Sample Category Title

EURGBP Intraday Analysis

EURGBP (0.8811): The EURGBP extended the declines yesterday as price breached past the support level at 0.8867 - 0.8857 level. This indicates continued decline with the next support at 0.8778 likely to be tested. Any short-term bounces are expected to be contained near the 0.8867 - 0.8857 level which could now act as resistance. However, a higher low being formed near the support of 0.8778 could suggest another move to the upside, provided the resistance level can be breached.

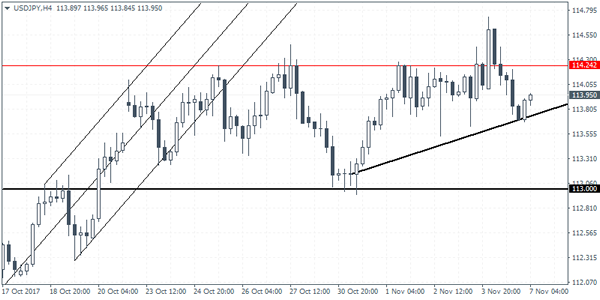

USDJPY Intraday Analysis

USDJPY (113.95): The USDJPY attempted to open on a bullish note yesterday. The yen weakened after comments from BoJ's Governor Kuroda. Kuroda said that the central bank's monetary policy was still needed for some time reiterating the central bank's commitment to fight deflation. Despite the brief rally in the dollar, USDJPY settled to close weaker on the day. Price action still consolidates below the resistance level which increases the risk of a downside correction. The evolving inverse head and shoulders pattern along with the ascending triangle pattern put the bias to the upside. However, USDJPY will need to clear the 114.00 price handle to post further gains.

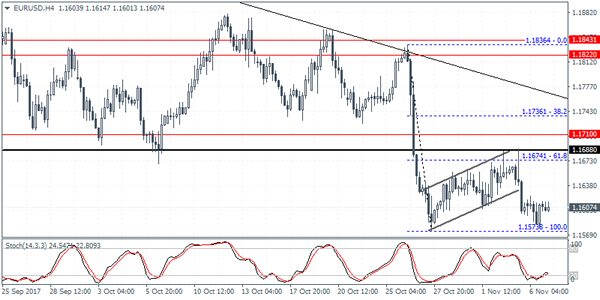

EURUSD Intraday Analysis

EURUSD (1.1607): Price action in EURUSD was muted as the overall price trend turns flat. EURUSD has been moving sideways for nearly seven consecutive days following the declines below the 1.1700 support level. On the 4-hour chart, following the breakout from the bearish flag pattern, EURUSD was seen turning bullish with a bullish engulfing pattern on the 4-hour chart. This could suggest some near term upside. However, with price supported above the 1.1573 handle, there is a strong potential for the bearish flag pattern to be invalidated. Still, EURUSD is expected to maintain its range within 1.1688 and 1.1573 levels of resistance and support.

Oil Prices Surge On Saudi Politics

Oil prices were seen trading higher reaching a two-year high as political developments in Saudi Arabia saw a wave of arrests of high ranking officials. WTI Crude oil prices rose to settle at $57.35 a barrel while Brent oil futures rose to $64.27. The gains in oil prices came as the OPEC general body meeting is due to be held in a few weeks time.

On the economic front, the RBA's monetary policy meeting earlier today saw no changes to interest rates. The RBA gave an optimistic view of the economy as it held interest rates unchanged at 1.5%. It forecasted that inflation would rise over time and expects GDP to improve as well.

Looking ahead, the economic data today includes speeches from ECB President Mario Draghi followed by Fed Chair Janet Yellen later in the afternoon. The BoC Governor Poloz is also expected to speak today. The German industrial production and the Eurozone retail sales figures will be released.

EURO Sellers Still Retain Control Below 1.1640

The euro has staged a minor recovery above the 1.1600 level against the U.S dollar, after the U.S dollar index started to decline during late Monday trade. A bullish double-bottom pattern on the EURUSD pair encouraged technical buying interest, as euro sellers failed to break the former monthly price-low at 1.1573. Traders now await European Central Bank President Mario Draghi’s opening remarks, as he delivers a scheduled speech at the ECB Forum on Banking Supervision, in Frankfurt, Germany.

The EURUSD still remains bearish while trading below the 1.1640 technical level, with sellers still retaining control of the pair. Further declines towards the 1.1599 and 1.1573 levels still seem most likely.

Should price-action break above the 1.1640 level for a sustained period, the bearish dynamic surrounding the pair will change, with buyers then likely to target the 1.1670 again.

Sterling Intraday Bullish ABove 1.3160

The British pound has started to recover against the U.S dollar, hitting 1.3177, amidst a broad-based sell-off in the U.S dollar index that began on Monday. Technical buying interest has accelerated in the GBPUSD pair, after intraday buyers pushed price-action clearly back above the 1.3130 resistance level. The pair currently trades towards the highs of the week, with financial markets attention now firmly focused on the upcoming speech by FED Chair Janet Yellen during today's U.S trading session.

The GBPUSD pair has turned intraday bullish while trading above the 1.3160 level. Further upside towards the 1.3200 and 1.3259 levels remains most likely while price-action holds above the 1.3160 region.

Should price action fall below the 1.3160 level, a decline towards the 1.3130 seems possible. Further extended GBPUSD intraday support is found at 1.3096 and 1.3070.

Central Bank Speeches Headline Tuesday

Central bank developments will take centre stage on Tuesday, as commentary from the ECB and Fed will move the financial markets.

European Central Bank President Mario Draghi will deliver a speech at 09:00 GMT. The ECB announced recently that it will begin to unwind its stimulus program, but that the duration of the bond-buying will likely continue beyond September 2018. The central bank is responding to a much-improved regional economy.

In North America, Federal Reserve Chairwoman Janet Yellen will deliver a speech at 19:30 GMT. Yellen is wrapping up her final months as Fed boss after President Donald Trump announced Jerome Powell as her replacement.

North of the boarder, Bank of Canada (BOC) Governor Stephen Poloz will also deliver a speech on Tuesday. The BOC has been actively raising interest rates this year in response to a booming Canadian economy.

Earlier in the day, the Reserve Bank of Australia (RBA) held its main interest rate at 1.5%, as expected by the great majority of economists.

'Conditions in the global economy are continuing to improve. Labour markets have tightened and further above-trend growth is expected in a number of advanced economies, although uncertainties remain,' the RBA said in its official rate statement. 'Growth in the Chinese economy is being supported by increased spending on infrastructure and property construction, with the high level of debt continuing to present a medium-term risk. Australia's terms of trade are expected to decline in the period ahead but remain at relatively high levels.'

In terms of economic data, the European Commission's statistical agency will report on retail sales at 10:00 GMT. Receipts at retail stores are forecast to rise 0.6% in September after falling 0.5% the previous month. This translates into an annualized gain of 2.7%.

In US data, the government will report on consumer credit change for the month of September. Meanwhile, the American Petroleum Institute (API) will report on weekly crude inventories ahead of the official tally on Wednesday.

EUR/USD

The euro was little changed on Tuesday, hovering just north of 1.1600. The pair remains in a tight range, with markets still speculating on the outlook of ECB policy. Investors can, therefore, expect little market movement for the euro without a major fundamental catalyst.

GBP/USD

Cable rose sharply at the start of the week, climbing back above 1.3100 US. The GBP/USD exchange rate was last seen trading at 1.3169. It faces a strong support zone near 1.3030. On the opposite side of the ledger, resistance is likely found just ahead near 1.3200.

USD/CAD

The Canadian dollar has strengthened in recent sessions, with the USD/CAD falling back toward the 1.2700 handle. The pair is down from more than three-month highs as the greenback backtracks against a basket of world peers.

Currencies: Dollar Fails To Overcome Technical Resistance, For Now

Sunrise Market Commentary

- Rates: Test of contract high (Bund) likely; sell-the-uptick?!

The German Bund is near the 163.43 contract high. Failure to sustainably move above this level could be an opportunity to sell-the-uptick. The rally of oil prices didn't impact bonds until now and we look out whether that remains the case. The start of the US' quarterly refinancing operation is negative for US Treasuries. - Currencies: Dollar fails to overcome technical resistance, for now

The dollar came close to/tested important technical levels yesterday and against the euro and the yen, but no real break occurred. Today, the calendar is again thin. Still we look out whether a next attempt might succeed. Sterling regains most of the post-BoE decline. For now, we don't seen any fundamental news to explain the move.

The Sunrise Headlines

- US equities ended with small gains, led by the energy sector after crude price soared more than 3%. Brent crude rose above $64/barrel for the first time since June 2015. Asian indices gain up to 1% this morning.

- Australia's central bank showed increasing confidence in the investment picture outside mining while retaining concerns about the prospects for household spending as it kept interest rates at a record-low 1.5%

- New Zealand's government confirmed it's considering a dual mandate for the central bank targeting full employment alongside price stability. WSJ reported that Fed Williams advocates the adoption of a price level targeting strategy in the face of the ongoing low inflation.

- The ECB will reinvest €130bn of bonds that are set to mature in the coming year, according to data released yesterday – but the early months of 2018 are likely to see a low amount of re-investments.

- The ECB's plan to force banks to set aside more money against future bad loans got tacit support from euro zone finance ministers despite concerns in Italy the move might weaken some of its banks.

- Italy's centre-right led by former prime minister Berlusconi has fended off a strong challenge from the populist Five Star Movement to win the presidency of Sicily, ringing alarm bells for Matteo Renzi and his centre-left Democratic party (PD) in a poll seen as the final test ahead of Italy's next general election.

- Today's eco calendar contains German industrial production, EMU retail sales and US JOLTS job openings. ECB Draghi, Lautenschlaeger and Nouy speak at an ECB conference. Austria, Germany and the US tap the market

Currencies: Dollar Fails To Overcome Technical Resistance, For Now

Dollar holding near recent highs

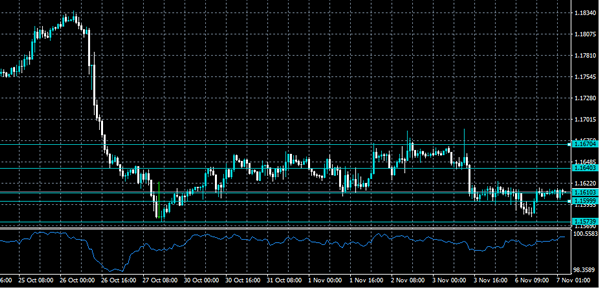

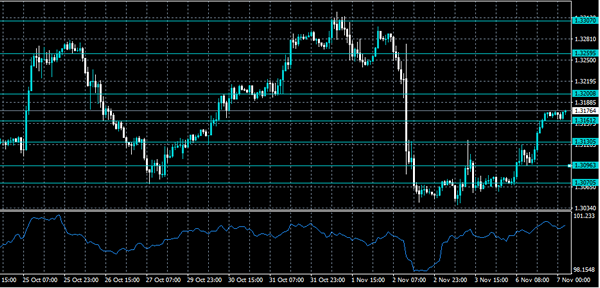

Yesterday, FX trading showed two faces. Initially, the euro was in the defensive even as EMU eco data were strong. USD/JPY, EUR/JPY and EUR/USD all lost ground in lockstep. EUR/USD dropped temporary below 1.16, but the correction stalled ahead of the 1.1575 post-ECB low Late in Europe, the dollar came under pressure. The USD decline coincided with a new up-leg of the oil price. EUR/USD closed the session at 1.1610, little changed from Friday. USD/JPY finished the session at 113.71 (from 114.07).

Overnight, Asian equities are in very good shape. Several indices including the Nikkei are trading at multi-year highs. Higher oil and commodity prices are supporting energy and materials companies. USD/JPY trades again in the 114 area. The USD/JPY performance remains mediocre given the stock market rally. EUR/USD is little changed in the 1.1605/10 area. The Reserve Bank of Australia as expected left its policy rate unchanged at 1.5%. The RBA remains positive on growth and employment, but low inflation/wages and a high consumer debt make the RBA cautious to raise rates in the foreseeable future. The AUD trades little changed below 0.77.

The eco calendar remains thin today, with the September US JOLTS job openings and the EMU retail sales. None is a market mover. The speeches of Draghi, Lautenschlager and Nouy at an ECB forum on supervision on “Europe's changing banking landscape” might be important for banks shares, but not for FX or bond markets. The start of the US quarterly refunding and some political events may be the focus today.

Last week, EUR/USD held close to the post-ECB low, but there were no followthrough losses for the euro. The nomination of Powell as next Fed-Chairman, new proposals to change the US tax code and Friday's payrolls were not able to break this stalemate. Until now, the dollar failed to really profit from high interest rate differentials (especially at the short end of the curve). This is slightly disappointing for USD bulls. That said, EUR/USD currently trades more than 400 ticks below the cycle top. The wide positive interest rate differential should give the dollar downside protection unless there is high profile US negative news. For now, the rise in oil prices had hardly any impact on interest rates or on FX. We look out whether this remains the case. Yesterday's USD price action was mixed. EUR/USD failed to go for a test of the 1.1575 area. USD/JPY was again not able to break the 114.50 range top. We maintain a sell-on-upticks bias, but the dollar clearly needs good news to realise any sustained gains. It is not sure this news will come in very soon.

From a technical point of view, EUR/USD dropped below 1.1670/62 support, but no convincing follow-through dollar gains occurred. A break below the 1.1575 post-ECB low would confirm that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. USD/JPY's momentum was positive in past months. The pair regained 110.67/95 resistance. The pair tested the 114.49 MT range top, but the attempt failed. A sustained break would improve the technicals. We remain cautious to preposition for further USD/JPY gains.

EUR/USD nearing the 1.1575 post-ECB low, but no real test yet

EUR/GBP

Sterling extends rebound

On Friday, sterling regained modest ground after Thursday's post-BoE sell-off. This rebound continued yesterday. We didn't see any eco or political news to explain the follow through sterling buying. Maybe some investors hope on progress in the next round of Brexit-negotiations which starts later this week. For now, the political scandals (inside and outside the Conservative party) don't affect sterling trading. EUR/GBP closed the session at 0.8815. The decline was at least partially due to euro softness. Cable also rebounded and finished the session at 1.3171.

Overnight, the Like for like BRC retail sales unexpectedly declined 1.0 Y/Y (a more modest slowdown from +1.9% Y/Y to +0.8% was expected). Later today, the Halifax house prices will be published. They probably won't be important for sterling trading. So, domestic politics and Brexit will probably set the tone for trading. We look out how far the repositioning of sterling goes.

MT technical. In September, sterling rebounded as the BoE prepared markets for a rate hike. This rebound ran into resistance as markets anticipated that any rate hikes would be very gradual and limited. This view was confirmed at last week's BoE policy meeting. EUR/GBP currently trades in a 0.8733/0.9033 consolidation range. A downside test of this range was rejected last week. We maintain the view that the 0.8733 -0.8652 support area will be though to break in a sustainable way. A EUR/GBP buy-on-dips approach is favoured. 0.9023/33 is the first important resistance for the EUR/GBP cross rate

EUR/GBP: reverses most of post-BoE sterling decline, but no important technical levels are hit.

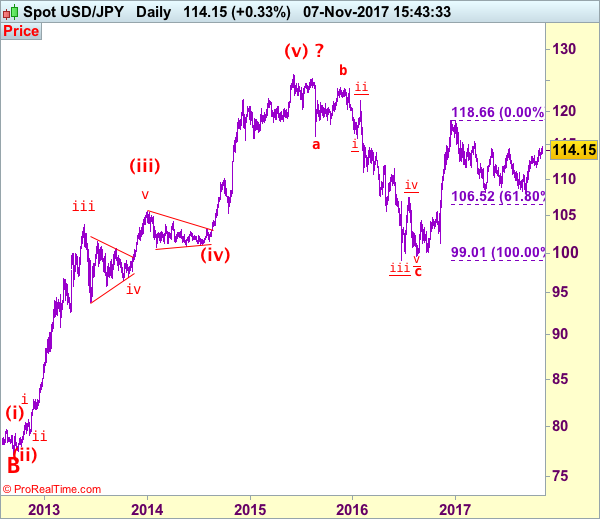

USD/JPY Elliott Wave Analysis

USD/JPY - 114.16

USD/JPY – Wave V of larger degree circle V has possibly ended at 75.31 and major correction has commenced and already met indicated target at 125.00.

As the greenback has maintained a firm undertone after recent break of indicated previous resistance at 114.45-50, adding credence to our bullish view that the rise from 107.32 low is still in progress and bullishness remains for this move to extend gain to 115.00, above there would signal the correction from 118.66 top has ended earlier at 107.32 and the rise from there may extend further gain to previous resistance at 115.51. Looking ahead, a sustained breach above this level at 115.51 would retain bullishness, then subsequent gain to 116.00-10 and possibly 116.50-60 would follow.

Our preferred count is that, triangle wave IV (with circle) ended at 101.45 and the circle wave V brought dollar down to the record low of 75.31 in 2011 and the subsequent rebound signal major correction has commenced with A leg ended at 84.19, followed by wave B at 77.14 and impulsive wave C is now unfolding (indicated upside target at 125.00 had been met) for gain towards 127.00 level. In the event dollar drops below support at 99.01, this would confirm medium term decline from 125.86 top (2015 high) has resumed for subsequent weakness to 98.00 and possibly 97.00.

Under this count, this wave C is unfolding as impulsive waves with (1) (2), 1 2 ended at 80.67, 79.07, 82.84 and 81.69 respectively, hence the extended wave 3 has ended at 103.74 and wave 4 correction of recent upmove should bring weakness to 92.57, then towards 90.88 but psychological support at 90.00 should limit downside and bring another rally later in wave 5, indicated target at 125.00 had been met and gain to 127.00 cannot be ruled out but reckon price would falter below 130.00.

On the downside, whilst initial pullback to 113.00-10 cannot be ruled out, reckon downside would be limited to 112.50-60 and 112.00 would contain downside, renewed buying interest should emerge above support at 111.65 and bring another rise later. Only a drop below said support at 111.65 would suggest a temporary top is formed instead, bring weakness to 111.00 but downside should be limited to 110.40-50 and support at 109.55 should remain intact. A breach of strong support at 109.55 would abort and suggest the rebound from 107.32 has ended instead, risk weakness to 109.00 and possibly 108.50-60 but price should stay well above said support at 107.32 and bring another rebound later.

Recommendation: Buy at 112.95 for 114.95 with stop below 111.95.

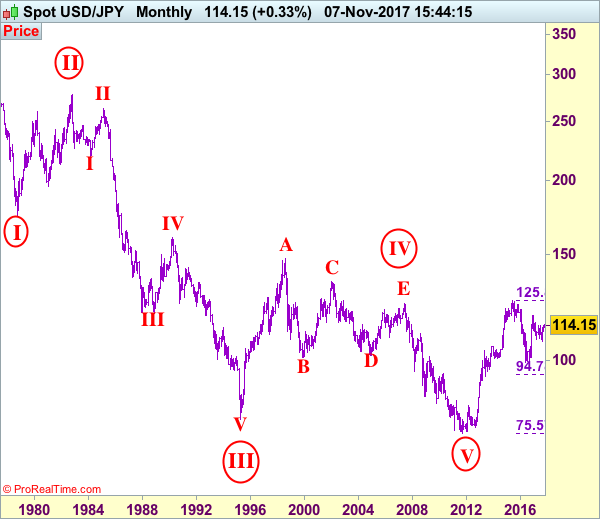

On the monthly chart, we have changed our preferred count that an impulsive wave is unfolding with major wave III with circle ended at 79.75, then followed by wave IV with circle and is labeled as a triangle with A: 147.64 (11 August, 1998), B: 101.25, C: 135.20, D: 101.67 and E leg ended at 124.14 to end the wave IV with circle. Hence, wave V with circle commenced from there and hit a record low of 75.31, however, the subsequent strong rebound signals this circle wave V has possibly ended there, hence gain to (indicated upside target at 122.00 and 125.00 had been met), the retreat from 125.86 suggests wave A of major correction has ended there and wave B correction back to 99.00, then 95.00 would be seen, however, reckon downside would be limited to 90.00, bring another rebound in wave C next year.

Oil Hits A New Two-Year High, No Immediate Resistance

Oil prices continue to be front and center for traders in a relatively quiet market. Brent crude surged 3.5% to trade above $64 on Monday, after the arrests in Saudi Arabia raised investors’ concerns over the stability of the Middle East region. Comments from Saudi Gulf Affairs Minister, Thamer Al-Sabhan, stating that the government of Lebanon has declared war on Saudi Arabia, added more tooil’s political risk premium. Fundamentals remain very positive, with OPEC’s willingness to resume the 1.8 million production cuts, and booming demand from developed and emerging markets. However, conflicts within the Middle East are becoming a majorinfluencer on energy markets, and a further surge in prices will likely be due to political risk premium rather than fundamental support. If tensions escalatefurther, traders will be targeting $70 for Brent, although such levels may not be sustainedin the long run.

In currency markets, the dollar changed little against its major peers, after falling slightly on Monday. There weren’t any significant economic releases to justify the dollar’s weakness, but U.S. TreasuryBonds seem to have a story to tell. Unlike U.S. stocks, which are showing a very bright economic outlook, yields on U.S. 10-year Treasury Bonds fell for six out of the seven past trading sessions, to trade at 2.31%. The yield curve flattened further, with the 2-year–30-year spread touching 117 basis points, a level last seen in 2007. The flattening yield curve suggests that economic growth and inflation willremain weak in the mid-to-long term which is just the opposite of what stock markets are suggesting. Who's right and who's wrong, only time will tell.

The decision by Reserve Bank of Australia to keep interest rates unchanged had little impact on the Australian dollar. AUDUSD jumped 0.2% after the announcement, but erased gains shortly thereafter and fell slightly into negative territory. The central bank’s language hasn’t changed, and continues to expect GDP growth to pick up and to average around 3% over the next few years, despite signs of weak inflation and consumer spending. Given the balanced approach by RBA, expect the Aussie to remain in narrow trading range.

The economic calendar is also light today, with only a few tier-2 economic data reports due for release. European Central Bank President, Mario Draghi, is due to speak later today at the ECB forum on banking supervision. But given that ECB has just revealed its plan of a gentle taper two weeks ago, I don’t expect his comments to move the markets.