Sample Category Title

October’s UK Retail Sales Could Feed Pound Bears

Inflation readings on Tuesday suggested that British pockets will remain squeezed ahead of the Christmas shopping season, as consumer prices continued growing steadily by 3.0% in October, potentially flagging another disappointing month for retailers. With Brexit negotiations trapped in a deadlock and British real wage growth showing no signs of a significant rise, annual retail sales in October are expected to post a negative performance on Thursday, reducing the odds of another interest rate hike this year and therefore deteriorating the outlook for the British pound.

Analysts forecast retail sales to contract in October for the first time since April 2013, declining by 0.6% y/y after rising by 1.2% in September. Recall that September's reading, which constituted the weakest growth observed since June, drove the quarterly gauge to a four-year low of 1.5%. Month-on-month, though, household spending is anticipated to recover by 0.1% following a fall of 0.8% in the previous month. Excluding auto sales and fuel, the core equivalent is estimated to slip by 0.4% y/y compared to a rise of 1.6% seen previously.

A monthly report published by the British Retail Consortium last week gave the first signs of a slowing retail sector, with like-for-like sales sinking by 1.0% in October, offsetting to a large extent the 1.9% growth seen in September. In-store sales of non-food products decreased by 2.9% over the three months to October, reaching a record low since the start of the survey in 2012. Overall, though, the survey revealed a 0.2% annual growth in the industry.

Although the British economy has to a large extent weathered the negative forecasts following the Brexit vote, uncertainty on the Brexit front firmly remains on the table, clouding the outlook. The UK and the EU Brexit negotiators have failed to reach sufficient progress in the talks, raising the probability of a cliff-edge scenario for business leaders. Lacking clarity on the UK's future relationship with the block, firms are reluctant to pay higher wages but instead are prepared to exercise their contingency plans in case of a "hard" or no-deal Brexit. Hence, consumers might cut back on spending as their budgets come under pressure.

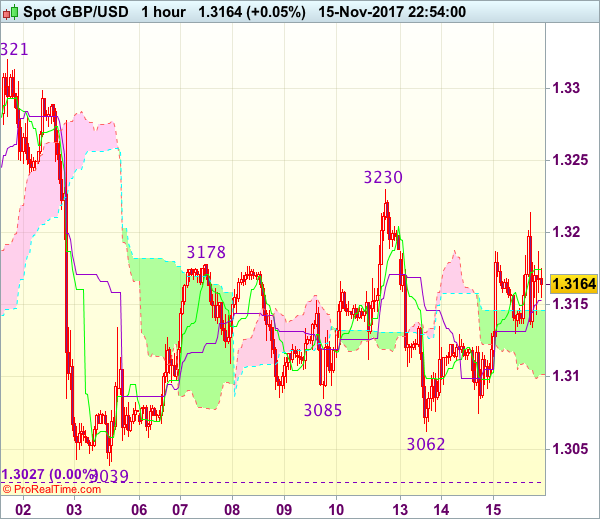

Unless actual numbers beat forecasts, the pound will likely move downwards to meet support at the previous bottom at 1.3023. Any violation of this point might also open the way towards August's low of 1.2770.

Alternatively, better-than-expected readings could see the 50-day simple moving average of 1.3253 and the previous top at 1.3337 acting as resistance, while a bigger positive deviation from estimates would shift focus to the 1.35 key-level (previously a support level).

Aussie Again on Spotlight as Employment Figures Eyed

Following a disappointing report on Australian wage growth on Wednesday, the Australian Bureau of Statistics is due to give an outline on the state of the labor market at 0030GMT on Thursday. Unlike wage forecasts which projected a rise in earnings, analysts anticipate the economy to create fewer jobs in October, maintaining the unemployment and participation rates steady at their previous levels. If the numbers fail to meet expectations or otherwise fail to impress, then the aussie could get another shake tomorrow as a slow-growing jobs market would keep wage growth subdued for longer, harming household spending which is a crucial contributor to economic growth.

In October, analysts anticipate 17,500 additional workers to join the labor market in Australia compared to the 19,800 seen in September, marking 13 consecutive months of gains. They also project the unemployment rate to hold flat at a four-year low of 5.5%, which is slightly above the RBA's rate under full employment, and the participation rate to remain steady at a two-year high of 65.2%.

However, the change in full-employment positions will also gather attention as an increase in such jobs has the capacity to push the unemployment rate even lower given that the ratio is calculated factoring in full-time workers rather than part-time ones. Such a development would be good news for RBA policymakers who believe that the unemployment rate will decline to 5.25% by the end of 2019. In September, 6,100 full-time positions were added in the economy, well below the number of 39,500 observed in August.

Still, the RBA might get dashed if low-income industries absorb a larger proportion of workers, restraining wage growth from rising faster and hence limiting inflation which has stuck under the central bank's target band of 2-3%. Consumers will also find it difficult to repay their overloaded debt obligations, meaning that household spending will narrow as well.

Should the data miss forecasts, aussie/dollar will likely extend its downtrend towards the 0.75 key level which acted as a barrier to upside movements in May, while the area around the 0.7326 mark, the lowest level reached since the beginning of the year, could also provide support given a sharper down movement.

Alternatively, if the data surprise to the upside, the 200-day simple moving average (SMA) of 0.7697 could provide resistance ahead of 0.7818, this being the 50-day SMA.

Dollar and Stocks Falter; Euro and Yen Shine

Markets remained in risk-off mode in European trading on Wednesday, with risk assets coming under pressure while safe-havens flourished. The US dollar extended its losses against the yen despite another batch of solid data out of the United States today. The euro rallied to a one-month high against the greenback, but the pound remained range-bound.

The yen was the day's strongest currency, though its driver was not the upbeat third quarter GDP figures released in Japan earlier in the day but safe-haven flows. Risk sentiment failed to recover during the course of the day, with a sell-off in commodities and doubts about the US tax reforms weighing heavily on investors. Major stock indices in Europe were all in the red, following on from declines in Asia today and on Wall Street overnight. US indices looked set for a second straight day of losses after opening lower.

The Swiss franc also benefited from safe-haven demand, rising against the dollar and the euro, but gold's advances were more constrained. The precious metal hit a 3½-week high of $1289.09 an ounce but had fallen back to around $1280 towards the close of European trading.

Long-term US treasury yields continued to decline as a plan by Senate Republicans to link a repeal of the individual mandate that requires Americans to buy health insurance – a key component of Obamacare – with the tax reforms raised concerns that it would make it harder for the legislation to pass. The development undermined the dollar's recent bullish run, with dollar/yen sliding to a 4-week low of 112.46 yen before recovering to around 112.90 in late session. The dollar index also fell to a 4-week low, hitting 93.40.

There was little support for the greenback from the latest US inflation and retail sales figures. The annual CPI rate eased from 2.2% to 2.0% in October as expected, but core CPI came in slightly above forecasts at 1.8%, up from 1.7% in September – the first gain since January. Retail sales impressed, growing by 0.2% month-on-month in October, beating forecasts of no change and follows an upwardly revised 1.9% jump in September. The retail control measure, which is used in GDP calculations, missed expectations of 0.4% to rise by 0.3%, but the prior month's figure was revised up from 0.4% to 0.5%. Also released today was the Empire State Manufacturing index, which missed estimates of 26.0 to sharply drop to 19.4 in November.

The euro reached a high of $1.1860 and was up against most major currencies. It stood 0.2% higher against the pound at 0.8980 in late trading, having earlier broken above 0.90 pounds to touch a near 4-week peak. It was down against the yen however, sliding by 0.5% to 133.15.

Sterling was mixed and saw limited reaction to today's UK jobs data. Britain's unemployment rate was unchanged at 4.3% in the three months to September. But there was an unexpected fall in employment of 14,000 during the period, raising fears that the slowing economy may be starting to impact the labour market. However, there was a positive surprise from wage growth. Average weekly earnings rose by 2.2% year-on-year in the three months to September. It compares with expectations of 2.1% and an upwardly revised 2.3% in August. Excluding bonuses, earnings also rose by 2.2%, in line with estimates.

The pound touched a session low of $1.3131 after the data but later rebounded slightly to around $1.3160. There was some support for the pound after the first day of debate for the UK government's EU Withdrawal bill passed without any hurdles on Tuesday, in a boost for the prime minister, Theresa May.

Meanwhile, the Bank of England's Deputy Governor Ben Broadbent today defended the Bank's rate increase earlier this month, though he gave little away about the path of future hikes.

Commodities continued to struggle on Wednesday, particularly base metals and energy. Copper was down sharply for a second day, slipping 0.75% to $3.037 a ton. Crude oil also extended its losses, falling by over 1% on the day. WTI crude was last trading just under $55 a barrel and Brent crude stood at $61.37. Oil prices came under further pressure today from a surprise build in US crude and gasoline stocks in the Energy Information Administration's latest weekly report.

EURGBP – Bulls Hesitate ahead of Daily Cloud Top

The cross eases below 0.9000 handle which was dented on today's spike to 0.9013, showing strong hesitation at key 0.9026 barriers (daily cloud top/former highs of 10/20 Oct). The price is holding within thick daily cloud and maintaining firm tone, favoring probes above daily cloud.

Meanwhile, some profit-taking on recent rally from 0.8791 may delay immediate bulls, with overbought slow stochastic on daily chart supporting scenario.

Broken 100SMA which holds today's action marks initial support at 0.8947, with daily cloud base (0.8927) expected to hold corrective dips before fresh push higher. Daily Tenkan-sen/Kijun-sen bull-cross which was formed yesterday underpins the action.

Eventual break above daily cloud would open next barrier at 0.9087 (Fibo 61.8% of 0.9306/0.8732 descend).

Res: 0.9013; 0.9026; 0.9046; 0.9087

Sup: 0.8947; 0.8927; 0.8902; 0.8882

USD Losing Positions Without Prospects of Tax Reform

The euro's upward trajectory continues as the greenback falls and more positive macro data is released from the Eurozone. USD investors are frustrated by the decreasing probability of tax reforms being passed by the legislative branch in the US. Expectations of tax cuts were among the main growth drivers for the US dollar throughout this year. At the same time, the EUR/USD bulls were cheered by positive news on the trade balance surplus in the Eurozone which grew to 25.0 billion in September against the 21.2 billion expected.

Even the better than expected retail sales in the US, which came in 0.2% for October, were not able to change the mood on the market. We should note that consumer price index growth by 0.1% in October was in line with the average predictions and has not led to significant changes in the probability of the interest rate hike by the Fed in December.

The British pound has shown a slight increase in volatility following the release of labour market data, according to which the unemployment rate remained at 4.3%. The average earnings index declined by 0.1% to 2.2%, which is 0.1% better than expected.

The preliminary report on GDP in Japan revealed a slowdown in the pace of expansion to 0.3% in the third quarter of this year compared to the 0.4% forecasted. Despite the disappointing news, the USD/JPY kept falling due to investors negative sentiment of the US dollar.

Tomorrow traders will turn their focus to Australian labour market data due at 00:30 GMT and industrial production in the US at 14:15 GMT.

EUR/USD

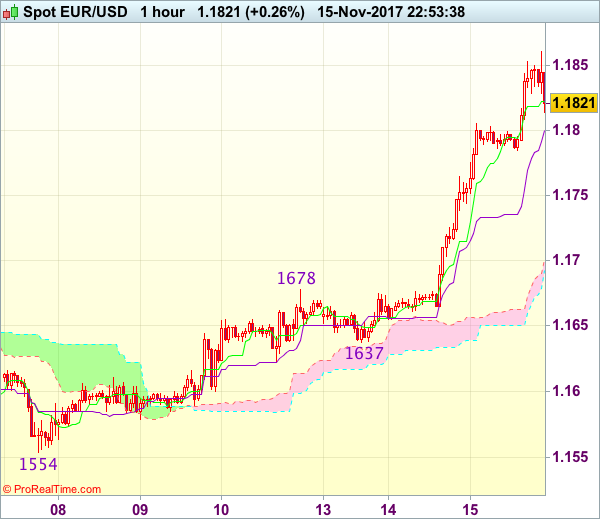

The EUR/USD keeps growing today and overcoming 1.1825 may become an additional stimulus for continued price increases with potential targets at 1.1925 and 1.2000. Correction is possible down to the support at 1.1730. The MACD signal line has turned around and its decline points to a possible price consolidation or decline soon.

GBP/USD

The British pound was unable to overcome the inclined resistance line and returned to the support at 1.3150. In case of the fall continuing, within the limits of the channel, the quotes may reach 1.3050 and 1.2950. On the other hand, in order to change the trend to positive, quotes need to gain a foothold above 1.3200.

USD/JPY

The USD/JPY price accelerated the pace of decline and touched the lower limit of the descending channel and in case of further decline within the limits of the channel, quotations may reach 111.70. We should note that RSI on the 15-minute chart came close to the oversold territory which signals a possible rebound with potential the target at 113.00.

Trade Idea Wrap-up: USD/CHF – Sell at 0.9920

USD/CHF - 0.9877

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9867

Kijun-Sen level : 0.9886

Ichimoku cloud top : 0.9947

Ichimoku cloud bottom : 0.9941

Original strategy :

Sell at 0.9920, Target: 0.9820, Stop: 0.9955

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9920, Target: 0.9820, Stop: 0.9955

Position : -

Target : -

Stop : -

As the greenback has fallen again after brief recovery, suggesting the erratic decline from 1.0038 top is still in progress for at least a retracement of early upmove, hence bearishness remains for this fall to extend further weakness to previous resistance at 0.9837, break below there would encourage for subsequent decline towards 0.9795-00 which is likely to hold on first testing due to near term oversold condition.

In view of this, we are looking to sell dollar on subsequent recovery as 0.9922 (previous support) should limit upside. Above 0.9940-45 would defer and risk test of 0.9970-75 but price should alter below resistance at 0.9987, bring another decline later.

US: Retail Sales Show Solid Demand in October

Retail sales rose 0.2 percent in October after rising 1.9 percent in September. Excluding categories impacted by weather events, retail sales remained quite strong which bodes well for Q4 personal consumption.

Retail Sales Ease in October as Hurricane Swell Recedes

Retail and food services sales rose 0.2 percent in October and September's surge was revised higher to 1.9 percent. This was stronger than expected, as consensus had penciled in a flat month of sales as the boost from gas prices, building supplies and auto sales associated with the hurricanes eased from September. Control group sales - which exclude autos, food, gasoline and building materials were less impacted by the hurricanes in September, and were up a stronger 0.3 percent in October. Control group sales are up a solid 3.5 percent average annualized rate over the past three months, which suggests spending has solid momentum going into the last quarter of 2017.

The higher gasoline prices caused by Hurricane Harvey's aim at the Gulf Coast faded in October, and gasoline station sales declined 1.2 percent on the month after surging 6.4 percent in September. Building materials sales also declined in October as payback for the outsized 3 percent rise the previous month, when immediate repairs and storm-proofing pushed up sales at home improvement stores. Notably, those were the only significant declines in October. The volatile nonstore retailer category fell 0.3 percent on the month but remains one of the strongest categories over the year.

Auto dealers' sales continued to increase in October, rising 0.8 percent after September's 4.6 percent surge. Vehicle replacement following the hurricanes have certainly provided a boost to the category, which saw sales rise 4.5 percent over the year on a three month average basis. Furniture stores may have also seen a boost from replacing storm damages, as sales rose 0.7 percent in October and are up 4.2 percent during the past three months relative to the same period last year. Continued inroads made in the housing market likely also helped with that year-over-year gain.

Sales at eating and drinking places ramped up 0.8 percent in October which was its largest monthly gain since January. Electronics and appliance stores also saw sales rise 0.7 percent in October but remain down over the year. Sales jumped 1.5 percent in the sporting goods and hobby store category in October - its first meaningful monthly increase this year, sales are down 2.4 percent over the year, however.

Control Group Sales Show Demand Strong for Q4

Retail sales were up for most categories in October, which is reassuring as a gauge of consumer spending momentum in the start of Q4. Control group sales, which go into the calculation of personal consumption expenditures in GDP, were up more than the headline in October because they were not adversely impacted by the comedown in gasoline prices. They also strip out volatile spending on food, auto and home improvement stores, and are thus a good gauge of underlying consumption demand. Control group sales saw momentum increase in October, which is good news for retailers going into the holiday season and for Q4 GDP calculations if this strength holds up.

Trade Idea Wrap-up: GBP/USD – Buy at 1.3100

GBP/USD - 1.3163

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.3174

Kijun-Sen level : 1.3155

Ichimoku cloud top : 1.3146

Ichimoku cloud bottom : 1.3102

Original strategy :

Buy at 1.3130, Target: 1.3230, Stop: 1.3095

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3100, Target: 1.3210, Stop: 1.3065

Position : -

Target : -

Stop : -

As the British pound rebounded again after holding above support at 1.3062 (this week’s low), retaining our view that further consolidation would take place and another bounce to 1.3210-15, then towards resistance at 1.3230 would be seen, however, as broad outlook remains consolidative, reckon upside would be limited to 1.3250 and price should falter below 1.3275-80.

In view of this, we are looking to buy cable on dips as 1.3100-05 should limit downside. Below 1.3075 would risk test of said support at 1.3062 but break there is needed to suggest a downside break of recent broad range has taken place, bring retest of strong support area at 1.3027-39, only break there would confirm and extend recent decline to psychological support at 1.3000 first.

Trade Idea Wrap-up: EUR/USD – Buy at 1.1745

EUR/USD - 1.1810

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1827

Kijun-Sen level : 1.1803

Ichimoku cloud top : 1.1711

Ichimoku cloud bottom : 1.1701

Original strategy :

Buy at 1.1745, Target: 1.1845, Stop: 1.1710

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1745, Target: 1.1845, Stop: 1.1710

Position : -

Target : -

Stop : -

As the single currency has retreated after rising to 1.1861, suggesting consolidation below this level would be seen and below the Kijun-Sen (now at 1.1803) would bring pullback to 1.1770, however, reckon 1.1745-50 (50% Fibonacci retracement of 1.1637-1.1861) would limit downside and bring another rise later, above said resistance at 1.1861 would extend recent see from 1.1554 low to previous resistance at 1.1880, then 1.1900-10.

In view of this, would not chase this rise here and we are looking to buy euro on pullback as 1.1745-50 should limit downside. Below the upper Kumo (now at 1.1711) would defer and signal a temporary top is formed instead, bring weakness to previous resistance at 1.1678 (now support) but only break there would provide confirmation.

CPI: Core Inflation Is Back on Track

Consumer price inflation rose more slowly in October due to a pullback in energy prices, but core inflation picked up. Reflation increasingly looks to be back on track which will support further Fed tightening.

Soft Headline, but Core Inflation Is Strengthening

Inflation was toned down in October with the Consumer Price Index increasing 0.1 percent after two months of 0.4 percent-plus gains. The yearover- year rate subsequently edged back down to 2.0 percent. The slowdown reflected a decline in energy prices as the supply disruptions surrounding Hurricanes Harvey and Irma abated. Gasoline prices fell 2.4 percent over the month, more than offsetting increases for electricity and gas services. Food prices were flat in October and have continued to increase more slowly than other items over the past year, up 1.3 percent.

Excluding food and energy, inflation was noticeably stronger. The core index rose a "high" 0.2 percent (0.225 percent before rounding). That pushed the year-over-year change up to 1.8 percent. The performance over the past three months is even more impressive; core prices have advanced at a 2.4 percent annualized rate, making the slowdown in inflation earlier this year look increasingly temporary.

Core services have been the primary source of inflation weakness this year, but services prices rose 0.3 percent in October. Gains were broadly based, including shelter, medical care, transportation and even wireless phone services, which were up for a second straight month.

Core goods prices also posted a rare increase. Replacement demand following the recent hurricanes generated some support to used car prices which were up 0.7 percent. However, other categories were also more supportive of inflation - or at least less deflation - including medical goods (non-prescription drugs) and tobacco products.

Reflation Supportive of Fed Tightening Plans, But Will Be Slow

The Fed has struggled this year in determining if the slowdown in core inflation has been due to a confluence of one-offs or more persistent disinflationary forces. We have been of the mindset that the pullback has been due primarily to a few unique factors that look unsustainable. The primary categories holding down core inflation earlier this year - cell phone plans, housing costs and physician services - have all gathered steam in recent months. The pickup clears the way for a December rate hike and supports the case for continued tightening in the year ahead.

The FOMC, however, will be watching the PCE deflator more closely. While much of the early estimates for the PCE deflator are derived from the CPI report, healthcare, which is about twice as important in the PCE deflator, is derived from Producer Price Index (PPI) estimates. Yesterday's PPI showed healthcare services inflation slipping to 1.2 percent, the smallest 12-month change since the spring of 2016. That should keep the core PCE deflator from swiftly rebounding to the FOMC's target in the coming months and keep the FOMC on the path of only gradual rate increases.