Sample Category Title

DAX Closing In On 13,000, German Factory Report Surges

In the Friday session, the DAX has inched higher in the Friday session. Currently, the index is at 12,980.50, up 0.10% on the day. On the release front, German Factory Orders surged 3.6%, crushing the estimate of 0.7%. Later in the day, the US releases key employment numbers. Nonfarm Payrolls are expected to slip to 85 thousand, while Average Hourly Earnings is forecast to improve to 0.3%.

The DAX continues to trade at record levels, as it moves towards the symbolic 13,000 level. The index has posted gains this week, surged 6.0 percent in September, as the robust German economy continues to show post strong economic numbers. German Factory Orders climbed 3.6% in August, marking its sharpest gain in 2017. Earlier in the week, German Manufacturing PMI improved to 60.6 in September, its highest level since April 2011. German Services PMI has also been strong, pointing to expansion. However, inflation levels remain low in both Germany and the eurozone. On Tuesday, there was good news on the inflation front, as Eurozone PPI beat expectations with a gain of 0.3 percent. Is eurozone inflation on its way up? If upcoming inflation indicators follow suit and point upwards, the ECB will have to revisit tightening its ultra-loose monetary policy. With the eurozone showing sustained growth in 2017, the cautious ECB will be reluctant to tighten policy, unless inflation moves higher. However, the ECB will have to make some important decisions, as the bank’s current asset-purchase program is scheduled to terminate in December.

The constitutional crisis in Spain continues to deepen, and this has predictably sent Spanish stock markets lower. The Spanish and Catalan governments show no signs of backing down from their entrenched positions. The Catalan parliament has scheduled a meeting for Monday, saying it will consider declaring independence. However, Madrid has obtained a court order suspending the Monday meeting, which would mean that any Catalan lawmakers that defy the court and hold a parliamentary session could be arrested. Which side will blink first? The national government has yet to invoke article 155 of the Spanish constitution, which would allow the government to disband the Catalanian parliament. This “nuclear response” could trigger a sharp reaction from Catalonia, which is still seething from the harsh crackdown by police which injured 900 civilians on Referendum Day.

Elliott Wave Analysis: Crude Oil And Audusd Intra-day View

Today let's take a look at AUDUSD and Crude Oil and their intra-day development.

AUDUSD is trading in a bearish leg as part of a higher degree wave 5. We know that wave five is an impulse, meaning it must consist out of five waves. At the moment we see only three of them fully unfolded, which means two more must show up.

That said, we see current price rising, but only for a temporary correction within sub-wave iv of 5. Resistance is seen at Fibonacci ratio of 38.2 and near the 0.7798 level.

AUDUSD, 1H

Let's now switch to Crude oil. On crude oil we are tracking a bigger three-wave decline, with first wave a completed. Ideally recent rise that followed was sub-wave a) of b that found a top near the 51.20 level. Current drop that is now underway can be sub-wave b) that can also unfold a minor three-wave move within itself, before a final and last push higher can come into play within sub-wave c) of b. The whole correction within blue wave b can later search for a top at the former swing high of wave ii) at the 51.75 level and near the Fibonacci ratio of 50.0/61.8. However if prices continues to drop sharply, then we can say wave b already found a top and that blue wave c can be in progress.

Crude OIL, 30Min

Technical Outlook: US DOLLAR INDEX – Bulls Look For Attack At Daily Cloud Top On Upbeat US Jobs Data

The dollar index remains in strong uptrend for the third consecutive week and moving within bullish channel from $91.20 (20 Sep low).

The price is heading higher within thick daily cloud and posted new high at $93.93 (the highest since 17 Aug) after bullish signal was generated on Thursday’s strong rally and close above $93.61 (Fibo 50% of $96.24/$90.97 Jul-Sep downleg).

Bullish daily techs and weekly studies regaining traction, suggest further upside, as rally in past three weeks generated initial reversal signal which could result in stronger correction of larger fall from $102.23 (05 Mar high) to $90.97(03 Sep low).

Bulls eye initial targets at $94.04 (16 Aug high) and $94.23 (Fibo 61.8% of $96.24/$90.97) which guard pivotal barrier, provided by daily cloud top at $94.44. Close above cloud would generate strong bullish signal.

US jobs data are in focus, with better than expected numbers in September to further inflate the greenback.

Res: 94.04, 94.23, 94.44, 95.00

Sup: 93.72, 93.47, 93.23, 93.07

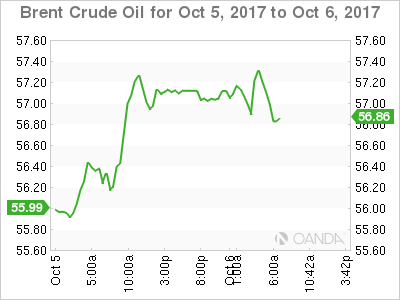

Crude’s Rally, Black Gold Or Fool’s Gold?

Crude's overnight spike in gave bulls much to cheer about, but it remains to be seen if the geopolitical drivers can sustain the rally.

Crude prices had a wellhead blowout overnight, erupting higher as a combination of rumours and geopolitical news created rich pickings for oil bulls. WTI climbed 1.75% on the day to close at 50.25, but it was coat tailing Brent which was the star of the show, rising 2.10% to close at 57.15.

Alleged reports that Russia and Saudi Arabia have agreed to extend the production cuts until the end of 2018, nicely dovetailing with the Saudi King's visit to Russia, gave oil it's initial boost. Worries that the U.S. may reimpose sanctions on Iran and the announcement that Turkey, Iran an Iran had agreed to curtail Kurdish oil exports, currently 550,000 barrels a day, did the rest. The question will be into the weekend, whether geopolitics alone will be enough to sustain yesterday's jump.

Brent crude is slightly lower at 57.10 in Asia, and the overnight high at 57.40 is the initial resistance followed by 57.60. On the downside, Brent has held the lower end of the longer term breakout zone at 55.50 in a pleasing technical development. Support then appears below there at 54.90.

WTI trades 30 cents lower at 50.30 with some profit taking around following the overnight rally. Resistance at 51.00 will be challenging initially closely followed by the 51.50 area. Support lies at 49.50 followed by the 200-day moving average at 49.25 with a break of the latter implying the rally was fool's gold and not black gold.

September NFP: What To Expect?

The September U.S. employment report (08:30 am EDT) should be affected by the impact of Hurricanes Irma and Harvey in late August.

The median forecast for this morning's release is a +80k gain in non-farm payrolls, less than half the average +182k monthly rise since the start of last year and an unemployment rate of +4.4%.

Note: U.S state by state data due near the end of this month will be able to strip out that impact for the rest of the country.

The 'mighty' U.S dollar is expected to carry on as usual, even though the headline number is expected to be much smaller. Beyond a headline shock, the consensus is anticipating the implication and knee-jerk reaction for bonds and FX should be muted and indeed short-lived as the Fed is expected to look though the fall and continue with its policy normalization.

However, if the headline print comes in on the strong side, it should inspire “bullish investors” in the U.S dollar, and potentially push the dollar index to new highs.

Fed fund futures are pricing in a +78% probability that the Fed will hike interest rates by the end of the year, up from around +44% last month.

Elsewhere, Canada will also release its employment report at 08:30 am EDT. Dealers are looking for a headline print of +13k and the unemployment rate to tick up a tad to +6.3%.

1. Stocks in the black

In Japan, the Nikkei share average scaled a fresh two-year peak on Friday and posted its fourth straight weekly gain, buoyed by the impact of a weaker yen (¥113.05) as well as record highs on Wall Street. The Nikkei ended +0.3% higher. For the week, it added +1.6%, while the broader Topix was up +0.2%.

In Hong Kong, the benchmark stock index closed at its highest level in a decade Friday, supported by Chinese automakers and banks. The Hang Seng index rose +0.3%. On the week, the index rose +3.3%, its biggest such gain in three-months. The China Enterprises Index rallied +0.5%, its highest close since mid-2015. It ended up +5% for the week, the best in six-weeks.

Note: The Shanghai Composite and Korea Kospi remained closed for Golden Week.

Down-under, S&P/ASX closed out the week up +1.04%, mostly supported by 'dovish' comments from RBA's Harper on potential rate cuts.

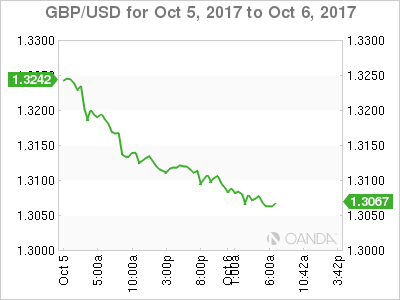

In Europe, regional bourses have opened mixed with peripherals once again under pressure; banks with exposure in Catalonia are especially impacted. U.K's FTSE 100 is being supported by weakness in sterling (£1.3073).

U.S stocks are set to open in the red (-0.5%).

Indices: Stoxx50 -0.2% at 3,604, FTSE +0.1% at 7,518, DAX +0.1% at 12,974, CAC-40 -0.2% at 5,370, IBEX-35 -0.7% at 10,144, FTSE MIB -0.8% at 22,393, SMI +0.2% at 9,280, S&P 500 Futures -0.05%.

2. Oil markets wary as a storm heads for Gulf of Mexico, gold lower

Oil markets remain cautious as traders monitor a tropical storm heading for the Gulf of Mexico.

However, the prospect of extended oil production cuts by OPEC and non-OPEC members is providing some underlying support.

Brent crude futures are down -12c at +$56.88 a barrel, while U.S light crude (WTI) is trading at +$50.63 per barrel, down -16c from Thursday's close.

Tropical storm Nate heading for the Gulf of Mexico has triggered U.S Gulf production and refinery closures just weeks after several hurricanes pummelled the region.

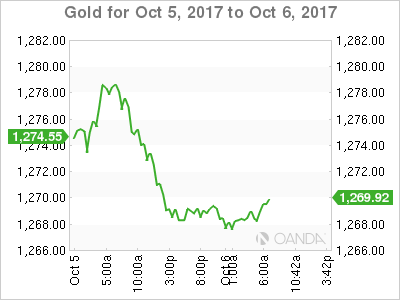

Ahead of the U.S open, gold has hit its lowest print in nearly two-months in range-bound trade, as the 'mighty' dollar climbs to a two-month high ahead of today's jobs data.

Spot gold is at +$1,267.71 an ounce, after hitting its lowest since Aug. 9 earlier in the session. It is down -0.9% for the week and is heading for a fourth straight weekly decline.

3. Yield differentials the name of the game

10-year Spanish government debt is broadly unchanged in early Friday trade as they continue to benefit from Thursday's well-received debt auction. Fixed income dealers say the auction may have “signaled a turning point in the mood toward Spanish debt” after its losing streak following Sunday's Catalan independence vote. The 10-year Spanish bond yield trades at +1.70%, about +9 BPS up from the Sept. 29 close, the last trading session before last weekends 'illegal' referendum.

Firming expectations that the Fed will hike rates in December coupled with domestic data pointing to steady growth in the U.S and talk of a potentially more 'hawkish' successor to Fed Chair Janet Yellen is helping to support higher U.S yields. The yield on 10-year Treasuries have gained +2 bps to +2.36%, the highest in more than three-months.

In Germany, the 10-year Bund yield has climbed +3 bps to +0.48%, the highest in more than two-months, while in the U.K, the 10-year gilt has advanced +3 bps to +1.414%, the highest in eight-months.

4. Pound under Political Pressure

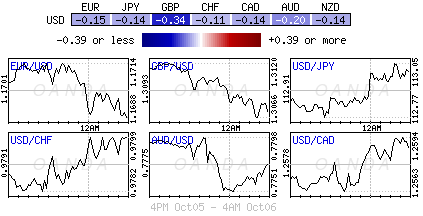

U.K's political uncertainty has sent the pound to three-week lows against the USD and EUR on reports that a group of Conservative MPs are calling for Theresa May to quit as Prime Minister. This threat is now posing market doubts on whether the Bank of England (BoE) would hike rate in November. GBP/USD is down -0.4% to £1.3060, while EUR/GBP has rallied to €0.8956.

The EUR is little changed after the release of the ECB minutes yesterday, which gave little detail on plans to scale back asset purchases under QE. The EUR/USD trades atop of €1.1700, little changed from Thursday's close. The minutes said ECB officials discussed how to scale down their giant bond-buying program at their September policy meeting, but said policy makers want to proceed “in a very gradual and cautious manner.” They expressed some concern about weak inflation and disagreed on the reasons for the recent appreciation of the EUR.

Down-under, following yesterday's Australian retail sales induced declines (-0.6% vs. +0.3% m/m); the AUD has again struggled in the overnight session (A$0.7763) after RBA official Harper surprised the market with his statement that the central bank did not rule out a rate cut amid the weaker retail sales data. The RBA last cut rates in Aug 2016.

5. Italian retail trade disappoints

The value of Italian retail trade decreased by -0.3% in August 2017 compared with the previous month (-0.4% for both food goods and non-food goods) and decreased by -0.5% compared with August 2016 (+0.8% for food goods and -1.5% for non-food goods).

Despite short-term variability, the underlying pattern in retail trade remains flat as in the three months to August 2017 the value is estimated to have decreased by -0.1%, whilst the volume is estimated to have increased by +0.1%.

The volume of retail trade decreased by -0.4% compared with July 2017 (-0.4% for food goods and -0.5% for non-food goods) and decreased by -1.0% from the same month a year earlier (+0.0% for food goods and -1.8% for non-food goods).

Note: Looking at year-on-year change, retail trade sales were up +1.4% in large-scale distribution and down -2.4% in small-scale distribution.

Technical Outlook: GBPJPY – Extended Wave ‘C’ Eyes Its Fibo Expansions At 147.02 And 146.25

.

Negative sentiment on political uncertainty in the UK keeps sterling under pressure. The cross extends weakness on Friday and broke below target at 147.67 (Fibo 38.2% of 139.30/152.85 rally), as Thursday's long bearish daily candle weighs.

Bears look for fresh negative signal on close below 147.67, with the pair being on track for the second weekly bearish close and biggest one-week fall since late January.

Next target lies at 147.02 (FE 138.2% / daily Kijun-sen / rising 30SMA) with further stretch of current third wave of five-wave cycle from 152.85, to target its Fibonacci expansion levels at 146.25 (FE 161.8%) and 145.76 (FE 176.4%).

Initial resistance lies at 148.02 (session high), followed by daily Tenkan-sen in steep fall (currently at 149.50).

Res: 147.67, 148.02, 148.37, 149.15

Sup: 147.02, 146.25, 146.07, 145.76

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1691

The outlook is bearish below 1.1730, for a break through 1.1660, towards 1.1480 zone.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1730 | 1.1830 | 1.1660 | 1.1660 |

| 1.1830 | 1.2070 | 1.1540 | 1.1480 |

USD/JPY

Current level - 113.04

I favor a break through 113.20 to provoke a rise towards 114.50 zone. Key support is projected at 112.15.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.20 | 113.80 | 113.20 | 113.80 |

| 113.80 | 114.50 | 113.80 | 114.50 |

GBP/USD

Current level - 1.3073

Yesterday's break through 1.3220 led to acceleration of the downtrend and the bias remains bearish, for a slide towards 1.3000 area. Initial intraday resistance lies at 1.3150, followed by 1.3220.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3150 | 1.3340 | 1.3000 | 1.2910 |

| 1.3220 | 1.3650 | 1.2910 | 1.2760 |

CRUDE OIL Bullish Consolidation

Crude Oil has bounced back above the $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 52.43 (26/09/2017) has been broken. Expected to show continued weakness.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Sideways Price Action

Silver is weighing down. Hourly resistance is given at 16.89 (04/10/2017 high) while hourly support can be found at 16.54 (04/10/2017 high). Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Weakening

Gold has broken hourly support given at 1267 (15/08/2017 low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further weakness.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major supp