Sample Category Title

Eurozone Trade Headlines Light Release Schedule On Monday

The global financial markets will be off to a slow start on Monday amid a dearth of economic data from around the world. A headline Eurozone trade report and US manufacturing survey will make headlines on this otherwise non-eventful day.

Eurostat, the European Commission's statistical agency, will release the August trade balance at 09:00 GMT. The seasonally adjusted and non-seasonally adjusted figures will be published.

In terms of geopolitics, Catalonia's president faces a critical decision that could determine the outcome of the region's secessionist movement. The Spanish government has given Carles Puigdemont until Monday to clarify whether he has declared independence following the Catalan referendum.

Shifting gears to North America, the New York Federal Reserve Bank will release the Empire State manufacturing index at 12:30 GMT. The monthly report provides a snapshot of business conditions for regional manufacturers.

North of the border, the Bank of Canada (BOC) will issue its Business Outlook Survey at 14:30 GMT. The report provides an overview of business conditions in the Canadian economy. Monday's report could shed light on how domestic businesses are coping with multiple interest rate hikes.

Earlier in the day, China's National Statistics Bureau said consumer inflation rose as expected in September, while producer prices shot up more than forecast.

China's consumer price index (CPI) accelerated 1.6% in the 12 months through September, following a 1.8% increase the previous month. Meanwhile, the producer price index (PPI) rose 6.9% year-over-year, much higher than August's 6.3% and forecasts calling for the same.

EUR/USD

The euro opened slightly lower in Asian trading but continued to hover above the 1.18 US handle. The EUR/USD rebounded sharply last week as the US dollar weakened against a basket of world peers. The technical picture is neutral, as investors await fresh trading catalysts in the form of economic data and monetary policy. The EUR/USD faces immediate support at 1.1795, followed by 1.1760. On the opposite side of the ledger, immediate resistance is located at 1.1865, followed by 1.1890.

USD/JPY

The USD/JPY is trading in positive territory to start the Monday session, as the greenback continued to trim some of its losses from the previous week. The pair advanced 0.2% overnight to trade just below 112.00. Despite the modest rally, the USD/JPY faces a difficult short-term outlook after prices fell below the 112.20 support region. The pair now faces immediate support at the 26 September low of 1.11.45. Meanwhile, immediate resistance is located at 112.10.

USD/CAD

The USD/CAD advanced on Monday to come within 10 pips of the 1.2500 level. The pair trimmed some of its weekly losses on Thursday and Friday even as oil prices continued to rise. NAFTA talks are in the spotlight for the USD/CAD, and negative headlines from the Trump camp are likely to impact the loonie much more than the greenback.

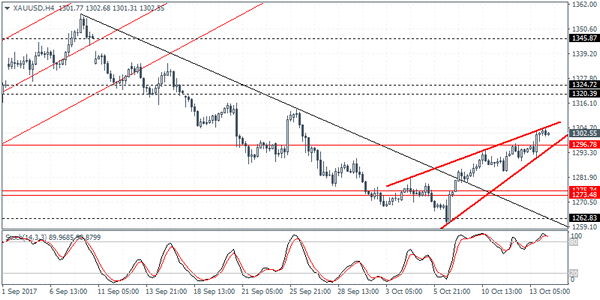

XAUUSD Intraday Analysis

XAUUSD (1302.55): Gold prices rallied to the psychological level of $1300.00 an ounce on Friday. Price action remains trading within the steep rising wedge pattern which could suggest a downside break down in prices. However, with price trading above the minor support level of 1296, we could expect the near-term declines to stall at this level. A breakdown below 1296 is neededin order for gold prices to post a correction towards the 1275 - 1274 level of support.

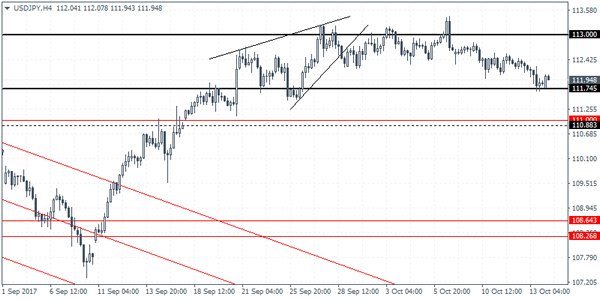

USDJPY Intraday Analysis

USDJPY (111.94): The USDJPY was seen falling to the support level at 111.74 on Friday. However, price action posted a strong bullish candle on the 4-hour session off this support. This suggests that the range between 113.00 and 111.74 could be maintained in the near term. USDJPY has been trading within this range for the past three weeks, and further gains or losses are expected only on a breakout from this range. To the upside, USDJPY will need to rally breaching the resistance level of 113.00 region. This could shift the bias to the upside for a test towards 115.00 region. To the downside, below 111.74 the next main support is seen at 111.00 region.

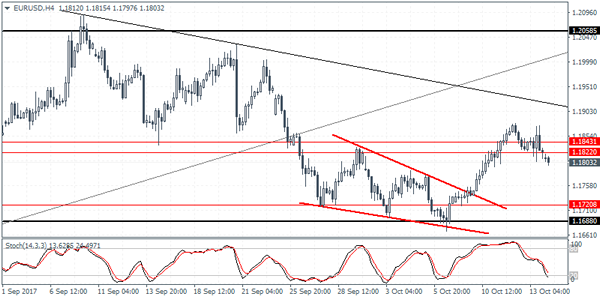

EURUSD Intraday Analysis

EURUSD (1.1803): The EURUSD was seen giving up the gains by Friday's close as price closed with a doji pattern on the daily session. The euro was seen opening weaker this morning as price gapped to the downside below the support level of 1.1822. Further declines could be expected which will see the EURUSD retest the breakout level from the falling wedge pattern that initially sent prices higher. A retest to this breakout level, close to the support established at 1.1720 could see another minor bounce to the upside. A break down below 1.1688 is essential for EURUSD to establish the downside bias. However, for the near term, we expect the range between 1.1822 and 1.1720 to be maintained into next week's ECB meeting.

US Dollar Shrugs Weaker CPI Data

The US dollar was seen trading flat by Friday's close despite the initial losses after data showed that consumer prices rose less than expected. Data from the Labor department showed on Friday that headline consumer prices rose 0.5% on the month in September, accelerating from 0.4% previously. But the data was below forecasts of 0.6%. Core consumer prices also rose 0.2% maintaining the same pace of gains as the previous month. Retail sales, on the other hand, rose 1.6% in September slightly below the forecasts of 1.7%.

The euro was seen trading weaker after comments from Draghi showed that substantial degree of monetary policy was still needed. His comments come ahead of next Thursday's ECB meeting where the central bank is expected to announce another round of tapering.

Earlier today, China's CPI data was seen rising 1.6% on the month as expected while producer prices rose 6.9%, beating expectations of a 6.3% increase. Later in the day, the US Empire state manufacturing index is to be released followed by the quarterly inflation data from New Zealand.

Dollar’s Rally Stall, Oil & Bitcoin On The Move

After enjoying a 4-week rally, the dollar came under pressure last week, falling against most of its major peers, leaving many traders questioning whether the most recent bull run is over for the greenback.

Although U.S. consumer prices rose 0.5% in September, the biggest increase in eight months, when stripping out food and energy, core CPI only recorded a 0.1% increase, suggesting that inflationary pressure remains absent from the largest economy in the world. Moreover, while retails sales jumped 1.6% in September, the largest since March 2015, when you exclude automobiles, gasoline, food services and building materials, core retail sales only recorded a 0.4% increase. The disappointment was felt in fixed income markets, with 10-year treasury yields falling 5 basis points on Friday. However, expectations for a thirdrate hike in December remained above 80%, according to CME's FedWatch Tool.

Given that a December rate hike is almost entirely priced in, the dollar will be driven by longer-term expectations. The three rate hikes plotted on the Fed's dot plot for 2018, is nowhere near to markets' expectations of only one, and the main risk facing the greenback is who will lead the Fed after Janet Yellen departs. It will require robust economic data for dollar bulls to regain control, particularly in wages and inflation expectations. If these two metrics remain weak in the final quarter of the year, I think the dollar will continue to be dragged lower.

Will Carles Puigdemont announce independence?

Euro traders are awaiting the announcement from Charles Puigdemont, on whether he will declare independence from Spain. The deadline given to him is today 8:00 am GMT. If Mr. Puigdemont claims independence, Spain would move towards dissolving Catalonia's parliament and call new local elections. We still don't know how this political conflict will end, but it will no doubt create downside risk to the single currency. However, I still believe that such threats are insignificant and the ECB's policy will remain the dominant driver in the days to come. Tuesday's CPI report will likely help to outline expectations for ECB's monetary policy decision on 26 October.

Iraq conflict moving oil prices

The oil price is the only asset class showing big moves on a quiet Monday. Brent is up more than 1%, trading at its highest level since 28 September, after Iraqi forces began marching towards Kirkuk- an oil-rich Kurdish province. Clashes have been reported between Kurdish fighters and Iraqi forces early today, threatening to disrupt output from Kurdish controlled fields. If the 600,000 barrels a day exports from Kirkuk's oil fields are halted, I expect Brent to retest September's high of $59.49. Oil traders are also monitoring the U.S. – Iranian situation very closely. If the U.S. Congress goes ahead with rekindling economic sanctions on Tehran, after Trump decertifies the nuclear deal, Brent prices will likely breach the $60 benchmark.

'Stupid' investors made more than 400% profit year-to-date

Despite JP Morgan Chase CEO Jamie Dimoncalling people buying Bitcoin 'stupid', and stating that they will 'pay the price for their stupidity', the cryptocurrency surged to a new high of $5,846 on Friday and continued to hover close to this record level. The attempts by government to crackdown on cryptocurrencies, with China being the biggest nay-sayer, is not stopping the growth of wallets in the digital currency. Since Bitcoin entered the mainstream, many investors, including hedge funds, want to be a part of this experiment and this has lead into more inflows into Bitcoin. It's difficult to know whether a bubble is being created, as there are no specific metrics that can be used as a benchmark to determine Bitcoin's intrinsic value. Given that the cryptocurrency is likely to continue attracting new investors, we're likely to see news highs in the weeks to come.

Markets Will Continue To Watch The Developments In Catalonia

Market movers today

Today we have only second tier data releases, with the US Empire manufacturing PMI being the most interesting.

Markets will continue to watch the developments in Catalonia, with a deadline set by the Spanish PM Rajoy to the Catalan president Puigdemont expiring today, regarding clarification of his independence declaration.

Later in the week, we have China's Communist party congress kicking-off, which will have important implications for the future reform progress in China or hear our short video on the congress on YouTube. Chinese President Xi Jinping gives his opening speech on Wednesday.

UK. PM Theresa May is in Brussels meeting with the EU's chief Brexit negotiat or Michel Barnier and head of EU commission Jean-Claude Juncker trying to unlock the Brexit negotiations ahead of the EU summit later this week.

Furthermore, markets will continue to scrutinise central bank speakers during the week for any hints on ECB, Fed and BoE policy direction in 2018.

Selected market news

Over the weekend, a bunch of central comments from the IMF gathering. Fed's Yellen reiterated 'my best guess is that these soft (inflation) readings will not persist' supporting our view that the Fed is hiking in December despite another lower-than-expected US CPI inflation print published Friday, see FOMC minutes. The main argument is still that strong growth will tighten the labour market further, which will eventually push wage growth higher, and hence inflation. On the ECB, all comments echoed the recent communication confirming that the council is moving towards the point that next week's QE extension will be a 'lower for longer ' one. In short , it appears that the ECB has managed to pre-announce the bulk of next week's decision and a 50% reduction in the QE purchases to 30bn is probably market consensus by now.

While central banks are turning more hawkish, they are only doing so slowly due to continuing low inflation. This in combination with the strong global business cycle and low risks are good for equities and Asian stocks are up this morning (also European and US stock futures are point ing higher). Brent oil is trading higher at USD57.9 per barrel, as fight ing between Iraq and Kurdish forces has broken out . Overnight , Chinese CPI inflation in September was 1.6% as expected (down from 1.8% in August ), while PPI inflation rose to 6.9% from 6.3%, which is the highest since April.

In Austria, the general election result Sunday confirmed the anticipated strong result for the right wing parties with the People Party led by Kurtz set to take power (possibly supported by the populist Freedom Party).

In Germany, the social democrats (SPD) surprisingly won the local election in Lower Saxony ahead of Angela Merkel's government coalition talks this week and some argue that the result is another sign of the fall in Merkel's popularity, see FT.

Currencies: Dollar ‘Survives’ Mixed US Data

Sunrise Market Commentary

- Rates: Thin eco calendar suggests directionless action

Confident comments by heavyweight central bankers on inflation and higher oil prices hang in the balance with election outcomes and the approaching Catalan deadline for the Bund this morning. We still shun Spanish assets because of the binary risk while the October 26 ECB meeting and a thin calendar could keep investors side-lines this week. - Currencies: Dollar 'survives' mixed US data

A soft USD CPI weighed temporary on the dollar on Friday, but part of the loss was reversed later indicating some USD resilience. The eco calendar will probably only be of second tier importance for USD trading. Yellen keeping the door open for a December rate hike helps to prevent further USD losses. Uncertainty on Catalonia might be slightly euro negative.

The Sunrise Headlines

- US stocks started strong on Friday, supported by strong US retail sales, but gains evaporated into the close. Nasdaq outperformed with a new record close. Asian bourses gais more than 0.5% overnight with China lagging.

- Austria's far-right nationalist Freedom party has scored its best result in a national election for two decades (26%) and is likely to join the country's next government with the mainstream conservative People's party (31.6%)

- Germany's Social Democrats have won a surprise victory in regional elections in Lower Saxony, in a blow to Angela Merkel's conservatives days before they launch delicate talks in Berlin on forming a three-way coalition government.

- Fed Chair Yellen kept the door open for another increase in short-term interest rates this year, but sounded a note of caution on still weak inflation in the US and abroad.

- China's factory prices jumped more than estimated in September (6.9% Y/Y), as domestic demand remained resilient and the government continued to reduce excess industrial capacity. Consumer price gains matched projections (1.6% Y/Y).

- Oil markets jumped this morning on concerns over potential renewed US sanctions against Iran as well as conflict in Iraq, while an explosion at a US oil rig and reduced exploration activity supported prices there.

- Today's eco calendar is very thin with only EMU trade balance and US empire manufacturing. Catalan President Puigdemont has a Madrid-imposed deadline to clarify the region's independence stance

Currencies: Dollar 'Survives' Mixed US Data

USD 'survives' soft US CPI

US data dominated global FX markets on Friday. Retail sales were strong, but inflation was slightly softer than expected. The latter initially was the more important factor, weighing on the dollar. EUR/USD jumped to the 1.1875 area. However, the dollar this time showed quite some resilience, especially against the euro. A very strong Michigan consumer confidence supported an intraday USD rebound. EUR/USD finished the session at 1.1820, even marginally lower from Thursday. USD/JPY finished the day at 111.82 (compared to 112.28 on Thursday).

The risk rally continues overnight as most Asian equity indices show solid gains. Major central bankers met in Washington this weekend. They saw a further improvement in the global economy. Yellen reiterated that she expects soft inflation readings not to persist. Also ECB top-policy makers expect inflation to pick up. The BoJ still indicates to pursue aggressive monetary easing, but BoJ Kuroda warned that markets might be too complacent when pricing geopolitical risks. USD/JPY profits only modestly from CB signals of ongoing policy divergence between the US/EMU and Japan or from the risk rally. USD/JPY trades near 112. The dollar is better bid against the euro. EUR/USD trades in the low 1.18 area.

The October NY Fed Empire State manufacturing survey is the only important eco release today. The headline index stood at a very high 24.4 in September. Consensus expects a modest decline to 20.5. We expect the October business surveys to remain strong, but have no good arguments to distance us from consensus. Later this week, the US eco calendar is rather light. Housing data recently showed signs of peaking. Will this be confirmed? Few Fed governors are scheduled to speak. The Eurozone eco calendar contains only second tier releases this week. The ECB black-out period before the October 26 meeting kicks in on Thursday, but ECB Constancio (Tuesday), Draghi, Praet and Coeuré (Wednesday) still appear in public. Political developments are plentiful. Catalonia has to respond to Madrid's ultimatum and the EU Summit (Thursday-Friday) will discuss the Brexit negotiations. In the US, the tax reform processes will be closely followed, as well as the Nafta re-negotiation.

The eco data will probably only be of second tier importance today. The dollar showed quite some resilience after an initial negative reaction to Friday's US CPI. The ST picture of EUR/USD remains neutral, but Friday's price action might give EUR/USD bears some confidence

The reaction could have been more negative for the dollar. There is plenty of event risk. Catalonia is the first in row and could be slightly negative for the euro. We start the week with a neutral-to-tentatively negative bias for EUR/USD. The day-to-day picture of USD/JPY is less convincing.

From a technical point of view, EUR/USD dropped below the 1.1823/ 1.2070 consolidation pattern last week, but no real test of the 1.1662 support occurred. Last week, the pair even returned (temporary?) above the 1.1823 previous range bottom, which was disappointing for EUR/USD bears. Friday's US data were unable to give clear guidance. We maintain a cautious sell-on upticks bias. However, the pair needs to drop below the 1.1670/62 support to really give comfort to EUR/USD bears. The USD/JPY momentum was constructive in September. The pair regained 110.67/95 (previous resistance), a short-term positive. The 114.49 correction top is the next important resistance. The rally clearly lost momentum last week. A break beyond 114.49 looks ever more difficult.

EUR/USD: Friday's US data give no clear guidance. Dollar shows tentative signs of resilience.

EUR/GBP

EUR/GBP drifting back south, below 0.89

Thursday's roller-coaster ride of sterling finally turned out in favour of the UK currency. (FX) markets still saw the glass half full rather than half empty on Friday on headlines that the EU considers a transition period, something the UK is aiming for. Enthusiasm eased later in the session on comments from Germany and EU Juncker who highlighted that the Brexit process remains extremely difficult. EUR/GBP rebounded (temporary?) back above 0.89, but sterling maintained most of Thursday's rebound. EUR/GBP finished the session at 0.8898. Cable spiked north of 1.33, partially due to USD weakness after the 'soft' US inflation, but closed the session at 1.3285.

There are no important UK eco data today. Global factors and headlines/rumours on Brexit might dominate sterling trading. A series of key eco data later this week might decide on the viability of a BoE rate hike in the near future. In a day-to-day perspective, euro softness due to Catalan uncertainty might weigh on EUR/GBP.

EUR/GBP staged a strong uptrend since April to set a top at 0.9307 late August. UK price data and hawkish BoE comments reinforced a sterling rebound. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of euro strength and sterling softness to persist. The prospect of (limited) withdrawal of BoE stimulus triggered a good sterling countermove, but this rebound has run its course. EUR/GBP supports at 0.8743 and 0.8652 are difficult to break. We look to buy EUR/GBP on dips. The recent rebound above 0.89 improved the ST technical picture of EUR/GBP, but for now there were no convincing follow-through gains. EUR/GBP 0.9026 is the 50% retracement of the recent countermove.

EUR/GBP rebound loses momentum

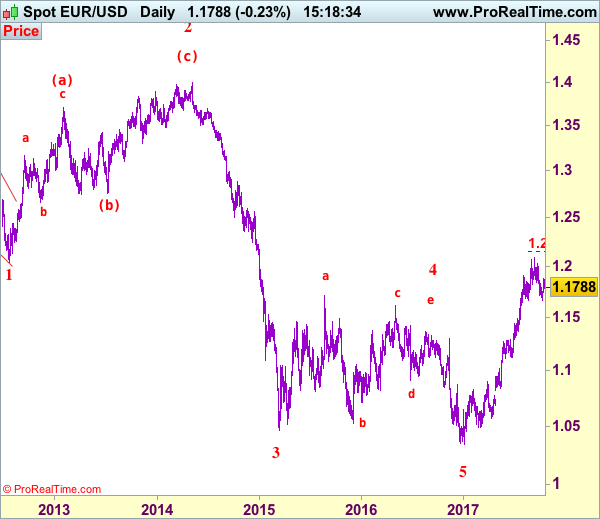

EUR/USD Elliott Wave Analysis

EUR/USD – 1.1800

EUR/USD: Wave (c) of 2 ended at 1.3993 and wave 3 of III has commenced for weakness to 1.0411 (1.236 of wave 1), then 1.0000.

Although the single fell to as low as 1.1669 earlier this month, as euro found good support there and has staged a strong rebound, suggesting the pullback from 1.2093 has possibly ended there, hence consolidation with upside bias is seen for further gain to 1.1900-10, then 1.1950-60, however, reckon upside would be limited to 1.2005 and bring further consolidation. Only break of resistance at 1.2034 would confirm and bring retest of 1.2093, break there would confirm recent upmove from 1.0340 low has resumed for headway to 1.2150-55 (61.8% projection of 1.1119-1.1910 measuring from 1.1662), having said that, loss of upward momentum should prevent sharp move beyond 1.2200-10 and price should falter below 1.2255-60, risk from there remains for a much-needed correction to take place later.

Our preferred count on the daily chart remains that a wave (II) from 1.2329 ended at 1.5145 with A-leg ended at 1.4720, followed by wave B at 1.2457, the wave C from there was also a 3 legged move and is labeled as (a): 1.3739, (b): 1.2885, the wave iii of the 5-waver (c) from 1.2885 has ended at 1.4339 and wave iv is a triangle ended at 1.3878 and wave v formed a top at 1.5145. The decline from there is a 5-waver (C) with minor wave (i) of I of (C) ended at 1.4218 with wave (ii) ended at 1.4580, wave (iii) ended at 1.3267 and wave (iv) ended at 1.3692 and wave (v) ended at 1.1876, this is also the low of wave I of (C) and wave II ended at 1.4940, hence wave III is now in progress with a diagonal wave 1 ended at 1.2042, the breach of previous support at 1.1876 (wave I trough) adds credence to our view that the wave 2 has ended at 1.3993, wave 3 has commenced for further weakness to 1.0411, then towards 1.0000.

On the downside, expect pullback to be limited to 1.1770-75 and price should stay well above said support at 1.1669, bring another rise later. A drop below 1.1669 would signal the corrective fall from 1.2093 top is still in progress for retracement of recent rise to previous support at 1.1662 (previous 4th of a lesser degree), break there would extend weakness to 1.1600-10 and possibly 1.1550-60 but reckon downside would be limited to 1.1500 and support at 1.1479 should remain intact, bring rebound later.

Recommendation: Buy at 1.1765 for 1.1965 with stop below 1.1665.

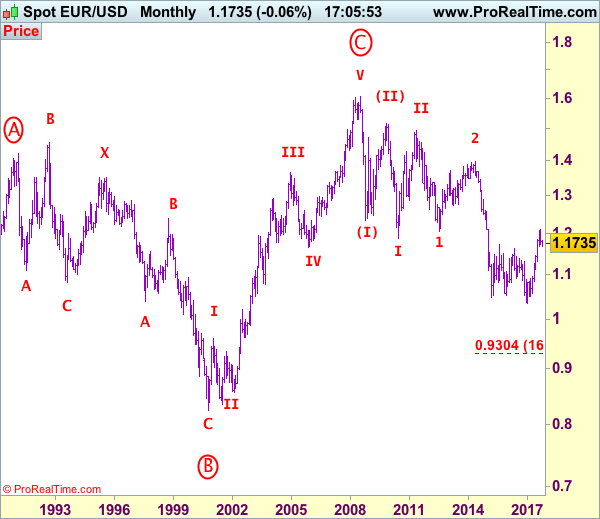

Euro's long-term uptrend started from 0.8228 (26 Oct 2000) with an impulsive structure. The rise from 0.8228 to 0.9593 (5 Jan 2001) is labeled as wave I, the retreat to 0.8352 (6 Jul 2001) is wave II and the rally to 1.3670 (31 Dec 2004) is wave III. Wave IV from there ended at 1.1640 (15 Nov 2005), the subsequent upmove to 1.6040 (July 15, 2008) is treated as wave V, the major selloff from the record high of 1.6040 to 1.2329 (October 27, 2008) signals a reversal has taken place with (I) leg ended at 1.2329 and once (II) ended at 1.5145, wave (III) itself is an extended move with I: 1.1876 and complex wave II ended at 1.4902, wave III has commenced with wave 1 and 2 ended at 1.2042 and 1.3993 respectively, wave 3 of III is now unfolding for weakness towards parity.

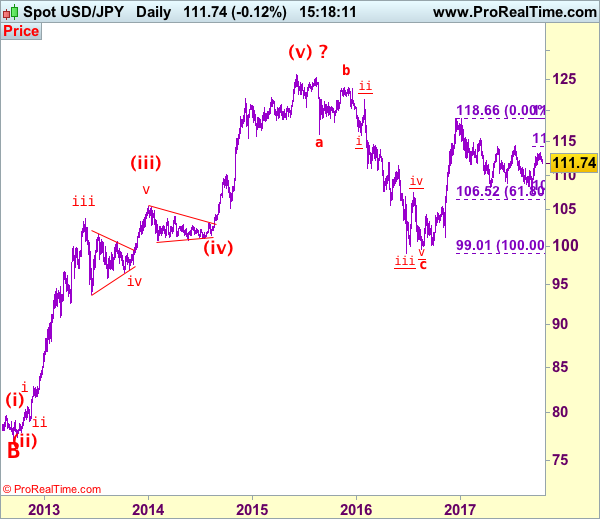

USD/JPY Elliott Wave Analysis

USD/JPY - 111.85

USD/JPY – Wave V of larger degree circle V has possibly ended at 75.31 and major correction has commenced and already met indicated target at 125.00.

Dollar’s retreat after early brief rise to 113.44 has retained our view that consolidation below this level would be seen and initial downside bias remains for correction to previous support at 111.47, however, reckon downside would be limited and renewed buying interest should emerge around 111.10-15 and bring another rise later, above resistance at 112.83 would signal the retreat from 113.44 has ended and bring retest of this resistance, break there would signal the rise from 107;32 low has resumed and extend further gain to 114.00, then towards 114.30-35 (61.8% Fibonacci retracement of 118.66-107.32 but still reckon resistance at 114.50 would hold on first testing and price should falter below 115.00, bring retreat later.

Our preferred count is that, triangle wave IV (with circle) ended at 101.45 and the circle wave V brought dollar down to the record low of 75.31 in 2011 and the subsequent rebound signal major correction has commenced with A leg ended at 84.19, followed by wave B at 77.14 and impulsive wave C is now unfolding (indicated upside target at 125.00 had been met) for gain towards 127.00 level. In the event dollar drops below support at 99.01, this would confirm medium term decline from 125.86 top (2015 high) has resumed for subsequent weakness to 98.00 and possibly 97.00.

Under this count, this wave C is unfolding as impulsive waves with (1) (2), 1 2 ended at 80.67, 79.07, 82.84 and 81.69 respectively, hence the extended wave 3 has ended at 103.74 and wave 4 correction of recent upmove should bring weakness to 92.57, then towards 90.88 but psychological support at 90.00 should limit downside and bring another rally later in wave 5, indicated target at 125.00 had been met and gain to 127.00 cannot be ruled out but reckon price would falter below 130.00.

On the downside, whilst pullback to 111.47 support is likely, reckon another support at 111.11 would limit downside and bring another rise to aforesaid upside targets later. A daily close below 111.11 would defer and risk weakness to 110.50-60, then towards 110.00 but support at 109.55 should remain intact. Only a drop below strong support at 109.55 would abort and suggest the rebound from 107.32 has ended instead, risk weakness to 109.00 and possibly 108.50-60 but price should stay well above said support at 107.32 and bring another rebound later.

Recommendation: Buy at 111.15 for 113.15 with stop below 110.15.

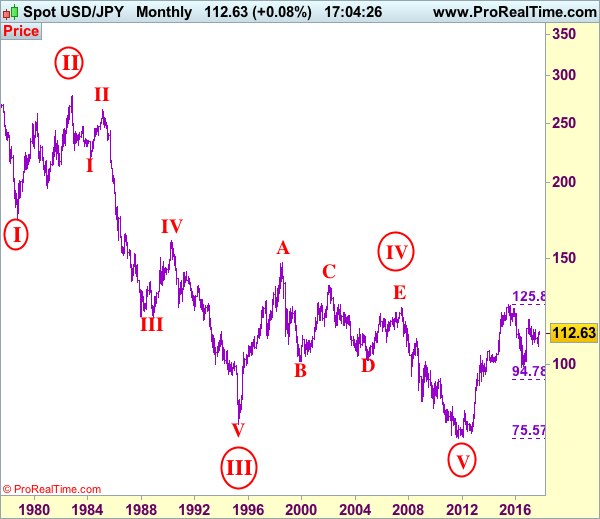

On the monthly chart, we have changed our preferred count that an impulsive wave is unfolding with major wave III with circle ended at 79.75, then followed by wave IV with circle and is labeled as a triangle with A: 147.64 (11 August, 1998), B: 101.25, C: 135.20, D: 101.67 and E leg ended at 124.14 to end the wave IV with circle. Hence, wave V with circle commenced from there and hit a record low of 75.31, however, the subsequent strong rebound signals this circle wave V has possibly ended there, hence gain to (indicated upside target at 122.00 and 125.00 had been met), the retreat from 125.86 suggests wave A of major correction has ended there and wave B correction back to 99.00, then 95.00 would be seen, however, reckon downside would be limited to 90.00, bring another rebound in wave C next year.