U.S 10-year Treasuries has decreased -4 bps to +2.33%, the lowest in more than a week. In Germany, the 10-year Bund yield has decreased -3 bps to +0.37%, their lowest yields in a week. In the U.K, the 10-year Gilt yield has declined -4 bps to +1.285%, the largest decrease in almost a fortnight.

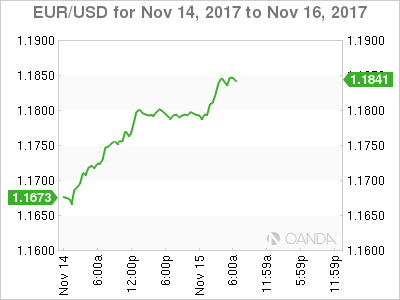

4. Dollar in trouble

The USD remains on the back foot on investor concerns over the U.S tax reform proposal losing momentum.

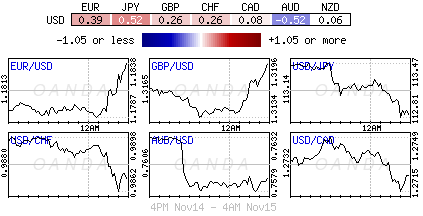

The EUR/USD (€1.1840) has managed to print a three-week high above the psychological €1.1850 print and is poised to record its sixth consecutive session gain. Euro data this month suggests that the market is witnessing the best macro-economic recovery since the 'single' unit has come into existence. If eurozone data strength continues, investors should expect the short-end of the Euro yield curve to correct and further support a stronger EUR.

GBP/USD tested above £1.32 ahead of key wage data (see below). The wage data did beat market expectations, but the sterling's firm tone has been short-lived as investors question the sustainability of the upward momentum.

USD/JPY (¥112.76) is a tad softer on mostly safe-haven flows as global equity markets fall again.

The Turkish lira (€4.6036) continues to struggle after hitting a record low against the euro yesterday. The lira has come under sustained pressure in recent weeks following its diplomatic spat with the U.S and a deteriorating economic position.

5. UK employment, real wages fall in Q3

Data this morning showed that the number of U.K citizens in work fell on a quarterly basis after nearly two years of growth, dropping by -14k. At the same time, the number of economically inactive Britons – those neither working nor seeking employment – rose by +117k, the biggest increase in seven-years.

Data from the Office for National Statistics (ONS) also showed that the squeeze on living standards in the U.K. continues, with real wages dropping for the seventh consecutive month. The data pointed to a -0.5% drop in real earnings on a yearly basis, excluding bonuses.

EURJPY Is Neutral In The Medium Term, Short-Term Bullish Phase Still Intact

EURJPY is neutral in the medium term but in a shorter time frame the pair is in a bullish phase.

The market has been consolidating gains made after a rally took EURJPY to the mid-134 handle, the highest level since November 2015. Since the end of September, prices have been moving sideways in a range with strong support in the mid-131 area.

On the 4-hour chart, EURJPY bounced off the range-low and rose towards the top of the range, reaching a high of 133.87 today. Bullish momentum is still in place and the short-term upleg has only retraced by 23.6%. This Fibonacci level is now acting as an immediate support at 133.28. A break below this would see further support at subsequent Fibonacci levels at 132.91, 132.63, 132.33 before making a full retracement to re-test the 131.39 low.

Breaking resistance at the recent rally’s top at 133.87 would bring the broader range-high level into view. A rise above 134.50 would bring a resumption of the longer-term uptrend.

The intra-day bias is neutral and the RSI is flat, while the short-term bullish phase from November 8 low of 131.39 is still intact.

Technical Outlook: Nikkei 225 – Extended Bears Eye Fibo Support At 21762

Nikkei is sharply lower on Wednesday, extending pullback from new multi-year high at 23420 into fifth straight day. Bearish acceleration through strong support at 22035 (daily Kijun-sen) and psychological 22000 support pressures next pivotal point at 21762 (Fibo 38.2% of 19080/23420 ascend) and would generate strong bearish signal on break. Negative sentiment that extended from the Wall St on Tuesday persists and could drive the price further down. Falling daily RSI is currently at the mid-point and shows plenty of room at the downside, however, bears may take a breather as strongly oversold slow stochastic warns of correction, but so far without firmer signal. Bears could travel to 21250 (50% of 19080/23420) on sustained break below 21762 trigger. Broken 20SMA marks solid resistance at 22125, ahead of session high at 22320 and south-turning 10SMA (2250), which is expected to cap extended upticks.

Res: 22000, 22125, 22320, 22500

Sup: 21830, 21762, 21585, 21250

Euro Rally Continues, US Consumer Data Eyed

The euro continues to gain ground on Wednesday session, after strong gains on Tuesday. Currently, EUR/USD is trading at 1.1830, up 0.27% on the day. In economic news, the eurozone trade surplus jumped to EUR 25.0 billion, above the estimate of EUR 21.2 billion. It’s a busy day in the US, with the focus on consumer data. CPI is expected to come in at 0.1% and Core CPI at 0.2%. Consumer spending is also expected to post low numbers, with the estimate for Retail Sales at 0.2% and Core Retail Sales at 0.0%.

The German economy is firing on all cylinders and showed no signs of fatigue in the third quarter. GDP jumped to 0.8% in the third quarter, recording its strongest quarter since 2014. Germany’s economy is growing at annualized rate of 2.8% in 2017. The catalyst for the strong reading was an increase in business investment, as sales of machinery and equipment increased. German fundamentals remain strong, as business and consumer confidence is high and unemployment remains at record-low levels. However, the positive economic conditions have failed to trigger much inflation, which has been a problem throughout the eurozone. German Final CPI dipped to 0.0% in October, the first time inflation has not moved higher since May. Germany has been the locomotive for the euorozone, and boosted traditional laggards such as France and Spain. Geopolitical concerns such as Catalonia and Brexit have the potential to crash the party, but in the meantime, eurozone indicators have generally been pointing upwards.

The heads of central banks met on Tuesday at an ECB event, with a focus on communication with the markets and the public. Federal Reserve Chair Janet Yellen acknowledged that the FOMC committee of 19 members posed problems, as members did not always speak with a unified voice. This led to the markets picking up on differences between policymakers, often leading to market volatility. Yellen admitted that this problem would not be solved anytime soon, saying it was “a work in progress”. To be fair, this is also an issue for the ECB, as the markets have on occasion reacted to comments from individual policymakers regarding monetary policy or quantitative easing

Financial Stocks Pull DAX Downwards

The DAX index has posted sharp in the Wednesday session. Currently, the DAX is at 12,862.50, down 1.31% on the day. On the release front, the eurozone trade surplus jumped to EUR 25.0 billion, above the estimate of EUR 21.2 billion. It's a busy day in the US, with the focus on consumer data. CPI is expected to come in at 0.1% and Core CPI at 0.2%. Consumer spending is also expected to post low numbers, with the estimate for Retail Sales at 0.2% and Core Retail Sales at 0.0%.

It's been a dismal November for the DAX, which has declined 3.6%. The index has posted six straight losing sessions and is at its lowest level since October 2. The downward trend has intensified on Wednesday, as financial stocks have dragged the index lower. Commerzbank is down 3.90%, while Deutsche Bank has declined 2.85 percent on the day.

Germany's economy continues to fire on all cylinders, and jumped to 0.8% in the third quarter, recording its strongest quarter since 2014. Germany's economy is growing at annualized rate of 2.8% in 2017. The catalyst for the strong reading was an increase in business investment, as sales of machinery and equipment increased. German fundamentals remain strong, as business and consumer confidence is high and unemployment remains at record-low levels. However, the positive economic conditions have failed to trigger much inflation, which has been a problem throughout the eurozone. German Final CPI dripped to 0.0% in October, the first time inflation has not moved higher since May. Germany has been the locomotive for the euorozone, and boosted traditional laggards such as France and Italy.

The heads of central banks met on Tuesday at an ECB event, with a focus on communication with the markets and the public. Federal Reserve Chair Janet Yellen acknowledged that the FOMC committee of 19 members posed problems, as members did not always speak with a unified voice. This led to the markets picking up on differences between policymakers, often leading to market volatility. Yellen admitted that this problem would not be solved anytime soon, saying it was “a work in progress”. To be fair, this is also an issue for the ECB, as the markets have on occasion reacted to comments from individual policymakers regarding monetary policy or quantitative easing.

CRUDE OIL Profit-Taking

Crude oil is consolidating after the commodity set up resistance at 57.92 (08/11/2017 high). The commodity is trading at 1-year high. Expected to show further shot-term bearish consolidation. Indeed the technical structure has a history of decent consolidation phase.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Increasing Slightly

Silver is heading higher. Hourly support can be found at 16.60 (27/10/2017 low). Hourly resistance is given at 17.46 (13/10/2017 high). Additional support can be found at 16.13 (06/10/2017 low).

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Riding Short-Term Uptrend Channel

Gold is pushing higher. The technical structure confirms the end of the consolidation phase. Support lies at a distance at 1251 (08/08/2017 high). Resistance is now located at 1288 (20/10/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Back Around $7000

Bitcoin is now consolidating after recent surge. The technical structure shows a tremendous positive short-term momentum. Hourly support is now located at 5605 (13/11/2017 low). Strong support stands very far at 2975 (22/08/2017 low). In the short-term, the digital currency should continue rising.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.