Sample Category Title

Daily Wave Analysis: Bullish EUR/USD Retraces Tto 50% Fib Level Of Wave-4

Currency pair EUR/USD

EUR/USD reached the 161.8% Fibonacci target of wave 3 (pink) after breaking above the 1.1750 resistance. The current bearish price action could be a retracement within this impulsive wave 3 pattern (pink).

The EUR/USD is probably building multiple wave 3s now. The Fibonacci levels of wave 4 (purple) could act as support and create a potential bouncing spot for a continuation of wave 3 (pink).

Currency pair GBP/USD

The GBP/USD is unable to break the support (blue) and resistance (red) trend lines. A breakout is needed before a larger directional move can be expected, although a bullish breakout still faces resistance from the Fibonacci levels of wave 2 (orange).

The GBP/USD could be expanding the choppy correction via a complex correction of WXY (green).

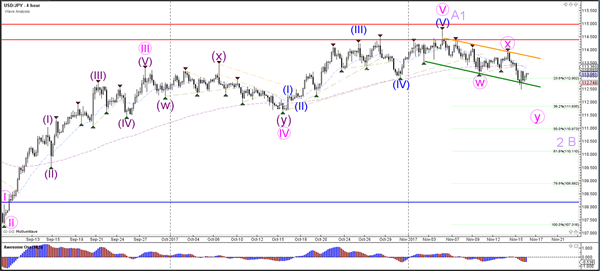

Currency pair USD/JPY

The USD/JPY's choppy bearish trend channel bounced at the 23.6% Fibonacci level. A bearish breakout below the 23.6% Fib could see a drop lower to the Fibonacci levels of wave 2 or wave B (light purple).

The USD/JPY is testing the Fibonacci support and trend line (blue). Price could be building an ABC (blue) within wave B (blue).

Market Update – Asian Session: Aussie Employment Change Lower Than Expected, KRW 13-Month Higher

Headlines/Economic Data

Japan

As of the time of writing, the Nikkei 225 is higher by over 0.7%, after opening down by 0.2%. Nikkei heavy component Fast Retailing has gained over 0.8%.

In the technology space, Canon has moved higher following press speculation that it may raise its annual dividend by ~7%. Meanwhile, shares of Softbank have risen by more than 0.9%.

Casualty insurers are lower amid press speculation that their FY profits may miss forecasts on exposure to hurricanes in the US. USD/JPY has traded steady ahead of the US House vote on its tax bill, expected later on Thursday.

(JP) Japan GDP seen at 1.6% for FY17 v 1.3% in FY16; lifted by strong exports and businesses investing in labor-saving measures – Nikkei

(JP) JAPAN Q3 HOUSING LOANS Y/Y: 2.9% V 3.3% PRIOR

(JP) Japan MoF sells ¥800B v ¥1.0T offered in 0.6% 20-yr JGBS; avg yield 0.573%; bid-to-cover 4.13x

(JP) Japan PM Abe top economic advisory panel in a draft will suggest they see economy closer to deflation exodus - financial press

Korea

The Kospi has gained over 0.3%, amid more than 0.5% gains in shares of Samsung Electronics.

More action has, however, been seen in the currency markets, as the Korean Won has hit the highest level against the US dollar since Oct 2016. On Wednesday, the Bank of Korea and Bank of Canada announced a bilateral currency swap agreement.

The agreement is expected to have limited direct impact on FX rates, says a Bank of Korea Deputy Gov. Even still, South Korea’s Finance Ministry reiterated that it would closely monitor markets in cases of ‘severe volatility.’

USD/KRW Onshore opens at KRW1,106 (13-month high) v KRW1,112 prior close

China/Hong Kong

The Shanghai Composite opened the session -0.3%, while the Hang Seng opened +0.4%. The Information Technology index in Hong Kong has risen by over 1%. Component, Tencent, has gained over 1.7% after reporting better than expected Q3 results.

The Hang Seng Energy index is trading lower by over -0.1%. Gasoline and diesel prices may be raised in China by as soon as Friday, according to a press report.

The Hang Seng Property Index is little changed. Banks in China are said to be conducting stress tests related to loans made to the property sector, according to a local press report.

China Legislature Official Huang said China should levy a property tax as it curbs speculation. China should also reform its FX reserves system and have the MOF play a larger management role, says the official.

Separately, the PBoC’s Research Head said there could be the risk of a ‘big crisis’ if economic reforms are too slow.

(CN) China port names moving higher on chatter that China could cut shipping fees

(CN) China may raise gasoline prices by CNY265/ton and diesel prices by CNY250/ton as of Friday

USD/CNY (CN) PBOC sets yuan reference rate at 6.6286 v 6.6263 prior

(CN) China PBoC Open Market Operations (OMO): CNY330B v CNY330B injected in 7, 14 and 63-day reverse repos prior; Net injection CNY310B v CNY220B prior

(CN) China Oct YTD Outbound Investments $86.3B, -40.9% y/y in USD terms

Australia/New Zealand

(AU) AUSTRALIA OCT EMPLOYMENT CHANGE: +3.7K V +18.8KE; UNEMPLOYMENT RATE: 5.4% V 5.5%E

Full-Time Employment Change: 24.3K v +6.1K prior

Part-Time Employment Change: -20.7K v +13.7K prior

Participation Rate: 65.1% v 65.2%e

AUD was little changed after an initial spike higher, little reaction in the bond market

(AU) Australia Nov Consumer Inflation Expectation y/y: 3.7% v 4.3% prior

(NZ) New Zealand Nov ANZ Consumer Confidence Index: 123.7 v 126.3 prior; M/M: -2.1% v -2.8% prior (7-month low)

(NZ) New Zealand sells NZ$200M in Apr 2025 bonds; avg yield 2.6711%

Other Asia

In the Philippines, the Peso currency and equity markets are moving higher following Q3 GDP data. The y/y figure rose by a better than expected 6.9%.

The economy is still not overheating, according to the Philippines Central Bank Chief Espenilla.

North America

(CA) Bank of Canada (BOC) Wilkins: Reason for caution is desire to avoid policy reversal, motivated by lower than expected inflation

(US) Christie's auction sells last privately held Leonardo da Vinci painting entitled 'Salvator Mundi' for record $450M (expected $100M+)

Ahead of the expected vote, US President Trump said tax cuts are getting ‘close.’

Various US companies have priced secondary offerings following the NY close and ahead of the expected tax vote (including JELD, STKS, NCLH, ACHN and GDI). Floor & Décor Holdings also priced a 6.5M share secondary, which was below the originally planned 9M shares.

Levels as of 23:00ET

Nikkei +0.7%, Hang Seng +0.5%; Shanghai Composite -0.1%; ASX200 +0.1%, Kospi +0.5%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.2%; FTSE100 +0.1%

EUR 1.1792-1.1769; JPY 113.05-112.76; AUD 0.7609-0.7569;NZD 0.6878-0.6850

Dec Gold +0.1% at $1,278/oz; Dec Crude Oil +0.0% at $55.34/brl; Dec Copper +0.2% at $3.06/lb

Equities notable movers

Australia/New Zealand

STO.AU Not currently engaged in talks, received earlier takeover approach from Harbour Energy at A$4.55/shr; +11%

RKN.AU Sells Accountants Practice Management business to MYOB (as expected) for A$180M cash; to pay special dividend; +33%

Hong Kong/China

700.HK Reports Q3 (CNY) Net 18.0B v 15.7Be, Rev 65.2B v 61Be; +1.5%

410.HK Approves special interim dividend of CNY0.576; +8.7%

4.HK Announces share price adjustment after spinoff of Wharf Estates; -63%

US

TIME Said to be in talks regarding selling itself to Meredith - US press

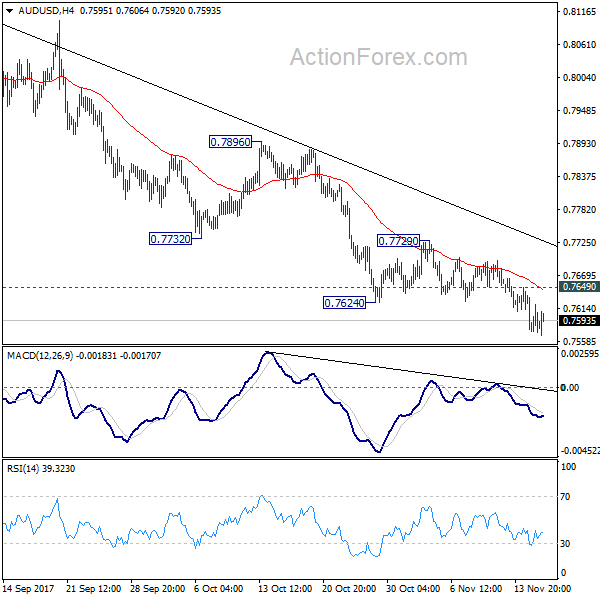

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7563; (P) 0.7598; (R1) 0.7622; More...

Intraday bias in AUD/USD remains on the downside with 0.7649 minor resistance intact. Current fall from 0.8124 is expected to target next key cluster level at 0.7322/8. On the upside, above 0.7649 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 0.7729 resistance holds.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Dollar Recovering Mildly as Sentiments Stabilized, Aussie Stays Weak after Job Data

US equities generally lower overnight as the global market rout continued, but sentiments stabilized in Asian session. DOW lost -138.19 pts, or -0.59% to end at 23271.28. It breached 23251.11 near term support during the day, which could seen as a sign of near term reversal. 10 year yield also followed lower, down -0.046 at 2.335 but it s held well above 2.273 structural support so far. Meanwhile, Dollar is trying to recovery after the deep selloff, in particular against Euro, earlier in the week. Overall, the sell off in oil is seen as a factor driving risk aversion. But WTI might now be stabilizing around 55 handle. Another risk averse factors emerges as US politicians are raising doubts on the legislation of the tax plan.

Senator Johnson and Collins oppose Republican tax bill

In US, Republican effort to push through the tax cuts before year end suffered serious setbacks yesterday. Republican Senator Ron Johnson openly expressed his opposition to both the Senate and House versions of the tax bill. He criticized that the plan benefits large corporations at the expense of the others, including smaller companies. Republican Senator Susan Collins also criticized the move to include the never-ending repeal of Obamacare in the tax bill.

Boston Fed Rosengren supports December hike

Boston Fed President Eric Rosengren, a hawk, said yesterday that "it is quite likely that unemployment will fall below 4 percent, which is likely to increase pressures on inflation and asset prices." And, "that suggests the need to continue to gradually remove monetary policy accommodation, which is quite consistent with market expectations of another increase in December."

ECB Praet talked the move back to conventional measures

ECB Chief Economist Peter Praet laid out the path that the central bank is moving from unconventional measures to conventional measures in policy setting. He noted that "as we progress towards a sustained adjustment in the path of inflation and approach the time when net purchases will gradually come to an end, the residual monetary support needed to assist the economy in its transition to a new normal will increasingly come from forward guidance on our policy rates." Then, "policy rates will eventually regain their status as the main instrument of policy, and our forward guidance will revert to a singular approach."

ECB Hansson: The world looks better to us

ECB Governing Council member Ardo Hansson sounded optimistic as he said "the world looks better to us" and the economy is enjoying "strong growth". Also, "with greater confidence in the outlook for the real economy there is some scope for a prudent but obvious recalibration of policies." Regarding policy, he emphasized that "one of my colleagues always likes to say monetary policy is not a solo, it's a quartet: you have the asset purchases, the accumulated stock of purchases, the re-investment policy and forward guidance."

AU job growth missed, unemployment rate at 4.5 year low

Australian Dollar recovers mildly today after job data, but stays near term bearish. Employment market grew 3.7k in October, slowed from prior month's 26.6k and missed expectation of 18.9k. Nonetheless, full time jobs grew 24.3k while part time jobs dropped -20.7k. Also, Unemployment rate, dropped to 5.4%, down from 5.5%. That's also the lowest reading since February 2013. Also from Australia, consumer inflation expectation rose 3.7% in November.

RBA Assistance Governor Luci Ellis said yesterday that there more growth engines in the country other than mining. She pointed out that infrastructure spending, tourism and services as some examples. Also, the economy would be supported by relatively fast population growth and pickup in participation. In addition, there will be "indirect effects" from better infrastructure that boost productivity.

Looking ahead

UK retail sales will be the main focus in European session. Eurozone will release CPI final. Later in the data. US will release jobless claims, Philly Fed survey, import price index, industrial production and NAHB housing index. Canada will release manufacturing sales and international securities transactions.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7563; (P) 0.7598; (R1) 0.7622; More...

Intraday bias in AUD/USD remains on the downside with 0.7649 minor resistance intact. Current fall from 0.8124 is expected to target next key cluster level at 0.7322/8. On the upside, above 0.7649 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 0.7729 resistance holds.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8067). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7896 near term resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | AUD | Consumer Inflation Expectation Nov | 3.70% | 4.30% | ||

| 0:30 | AUD | Employment Change Oct | 3.7K | 18.9K | 19.8K | 26.6K |

| 0:30 | AUD | Unemployment Rate Oct | 5.40% | 5.50% | 5.50% | |

| 9:30 | GBP | Retail Sales M/M Oct | 0.20% | -0.80% | ||

| 10:00 | EUR | Eurozone CPI M/M Oct | 0.10% | 0.40% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct F | 1.40% | 1.50% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct F | 0.90% | 0.90% | ||

| 13:30 | CAD | Manufacturing Sales M/M Sep | -0.20% | 1.60% | ||

| 13:30 | CAD | International Securities Transactions (CAD) Sep | 9.85B | |||

| 13:30 | USD | Initial Jobless Claims (NOV 11) | 234k | 239k | ||

| 13:30 | USD | Philly Fed Manufacturing Index Nov | 24.1 | 27.9 | ||

| 13:30 | USD | Import Price Index M/M Oct | 0.40% | 0.70% | ||

| 14:15 | USD | Industrial Production M/M Oct | 0.50% | 0.30% | ||

| 14:15 | USD | Capacity Utilization Oct | 76.30% | 76.00% | ||

| 15:00 | USD | NAHB Housing Market Index Nov | 67 | 68 | ||

| 15:30 | USD | Natural Gas Storage | 15B |

Elliott Wave View: SPX Intra-Day

SPX Intra Day Elliott Wave view suggests that the rally to 2597.02 ended Intermediate wave (3). Intermediate wave (4) pullback is currently in progress as a double three Elliott Wave structure. Down from 2597.02, Minor wave W of (4) ended at 2566.33 and Minor wave X of (4) ended at 2587.66. While staying below 2597.02, expect the Index to continue lower towards 2538 – 2557 area to finish Intermediate wave (4) before Index resumes the rally or bounce in 3 waves at least. We don’t like selling the Index and expect dip buyers to appear from the aforementioned area for at least a 3 waves bounce.

SPX 1 Hour Elliott Wave Analysis

Market Morning Briefing: The Aussie Disappointed By Breaking Below The 0.7600 Support Yesterday

STOCKS

Dow (23271.28, -0.59%) has come down as expected and could soon head towards our mentioned target of 23200-23000 in the next few sessions. Note that 23000 is an important near term support and is likely to hold in the medium term producing a bounce back to levels near 23400/500 in the next week.

The downward momentum from levels below 13600 has been fast and sharp in Dax (12976.37, -0.44%). While the momentum continues it may possibly not stop at 12900 levels. A break below 12900 could then take it lower towards 12800-12600 in the next couple of weeks.

Nikkei (22210.45, +0.83%) is trading slightly higher than yesterday's close at 22028.3, but has scope of falling towards 21800 in the medium term (maybe by end of Nov'17). Dollar Yen (112.98) trades below 113 just now and in case it continues to fall further, Nikkei would also eventually come down. Near term looks bearish.

Shanghai (3398.91, -0.11%) has come down as expected and could test 3380 as mentioned yesterday. Note that the 3380-3450 is an important region of trade for the near term and is likely to hold for some time.

Nifty (10118.05, -0.67%) made an intra-day low of 10090 yesterday exactly as expected and bounced back slightly to close above 10100. Note that 10000-10100 is an important near term support which is likely to hold in the first attempt producing a bounce back towards 10300/400. But in case 10000 breaks on the downside (it could happen next week if the Bears continue to remain strong) then the index could be vulnerable to a sharp fall by end of the month.

COMMODITIES

1260-1280 continues to remain as strong support for the near term and while that holds, some movement within 1300-1260 is possible before the upward rally resumes in Gold (1278.20). The price seems to be stable and quiet for the last few sessions and may remain so this week.

Silver (16.98) is down in line with our expectation. Sideways trade within 16.60-17.20 is possible in the near term.

Brent (61.93) could test some support near 61.00-60.85 and if that holds, a bounce back towards 63-64 would be on the cards contrary of our expectation to a fall to 60 just now.

WTI (55.33) could trade in the 54.90-56.00 region (could extend to 54.70 and 57 on either side) for a few sessions. Only a break below 54.90, if seen could take it lower towards 54 in the medium term.

Copper (3.0555) has broken immediate support levels and could now be headed lower to test 3.00-2.95 in the coming sessions.

FOREX

Yesterday, we suggested a range of 1.1850-1500 for the Euro (1.1781) for some weeks. A high of 1.1861 was seen yesterday and the Euro has come off a bit from there, despite a further dip in US yields (see Interest Rates below). Look for a near-term range of 1.1850-1710.

Dollar-Yen (113.02) has also recovered a bit from an intra-day low of 112.47 seen on break below 113.00. Possibly we may see sideways trade between 112.50-114.35 for the next several days if 112.50 turns out to be a decent Support.

The Euro-Yen (133.15) has come down a bit as the Resistance at 134.00 held well enough. However, the overall trend might be biddish while above 132.

The Pound (1.3173) is a prime candidate for range trade between 1.3025-3275 for the next several days. Good time for those who have the ability to buy low/ sell high and then reverse the trade and then do it again.

The Aussie (0.7598) disappointed by breaking below the 0.7600 support yesterday and has seen a low of 0.7559 so far today. If it does not see a sharp bounce from here, it could be vulnerable to some more downside to 0.7500.

Dollar-Rupee (65.2150) may trade between 65.10-30 over the next few days.

INTEREST RATES

US Bond yields have dipped some more after the US October CPI (+2.05% y/y) came in lower than the previous reading of 2.23%. The 10Yr (2.34%) and 30Yr (2.78%) are down from 2.38% and 2.83% respectively. We have to see if they bounce from current levels or not.

There is fresh concern in the markets about the continued flattening of the US Yield Curve, but perhaps the 10-2 Spread (0.29%) will find Support near current levels.

While there is concern in the USA about yield flattening (will someone please tell once and for all whether Inflation will rise or not), there is concern in India that Inflation will indeed rise. And that has been pushing the 10Yr GOI (7.0170%) higher. Levels below 6.8% seem to be outside consideration now.

No Conviction

No conviction

Picking bottoms on the USD is an exercise in futility even more so after the washout in near-term currency ranges that transpired this week

Indeed, a risk-off point of view continued to influence the market structure overnight with global interest rates rallying; traders becoming increasingly long on theory but short on execution when it comes to rationalizing a flatter the US yield curve

The Euro

To be honest, there are few plausible explanations as to why EUR USD got paid at 1.1859 overnight other than when risk-off mode permeates, and with few EU politic fissures hitting the headlines; the EURO performs admirably as a funding currency.

But other than the than the EUR ramp, the markets have become little more than a pin the tail on the donkey exercise, and despite lower lows and lower highs on the USD this week, there are signs an intransigent greenback is getting ready to stare down the bears. ( forever the eternal USD bull)

Japanese Yen

The break of 113 was nowhere near as severe as anticipated. But with the Nikkie on a massive losing streak from this point forward, it should be a risk-off storyline given that the Tokyo sell-off was the core driver behind this weeks move.

The Australian Dollar

With a mere 25 bps priced in the 2018 rates curve and the RBA downgrading their inflation trajectory, is there any better signal to Sell the AUD?

Weak wages are not a new theme in Australia but yesterday’s data all but reinforced the notion that things are likely to get worse

The AUD employment figures have sparked a small short-covering move on the revisions, but with traders in a fade mode, the AUDUSD is unlikely to challenge.7625

Employment change was +3.7k vs 18.8k expected. However looking at the details, part-time employment fell -20.7k, undermining the +24.3k in full-time jobs. As a consequence, the unemployment rate unexpectedly edged lower to 5.4%.

The initial decision was AUD lower on the headline, but the currency has since recovered

EM Asia FX

The long end of the US rates curve is driving sentiment.After yesterday USD regional meltdown with USDKRW plunging below the 1110 support level and USDPHP broke through 51.00 I think its safe to say investors like Asian currencies despite the sell-off in regional equities. Ok so there is a massive break in logic but price action must be respected.

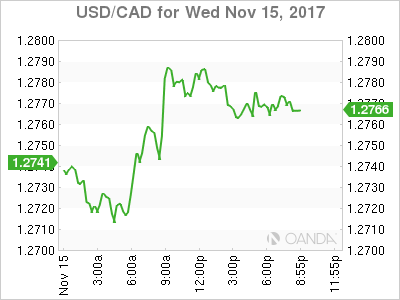

USD/CAD Canadian Dollar Lower On Weak Oil And Upcoming NAFTA Talks

The Canadian dollar depreciated on Wednesday. The loonie lost 0.30 percent versus the greenback after solid inflation and strong retail sales data show the U.S. Federal Reserve is ready to announce a rate hike in December. Positive inflation growth and gains in retail sales will make it harder for the doves within the Federal Open Market Committee (FOMC) to vote against an interest rate lift at the end of the December monetary policy meeting. The meeting will mark the last influential decision of Fed Chair Janet Yellen’s helm at the central bank.

US core consumer prices rose 0.2 percent in October and an unexpected rise by retail sales by 0.2 percent when the forecast called for a flat reading boosted the USD across the board and validating the telegraphed announcement by the Fed that it would hike in December. The market focused on fundamentals on Wednesdays after a couple of weeks with little data to chew on with the tax overhaul in the US as the biggest factor in currencies.

The fall in oil prices as US inventories showed a hefty buildup when a drawdown was expected put more pressure on the CAD. Oil prices surged after the Saudi Arabia Crown Prince Mohammed bin Salman triggered a power play that ended up with various prices and influential business men under arrest and raised questions on how well would the de facto leadership of the Organization of the Petroleum Exporting Countries (OPEC) handle rising diplomatic infighting between members.

The USD/CAD gained 0.30 percent on Wednesday. The currency pair is trading at 1.2769 after the December rate hike chances have been boosted by strong inflation and retail sales data in the US. The market has already priced in a rate move in December, but with a slowdown in inflation and incomplete data due to the tropical storms in September the Fed could keep from raising rates this year. The expected wider gap between Canadian interest rates and the Fed funds rate added pressure to a loonie that was slowly losing momentum due to the losses in oil prices.

Bank of Canada (BoC) Deputy Governor Wilkins spoke today in New York. She reiterated that the central bank will be cautious on its monetary policy decisions which was a departure from the comments in June when the BoC hiked rates in July with a hawkish tone to be followed by a surprise back to back hike in September. NAFTA unknowns remains a concern as it could negatively effect the Canadian economy with the fifth round getting underway in Mexico City.

The NAFTA renegotiation talks will be without the Trade Ministers and will hope to take on less contentious topics such as textiles, services, labor and intellectual property. The last round ended with little progress and Canadian and Mexican negotiators unhappy at the America first proposals from the Trump Administration.

NAFTA has been a target for Trump supporters, but the agreement has the backing of some republican congress members who have sided with their democrat counterparts urging the President to leave US requirements for autos as the original agreement. The move was considered a poison pill as it would unfairly favour US production in the detriment to the other two nations.

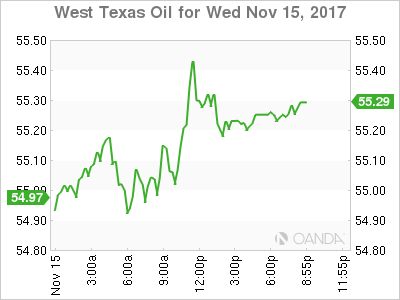

The price of oil is net weekly lows after for the second week in a row there was a surprise buildup of US crude inventories. The prices of West Texas Intermediate is trading at $55.20 after the Energy Information Administration (EIA) published a rise of 1.9 million barrels. The market was expecting a miss on the forecast after the API reported an overnight rise of 6.5 million barrels. The Industry group data and the US movement’s are not correlated 1 to 1. The market had already sold off crude, but since the scale of the official buildup was lower some investors reentered their long positions.

The IEA had cut demand forecasts earlier in the week contradicting the estimates form the Organization of the Petroleum Exporting Countries (OPEC). The price of oil has been trading higher after the events in Saudi Arabia but with no new or development, prices are discounting the political uncertainty in the Kingdom.

The battle between the rise in production in the US and the cut agreement between OPEC and other major producers will continue. The Russian Energy Minister Alexander Novak spoke today to reassure that Russian producers are committed to the agreement to cut output, but he did not mention if they will go ahead with an extension of said agreement. The OPEC and major producers will meet in Vienna on November 30.

Market events to watch this week:

Thursday, November 16

4:30am GBP Retail Sales m/m

8:30am USD Unemployment Claims

Friday, November 17

8:30am CAD CPI m/m

8:30am USD Building Permits

Gold Slightly Lower As Markets Digest Consumer Spending And Inflation Numbers

Gold prices have posted small losses in the Wednesday session. In the North American session, the spot price for an ounce of gold is $1278.34, down 0.14% on the day. On the release front, the focus was on consumer indicators. CPI and Core CPI matched the forecasts, with gains of 0.1% and 0.2%, respectively. Consumer spending reports were a mix – retail sales gained 0.1%, below the estimate of 0.2%. Core Retail Sales came in at 0.2%, beating the forecast of 0.0%. As well, the Empire State Manufacturing Index slowed to 19.4 points, well short of the estimate of 25.3 points. This reading marked a 4-month low.

Gold is showing volatility on Wednesday. The metal pushed to a high of $1289.50, its highest level since October 20. However, the metal has given up these gains in the North American session, after the release of retail sales and CPI. We could continue to see movement from gold, as investors keep a close eye on the tax overhaul bill which is on its way to Congress. If the bill gains steam, we are likely to see the dollar move higher, which could weigh on gold prices.

Although consumer price index numbers remain weak, there was better news from producer price index reports on Wednesday. Core PPI and PPI remained unchanged at 0.4%, beating their estimates. PPI increased at an annualized rate of 2.8%, its fastest gain since February 2012. Inflation levels are being closely monitored by the Federal Reserve, as stronger inflation levels would likely result in a rate hike in early 2018. The markets are very bullish on higher rates, with a December hike priced in at 93% and a January raise priced in at 89%.

The heads of central banks met on Tuesday at an ECB event, with a focus on communication with the markets and the public. Federal Reserve Chair Janet Yellen acknowledged that the FOMC committee of 19 members posed problems, as members did not always speak with a unified voice. This led to the markets picking up on differences between policymakers, often leading to market volatility. Yellen admitted that this problem would not be solved anytime soon, saying it was “a work in progress”.

Yen Gains Ground as US Inflation Remains Weak

The yen has improved in the Wednesday session. In North American trade, USD/JPY is trading at 113.03, down 0.38% on the day. On the release front, Japanese Preliminary GDP gained 0.3%, missing the forecast of 0.4%. In the US, CPI and Core CPI matched the forecasts, with gains of 0.1% and 0.2%, respectively. Consumer spending reports were a mix – retail sales gained 0.1%, shy of the estimate of 0.2%. Core Retail Sales came in at 0.2%, beating the forecast of 0.0%. There was disappointing news on the manufacturing front, as the Empire State Manufacturing Index slowed to 19.4 points, well short of the estimate of 25.3 points. This reading marked a 4-month low.

There were no surprises from consumer inflation and spending data for October. Inflation indicators showed small gains, as a strong US economy has not led to higher prices. Consumer spending was unexpectedly strong in September, with Core Retail Sales posting an impressive gain of 1.6 percent. However, the October reading slowed to just 0.2 percent. These early third quarter numbers are somewhat disappointing, coming just weeks before the busy Christmas season. The Federal Reserve is keeping a close eye on inflation numbers, as an uptick in inflation indicators could mean additional rate hikes in 2018. The markets expect some action from the Fed, having priced in a rate hike in December at 91% and a January hike at 89%.

Japan's economy continues to expand, but Preliminary GDP for the third quarter slowed to 0.3%, down from 0.6% in Final GDP for Q2. This marks the longest expansion since 2001, but a stronger economy has not translated into higher inflation levels. Earlier in the week, BoJ Governor Haruhiko Kuroda acknowledged the inflation issue, saying "it is not easy to quickly dispel the deflationary mindset that has formed over the course of 15 years of deflation." Kuroda added that he expects inflation levels to rise, and that the BoJ would continue its massive monetary easing, a key component of the "Abenomics" program.