Sample Category Title

EUR/JPY Upside Momentum Favored

Price failed to stay below the outside sliding line (SL) and now tries to climb higher because the Yen is demolished by the Nikkei’s impressive rally. The Nikkei stock index rallied and jumped much above the 20498 previous high. The index opened with a gap up in the yesterday’s morning, signaling that the bulls are in full control. However, only a valid breakout above the median line (ml) of the black ascending pitchfork will confirm a further increase in the upcoming weeks.

EUR/CHF Further Drop Invalidated

Price increased significantly in the second part of the yesterday’s trading session and has managed to stay much above the upper median line (uml) of the minor ascending pitchfork. Price increased today and resumes the yesterday’s increase. Technically, it should approach and reach the upper median line (uml) of the descending pitchfork in the upcoming period after the failure to reach the median line (ml).

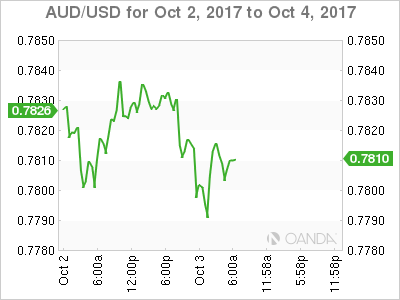

AUD/USD Focused On Correction

AUD/USD drops further and extends the bearish movement. The USD drags the price lower as the USDX has managed to resume the yesterday's impressive rally. Price is trading in the red and is targeting new lows after the retest of a dynamic resistance (support turned into resistance). Technically is expected to drop further in the upcoming days because has fallen much below the 0.7807 August low.

Remains to see what will happen because the USDX is pressuring the 93.81 static resistance, has climbed above it, but this needs to be confirmed.

The AUD/USD increased a little in the last hour as the USDX has slipped lower after the morning rally. The Reserve bank of Australia has decided to leave the Cash Rate unchanged at 1.50%, matching expectations. The Australian Commodity Prices increased only by 18.3% in September, less versus the 20.8% growth in the former reading period, while the ANZ Job Advertisements rose by 0.0%, less compared to the 1.7% growth in the former reading period. Moreover, the Building Approvals surged by 0.4%, less versus the 1.1% estimate.

Price dropped further after the yesterday's minor indecision and reached the 0.7784 level. The perspective remains bearish as long as is trading below the median line (ml) of the minor descending pitchfork. The next downside target will be at the 0.7755 level, but could be attracted by the first warning line (WL1) of the major ascending pitchfork.

Technical Outlook: AUDUSD Maintains Bearish Tone After RBA But Daily Cloud Base Still Holds

The Aussie dollar remains in red on Tuesday and hit new 2 ½ month low at 0.7785 on renewed probe below daily cloud base (0.7800).

The Reserve Bank of Australia held interest rates steady at record low at 1.5%, despite signals that the economy continues to improve.

The pair remains in steady descend but so far unable to clearly break below cloud base. Narrow consolidation could be expected before bears resume, with 0.7835/60 resistance zone to cap upside attempts.

Close below daily cloud will be bearish signal, with violation of next support at 0.7770 (100SMA) needed to confirm bearish continuation of the wave C from 0.8102 (20 Sep high) towards its FE 200% at 0.7733.

Alternative scenario requires sustained lift above 0.7860 to sideline immediate bearish threats and turn focus towards upper pivot at 0.7915/10 (daily cloud top, reinforced by falling Tenkan-sen).

Res: 0.7820, 0.7835, 0.7860, 0.7910

Sup: 0.7800, 0.7785, 0.7770, 0.7733

Technical Outlook: EURUSD – Bears Struggling To Break 1.1720 Pivot

The Euro is holding in daily cloud on Tuesday and probes again below strong supports at 1.1720/10 (Fibo 38.2% of 1.1118/1.2092 rally / weekly 200SMA).

The pair hit new low at 1.1696 (the lowest since 17 Aug) but so far without clear break lower. Monday’s long bearish candle weighs on near-term action for final break below 1.1720/10 pivots and fresh bearish acceleration which could extend towards next strong supports at 1.1605/1.1594 (50% retracement of Jun/Sep 1.1118/1.2092 ascend / daily cloud base).

Meanwhile, extended consolidation could be expected while supports at 1.1720/10 hold, but upside action should be limited under cloud top, as formation of 10/55 SMA’s bear-cross (1.1825) maintains downside pressure.

Res: 1.1748, 1.1764, 1.1780, 1.1810

Sup: 1.1720, 1.1696, 1.1662, 1.1594

Technical Outlook: GBPUSD – Consolidation To Precede Fresh Downside

Cable bounced from fresh 2 ½ week low at 1.3228, posted in Asia, consolidating strong fall on Monday and keeping bearish near-term stance.

Initial probe below daily Kijun-sen (1.3253) did not result in clear break lower. Bears are expected to consolidate before fresh push lower for test of rising 30SMA (1.3209) and possible extension towards 55SMA at 1.3120).

Monday’s close below weekly 100SMA (1.3363) and Fibo 61.8% of 1.3148/1.3655 upleg generated bearish signals, turning these points to resistances which should ideally cap upside attempts.

Today’s focus is on UK Construction PMI data. Forecast for September lies at 51.0 vs 51.1 in Aug, with lower than expected release to put sterling under fresh pressure (especially if Sep release falls below 50 threshold), while upside surprise would support pound for further recovery.

Res: 1.3287, 1.3342, 1.3363, 1.3401

Sup: 1.3253, 1.3228, 1.3209, 1.3148

Technical Outlook: USDJPY – Bulls Look For Final Break Above 113.20/25 Pivots

The pair maintains firm tone on Tuesday and is back above 113.00 handle, approaching recent highs at 113.20/25.

Fresh bullish extension on Tuesday is on track to fully retrace 113.25/112.21 correction and generate bullish signal on eventual close above cracked 112.80 barrier (Fibo 76.4% of 114.49/107.31 descend) and lift above 113.20/25 spikes.

Bullish tech on daily chart are supportive, with rising 10SMA tracking the advance in past three week and bullish stance being boosted by 10/200SMA Golden cross.

Sustained break above 113.20/25 pivots is required to confirm scenario and open way towards next barriers at 113.57/114.00 (14 July lower top / round-figure resistance) with key barrier at 114.49 (114 July peak) expected to come in focus.

However, recent repeated failures to sustain probes above 113.00 warn of possible extended consolidation if bulls stall again.

Bullish stance is expected to stay intact while rising 10 SMA (112.41) holds, while break here would generate bearish signal.

Res: 113.25, 113.57, 114.00, 114.49

Sup: 112.61, 112.41, 112.21, 111.98

Technical Outlook: EURGBP – Recovery Eyes Key Barrier At 0.8900

The cross rallied on Tuesday and retested Monday's high at 0.8868, as pound was hit be weaker than expected UK data.

Bulls extend for the third straight day and set for further advance towards key near-term barrier at 0.8900 zone (19 Sep correction high / converged sideways-moving 100SMA / falling 20SMA).

Current recovery rally is seen as correction of broader downtrend which should be ideally capped at 0.8900 zone before bears resume.

Slow stochastic is entering overbought territory and supports scenario, with falling 20SMA on track to form bear-cross with 100SMA and produce additional pressure.

Alternative scenario requires sustained break above 0.8900 barrier to ease bearish pressure, but break above 0.8960 (Fibo 38.2% of 0.9306/0.8745 fall) is needed to confirm reversal and open way for further recovery.

Res: 0.8878, 0.8900, 0.8960, 0.9000

Sup: 0.8821, 0.8808, 0.8745, 0.8725

Sterling Stymied By Construction Numbers

Tuesday October 3: Five things the markets are talking about

Ahead of the U.S open, investors appear to be taking a breather after the themes of tighter U.S monetary policy, a potentially more 'hawkish' Fed chief and stronger U.S data helped to drive recent gains for both the 'mighty' dollar and equities.

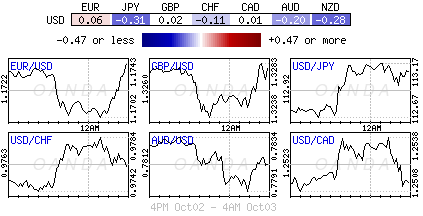

The EUR (€1.1737) is facing ongoing pressure from Spain's biggest constitutional crisis in decades, after last weekends violent 'illegal' independence referendum in Catalonia may have opened the door for the region to move for separation as early as this week.

In the U.K, GBP (£1.3247) continues to trade under pressure in the midst of this week's U.K Conservative Party's annual conference where there could be challenges to PM Theresa May's leadership. Boris Johnston, Davis, Rudd and Fox are all scheduled to speak today – U.K's foreign minister Johnston in particular could cause a ripple effect for the pound.

Weaker U.K construction PMI this morning (see below) is also providing the pound some problems and in mainland Europe some E.U officials have reiterated their views of insufficient progress in Brexit talks.

U.S. data this week include trade, durable goods and Friday's September non-farm payroll (NFP) report, which may be distorted from hurricanes that hit stateside from late August.

1. Stocks mostly in the 'black'

Stateside Monday, all three major indexes posting record-high closes after the ISM index of U.S manufacturing surged to just shy of a four-year high in September.

In Japan, the Nikkei stock index ended up +1.1% as a tailwind from a weaker yen (¥113.00) helped power it to its highest levels in two-years. The broader Topix gained +0.7%, also the highest closing level since mid August 2015.

Note: Markets in China, S. Korea and Germany are closed for holidays.

In Hong Kong, the blue-chip Hang Seng index rallied +1.9% as trading resumed following a public holiday on Monday, led by mainland banks and insurers after the People's Bank of China (PBoC) cut reserve ratios (RRR) over the weekend to encourage lending. The Hong Kong China Enterprises Index rallied +3.2%.

Down-under, Australia's S&P/ASX 200 slipped -0.5%, pressured by financial and energy shares.

Note: As widely expected, the Reserve Bank of Australia (RBA) kept interest rates on hold at a record low of +1.5%. The RBA said a stronger AUD (A$0.7800) would slow the economy and restrain price pressures.

In Europe, regional bourses have opened higher and continue to trade in positive territory. Materials are underperforming on drop in commodities, while energy is also under pressure from oil price. Uncertainty over Catalonia continues to weigh on risk sentiment and especially Spanish stocks.

U.S equities are set to open little changed.

Indices: Stoxx50 +0.1% at 3,599, FTSE +0.1% at 7,433, DAX closed, CAC-40 +0.2% at 5,359, IBEX-35 -0.1% at 10,245, FTSE MIB -0.2% at 22,777, SMI +0.2% at 9,258, S&P 500 Futures -0.05%

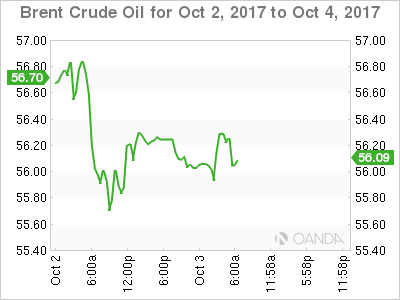

2. Oil prices fall on oversupply concerns, gold at seven week low

Oil futures have extended their losses after tumbling yesterday, as a rise in U.S drilling and higher OPEC output stalls the recent rally and rekindled concerns about oversupply.

Brent crude has slipped -0.4% to +$55.90 a barrel, after marking a third-quarter gain of about +20%, while U.S light crude (WTI) has fallen -0.3% to +$50.42.

Note: Iraq indicated yesterday that exports rose slightly last month from its southern oilfields, while a Reuters survey indicated that OPEC boosted output in the month.

Expect investors to take their cues from this week's inventory reports.

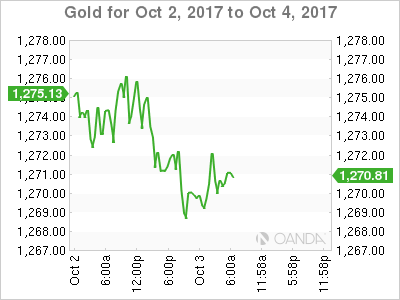

Ahead of the U.S open, gold trades atop of its seven-week low, as equities and the dollar remain somewhat buoyed by upbeat U.S economic data and stronger treasury yields. Spot gold is down -0.1% at +$1,269.71 an ounce.

3. Sovereign yields back up

Firming expectations that the Fed will hike rates in December coupled with domestic data pointing to steady growth in the U.S and talk of a potentially more hawkish successor to Fed Chair Janet Yellen is helping to push U.S yields higher.

Ten-year yields are trading atop of +2.35%; it's highest yield since mid-July, which has also pushed the dollar higher against G10 currencies.

Note: Speculation that President Trump could choose former Fed Governor Kevin Warsh, who is considered more 'hawkish' than Yellen, to replace her as head of the Fed.

Elsewhere, Germany's 10-year Bund yield has rallied +2 bps to +0.47%, while the U.K's 10-year Gilt yield has climbed +3 bps to +1.359%.

Note: The BoE has sent repeated signals that it is readying its first interest-rate increase in more than a decade as the U.K.'s looming departure from the E.U weighs on the economy. Fixed income dealers are pricing in a November hike.

4. Dollar remains better bid on rate differentials

A higher U.S yield again is providing support for the 'mighty' dollar across the board. Dealers are pricing in +70% odds that the Fed would resume rate hikes in December following a recent spat of stronger U.S data.

The EUR (€1.1742) trades atop of this week's lows, as divergence trades between the Fed and ECB remain intact. The pair had some technical resistance just above the psychological €1.2000 print last month, while short-term support is featured around €1.1700.

In the U.K, Sept PMI Construction data (see below) slipped into contraction territory for the first-time in 13-months and is providing some additional headwind for the pound (£1.3245).

Down-under, AUD is trading atop of its two-month low outright (A$0.7800) after the Reserve Bank of Australia (RBA) left interest rates unchanged and gave a cautious assessment of the local economy

5. UK construction PMI falls

There was more downbeat news on the U.K economy this morning as the purchasing managers' index on U.K. construction activity fell below the 50 level in September, marking contraction rather than expansion for the first time in 13-months.

The index dropped to 48.1 last month, from 51.1 in August. The market had expected the reading to remain above 50.

The headline fall is being attributed to a drop in new orders, with respondents reporting “fragile confidence and subdued risk appetite among clients, especially in the commercial building sector.”

Note: A lower construction PMI, which follows yesterday's smaller U.K manufacturing PMI, highlights concerns about a weakening U.K economy just as the BoE is expected to raise interest rates in November.

Euro Quiet As German Banks Closed For Holiday

The euro is almost unchanged in the Tuesday session, after starting the week with considerable losses. Currently, EUR/USD is trading at 1.1736, up 0.03% on the day. German banks are closed for a holiday, so we’re unlikely to see much movement from the pair during the day. The eurozone will release PPI, which is expected to post a weak gain of 0.1%. There are no major US releases on the schedule.

The Spanish region of Catalonia was a scene of chaos and violence on the weekend. The Catalan regional government attempted to hold a referendum on independence, but the national government was adamantly opposed to the move and banned the vote. When voters showed up at polling stations, the police moved in with force, injuring close to 900 civilians. Catalonian officials claimed that 90 percent of voters had voted for independence, setting the stage for a full-blown crisis with Madrid. The Spanish constitution prohibits any region from seceding, but Catalan Carles Puigdemont has not showed any intent to back down, and has called for a general strike on Tuesday. Although the euro lost ground on Monday, the crisis is not expected to continue to weigh on the currency, given that the referendum is viewed as an issue local to Spain, and not to the eurozone in general. As well, the Spanish economy is in good shape, so a constitutional crisis is unlikely to affect the country’s economic growth.

President Trump has set is sight on tax reform, but the tax proposal, called the Unified Tax Reform Framework, has been sketchy and short on specifics. Under the proposal, corporate tax would be lowered from 35 percent to 20 percent, and there would be deep cuts in personal income tax as well. However, it’s not clear how the government would pay for these cuts, with Trump saying that the cuts will trigger strong economic growth. Moody’s, the well-respected credit rating company, isn’t buying what Trump is selling. On Monday, Moody’s said that the tax plan is “likely credit negative”, arguing that tax cuts would not be offset in spending cuts, which would result in a higher federal budget deficit and debt. The reduction in federal government revenue would negatively affect the US credit rating. Some republican lawmakers have already come out against the plan, so it appears that the proposal will have an uphill battle to pass through the House of Representatives and the Senate.