Sample Category Title

US Non-Farm Payrolls Fell for the First Time Since 2010

US NFP showed the negative result for the first time in seven years, with record drop in employment registered in hospitality and leisure sector, as expected.

Fall in payrolls which strongly undershoot already low forecast at 90K and previous month's upward-revised 169K build, is expected to be short-lived, as negative numbers were caused by the weather and most of displaced people would probably return to work.

Unemployment rate fell to 4.2% in September, the lowest since Feb 2001 and the figure was not impacted by hurricanes which hit states of Florida and Texas last month.

Wages growth, which was focused today, surprised at the upside with Average Hourly Earnings showing 0.5% rise in September vs forecast for increase by 0.3% and upwards-revised figure in August to 0.2% from 0.1%.

Increase in wages had the strongest impact on the greenback and offset negative tone from NFP's miss.

The US dollar hit fresh highs against the basket of major currencies shortly after US jobs data release.

USDJPY pair broke above pivotal barrier at 113.25 and hit the highest since July 14 at 113.41.

EURUSD slid to new seven-week low at 1.1669, while the British pound fell to one-month low at 1.3035 and eyes psychological 1.3000 support as political uncertainty in the UK additionally pressures pound.

Spot Gold extended broader weakness and met target at $1263, after US jobs data inflated the greenback and Crude Oil fell on dollar's fresh post US jobs report acceleration higher. WTI oil price fell to the lowest in three weeks at $49.55, while Brent oil fell over $1 after US jobs data.

US: Hurricane Impact Played a Role in September’s Jobs Losses

Non-farm payrolls fell 33k positions in September, due largely to disruptions caused by Hurricanes Harvey and Irma. The Bureau of Labor Statistics (BLS) cited that the Hurricanes reduced payroll employment, but that there was no discernable effect on the unemployment rate, which dipped to a 16-year low of 4.2%.

In the payrolls survey, workers who were not paid for the week of September 12th due to disruptions caused by the Hurricanes, are not counted as employed. However, in the household survey, which produces the unemployment rate, persons with a job are counted as employed even if they miss work for the entire week. The BLS stated that no changes were made to the survey or estimation procedures for the September figures and that collection rates were within normal ranges.

Details of the September payrolls report are less meaningful, but it is worth noting that September was the first negative month since 2010. Job losses were concentrated in services (-49k), but goods sector hiring was also soft (+9k). The largest losses, not surprisingly, were in the leisure and hospitality sector (-111k) likely due to Hurricane Irma hitting Florida, and its outsized tourist sector, in the reference week.

On the household side, labor market signals continued to strengthen. The participation rate and the employment to population ratio both increased. In fact, the employment-to-population ratio rose to a new post-recession high of 63.1%.

A healthy wage gain, was the most encouraging aspect of the report. Average hourly earnings rose 0.5% during the month. As a result, the year-over-year wage metric accelerated to 2.9% in September.

Key Implications

Given all the noise associated with the hurricanes, September's payroll disappointing headline should be discounted. Particularly given the healthy results from the household survey. Wage growth is encouraging, but September's data should be taken with a grain of salt, given that wages might have been affected by the industrial composition of jobs, with the losses seen in relatively lower-paying leisure and hospitality sector potentially affecting the average.

The jobs report is another example of economic data being affected by the Hurricanes, making it more difficult to discern underlying trends in the economy. Looking ahead, we would expect the October jobs report to show a solid rebound. Provided the data excluding the effects of the hurricanes remain solid, we continue to expect the Fed to hike rates in December.

Canada Ended Q3 on Another Positive Note for Jobs

Canada recorded a tenth straight month of job gains as 10k net positions were added in September. The unemployment rate was unchanged at 6.2%.

Beneath the relatively modest headline were favourable details, as 112k net full time positions were added, while 102k part time jobs were lost on net – a reversal of August's outturn. The public sector led hiring on net, up 26.2k positions as the private sector shed a net 15.5k postions. Accordingly, the overall gain in employment was the result of employees, with self-employment down a tick on the month.

Goods-producing industries led the gain, adding 10.5k positions, with notable strength in construction (+7.4k). The services side of the economy was flat on the month, as healthy gains in educational services (+20k) and trade (+16.6k) were offset by drops in information services (-23.7k) and health care (-10.4k). Other service industries recorded mixed performances.

Looking across the country, Ontario led the way for a third straight month, notching up 34.7k net new positions on a fairly broad-based industry mix. It was a more modest story across the rest of the country, with declines recorded in Alberta (-7.8k), Quebec (-7.6k) and B.C. (-6.7k).

Wages and hours worked were encouraging. The headline hourly wage rate accelerated further, to 2.2% year-on-year, while hours worked rose 2.4% year-on-year, with the favourable full-time/part-time split helping generate a 0.6% month-on-month increase.

Key Implications

Is there any stopping the Canadian labour market? While the details have often been mixed, Canada has now turned in ten straight months of job gains, and, in a welcome change, the details of September's report were generally encouraging. While hiring was concentrated in the public sector, you have to go back to 2006 to find a month with stronger full-time job gains, and the unemployment rate remained at a post-crisis low.

Perhaps most welcome in this report is evidence that wages and hours worked appear to be leaving this past spring's weakness behind them. While 2.2% wage growth may not be as robust as Canadians are used to, it is also a far cry from the 0.8% growth averaged during the second quarter.

As always, it must be remembered that this is a very noisy series, and so we shouldn't dwell too much on one month, but the trend this year has been very encouraging as the unemployment rate has dropped 0.7 percentage points, and roughly 250k full-time positions have been added on net.

The Bank of Canada will likely be encouraged again by this report, particularly the recovery in wages, but will weigh its implications alongside other, softer data, such as this week's disappointing trade report. On balance, additional tightening remains likely this year, but the Bank of Canada may not feel the same pressure to move quickly, as evidenced by the more dovish tone of recent communication.

September NFP and Canada Job Numbers

U.S non-farm payroll (NFP) saw the first negative reading in seven years at -33k. Headline affected by distortion due to August hurricanes. The unemployment rate, fell two-tenths of a percentage point to +4.2%, a level not seen since early 2001. Workers' wages jumped last month, another figure that may have been affected by the storms. Average hourly earnings rose 12 cents, or 0.45% from a month earlier. Wages were 2.9% higher from a year earlier.

Details:

- US Labor Sep Nonfarm Payrolls -33K; Consensus +80K

- US Sep Unemployment Rate 4.2%; Consensus 4.4%

- US Sep Average Hourly Earnings +0.45%, or +$0.12 to $26.55; Over Year +2.9%

- US Sep Private Sector Payrolls -40K and Government Payrolls +7K

- US Sep Average Workweek 0.0 Hour to 34.4 Hours

- US Sep Labor-Force Participation Rate 63.1%

- US Aug Payrolls Revised to +169K; Jul Revised to +138K

USD remains better bid (€1.1678, £1.3037, ¥113.37) across the board, with treasury yields continuing to back up on inflation expectations.

In Canada, employment rose in September for a tenth straight month and workers' wages increased at their fastest pace in over 17-months. The country's jobless remain unchanged from the previous month, sitting at a post-crisis low.

- Canada Sep Net Jobs +10,000 From Aug

- Canada Sep Jobless Rate Forecast At 6.2%

- Canada Sep Full-Time Jobs +112,000; Part-Time -100,000

- Canada Sep Avg Hourly Wages +2.2% From Year Ago

- Canada Sep Participation Rate At 65.6% Vs 65.7% In Aug

On a year-over-year basis, Canadian employment increased 319,700, or 1.8%, with nearly all of the new jobs created over the past 12 months of the full-time variety, which tend to offer higher pay and steady benefits.

The loonie (C$1.2564) finding support from the full-time employment headline print.

Pound Slide Continues, US Nonfarm Payrolls Next

In the Friday session, the British pound has posted slight losses. Currently, GBP/USD is trading at 1.3094, down 0.18% on the day. On the release front, British Halifax HPI gained 0.8%, well above the forecast of 0.0%. BoE Chief Economist Andy Haldane will speak at an event in London, and the markets will be looking for clues regarding a rate move in November. The US releases key employment numbers, so we could see some movement from the dollar. The markets are braced for a sharp slowdown in Nonfarm Payrolls, with an estimate of just 85 thousand, while Average Hourly Earnings is expected to improve to 0.3%.

The British pound continues to struggle. GBP/USD has posted losses over five straight daily sessions, and the pair is down 2.4% this week. Investors were not impressed with this week's PMIs, which are key gauges of economic activity. Construction and manufacturing PMIs both slowed down in September, raising questions about the health of the British economy ahead of the dark cloud of Brexit. Construction PMI dropped to 48.5, pointing to contraction in the construction sector for the first time since August 2016, shortly after the Brexit vote. Manufacturing PMI slipped to 55.9 in September, down from 56.9 points a month earlier. Although this indicates expansion, the indicator missed expectations. The weak PMI reports could delay plans by the BoE to raise interest rates. BoE Governor Mark Carney has hinted that the Bank will raise rates in the near future, but not all BoE policymakers are on board. Proponents of a rate hike have cited low unemployment and high inflation as reasons to raise rates, but weak data such as the PMIs have raised doubts about whether the economy needs a rate hike at this time.

The crisis in Catalonia continues, as the Spanish and Catalan governments show no signs of backing down. The Catalan parliament has scheduled a meeting for Monday, saying it will consider declaring independence. However, Madrid has obtained a court order suspending the Monday meeting, which would mean that any Catalan lawmakers that defy the court and hold a parliamentary session could be arrested. Which side will blink first? The national government has yet to invoke article 155 of the Spanish constitution, which would allow the government to disband the Catalan parliament. This "nuclear response" could trigger a sharp reaction from Catalonia, which is still seething from the harsh crackdown by police which injured 900 civilians on Referendum Day.

As more Federal Reserve policymakers express support for another rate hike in the near future, the odds of hike continue to climb. On Thursday, Kansas City Federal Reserve Bank President Esther George weighed in, saying that further rate hikes were needed in order for the labor market to remain close to full employment and raise inflation to the Fed's target of 2 percent. The markets have been taking note of the Fed's message, as the odds of a December hike have climbed to 81%. Just a few weeks ago, Federal futures had priced in a December hike at below 50 percent. The Achilles heel in an otherwise strong economy is weak inflation, which remains well below the Fed's target of 2 percent. In addition to a December hike, the markets are keeping a close eye on a possible changing of the guard at the Federal Reserve. Janet Yellen's term as Fed Chair expires in February 2018, and President Trump may decide not to ask her to stay on. The current front-runner for the position is Kevin Warsh a former FOMC member, who is considered hawkish by the markets. Other candidates for the Fed Chair include Federal Governor Jerome Powell and Trump economic adviser Gary Cohn.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1678; (P) 1.1729 (R1) 1.1759; More...

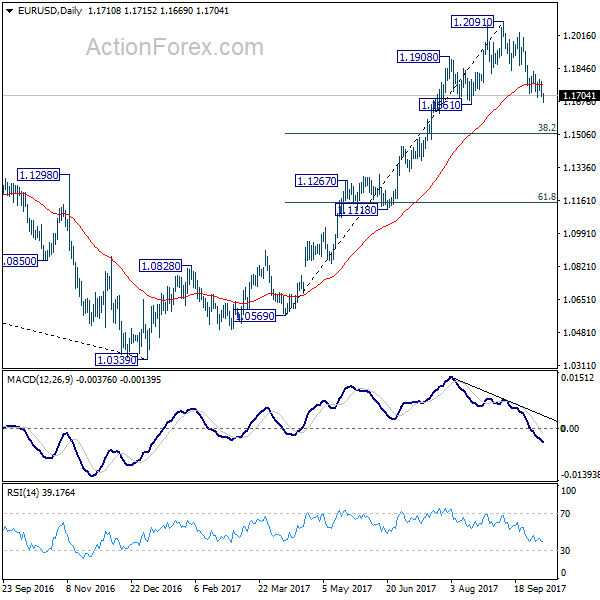

EUR/USD reaches as low as 1.1669 so far as fall from 1.2091 extends. Intraday bias remains on the downside for 38.2% retracement of 1.0569 to 1.2091 at 1.1510. Such decline is seen as a correction to whole rise from 1.0569. We're expecting support from 1.1510 to bring rebound. On the upside, break of 1.1832 minor resistance will suggest that the corrective fall is completed and turn bias back to the upside.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3066; (P) 1.3158; (R1) 1.3208; More....

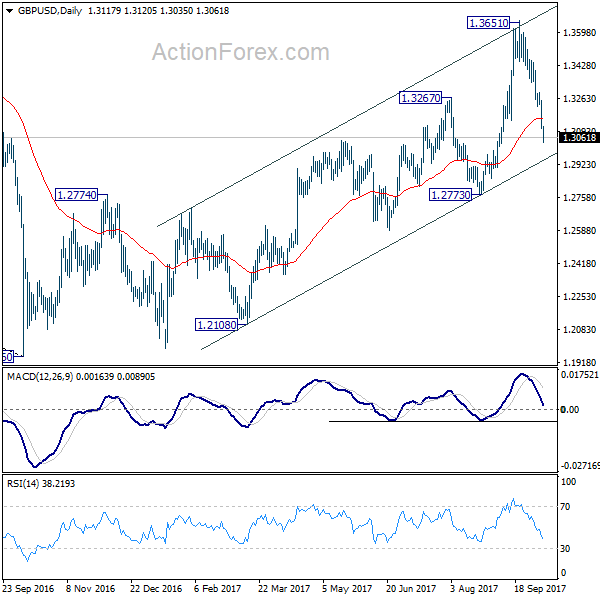

Intraday bias in GBP/USD remains on the downside Current decline from 1.3651 would be targeting 1.2773 key support next. We'll start to look for bottoming around there. On the upside, above 1.3221 minor resistance will turn intraday bias neutral first. Another decline is mildly in favor after the consolidation completes.

In the bigger picture, current development argues that the long term trend in GBP/USD has reversed. That is, a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.51; (P) 112.71; (R1) 113.02; More....

The break of 113.25 temporary top argues that USD/JPY's rise from 107.31 is resuming. Intraday bias is cautiously back on the upside. Sustained break of medium term falling channel will argue that correction from 118.65 is already completed with three waves down to 107.31. Break of 114.49 will confirm this bullish case and target a test on 118.65 next. On the downside, however, break of 112.31 minor support will mix up the near term outlook again and turn bias neutral first.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9750; (P) 0.9773; (R1) 0.9805; More....

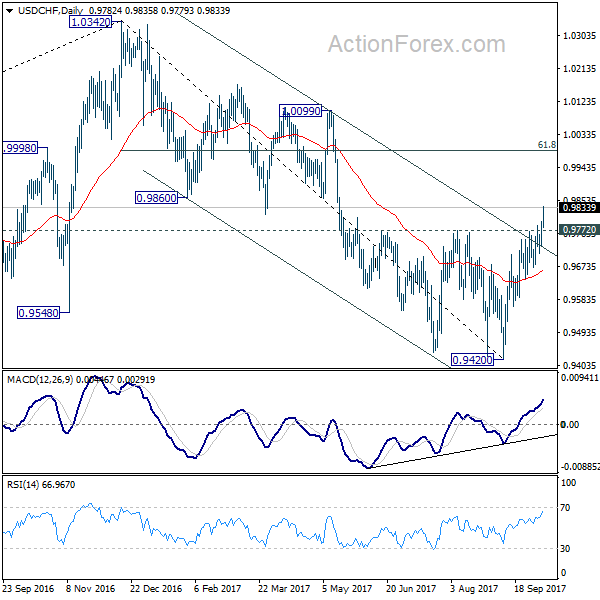

USD/CHF surges to as high as 0.9813 so far after finally taking out 0.9772 resistance decisive. As noted before, fall from 1.0342 should be completed at 0.9420, considering the sustained trading above medium term channel resistance. Intraday bias remains on the upside for 61.8% retracement of 1.0342 to 0.9420 at 0.9990. On the downside, break of 0.9708 support is needed to be first sign of short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Dollar Shrugs off -33K NFP Contraction, Surges on Strong Wage Growth

Dollar spikes higher in early US session even though the headline Non-Farm Payrolls number is a big disappointment. NFP dropped -33K in September, first contraction seen since 2010. That's also much worse than expectation of 77K. However, it should be noted that the figure was skewed heavily by the impact of hurricanes Harvey and Irma. And the markets seem not to be to bothered by it. Unemployment rate dropped to 4.2%, down from 4.4%, lowest since December 2000. Participation rate also increased to 63.1%, up from 62.9%. The most positive surprise is wage growth. Average hourly earnings jumped 0.5% mom. While wage growth could also be inflated by the hurricanes, it beats an also optimistic expectation of 0.3% mom already.

Released elsewhere, Canada job market grew 10K in September, below expectation of 14k. But unemployment rate was unchanged at 6.2%. Swiss foreign currency reserve hit record high of CHF 724B in September. German factory orders rose 3.6% mom in August. Japan Japan labour cash earnings rose 0.9% yoy in August. Leading indicator rose to 106.8 in August.

Sterling staying weak on political turmoil

Sterling will likely end the week as the weakest major currency on political turmoil in UK. Former Conservative Chairman Grant Shapps admitted that he is leading a plot to force Prime Minister Theresa May to call a leadership election. Shapps said that up to 30 MPs are backing him. May hit back and pledged to stay as "the country needs calm leadership and that is exactly what I am providing." Even worse for the country is that EU ministers are going to meet on October 19-20. Decision will be likely be made that there is not enough progress in Brexit negotiation to move on the the next stage. It's already unlikely to have any breakthrough in such short period of time. And it's even harder as May could be fighting her own crisis. So far, no clear contender is named to challenge May yet. But it's believed that Foreign Secretary Boris Johnson, Home Secretary Amber Rudd, Brexit secretary David Davis, Leader of Scottish Conservative Party Ruth Davidson and MP Jacob Rees-Mogg.

BoJ survey showed fewer people expected price rise

According to a Bank of Japan survey conducted across 4000 households, 70.4% expected price will rise a year from now. That's a notable drop from 75.4% from the last survey. Meanwhile, 81.4% expected price to rise five years from now, also down from June's 82.3%. Meanwhile, BoJ's government bond holds dropped in September, the first time since the massive stimulus program was deployed back in 2013. Holdings dropped to JPY 404.24T in September, down JPY 705b from August. The results showed that BoJ could be starting to slow down the purchases under the Yield Curve Control framework. But a few more months of data is needed to confirm.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9750; (P) 0.9773; (R1) 0.9805; More....

USD/CHF surges to as high as 0.9813 so far after finally taking out 0.9772 resistance decisive. As noted before, fall from 1.0342 should be completed at 0.9420, considering the sustained trading above medium term channel resistance. Intraday bias remains on the upside for 61.8% retracement of 1.0342 to 0.9420 at 0.9990. On the downside, break of 0.9708 support is needed to be first sign of short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development suggests that USD/CHF has defended 0.9443 (2016 low) key support level again. Rise from 0.9420 could develop into a medium term move and target a test on 1.0342 high. This represents the upper end of a long term range that started back in 2015. On the downside, break of 0.9587 support is now needed to indicate completion of the rise from 0.9420. Otherwise, further rally will remain in favor in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Aug | 0.90% | 0.50% | -0.30% | -0.60% |

| 05:00 | JPY | Leading Index Aug P | 106.8 | 107.2 | 105.2 | |

| 06:00 | EUR | German Factory Orders M/M Aug | 3.60% | 0.70% | -0.70% | -0.40% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Sep | 724B | 717B | ||

| 12:30 | CAD | Net Change in Employment Sep | 10K | 14.0K | 22.2K | |

| 12:30 | CAD | Unemployment Rate Sep | 6.20% | 6.30% | 6.20% | |

| 12:30 | USD | Change in Non-farm Payrolls Sep | -33K | 77K | 156K | 169K |

| 12:30 | USD | Unemployment Rate Sep | 4.20% | 4.40% | 4.40% | |

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.50% | 0.30% | 0.10% | |

| 14:00 | CAD | Ivey PMI Sep | 57.2 | 56.3 | ||

| 14:00 | USD | Wholesale Inventories Aug F | 1.00% | 1.00% |