Sample Category Title

Forex: US Inflation Disappoints

On Friday, US Consumer Price Index data was released and failed to impress the markets. With US gasoline prices spiking, following the disruption caused by the recent Hurricanes, consumer prices rose the most in eight months to 1.6% in September – coming up short of the forecast of 1.7%. Additionally, annualized inflation missed its forecast of 2.3%, coming in at 2.2%. To add to the Fed’s woes was the release of average weekly earnings easing to 0.6% from 1.0% on a yearly basis. The markets’ disappointment resulted in a broad sell-off of USD following the release, although USD has retraced over the weekend.

Fed Chair Janet Yellen commented on Sunday that the US economy remains strong and the continued strength of the labor market calls for a gradual increase in interest rates, despite subdued inflation. At an international banking seminar in Washington DC Yellen said, “We will be paying close attention to the inflation data in the months ahead”, “My best guess is that these soft readings will not persist” & “We continue to expect that the ongoing strength of the recovery will warrant gradual increases in that rate to sustain a healthy labor market and stabilize inflation around our 2 percent longer-run objective”.

The Austrian election appears to highlight another country focusing on Nationalistic policies. The conservative People’s Party, led by Sebastian Kurz, appear to be on track to win the election with 31.6% of the vote. Kurz’s campaign focused on stronger border controls, reducing the number of immigrants and cutting benefits for newcomers. The obvious concern is for another country to go against its Euro members stance on immigration and what that could mean for Austria and the greater Eurozone.

Politics remain in focus, as Catalan leader Carles Puigdemont has until 09:00 BST to clarify as to whether he is calling for Catalan’s independence from Spain. Spanish Prime Minister Rajoy gave Puigdemont until Monday to declare his intentions and until Thursday if he changes his decision. Rajoy has made it clear that a call for Catalan independence will result in that region’s suspension from the Spanish parliament.

EURUSD is little changed from Friday’s close, currently trading around 1.1810.

USDJPY is 0.15% higher to currently trade around 111.95.

GBPUSD is little changed in early Monday trading. Currently, GBPUSD is trading around 1.3295.

Gold is 0.16% lower to currently trade around $1,302.50.

WTI is nearly 1% higher in early Monday trading. Currently, WTI is trading around $52.15.

Major data releases for today:

09:00 BST is the deadline for the Catalan Prime Minister to confirm his region’s intention to declare independence. Any answer other than a “No” will result in the dismantling of the Catalan Government, leading to civil unrest and the likelihood of a sell-off in EUR.

At 10:00 BST, Eurostat will release Eurozone Trade Balance for August.

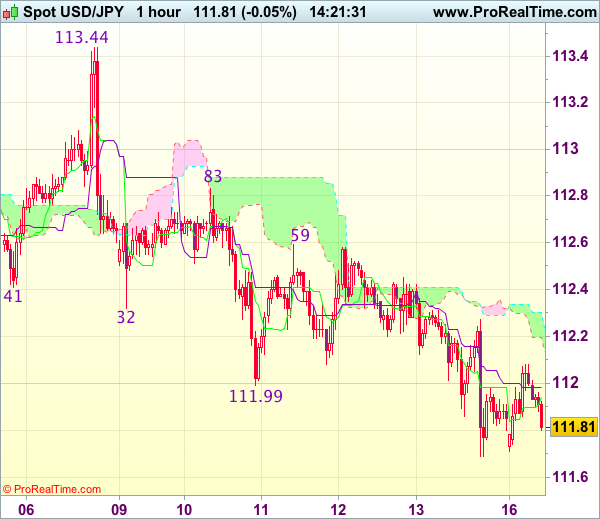

Trade Idea : USD/JPY – Hold short entered at 112.25

USD/JPY - 111.80

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.94

Kijun-Sen level : 111.98

Ichimoku cloud top : 112.30

Ichimoku cloud bottom : 112.20

Original strategy :

Sold at 112.25, Target: 111.25, Stop: 112.25

Position : - Short at 112.25

Target : - 111.25

Stop : - 112.25

New strategy :

Hold short entered at 112.25, Target: 111.25, Stop: 112.25

Position : - Short at 112.25

Target : - 111.25

Stop : - 112.25

As dollar has remained under pressure after breaking below last week’s low at 111.99, adding credence to our bearishness and signaling the fall from 113.44 top is still in progress, hence downside bias remains for this move to extend weakness to 111.70 (100% projection of 113.44-112.32 measuring from 112.83), below there would bring subsequent decline to 111.47 support but oversold condition would limit downside and reckon 111.11 support would remain intact.

In view of this, we are holding on to our short position entered at 112.25. Only above resistance at 112.59 would abort and signal low is formed instead, risk a stronger rebound to indicated resistance level at 112.83.

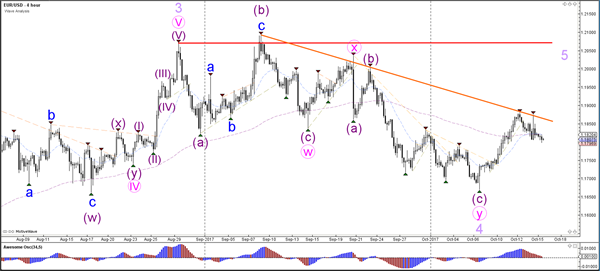

Daily Wave Analysis: EUR/USD Testing Wave 4 Fibonacci Support At 1.18

Currency pair EUR/USD

The EUR/USD is challenging a resistance trend line (orange). A bullish breakout could see price challenge the larger resistance (red) but it remains unclear whether price is in a wave 5 or in an expanded wave 4 at the moment. The 1-hour chart however could provide more guidance about that aspect.

The EUR/USD has retraced back to the 50% Fibonacci level of wave 4 (pink). Price could be ready for a bullish continuation as long as price stays above the 61.8% Fibonacci level. A continuation of the wave 5 would indicate a long-term bullish signal as it completes 5 waves within a larger potential wave 1. A break below 1.18 however could indicate that the wave 4 (purple) is still intact and price could bounce again at the previous bottom around 1.17.

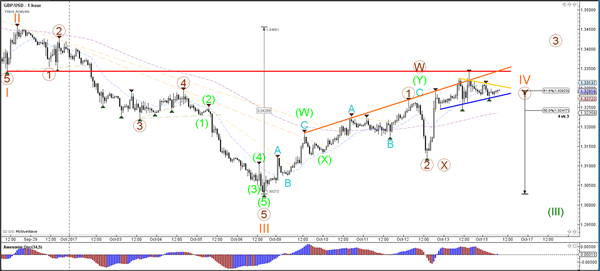

Currency pair GBP/USD

The GBP/USD offers two main scenarios where either a bearish ABC (green) or a wave 123 (green) is taking place. Price invalidates that wave 4 (orange) correction if price breaks above the bottom of wave 1 (red line).

The GBP/USD is building a triangle pattern (orange/blue lines). A bearish break could confirm the completion of wave 4 (orange) whereas a bullish break could invalidate it.

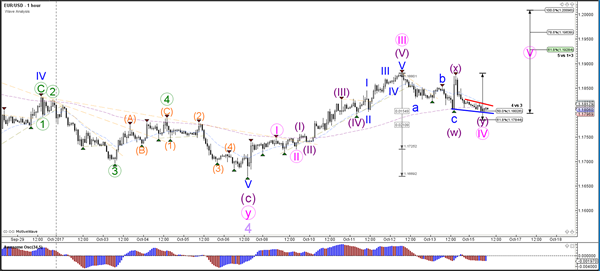

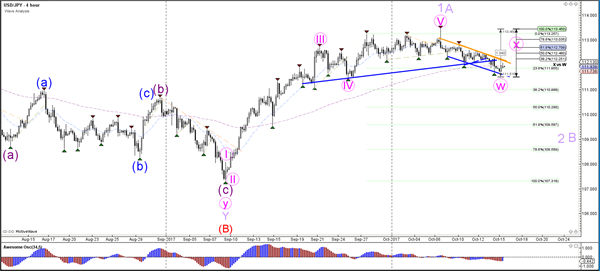

Currency pair USD/JPY

The USD/JPY could be building a larger WXY (pink) correction within wave 2 or B (purple).

The USD/JPY is in a bearish channel (orange/blue lines) which could be part of a bearish wave Y (purple). A break above the channel could indicate a potential retracement within wave X (pink).

Market Update – Asian Session: Yellen And Rosengren Comment On Rates And Policy

Asia Summary

Asian equity markets opened generally higher. After hitting multi-year highs on Friday’s session, the Nikkei 225 has continued to gain on today’s session. Japanese technology names, including Toshiba, Hitachi and Softbank have all traded higher following today’s weakness in the yen, Friday’s gain seen on the Nasdaq and the recent earnings guidance out of HP Inc.

Australia’s ASX 200 has gained over 0.5%. Various names including, OZ Minerals, have started to release their Q3 production updates. On tomorrow’s session, iron-ore giant Rio Tinto is expected to release its production report and its shares have gained over 3% on today’s session. On the macro front, the Reserve Bank of Australia (RBA) Oct meeting minutes are due to be released on Oct 17th, while the September employment change figures are due on Oct 19th.

The South Korean Won has gained for the 6th straight day, even as its navy confirmed the start of joint military drills with the US. In Taiwan, solar names have traded broadly higher following a report that the government is planning to fund a new solar company.

In New Zealand, the government formation talks continue to drag on. Earlier today, the head of the ruling National Party English said the government formation process could take until the end of the week, as the First Party continues to decide on a coalition partner. Later this week, New Zealand’s Q3 CPI data is due to be released on Oct 17th.

The Hang Seng has hit highs not seen since Dec 2007 amid over 4% gains in shares of Hong Kong Exchange [0388.HK]. Cheung Kong Property Holdings [1113.HK] has gained over 2%, as there has been press speculation that the company will sell most of its stake in The Center office tower in Hong Kong for a record HK$40.2B. Great Wall Motor [2333.HK] had earlier traded higher by over 9%, but shares have since pared gains. Last week, the company’s shares rose over 12% amid speculation related to a partnership with BMW.

In China, the ChiNext small-cap index has declined and underperformed the broader market. At the same time, the country’s 10-year sovereign bond yield has traded at over 2 year highs.

China’s Sept banking data released over the weekend (M2, M1, New Yuan Loans and Aggregate Financing) all beat market expectations. The inflation data released earlier today was mixed, as CPI was inline while PPI rose more than expected. Looking ahead, China’s twice per decade Communist Party Congress is due to begin on Oct 18th, while Q3 GDP is expected to be released on Thursday, Oct 19th. Ahead of the data, PBoC Gov Zhou was quoted as saying that H2 GDP growth was seen at 7%, which would be ahead of the 6.9% readings seen in each Q1 and Q2.

Separately, Zhou said total debt leverage in China is too high. The latter comments by the Chinese central banker were made at the Group of 30 seminar in Washington D.C. Other central bankers that made comments at this event over the weekend included, Fed Chair Yellen. ECB’s Draghi also made comments on Saturday on the sidelines of the IMF and World Bank meetings, which also occurred in the US capital.

Brent Crude futures are higher by over 1%, amid reports that Iraqi forces have advanced towards Kurdish-held Kirkuk. Recall in late Sept, the Kurdish region held a referendum and there was said to be 90% support for independence.

Meanwhile in Catalonia, today is the deadline imposed by Spain’s central government for the leaders of the region to clarify their independence stance. According to a prior press report, if Catalan President Puigdemont confirmed by today that he has declared independence, he will be given a further 3 days to withdraw the declaration.

Key economic data

(CN) CHINA SEPT NEW YUAN LOANS (CNY): 1.27T V 1.23TE

(CN) CHINA SEPT AGGREGATE FINANCING (CNY): 1.82T V 1.57TE

(CN) CHINA SEPT M2 MONEY SUPPLY Y/Y: 9.2% V 8.9%E; M1 MONEY SUPPLY Y/Y: 14.0% V 13.5%E

(UK) Oct Rightmove House Prices m/m: 1.1% v -1.2% prior; y/y: 1.4% v 1.1% prior

(CN) CHINA SEPT CPI M/M: 0.5% V 0.3%E; Y/Y: 1.6% V 1.6%E; PPI Y/Y: 6.9% V 6.4%E

Speakers and Press

Japan

(JP) BoJ Gov Kuroda: Real interest rates expected to fall further as inflation expectations rise, further enhancing effects of BoJ’s monetary easing

Korea

(KR) South Korea Fin Min Kim: the worst would be soon over with China after the Communist Party Congress in Beijing - financial press

China

(CN) PBOC Gov Zhou: Total debt leverage in China is too high, there is no clear fiscal discipline to constrain local govts

(CN) China Q3 GDP may have grown ~6.8% y/y; Q4 GDP may grow 6.7% and 6.8% in 2017 - Chinese Press

(CN) PBOC Gov Zhou: Sees H2 GDP to reach 7%

Australia/New Zealand

(NZ) New Zealand National Party (ruling) leader English said outstanding issues remain and further talks are needed before government can be formed; government formation could take until end of week – NZ Press

Europe

(UK) UK PM May’s Office confirms she will meet with EU officials Barnier and Juncker

(EU) ECB Constancio says reinvestment policy will continue until further notice

(EU) Some ECB members said to identify €2.5T limit for QE - US financial press

(EU) On Saturday, ECB President Draghi reiterated have to be persistent with our monetary policy

US

(US) Fed Chair Yellen: New normal will be lower interest rates than we've seen historically; biggest surprise in the US economy this year has been inflation

(US) Fed's Rosengren (moderate, non-voter): 3-4 rate hikes next year will probably be appropriate; may need to overshoot on rates if unemployment is below 4% while inflation reaches target

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.7%, Hang Seng +0.9%; Shanghai Composite -0.1%; ASX200 +0.7%, Kospi +0.1%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.2%, Dax +0.1%; FTSE100 +0.1%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.1823-1.1798; JPY 112.08-111.74; AUD 0.7889-0.7868;NZD 0.7183-0.7166

Dec Gold +0.0% at $1,304/oz; Nov Crude Oil +0.9% at $51.89/brl; Dec Copper +0.6% at $3.15/lb

(CN) China PBOC injects CNY20B in 7-day reverse repos v skipped prior; injection matches maturities

USD/CNY (CN) PBOC SETS YUAN REFERENCE RATE AT 6.5839 V 6.5866 PRIOR

(CN) PBOC has completed trial runs on the algorithms needed for digital currency supply, taking it a step closer to addressing the technological challenges associated with digital currencies - Chinese press

(KR) Bank of Korea (BOK) sells KRW950B in 1-yr bonds at 1.61%

Equities notable movers

Australia/New Zealand

NEU.AU Confirms Phase 3 plan for Rett syndrome at FDA Meeting; +17.5%

TGA.AU Cuts FY17 Net A$17-20M (prior A$24-26M); Guides H1 Net A$11M; -22%

Korea

000080.KR Operations at four of the six factories halted on Friday, as union decided to stage a strike after failure of negotiations on wage increases – filing; -8%, 6-yr low

006400.KR Said to be selling retirement pension to Samsung Fire & Marine Insurance without going through without competitive bidding – press; -5%

China/Hong Kong

2333.HK Unusual share price movement and trading volume movement: cooperation for vehicles of MINI brand is still at preliminary stage (Friday headline), +10% daily limit for premarket

US

TSLA Said to have fired ~400 employees in the past week as part of its company wide annual review - financial press

Aussie Dollar Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.84% against the USD and closed at 0.7889 on Friday.

LME Copper prices rose 0.7% or $45.0/MT to $6858.0/MT. Aluminium prices rose 1.1% or $22.5/MT to $2140.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7876, with the AUD trading 0.16% lower against the USD from Friday's close.

Earlier today, in China, Australia's largest trading partner, the consumer price index (CPI) registered a rise of 1.6% on a yearly basis in September, at par with market expectations. The CPI had risen 1.8% in the previous month. Moreover, the nation's producer price index (PPI) grew 6.9% YoY in September, surging to a six-month high and surpassing market expectations for an advance of 6.4%. The PPI had risen 6.3% in the previous month.

The pair is expected to find support at 0.7835, and a fall through could take it to the next support level of 0.7794. The pair is expected to find its first resistance at 0.7907, and a rise through could take it to the next resistance level of 0.7938.

Looking forward, market participants would closely monitor the Reserve Bank of Australia's October meeting minutes, due to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Germany’s Annual Inflation Confirmed At 1.8% In September

For the 24 hours to 23:00 GMT, the EUR marginally declined against the USD and closed at 1.1821 on Friday.

In economic news, Germany's final consumer price index (CPI) rose 1.8% YoY in September, confirming the preliminary print and following a similar rise in the prior month.

The greenback declined against its major counterparts on Friday, on the heels of weaker-than-expected US inflation report.

Data showed that consumer price inflation in the US climbed less-than-anticipated by 0.5% on a monthly basis in September, while market participants had expected for a rise of 0.6%. Nevertheless, it was the biggest increase in eight months, amid a rise in gasoline prices following Hurricane Harvey. The CPI had recorded a rise of 0.4% in the previous month. Moreover, the nation's advance retail sales rebounded 1.6% in September, rising by the most in nearly three years, driven by strong auto and auto parts sales. However, investors had envisaged advance retail sales to rise by 1.7%, after registering a revised drop of 0.1% in the prior month.

Other economic data indicated that the US flash Reuters/Michigan consumer sentiment index unexpectedly climbed to a thirteen-year high level of 101.1 in October, defying market expectations for a drop to a level of 95.0, offering signs that Americans turned upbeat about the nation's growth prospects. In the prior month, the index had registered a level of 95.1.

Over the weekend, the Federal Reserve (Fed) Chair, Janet Yellen, stated that the central bank expects to continue raising interest rates gradually as ongoing strength of the US economy and tightening labour market will eventually boost inflation. Further, Yellen acknowledged that the persistence of undesirably low inflation this year has been a surprise and that the central bank will be paying close attention to the inflation data in the months ahead. Yellen also reiterated that the impact of recent hurricanes on the economy would be temporary.

In the Asian session, at GMT0300, the pair is trading at 1.1807, with the EUR trading 0.12% lower against the USD from Friday's close.

The pair is expected to find support at 1.1778, and a fall through could take it to the next support level of 1.1750. The pair is expected to find its first resistance at 1.1855, and a rise through could take it to the next resistance level of 1.1904.

Going ahead, investors will focus on the Euro-zone's trade balance for August, slated to release in a few hours. Moreover, the US New York Empire State manufacturing index for October, due to release later today, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Pound Trading Marginally Lower This Morning

For the 24 hours to 23:00 GMT, the GBP rose 0.23% against the USD and closed at 1.3292 on Friday, on expectations that the UK could be offered a two-year Brexit transition deal.

In the Asian session, at GMT0300, the pair is trading at 1.3291, with the GBP trading a tad lower against the USD from Friday’s close.

Overnight data showed that UK’s Rightmove house price index rebounded 1.1% MoM in October. The price index had fallen 1.2% in the previous month.

The pair is expected to find support at 1.3247, and a fall through could take it to the next support level of 1.3202. The pair is expected to find its first resistance at 1.3337, and a rise through could take it to the next resistance level of 1.3382.

With no macroeconomic releases in the UK today, investor sentiment would be governed by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Yen Trading On A Weaker Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.35% against the JPY and closed at 111.88 on Friday.

In the Asian session, at GMT0300, the pair is trading at 112, with the USD trading 0.11% higher against the JPY from Friday’s close.

Early morning data indicated that Japan’s final industrial production rebounded less than initially estimated by 2.0% on a monthly basis in August, while the preliminary figures had recorded a rise of 2.1%. Industrial production had dropped 0.8% in the prior month.

The pair is expected to find support at 111.7, and a fall through could take it to the next support level of 111.41. The pair is expected to find its first resistance at 112.28, and a rise through could take it to the next resistance level of 112.57.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Swiss Franc Reverses Its Gains This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.11% against the CHF and closed at 0.9743 on Friday.

On the data front, Switzerland’s producer and import price index recorded a rise of 0.5% on a monthly basis in September, more than market consensus for a gain of 0.3%. In the prior month, the index had registered a rise of 0.3%.

In the Asian session, at GMT0300, the pair is trading at 0.9757, with the USD trading 0.14% higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9717, and a fall through could take it to the next support level of 0.9678. The pair is expected to find its first resistance at 0.9784, and a rise through could take it to the next resistance level of 0.9812.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading A Tad Lower This Morning

For the 24 hours to 23:00 GMT, the USD slightly rose against the CAD and closed at 1.2479 on Friday.

In the Asian session, at GMT0300, the pair is trading at 1.2484, with the USD trading marginally higher against the CAD from Friday’s close.

The pair is expected to find support at 1.2451, and a fall through could take it to the next support level of 1.2419. The pair is expected to find its first resistance at 1.2518, and a rise through could take it to the next resistance level of 1.2553.

Moving ahead, the Bank of Canada’s (BoC) business outlook survey report for the third quarter, scheduled to release later in the day, will be on investors’ radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.