Sample Category Title

GBPUSD – Vulnerable, Sees Price Extension

GBPUSD - The pair weakened further during Friday trading session opening the door additional weakness. Support lies at the 1.3050 level where a break will turn attention to the 1.3000 level. Further down, support lies at the 1.2950 level. Below here will set the stage for more weakness towards the 1.2900 level. Conversely, resistance stands at the 1.3150 levels with a turn above here allowing more strength to build up towards the 1.3200 level. Further out, resistance resides at the 1.3250 level followed by the 1.3300 level. On the whole, GBPUSD continues to face further downside pressure.

US Indices Rebound Ahead Of GDP Data

- Tech Earnings Lift US Futures;

- EURUSD Breaks Technical Support After ECB Decision;

- USD Poised For Strong End to the Year;

- Sterling Under Pressure But Remains Range-Bound Ahead of BoE.

US futures are pointing to a higher open on Wall Street on the final trading day of the week, buoyed by better than expected earnings reports after the close on Thursday.

We've seen a bit of a wobble in US equity markets this week following what was a very steady climb in previous weeks. We're seeing decent gains across Europe as well, with the exception of Spain and Italy with the former being weighed down by the ongoing independence dispute between Catalonia and Madrid. With votes taking place in Barcelona and Madrid today, it's likely to be a defining day following an almost month long stand-off between the two.

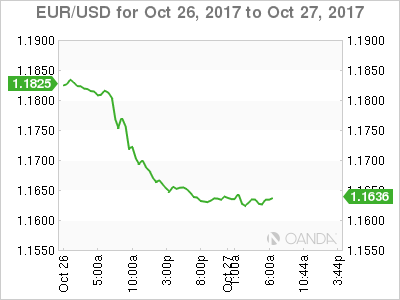

The euro is coming under pressure once again on Friday, a move that's being made worse by the resurgence in the dollar. From a technical perspective, we've seen significant breaks in both EURUSD and the dollar index – not entirely surprising given the significant contribution of the euro to the index – on the back of yesterday's ECB meeting, which could trigger much bigger gains for the greenback over the coming weeks.

A combination of profit taking as the ECB announcement fell in line with expectations and some very dovish language drove significant losses in the single currency on Thursday and triggered a move below a significant support zone. This in turn forced the dollar index through a major resistance zone which could see it rally over the coming weeks and months. The next big test for EURUSD could come around 1.15 but further downside is possible.

Should we see the appointment of hawkish policy makers at the top levels of the Federal Reserve in the coming weeks, which is already starting to be priced in, it will only aid the rebound in the greenback. Tax reform is another potential boost for the currency and while Donald Trump has struggled getting parts of his agenda over the line, this may prove a little easier.

It's been a big week for earnings but focus today will temporarily shift back to the economic data, with fewer companies reporting and GDP figures for the third quarter being released. The economy performed very well in the second quarter and another strong number is expected today, which will only increase the likelihood that the Fed raises interest rates at the December meeting. While there's no room for manoeuvre on this for the December meeting – a rate hike is fully priced in – there's plenty of room next year with markets severely under-pricing the three hikes the Fed has projected for 2018.

The pound is also trading in negative territory again on Friday, extending the losses initiated on Thursday that may have been triggered by worrying retail sales data from CBI. Despite this, the pound remains range-bound with traders potentially sitting on the fence ahead of next week's Bank of England meeting, at which we could see the first rate hike since the financial crisis.

Dollar’s Rate Divergence Rally

Continued optimism about U.S tax reform after yesterday's House passing of a budget plan is helping to keep the U.S dollar well supported.

With the European Central Bank (ECB) out of the way, market expectations regarding the next Fed chair is also giving the greenback a lift with Powell and Taylor – two 'hawks' – seen coming to the finish line first, now that Ms. Yellen is apparently not in the picture.

Note: President Trump is expected to reveal his choice to lead the Fed by Nov. 3. The Fed's next rate decision is on Nov. 1 and expectations are for no rate hike. The market is pricing in a +90% odds for the Fed to increase them at the Dec. meeting

In equities, Euro gains are broad-based this morning as the ECB's 'slow' approach to reducing stimulus is encouraging some equity bulls.

However, the exception is Iberian assets. Spanish stocks continue to underperform as Europe's worst constitutional crisis for 30-years comes to a head. Federal politicians are expected to pass legislation later today to allow PM Rajoy to seize control of the Catalan administration.

Later this morning, the advance reading on U.S Q3 GDP is due (08:30 pm EDT). The market is expecting growth of +2.6%.

1. Stocks well supported

In Japan, the Nikkei surged +1.2% to a fresh 21-year high overnight, led by financial shares as U.S yields remained elevated and by tech shares after their U.S counterparts posted strong earnings. The broader Topix rose +1%.

Down-under, Australia's S&P/ASX 200 Index fell -0.2% to solidify its first weekly slide in four, while South Korea's Kospi index climbed +0.7%.

In Hong Kong, stocks have ended the week on a firmer footing after an encouraging slew of earnings from U.S. tech firms and the ECB's having extended its stimulus. The Hang Seng index rose +0.8%, while the China Enterprises Index gained +1.7%.

In China, blue chip stocks rallied on President Xi's vision of a 'new era.' Signs of economic resilience have also fuelled the three-week rally. The blue-chip CSI300 index rose +0.4%, bringing its gains to +2.1% this week. The Shanghai Composite Index edged up +0.3% or +1.1% on the week.

In Europe, regional indices trade mostly higher across the board with notable outperforms in the DAX and CAC which trades at all time highs, while the Spanish IBEX trades lower.

U.S stocks are set to open in the 'black' (+0.2%).

Indices: Stoxx600 +0.5% at 393.3, FTSE +0.3% at 5504, DAX +0.7% at 13229, CAC-40 +0.9% at 5502, IBEX-35 -0.5% at 10293, FTSE MIB -0.1% at 22782, SMI +0.3% at 9225, S&P 500 Futures +0.2%

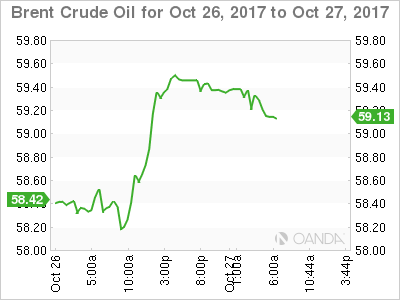

2. Brent crude approaches $60 as markets tighten, gold lower

Oil prices are steady, with benchmark Brent crude trading a tad shy of +$60 a barrel, supported by comments from Saudi Arabia's crown prince backing the extension of OPEC-led output cuts.

Brent crude is unchanged at +$59.30. The contract is more than +30% above this year's low print touched in June. U.S light crude is down -4c at +$52.60, but still +25% above its June 2017 low. U.S crude prices have been capped by rising U.S production.

OPEC is expected to discuss extending that agreement of cutting daily production by -1.8m bpd at a meeting in Vienna on Nov. 30.

However, rising U.S crude production continues to remain an issue for OPEC as it strives to clear a global overhang. Data from the EIA this week showed that U.S crude production rose by +1.1m bpd to +9.5m bpd in the week ended Oct. 20.

Gold prices have inched down ahead of the U.S open, to print new low in nearly three weeks, as the dollar finds traction against G7 currency pairs after the ECB extended its bond-buying programme. Spot gold has dropped -0.1% to +$1,265.71 per ounce. It's heading for a weekly decline of about -1%.

3. Dovish taper tantrum has the Fed as lonesome hawk

With the ECB's new 'lower for longer' QE policy has achieved to put monetary policy divergence back on the agenda.

The ECB's 'dovish' decision yesterday to pare bond purchases is in stark contrast with market speculation that the Fed will be leading the pack when it comes to hiking rates, no matter who comes out on top in the race to lead the Fed from February onwards.

European bond prices have remained better bid as the ECB decided to reduce bond purchases to €30B a month in 2018 and cushion the blow by continuing to reinvest proceeds from maturing securities. In his press conference yesterday, Draghi strengthened his 'dovishness' by stressing the need for caution as the ECB moves toward the stimulus exit.

With the ECB taking the 'lower-for-longer' route, U.S debt product is facing the prospects that even a Janet Yellen led Fed might pursue a pace of higher rates.

Overnight, the yield on U.S 10-year Treasuries decreased -1 bps to +2.45%. In Germany, 10-year Bund yields fell -1 bps to +0.41%, the lowest in more than a week. In The U.K, the 10-year Gilt yield increased +2 bps to +1.384%.

4. Dollar's rate divergence rally

Rate divergence remains the incentive to owning particular FX currency pairs.

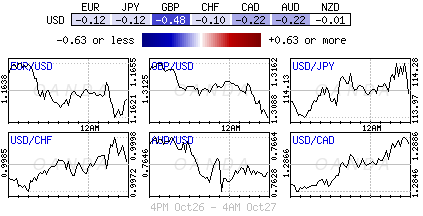

In the aftermath of the ECB rate decision yesterday and the lack of a signal on any potential first rate hike any time soon by Draghi and company has sent the euro's 'single unit' (€1.1634) to test its three-month low outright.

Elsewhere, USD/CHF ($0.9993) managed to trade above parity for first time in four-months.

Dow-under, AUD/USD (A$0.7647) is a tad softer on political uncertainty after a High Court ruling erased PM Turnball's one seat majority in Parliament. The Court ruling has disqualified Deputy PM Barnaby Joyce from sitting in parliament on account of his dual citizenship (Australia and New Zealand) at the time of last year's Federal election. Joyce is expected to re-contest his seat in a special by-election.

5. French consumer confidence continues to fall

Data this morning from statistics agency Insee shows that French consumer confidence continued to decline this month.

Consumer confidence in the eurozone's second-largest economy fell slightly to 100 from 101 in September. Market expectations were looking for consumer confidence to remain stable in October.

Note: The reading jumped +6 points in June after Emmanuel Macron won the French presidential election and a majority in the national assembly.

However, consumer confidence dropped to 104 in July from 108 in June as households lost confidence in their finances and as Macron's oen popularity declined.

Market Update – European Session: Awaiting US GDP Data To Gauge Impact From Recent Hurricanes

Notes/Observations

Focus on US Q3 GDP data and gauge impact of the hurricanes in August and September

Overnight

Asia:

Japan Sept National CPI Ex Fresh Food Y/Y: 0.7% v 0.7%e; CPI Ex-Fresh Food (Core) Y/Y: 0.7% v 0.7%e

Australia’s High Court disqualified Dep PM (and Lower House MP) Barnaby Joyce from sitting in parliament on account of his dual citizenship (Australia and New Zealand) at the time of last year’s Federal election. Govt lost its majority as a resul. (**Insight: Court action erased PM Turnball’s one seat majority in the lower house. Joyce to re-contest his seat in a special election)

Europe:

ECB reportedly considering option to end QE with a short tapering period during 2018. Implicitly assumed the new extended asset purchase program to be tapered to a halt by the end of next year as long as inflation outlook improved

Catalan President Puigdemont considered calling for snap election, but has ruled it out citing that central govt did not offer assurances that it would not take control of the region if early elections were called

Italy PM Gentiloni nominates Gov Visco for a second term at Bank of Italy (BOI) (as expected)

High court rejected review of Tory Party's earlier £1B deal with Northern Ireland's DUP to shore up its minority govt

Americas:

House voted to pass Senate budget proposal that paves way for tax reform bill by 216-212 vote. Senate budget resolution gave congressional GOP the ability to avoid a Democratic filibuster so that it could pass the Senate with 50 votes.

Fed Chairman position contender John Taylor: Lower US growth due to economic policy

Economic Data

(DE) Germany Sept Import Price Index M/M: 0.9% v 0.5%e; Y/Y: 3.0% v 2.6%e

(FI) Finland Oct Consumer Confidence: 23.1 v 23.7 prior; Business Confidence: 12 v 10 prior

(FR) France Oct Consumer Confidence: 100 v 101e

(ES) Spain Sept Adjusted Retail Sales Y/Y: 2.1% v 1.9%e; Retail Sales (unadj) Y/Y: 2.2% v 1.6%e

(SE) Sweden Oct Consumer Confidence: 105.3 v 102.0e; Manufacturing Confidence: 121.1 v 120.0e; Economic Tendency Survey: 113.3 v 112.0e

Fixed Income Issuance:

(IN) India sold total INR150B vs. INR150B indicated in 2022, 2031, 2033 and 2055 bonds

(IT) Italy Debt Agency (Tesoro) sold €6.0B vs. €6.0B indicated in 6-month Bills; Avg Yield: -0.382% prior; Bid-to-cover: 1.99x v 2.07x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.5% at 393.3, FTSE +0.3% at 5504, DAX +0.7% at 13229, CAC-40 +0.9% at 5502, IBEX-35 -0.5% at 10293, FTSE MIB -0.1% at 22782, SMI +0.3% at 9225, S&P 500 Futures +0.2%)

Market Focal Points/Key Themes:

European Indices trade mostly higher across the board with notable outperform in the Dax and CAC which trades at all time highs, while the Spanish IBEX trades lower.

Markets have been on the front foot following strong results from Amazon, Alphabet and Microsoft overnight, while in Europe solid results from Volkswagen, Total, and Electrolux helped lift indices, while IAG trades lower following their results, and muted passenger growth figures. In Switzerland Clariant trades sharply lower after terminating their merger agreement with Huntsman; Kuka and SES also notbaly lower following results.

Looking ahead notable earners include Chevron, Aon and Colgate.

Equities

Consumer discretionary [IAG [IAG.UK] -4% (Earnings)]

Materials: [Clariant [CLN.CH] -5.5% (Terminates merger with Huntsman),

Industrials: [Safran [SAF.UK] +1.4% (Earnings), Electrolux [ELUXB.SE] +3.1% (Earnings), Volkswagen [VOW3.DE] +1.9% (Earnings)]

Financials: [UBS [UBSG.CH] +1.7% (Earnings), RBS [RBS>UK] +2.3% (Earnings)]

Energy: [Total [FP.FR] +1.2% (earnings), Linde [LIN.DE] +2.9% (Earnings)]

Speakers

ECB's Vasiliauskas (Lithuania): smaller QE as continued boost to economy

ECB’s Praet (Belgium, chief economist): Political accepted fiscal capacity in region will be modest in size. Central budget could help monetary policy, especially during deep recessions when nominal interest rates might reach their effective lower bound

ECB's Villeroy (France): Have taken the essential steps towards ending the bond buying program (QE). Should use all tools in the progressive normalization

ECB's Costa (Portugal): Essential that banking union is completed

ECB Survey of Professional Forecasters (SPF) kept its inflation outlook unchanged for the forecast horizon (2017-19). Raised euro zone long term inflation expectations (2021) from 1.8% to 1.9%. The survey raised its growth outlook with 2017 GDP growth forecast from 1.9% to 2.2%; 2018 GDP growth from 1.8% to 1.9% and 2019 GDP growth from 1.6% to 1.7%

Spain PM Rajoy: Confronting an exceptional situation, with grave consequences for many people; illegal actions hurt economy

Greece govt official: Creditors to return to Athens at end of November

Turkey Econ Min Zeybekci: Current level of exchange rate is not reflecting reality

South Africa Fin Min Gigaba: To unveil stimulus package that focusing on tourism and manufacturing

Currencies

Rate divergence remained the catalyst for FX pairs.

The aftermath of the ECB rate decision and lack of signal on any potential 1st rate hike has sent the EUR/USD to a 3-month low. Draghi noted that interest rates won't rise shortly QE bond buying ended. Pair under 1.1640 just ahead of the NY morning.

USD/CHF pair tested above parity for 1st time since May 15th

AUD/USD was softer on political uncertainty after a High Court ruling erased PM Turnball’s one seat majority in Parliament. AUD/USD off by 0.2% to trade at 0.7650 area

Fixed Income

Bund futures trade at 162.14 up 46 ticks as dovish repricing continues in European rates as markets adjusts to a lower for longer outlook from the ECB. Support lies at 161.00, followed by 160.38. Resistance stands initially at 162.75, followed by 163.51.

Gilt futures trade at 124.09 up 26 ticks, after initially opening a little lower after a block seller of 10-year Treasuries late on Thursday knocked both US and German 10y contracts lower ahead of the futures close. Continued downside eyeing 123.26. Upside targets 124.90 then 125.24.

Friday’s liquidity report showed Thursday’s excess liquidity fell to €1.810T from €1.825T and use of the marginal lending facility rose to €253M from €133M

Corporate issuance saw $7.6B come to market via 6 issuers. For the week ending Oct 25th Lipper fund flows reported IG fund net inflows of $4.7B and High yield funds reported net inflows of $122.5M.

Looking Ahead

05:30 (ZA) South Africa to sell combined ZAR800M in I/L 2025, 2029 and 2046 bonds

06:00 (IE) Ireland Sept Retail Sales M/M: No est v -4.2% prior; Y/Y: No est v 4.7% prior

06:00 (UK) DMO to sell combined £4.5B in 1-month, 3-month and 6-month Bills (£0.5B, £2.0B and £2.0B respectively)

06:30 (RU) Russia Central Bank (CBR) Interest Rate Decision: Expected to cut 1-Week Auction Rate by 25bps to 8.25%

06:45 (EU) ECB's Angeloni (SSM board member)in Frankfurt

06:45 (US) Daily Libor Fixing

07:00 (DE) ECB’s Weidmann (Germany) in Paris

07:30 (IN) India Weekly Forex Reserves

08:00 (ES) Spain Debt Agency (Tesoro) announces upcoming issuance

08:00 (IN) India announces upcoming Bill auction (held on Wed)

08:00 (RU) Russia Central Bank (CBR) Gov Nabiullina to hold post rate press conference

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Q3 Advance GDP Annualized Q/Q: 2.6%e v 3.1% prior; Personal Consumption: 2.1%e v 3.3% prior

08:30 (US) Q3 Advance GDP Price Index: 1.7%e v 1.0% prior; CORE PCE Q/Q: 1.3%e v 0.9% prior

08:30 (BR) Brazil Sept Total Outstanding Loans (BRL): No est v 3.047T prior; M/M: No est v -0.1% prior

10:00 (US) Oct Final University of Michigan Confidence: 100.7e v 101.1 prelim

11:00 (EU) Potential sovereign rating after European close

(FI) Finland Sovereign Debt to be rated by Moody's

(DE) Germany Sovereign Debt to be rated by S&P

(NL) Netherlands Sovereign Debt to be rated by Fitch

(NL) Netherlands Sovereign Debt to be rated by Moody's

(UR) Ukraine Sovereign Debt to be rated by Fitch

(UK) United Kingdom Sovereign Debt to be rated by Fitch

(UK) United Kingdom Sovereign Debt to be rated by S&P

13:00 (US) Weekly Baker Hughes Rig Count data

15:00 (CO) Colombia Central Bank Interest Rate Decision: Expected to leave Overnight Lending Rate unchanged at 5.25%

CAC Leaps As ECB Tightens Its Belt

The CAC index has posted strong gains in the Friday session, continuing the upward movement seen on Thursday. Currently, the CAC is trading at 5,498.50, up 0.79% on the day. On the release front, there are no eurozone or French events on the schedule. The US will release Advance GDP, with an estimate of 2.5%.

The ECB decision to implement quantitative tightening has buoyed European stock markets. The CAC has jumped on the bandwagon and has jumped 2.4% this week. Investors gave a thumbs-up as the ECB cut the asset purchase program (QE) from EUR 60 billion to 30 billion/mth. The QE program, which was due to terminate in December, has been extended to September 2018. ECB President Mario Draghi did surprise the markets, however, with dovish comments. Draghi said that the program would remain open-ended, which allows the ECB to extend QE beyond September 2018. As expected, the ECB maintained interest rates at a flat 0.00%, and Draghi provided no hints about the timing of future rate hikes. The ECB appears in no rush to tinker with rate policy, and we’re unlikely to see any rate increases until QE is completed.

Investors are casting a nervous eye on Spain, as the Catalan crisis has reached a fever pitch. Spain’s Senate will convene later on Friday and is expected to authorize the central government to invoke Article 155 of Spain’s constitution and apply direct rule over Catalonia. What steps will Madrid take? It could dismiss the Catalan government and parliament and take control of the regional police and radio and television stations. This drastic clause has never been invoked, and it remains unclear what lies ahead. How will the Catalan parliament respond? On Thursday, the Catalan vice-president warned that if Madrid imposed direct rule, the Catalan government would have no choice but to declare independence. So far, the crisis has not affected the euro, and Caixabank, the third largest bank in the country, does not expect the Catalonia issue to affect Spain’s GDP, which the bank projects will expand 2.7 percent in 2018. Still, if the crisis worsens and Catalans respond with civil disobedience, investors could get nervous and stocks could drop.

DAX Jumps As ECB Chops Stimulus Program

The DAX has hit record highs on Friday, buoyed by the ECB decision to taper its bond-buying program but also extend the scheme to September 2018. Currently, the DAX is at 13,242.00, up 0.81%. On the release front, the sole eurozone event is German Import Prices, which posted a gain of 0.9%. This beat the estimate of 0.5%, and marked the first gain since February. The US will release Advance GDP, which is expected to gain 2.5%.

It was Black Thursday for the euro, but European stock markets were up sharply, and the gains have continued on Friday. The DAX responded to the ECB decision to taper its quantitative easing program with strong gains of 1.4% on Thursday. As expected, the ECB finally pressed the trigger and chopped QE from EUR 60 billion to 30 billion/mth. The ECB extended the program, which was due to terminate in December, to September 2018. However, many investors were hoping that the ECB would not only taper the bond-buying scheme, but would also announce a date when the program would end. ECB President Mario Draghi has given himself plenty of wiggle room, as he can simply extend QE beyond next September. The ECB maintained interest rates at a flat 0.00%, and Draghi provided no hints about the timing of future rate hikes. The ECB appears in no rush to tinker with rate policy, and we’re unlikely to see any rate increases until QE is completed.

Earlier this week, German Ifo Business Climate jumped to 116.7, an all-time high. The business sector is very optimistic about the robust economy, and appears unfazed by German coalition talks and the deadlock in the Brexit talks. The strong reading suggests that the German economy will enjoy a strong fourth quarter. German policymakers insist that the ECB’s interest rate policy is too loose for Germany, but the economy is still expected to thrive. Earlier in the week, German Manufacturing PMI posted a strong reading of 60.5 points, beating expectations. The manufacturing sector continues to expand, buoyed by strong domestic demand and the global appetite for German exports.

Euro Plunges on Draghi Stimulus Remarks

The euro remains under pressure in the Friday session, after dropping sharply on Thursday. Currently, EUR/USD is trading at 1.1628, down 0.19% on the day. On the release front, the sole eurozone event is German Import Prices, which posted a gain of 0.9%. This beat the estimate of 0.5%, and marked the first gain since February. The US will release Advance GDP, which is expected to gain 2.5%. The other major indicator is UoM Consumer Sentiment, with the indicator forecast to jump to 100.7 points.

EUR/USD suffered its largest daily loss of the year after ECB head Mario Draghi said that the Bank’s bond-buying program (QE) would remain open-ended. As expected, the ECB finally pressed the trigger and chopped QE from EUR 60 billion to 30 billion/mth. The ECB extended the program, which was due to terminate in December, to September 2018. However, many investors were hoping that the ECB would not only taper the bond-buying scheme, but would also announce a date when the program would end. ECB President Mario Draghi has given himself plenty of wiggle room, as he can simply extend QE beyond next September. The ECB maintained interest rates at a flat 0.00%, and Draghi provided no hints about the timing of future rate hikes. The ECB appears in no rush to tinker with rate policy, and we’re unlikely to see any rate increases until QE is completed. The euro responded with losses of 1.4%, and is currently trading at its lowest level since late July.

It’s crunch day in Spain, as the Senate will convene later on Friday and is expected to authorize the central government to invoke Article 155 of Spain’s constitution and apply direct rule over Catalonia. What steps will Madrid take? It could dismiss the Catalan government and parliament and take control of the regional police and radio and television stations. This drastic clause has never been invoked, and it remains unclear what lies ahead. How will the Catalan parliament respond? On Thursday, the Catalan vice-president warned that if Madrid imposed direct rule, the Catalan government would have no choice but to declare independence. So far, the crisis has not affected the euro, and Caixabank, the third largest bank in the country, does not expect the Catalonia issue to affect Spain’s GDP, which the bank projects will expand 2.7 percent in 2018. Still, the crisis worsens and Catalans respond with civil disobedience, investors could get nervous and dump their euros for safe-haven assets.

Technical Outlook: AUDUSD Extends Steep Descend To New Multi-Month High

The Aussie dollar continues to trend lower and hit fresh low at 0.7625 on Friday (the lowest since 11 July).

Steep downtrend extends into sixth straight day and cracked important support at 0.7632 (Fibo 61.8% of 0.7328/0.8124, 09 May / 08 Sep ascend) close below which would generate fresh bearish signal for extension of the downleg from 0.7883 (19 Oct lower top) towards 0.7530 (top of weekly cloud / weekly 100SMA). Weekly cloud is twisting next month and attracts for further weakness.

The pair is also on track for strong bearish weekly close (the biggest one-week loss since mid-November 2016) which also weighs on the price.

Meanwhile, bears may take a breather as slow stochastic is deeply oversold on daily chart and RSI is penetrating oversold territory, indicating correction but without clearer signal so far.

Also, traders are likely to book their profits on this week’s sharp fall.

However, firm bearish structure keeps the downside under pressure, suggesting limited correction.

Broken 200SMA offers initial resistance at 0.7693, with former low of 06 Oct at 0.7732 (also Fibo 38.2% of 0.7883/0.7625 descend) expected to ideally cap.

US GDP data today are closely watched for fresh signals.

Res: 0.7664, 0.7693, 0.7732, 0.7782

Sup: 0.7630, 0.7571, 0.7530, 0.7500

USD/JPY Month End Flow Might Decide Today’s Price Direction

The USD/JPY is in uptrend. The Yen weakness that we could see on real time trading webinars and analyses was following both the USD and GBP strength. Today is Friday and end of month so in my opinion, we should see a profit taking. Managers of passive portfolios usually sell the extra" dollars and buy other currencies to bring the overall fund back into balance. These flows can be very heavy at the end of the month so pay attention to it.

The POC zone is the crossroads for the USD/JPY. 113.80-113.95 (50.0, trend line, D L3, EMA 89, atr pivot). If it rejects from the POC to the upside targets are - near term inverted SHS top - 114.24, 114.40 and 114.60. However the break below 113.80 and the pair could target 113.58 and 113.24. The important thing is to watch these important levels (see the chart) and act accordingly. Month end profit taking usually ends up in 2-way trading direction.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

CRUDE OIL Pushing Towards Key Resistance

Crude oil is consolidating within range defined by support at 50.43 and the strong resistance lies at 52.86 (28/09/2017). Expected to show continued increase within this range.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).