Sample Category Title

More Signs of Stabilization in U.S. CPI in October

Highlights:

- Year-over-year headline CPI growth edged down from 2.0% from 2.2% in September as part of a surge in September gasoline prices was reversed.

- Food prices were unchanged on a month-over-month basis, but the year-over-year rate ticked up to 1.3% - its highest reading since November 2015.

- Excluding food & energy prices, 'core' CPI inched up 0.2% on a month-over-month basis and the year -over-year ticked up to 1.8% after 5 straight 1.7% readings.

The headline year-over-year rate dipped lower to 2.0% but only because gasoline prices partially retraced a hurricane-related 13% surge in September. Energy prices were still up 6.4% from a year ago.

Year-over-year food price growth ticked up to 1.3% - still modest but nonetheless the fastest annual gain for the component since November 2015.

Core CPI increased 0.2% on a month-over-month basis. That was enough to push the year-over-year rate of growth in October up to 1.8% after five straight 1.7% readings. A sharp drop in telecommunication prices earlier this year is still biasing the measure lower. Excluding that drop, core price growth would be right at the Fed's 2% inflation objective. There is still little evidence that inflation is getting out of hand but the stabilization in core measures in recent months and indications that demand growth remains solid - including somewhat stronger-than-expected October retail sales separately reported this morning - should reassure the Fed that price growth will tick higher rather than lower going forward. A 25 basis point hike in the fed funds target range is widely expected in December. We continue expect further demand growth and further tightening in labour markets will ultimately prompt a gradual hiking cycle to continue next year.

US Data Not Strong Enough to Reverse USD Sell-off

- European equities suffer more losses as the stock market correction continues. Main indices lose up to 1%. US stock markets open on a weak footing as well, dropping around 0.75%.

- US consumer prices barely rose in October (0.1% M/M) as the boost to gasoline prices from hurricane-related disruptions to Gulf Coast oil refineries was unwound, but rising rents and healthcare costs pointed to a gradual buildup of underlying inflation (0.2% M/M).

- US retail sales rose more than expected in October (0.2% M/M). The market had expected no change after retail sales clocked a blistering 1.9% M/M rise in September when people replaced vehicles and items destroyed by hurricane Harvey and Irma. Control retail sales, which exclude volatile items, rose 0.3% from September.

- The UK labor market showed signs of slowing in the third quarter as the number of people in work fell for the first time in almost a year even as unemployment held at a 42-yr low. There was no sign of respite for UK wage earners though who face a squeeze on incomes from high inflation, after pay growth held steady in the latest three months

- BoE governor Broadbent said markets have placed too much emphasis on the idea that interest rates need to be kept low in the face of Brexit uncertainty. "Even as inflation rose, and the rate of unemployment fell further, interest-rate markets continued to under-weight the possibility that bank rate might actually go up this year," he said.

- Waiting too long to halt monetary policy stimulus could be disruptive, ECB Hansson said, adding that a more supportive euro zone economy justified a shift in the central bank's policies.

- Greece invited holders of about €30 bn euros in its debt to swap 20 small outstanding bonds for 5 new benchmark ones. The plan is to boost market liquidity before Greece emerges from bailouts in August 2018. The eligible papers are 20 bonds that were issued in 2012 in a voluntary scheme where private bondholders took a 53.5% haircut.

- Signs that Sweden's red-hot housing market is cooling off are unlikely to impact monetary policy now, but may make the central bank's path toward normalizing rates trickier, Swedish Riksbank Governor Ingves said.

Rates

Bull flattening yield curves

Global core bonds gained ground today, bull flattening the yield curves. The move occurred mainly in Asian and European dealings on the back of deteriorating risk sentiment on stock markets, re-establishing last week's lost correlations. A disappointing Bund auction couldn't change the tide. Brent crude stabilized after yesterday's sell-off, but the picture remains fragile. The upleg in core bonds petered out ahead of key US eco data. Both CPI inflation and retail sales moderated from last month's levels, but printed near consensus. Their impact on core bond markets was negligible.

At the time of writing, US yield changes range between flat and -3.7 bps (30-yr). The German yield curve drops up to 4 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany are broadly unchanged with Portugal (+5 bps), Greece (+4 bps) and Spain (+3 bps) underperforming. Portuguese bonds fell prey to some profit taking following the impressive rally of late. Investors anticipate a second rating upgrade into investment grade by Fitch in December (current rating BB+ with positive outlook).

The German Finanzagentur held a 10-yr Bund auction (€3 bn 0.5% Aug2027). Demand was weak with total bids amounting only to €2.97 bn, below the amount on offer and below the €3.68 bn average at the previous 4 Bund auctions. The Bundesbank retained €0.52bn for secondary market operations, resulting in an official bid cover of 1.2 (real bid cover 0.99). The auction had no tail.

Currencies

US data not strong enough to reverse USD sell-off

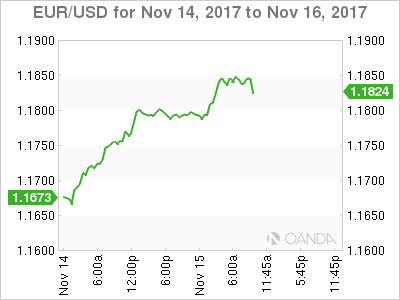

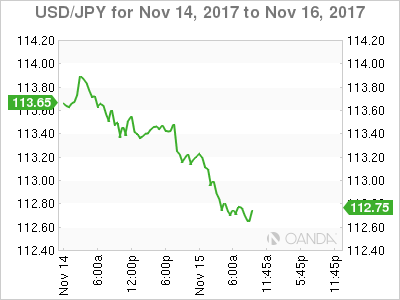

The euro rally/USD sell-off continued today. There was again no high profile story to explain the move. Overall risk sentiment again weighed more on the dollar than on the euro. EUR/USD (temporary) cleared the 1.1837 post-ECB top. US retail sales and CPI were marginally better than expected, but didn't help the dollar much. EUR/USD trades in the 1.1820 area. USD/JPY is changing hands around 112.75.

Profit taking on risky assets continued overnight. Japan Q3 growth was marginally below consensus at 1.4% Q/Qa, with especially private consumption being a drag on growth. USD/JPY drifted further south in the 113 big figure (yen strengthened). The decline in core yields and risk-off sentiment outweighed Japanese domestic data, as usual. EUR/USD (1.1790 area) maintained yesterday's gains.

There were no data with market moving potential in EMU. The euro short squeeze simply resumed at the start of the European trading session, almost exactly the same way as was the case yesterday morning. EUR/USD set a new post-ECB top north of 1.1837. Again, we didn't see a specific trigger. The move was partially euro strength, but growing risk off sentiment also kept the dollar in the defensive. In the afternoon, the focus turned to the 'key' US CPI and retail sales data. Except for the early month data (ISM, payrolls) those data are the last important input for the December 13 Fed decision. Unfortunately (from a market point of view), the retail sales and the CPI were very close to expectations. If anything, they were marginally stronger than expected. Still, the dollar lost a few more ticks immediately after the publication of the data, but the USD decline finally petered out. The USD currency is looking for an intraday bottom. USD/JPY trades in the 112.75 area (from an intraday low near 112.50 and despite ongoing risk-off). EUR/USD jumped to the 1.1860 area, but a test of the next key resistance (1.1880) didn't occur. EUR/USD trades currently again in the 1.1820 area. We still consider the USD sell-off overdone (especially against the euro), but for now there is no trigger to turn the established trend. So, no good reasons to try to catch the falling (USD-)knife yet.

EUR/GBP tests 0.90

UK labour market data showed a mixed picture today. Wage growth (2.2% Y/Y) was marginally higher than expected, but remains low. The unemployment rate was stable as expected at 4.3%. Employment growth in the three months to September unexpectedly declined by 14k. A 52K rise was expected. The unexpected decline in employment confirms the recent slowdown in the UK economy. Sterling lost some further ground after the publication of the data. EUR/GBP jumped temporary north of 0.90, but the gain could not be sustained. The pair trades currently in the 0.8985 area. Cable spiked to the 1.3135/40 area, but trades currently again around 1.3165. The price moves in the sterling cross rates were also perturbed by the intraday price swings in the dollar and the euro.

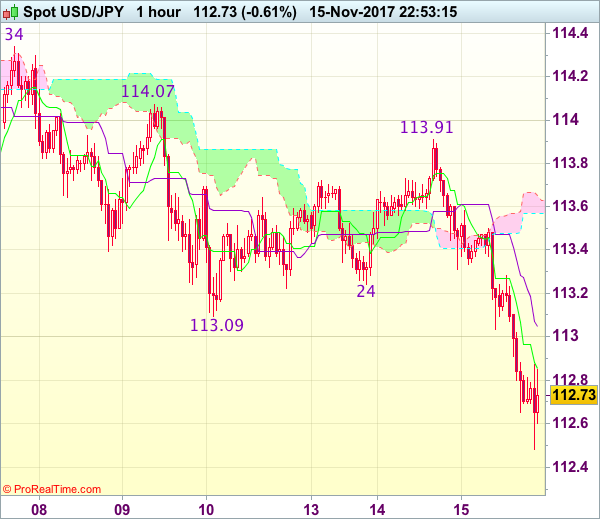

Trade Idea Wrap-up: USD/JPY – Hold long entered at 112.60

USD/JPY - 112.72

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 112.86

Kijun-Sen level : 113.05

Ichimoku cloud top : 113.65

Ichimoku cloud bottom : 113.57

Original strategy :

Bought at 112.60, Target: 113.60, Stop: 112.25

Position : - Long at 112.60

Target : - 113.60

Stop : - 112.25

New strategy :

Hold long entered at 112.60, Target: 113.60, Stop: 112.25

Position : - Long at 112.60

Target : - 113.60

Stop : - 112.25

As the greenback has remained under pressure after recent selloff on dollar’s broad-based weakness, oversold condition should prevent further sharp fall below 112.40-45 and bring rebound later today or tomorrow, above 113.05-09 (current level of the Kijun-Sen and previous support) would suggest low is possibly formed, bring test of 113.25-30 but break of latter level is needed to add credence to this view, bring further gain to 113.60-65, having said that,. price should falter well below resistance at 113.91.

In view of this, we are holding on to our long position entered at 112.60. Below support at 112.30 would signal the fall from 114.74 top is still in progress for weakness towards 112.00-05 before prospect of another rebound.

Commentary on US CPI / Retail Sales

Sellers immediately attacked the Dollar on Wednesday after U.S. consumer prices marginally increased by 0.1% in October – the smallest gain witnessed in three months.

Although the 0.1% increase in consumer prices was in line with market expectations, it continues to highlight how stubbornly low inflation in the United States remains a recurrent theme. While it is widely expected that the Federal Reserve will raise interest rates in December, the future path of rate hikes beyond 2017, is open to discussion amid low inflation concerns. On a positive note, U.S. retail sales unexpectedly rose 0.2% in October which is likely to boost sentiment towards the U.S. economy and offer some support to the tired Dollar.

Taking a look at the technical picture, the Dollar Index dipped towards 93.40 following the release. The 94.00 level has the ability to transform into a dynamic resistance that could encourage a further decline towards 93.50 and 93.00, respectively. A solid breakout back above 94.50 threatens the current bearish setup.

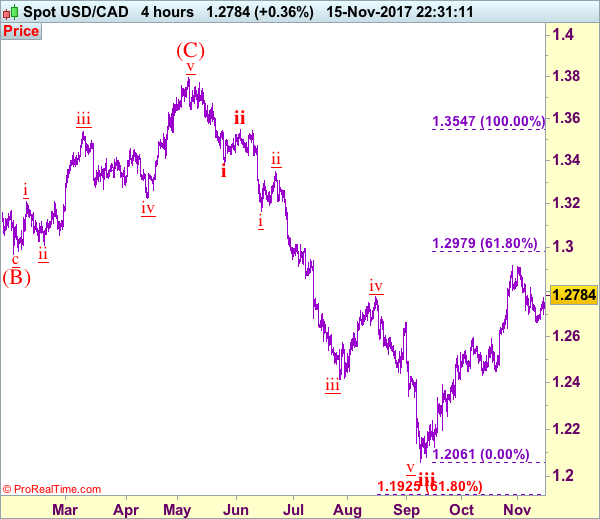

Trade Idea: USD/CAD – Exit short entered at 1.2770

USD/CAD - 1.2785

Trend: Near term up

Original strategy :

Sold at 1.2770, Target: 1.2570, Stop: 1.2830

Position: - Short at 1.2770

Target: - 1.2570

Stop: - 1.2830

New strategy :

Exit short entered at 1.2770

Position: - Short at 1.2770

Target: -

Stop:-

Although the greenback did retreat after meeting resistance at 1.2773 yesterday, the pair found renewed buying interest at 1.2700 and has staged another rebound today, dampening our bearishness and suggesting near term upside risk remains for the rebound from 1.2665 (last week’s low) to extend gain to 1.2800, then test of resistance at 1.2820 but a firm break above this level is needed to signal the correction from 1.2917 has ended, bring further gain to 1.2880, then towards this level which is likely to hold from here.

In view of this, would be prudent to exit short entered at 1.2770 and stand aside for now. Only below said support at 1.2700 would revive bearishness and signal the rebound from 1.2665 has ended, bring another test o this level, break there would extend the fall from 1.2917 top for retracement of recent rise to support at 1.2636 but a drop below this level is needed to signal recent rise has ended at 1.2917, bring further fall to 1.2600 and later towards 1.2550-60.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

US: Finally, Core Inflation Firms in October

A modest 0.1% increase in October for the headline consumer price index (CPI), saw total inflation ebb slightly to 2.0% year-on-year, from 2.2% in September. October's modest increase is right in line with market expectations.

Energy prices fell 1.0% m/m in October, only partly giving back their hurricane-induced bump-up in August and September. Food prices were unchanged on the month, and are up only 1.3% from twelve months ago.

Core inflation finally gained a step, rising 0.2% in October. That took the year-on-year pace up one tick to 1.8%, after remaining stuck at 1.7% for most of the middle of 2017. The shelter index was a key factor taking core higher, with both rent and owners' equivalent rent firming 0.3% on the month. Increases in core inflation were widespread. Some examples include medical care (+0.3%), used cars and trucks (+0.7%), tobacco (+1.6%), education (0.3%) and wireless phone services (+0.4%).

Finally, both core goods (0.1% m/m) and core services (0.3% m/m) were rowing in the same direction, taking core inflation higher. Core services are now up 2.7% year-on-year, the fastest pace since February. Core goods prices are still down 1% year-on-year, reflecting past strength in the U.S. dollar.

Key Implications

One would expect that in an economy running at a 3% annualized pace over the past two quarters, and an unemployment rate at a 17-year low, that inflation would show signs of picking up. October's inflation data is a tentative step in the right direction after a soft patch through much of 2017 worried many at the FOMC.

Today's report should remove any lingering doubts that the Fed will hike rates in December. From a full-employment standpoint, the argument for rate hikes is strong. But, inflation has been a missing piece for much of the year. Now that it is starting to move into place, we see little to prevent the Fed from moving ahead next month.

US: Retail Sales Continue to Rise in October, Extending the Post-Hurricane Rebound in September

Retail sales rose 0.2% m/m in October, ahead of expectations for a flat reading. The rise follows an upwardly-revised growth of 1.9% m/m in September (previously 1.6%), which was boosted by a rebound in purchases following Hurricanes Harvey and Irma.

Most categories rose in October, with the only major declines experienced by building material stores (-1.2%), gasoline stations (-1.2%), and non-store retailers (-0.3%). Having said that, the decline in sales at gasoline stations was partly a price story, with the price of gasoline pulling-back as the impact of refinery shutdowns waned.

The 'control group' used in calculating GDP (excluding gas, autos, building materials, and food services) was up 0.3% on the month - on par with consensus. Still, it follows an upwardly revised gain of 0.5% in September suggesting more consumption spending during the third quarter.

Key Implications

With upward revisions in September and better-than-expected retail sales growth in October, consumer spending appears likely to increase by around 3% (annualized) in the third quarter. While some of the recent momentum reflects the normalization of activity following the hurricanes, looking through the volatility consumers are likely to continue to a vital support to economic growth through the next year.

Alongside an acceleration in inflation, this report cements the case for the Federal Reserve to raise interest rates in December. Further out, the outlook for rate hikes over the course of 2018 will depend in large part on the stance of fiscal policy. A major tax cut at this stage in the cycle, while giving support to disposable income growth, is likely to be met with additional interest rate hikes by the Federal Reserve. Over the medium term, this will help return the economy to its trend rate of growth around 2.0%.

XAU/USD Analysis: Gold is Pushing Higher

As I have showed in my previous Gold Spot analysis, the price rejected from the POC zone, making a push higher. The price followed the continuation move and now we have another POC formed for possible new bullish swing. If the price stays above 1283.90 we might see a continuation towards 1287.70 and 1288.44. Breakout might happen above 1288.44 towards 1290.37 and 1293.91. However in case of retracement pay attention to 1278.15-1280.05 POC zone as the price might reject towards H3 then. So as long as the price is above D H3 and W H3, the bias is bullish.

- H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

- W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

- D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

- D L3 - Daily Camarilla Pivot (Daily Support)

- D L4 - Daily H4 Camarilla (Very Strong Daily Support)

- PPR - Progressive Polynomial Channel

- POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

U.S. Retail Sales Rise in October, Inflation Picks Up

Data this morning shows that U.S consumers increased their spending only slightly in October, a sign that households spend moderated after a hurricane-related bump the previous month.

Sales at restaurants, retail stores and online-shopping platforms rose +0.2% m/m to a seasonally adjusted +$486.55B in October. Compared with a year earlier, sales increased +4.6%.

The market were expecting a +0.1% increase in October.

Digging deeper, sales at gas stations fell -1.2%, likely reflecting pullback from the spike in gas prices after the storms. Motor vehicles and parts dealers had a +0.7% sales increase, compared to a +4.6% increase in September.

Ex-motor vehicles, retail sales were up +0.1% in October, and ex-gas, sales were up +0.4%. Excluding both categories, sales were up +0.3% m/m.

Core U.S inflation finally picks up

The CPI index rose +0.1% in October, in line with markets expectations. The increase was driven largely by higher shelter costs, as food prices were unchanged and energy costs declined.

U.S consumer prices were up +2.0% on the year last month. Core prices were up +0.2% on the month and +1.8% on the year.

Note: That's slightly higher compared to September's reading, when core inflation was up +1.7% y/y - it's the strongest in six months.

Empire manufacturing index disappoints

Other data shows that business activity continued to grow strongly in New York State.

The Empire manufacturing index headline general business conditions index fell -11 points from the multiyear high (30.2) it reached last month, it remained firmly in positive territory at 19.4.

The new orders index climbed to 20.7 and the shipments index came in at 18.4 - readings that pointed to ongoing solid gains in orders and shipments.

Market reaction

U.S Treasuries have held onto their overnight gains after consumer prices rose only slightly.

The yield on U.S 10-year note is trading at +2.331%. The market was looking for a stronger-than-expected inflation reading that would of solidified the Fed's case to raise rates at next month's meeting. This morning's data has done little to suggest acceleration in inflation that might pose a threat to bond prices.

The USD remains on the back foot on investor concerns over the U.S tax reform proposal losing momentum.

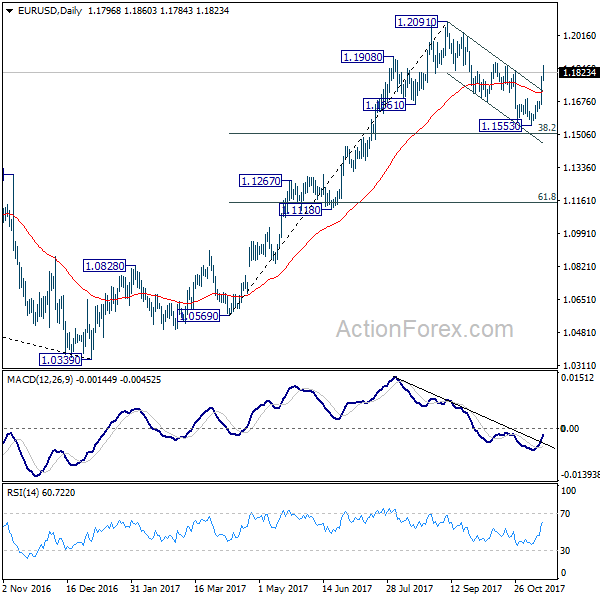

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1704; (P) 1.1754 (R1) 1.1848; More...

EUR/USD's rise from 1.1553 is still in progress. The break of 1.1836 resistance should confirm our bullish view. That is, correction from 1.2091 has completed at 1.1553 already. Further rally would be seen to retest 1.2091 high. On the downside, below 1.1784 minor support will bring consolidations before staging another rally.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be cautious on 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1346) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.