Sample Category Title

Trade Idea: USD/CAD – Buy at 1.2285

USD/CAD - 1.2350

Trend: Down

Original strategy :

Bought at 1.2285, Target: 1.2450, Stop: 1.2225

Position: - Long at 1.2285

Target: - 1.2450

Stop: - 1.2225

New strategy :

Hold long entered at 1.2285, Target: 1.2450, Stop: 1.2225

Position: - Long at 1.2285

Target: - 1.2450

Stop:- 1.2225

Although the greenback retreated after meeting resistance at 1.2391, reckon downside would be limited to 1.2250-55 and bring another rebound, above 1.2345-50 would bring test of said resistance at 1.2391, break there would add credence to our view that a temporary low has been made at 1.2061 earlier this month, bring retracement of recent decline to resistance at 1.2425-30, then 1.2450, however, near term overbought condition should limit upside and reckon 1.2500 would hold from here, bring retreat later.

In view of this, we are holding on to our long position entered at 1.2285. Only below indicated support at 1.2197 would abort and signal top is formed instead, bring weakness to 1.2160-65, then towards support at 1.2121, break there would confirm the rebound from 1.2061 has ended and bring retest of this level later, We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our indicated downside target at 1.2100 and may extend to 1.2000.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Data Support Euro. Dollar Continues to Struggle

- European equities opened weak as Asian risk off sentiment carried over to EMU, but equities gradually went up, well into positive territory on the back of strong EMU PMI's. Later on, risk sentiment deteriorated again, helped by another Trump tweet, pushing equities back to yesterday's closing levels.

- Eurozone business activity accelerated to the strongest pace since May, putting upward pressure on prices, according to a survey that highlights the expectations that the European Central Bank will soon begin easing its bond buying programme. Composite PMI index rose to 56.7 in Sept., from 55.7 in August, the strongest gain in 6 years.

- Mario Draghi has made a fresh plea to eurozone governments to reform their labour markets and improve the prospects of young people, saying higher unemployment rates for younger workers had high costs for society. Mario Draghi was silent on policy-sensitive issues.

- San Francisco Fed Williams called rates still low in the US, could see another rate hike in December and expects gradual increases of rates in the next couple of years. However, everything depending how the economy fares. Williams, who did a lot of research on the natural rate, said 2.5% is the new normal for the long run or neutral rate.

- Uber's license to operate taxis in London was revoked, a surprise decision that will affect the 3.5 million people and 40,000 drivers who use the app in the city. If the decision stands, Uber appeals, it will have a considerable impact on the company's global business. London is one of Uber's most established markets.

- "The recent euro appreciation may have a more limited dampening effect on inflation than what would be implied by historical averages" based on recent research, ECB Vice President Constancio said .

Rates

German bonds underperform US Treasuries

US Treasuries eked out some gains in the Asian session, as risk-aversion linked to North-Korean nuclear test threats, dominated trading. They kept the gains, but moved sideways further out. The Bund opened higher, reflecting US Treasury gains, but soon slid lower as risk sentiment improved and EMU PMI business confidence largely exceeded expectations. It confirms the buoyancy of the euro area economy. The Bund bottomed even before noon and struggled higher to erase losses, maybe helped by declining equities. All in all, the bond moves are minor, but more than half of the post FOMC losses on Wednesday have now been recouped.

Central bankers gave a number of interesting comments that were however largely ignored. San Francisco Fed Williams is on board of the majority group inside the FOMC. He sees a rate hike this year as likely and calls current rates still low. He also expects gradual rate increases in the next years, but, most important, sees 2.5% as the new normal (meaning the long run or neutral rate). ECB Constancio said that the strong euro might have less impact on (lower) inflation than historical experience would suggest. This could be called hawkish coming from the dovish ECB vice chairman, as it lessen fears that QE tapering would push inflation lower via a stronger euro. Mario Draghi didn't touch sensitive issues in his speech and later today, we hear the views of Fed governors George (hawk) and Kaplan (rather dove).

At the time of writing, US yields decline between 0.7 bps (2-yr) and 2.7 bps (10-yr), while German yields are little changed (between flat and +0.5 bps). On intra-EMU bond markets, 10-yr yield spreads versus Germany are unchanged.

Currencies

Data support euro. Dollar continues to struggle

Dollar sentiment remained fragile as (geopolitical) uncertainty and a cautious risk-off mood deprived the dollar of highly needed interest rate support. At the same time, the euro was supported by very strong EMU PMI's. At the end of the day, the moves are modest. Still, the conclusion survives that the dollar fails to profited from the Fed's commitment to continue policy normalisation. This especially applies to EUR/USD. The pair trades in the 1.1975 area. USD/JPY hovers near the 112 big figure.

Overnight, risk sentiment soured in Asia. Press reports said that North Korea might retaliate on Trump's speech and trade measures, by testing a hydrogen bomb in the pacific. The renewed geopolitical tensions caused a modest risk-off repositioning. Asian equity indices declined, bonds gain and the yen outperformed. USD/JPY declined from the mid 112 area to trade in the high 111 area at the start of European trading. The dollar also declined slightly further against the euro. EUR/USD rebounded north of 1.1950.

European equity markets opened with modest losses, but the risk-off sentiment from Asia evaporated almost immediately. The EMU September PMI's were rock-solid with the composite PMI in France and Germany reaching a new cycle top. European yields rose slightly. A the same time, US yields maintained a tentative downward bias. EUR/USD rebounded to the psychological barrier of 1.20, but a sustained break didn't occur. The dollar even regained some ground towards the end of the European morning session. EUR/USD dropped back to the 1.1960/75 area. USD/JPY tried to regain the 112 big figure. ECB's Constancio said that the appreciation of the euro may have a more limited dampening impact on inflation than what would be implied by historical averages, but the euro hardly reacted.

Early in the US, president Trump reacted sharply to the overnight 'threats' from North Korea. There was no immediate market reaction, but risk sentiment gradually deteriorated as US trading developed. For now, the negative impact on the dollar remains modest. EUR/USD trades in the 1.1970 area. USD/JPY hovers around 112.

Sterling under pressure at the start of May's speech

During the morning session, sterling was at the mercy of the broader swings in the euro and the dollar as UK markets awaited UK PM May's Brexit speech in Florence this afternoon. EUR/GBP drifted higher as the euro was well bid after the strong PMI's. The pair filled offers just below 0.8850. Cable lost a few ticks on overall USD softness. However, at start op PM May's Brexit speech, intraday changes were limited. CBI trends orders were softer than expected but ignored. PM May's Brexit speech is still ongoing at the moment of writing. She only brought some general considerations on the relationship between the EU and the UK. For now we didn't see much concession from May. Sterling is losing ground as the speech proceeds, but this can still change when May addresses more concrete issues on the Brexit process. EUR/GBP trades currently in the 0.8860 area. Cable trades in the 1.3515 area.

Canadian Inflation Ticks up in August

The all-items consumer price index for August ticked up to 1.4% on a year-on-year basis in August (July:1.2% y/y). On a month-on-month, seasonally adjusted basis, prices rose 0.1%, the first increase since this past May.

Goods prices rose 0.4% y/y, largely driven by an uptick in energy and food prices. The average price of services rose 2.2% y/y.

Two of the Bank of Canada's measures of underlying inflation rose in August. Both CPI-trim and CPI-common rose by a tenth of a percentage point to 1.4% and 1.5% respectively, while CPI-median held at 1.7% on a year-on-year basis.

Key Implications

Today's inflation data remains broadly consistent with our outlook for consumer price growth in the third quarter. The uptick in goods prices is likely to be more pronounced in September due to the spike in gasoline prices in the aftermath of hurricane Harvey, and there may be some upward pressure on fresh foods and vegetables later this year related to the damage that hurricane Irma has wrought upon Florida's agricultural industry. However, the strong advance in the Canadian dollar should begin to exert downward pressure on goods prices in the months ahead.

An uptick in underlying inflation is somewhat encouraging and suggests that inflation may have stabilized in the last couple of months. Overall, this report will do little to change how the Bank of Canada is seeing the Canadian economy as evolving in the medium term. Underlying inflation pressures have risen a touch, consistent with the need to remove some monetary accommodation and may justify the two 25 basis point interest rate increases in the span of six weeks. Although the loonie is expected to exert a drag on goods prices in the months ahead, the Bank of Canada should continue to see through these tempoary factors as yet another quarter of robust economic activity is likely in 17Q3, eliminating even more slack and suggesting the need for tighter monetary policy.

Canadian CPI Inflation Shows More Signs of Stabilization in August

Highlights:

- The year-over-year rate of headline CPI inflation rose to 1.4% from 1.2% in July - largely because of an increase in energy prices.

- 2 of 3 of the Bank of Canada's preferred 'core' measures ticked higher

- Year-over-year price growth excluding food & energy prices held steady at 1.5%.

Our Take:

There were further tentative signs in August that the puzzling recent underperformance of Canadian inflation measures is gradually coming to an end. To be sure, most of a pop higher in the year-over-year headline inflation rate to 1.4% in August was the result of higher gasoline prices - and the rate itself is still well-below the Bank of Canada's 2% inflation target. The year-over-year rate excluding food & energy products held steady at 1.5% after posting its first increase in six months in July but two of the Bank of Canada's preferred 'core' inflation measures-the CPI-trim and CPI-common - ticked up slightly with the third - the CPI-median - holding steady at a stronger 1.7%. Perhaps more telling, the underperformance in those core measures on a year-over-year basis seems to have been concentrated earlier in this year. Our calculations suggest the month-over-month increases in the CPI-trim and CPI-median rates, for example, have both averaged over a 2% annualized rate over the last three months. That is the first time that has happened since June 2016.

It remains difficult to argue that the underperformance of core measures of inflation over the last year in Canada is related to a lack of consumer demand given strong household spending and what look like relatively tight labour markets. That suggests other likely transitory, but frustratingly difficult-to-identify, factors have been at play. Today's report provides tentative evidence this underperformance is easing, consistent with our view that price growth closer to the Bank of Canada's 2% target will gradually reassert itself. We expect that will allow the Bank to continue to hike rates at a gradual pace to lean against strong economic growth, even if current inflation pressures aren't yet forcing policymakers' hands.

Canadian Retail Spending Took a Breather in July

Highlights:

- Nominal retail sales rose 0.4% in July, but removing the impact of prices, the volume of sales edged down by 0.2%.

- Higher auto sales and stronger spending at food retailers led the nominal increase.

- E-commerce sales (not all of which are included in the retail sales totals) were up 47% year-over-year in July though their share of retail trade is just 2.3%.

Our Take:

Today's lukewarm retail sales report showed a modest, price-driven increase in retail sales with volumes edging slightly lower. The pause in July is hardly concerning given the robust gains in recent months that drove year-over-year volumes growth to a decade-high in June. Strength in the retail sector is consistent with impressive job gains over the last year, although an uptick in consumer credit which is now growing at its fastest pace since 2011 was also a factor. Canada's recent pace of consumer spending growth—annualized gains of nearly 5% over the first half of this year—looks unsustainable, and with GDP growth now better balanced by other areas like business investment, we think further gradual removal of monetary policy accommodation is in order. We expect the Bank of Canada will raise interest rates once more by the end of the year following consecutive moves in July and September.

Today's retail sales report follows yesterday's solid increase in wholesale trade and a more mixed set of manufacturing data on Monday that showed a narrowly-based decline in shipment volumes. On balance, we think this week's data point to a more modest 0.1% increase in July GDP following solid gains of 0.3% and 0.6% in the prior two months. Even with a slower start to the quarter, we continue to look for an above-trend 2.5% annualized increase in Q3 GDP.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.17; (P) 112.44; (R1) 112.75; More...

Intraday bias in USD/JPY remains neutral at this point. Further rally is in favor as long as 111.07 support holds. Sustained break of medium term channel resistance (now at 113.03) will argue that whole correction from 118.65 has completed too. In that case, further rise should be seen to 114.49 resistance for confirmation. However, break of 111.07 minor support will raise the risk of rejection from channel resistance and turn bias back to the downside for 55 day EMA (now at 110.58).

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9617; (P) 0.9667; (R1) 0.9747; More....

Intraday bias in USD/CHF remains neutral for the moment. On the upside decisive break of 0.9772 resistance will suggest that whole down trend form 1.0342 has completed. In that case, near term outlook will be turned bullish for 0.9860/1.0099 resistance zone. Nonetheless, with 0.9772 resistance intact, outlook remains bearish. Below 0.9587 minor support will turn bias back to the downside for 0.9420 low.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

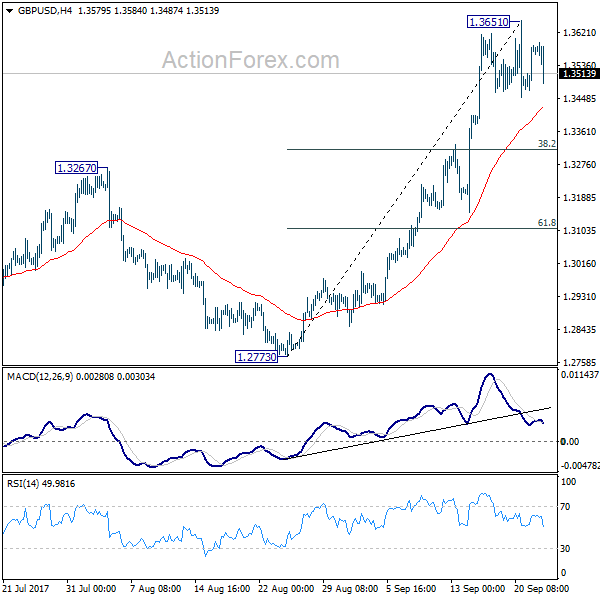

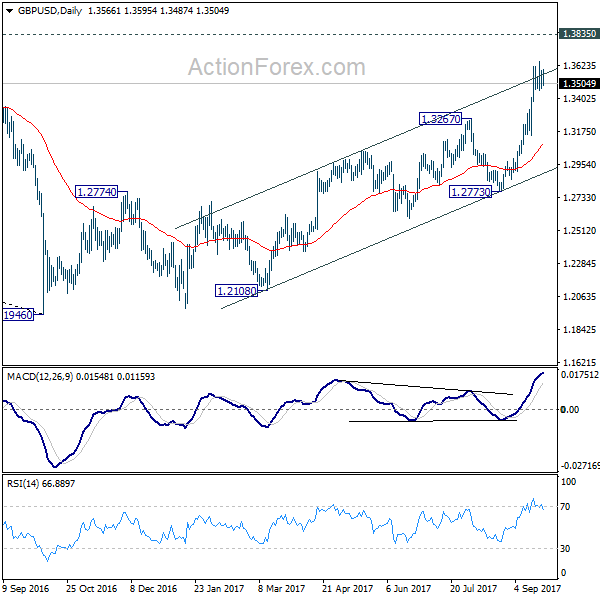

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3505; (P) 1.3546; (R1) 1.3621; More....

Intraday bias in GBP/USD remains neutral as consolidation from 1.3651 continues. In case of deeper fall, downside should be contained by 38.2% retracement of 1.2773 to 1.3651 at 1.3316 and bring rise resumption. Above 1.3651 will turn bias back to the upside for 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405).

In the bigger picture, the strong break of 1.3444 key resistance now argues that the long term trend in GBP/USD has reversed. That is a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

Canada: Retail Sales Up in July on Strength in Autos

Retail sales in Canada rose in July, up 0.4% month-on-month, although slight downward revisions to the June figures broke what would have been a five month streak of increased spending. July's gains were entirely due to price increases however, as volumes declined 0.2%.

The two largest spending categories, motor vehicle and parts dealers (+0.8%) and food and beverage stores (+0.9%) saw solid increases in July. Offsetting these somewhat were declines in the furniture and home furnishings (-0.6%), electronics and appliances (-0.2%), and building material and garden equipment (-0.2%) categories. Sales elsewhere were generally up. Excluding car/parts dealers and gasoline sales, retail sales growth was a tick lower, at 0.3%.

Across the provinces, it was Quebec that drove the result, as sales rose 1.0% in July. Saskatchewan (+1.3%) and British Columbia (+0.7%) also saw decent sales growth, with the latter recording a 5th straight month of gains. Sales growth across the remaining provinces was mixed.

Key Implications

Canadians seem to have celebrated Canada Day by heading to a car dealership as new vehicle sales helped drive a respectable climb in retail sales in July. While the volume of goods sold was down a tick, the broader data evolution remains consistent with a healthy pace of GDP growth over the back half of the year.

Indeed, as discussed in our latest Quarterly Economic Forecast, consumer spending is likely to moderate from the hot pace seen at the start of the year. But, it is expected to remain an important driver of growth, supported by rising aggregate incomes generated by a healthy labour market.

With the July data likely to only partially reflect the impact of tighter monetary policy, today's data will likely be discounted somewhat as the Bank of Canada assesses the impacts of its actions. That said, with robust July wholesale trade figures released yesterday, and a modest uptick in inflation also reported this morning, the data continues to support further monetary tightening in the final quarter of the year.

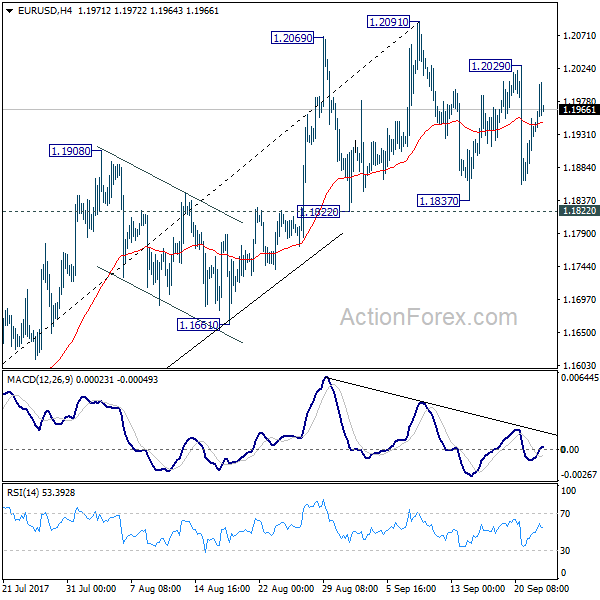

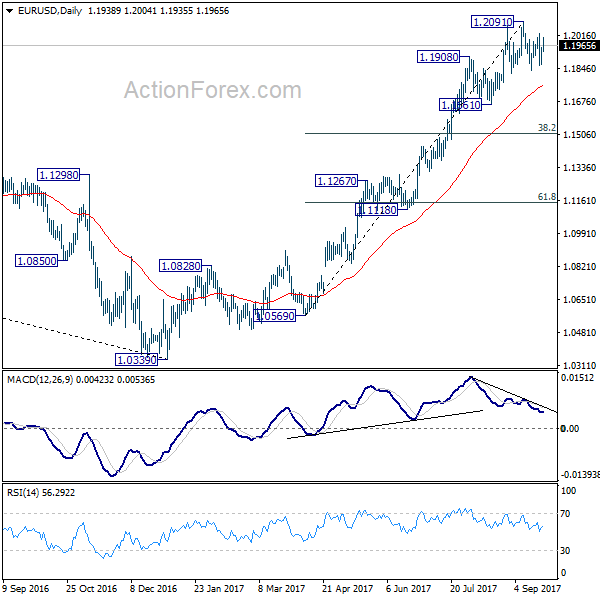

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1886; (P) 1.1919 (R1) 1.1974; More...

EUR/USD is bounded in range of 1.1822/2091 so far and intraday bias stays neutral. Considering bearish divergence condition in 4 hour and daily MACD, break of 1.1822 should confirm near term reversal. In the case, intraday bias will be turned back to the downside through 1.1661 support. EUR/USD should then correct whole rise from 1.0569 and target 38.2% retracement of 1.0569 to 1.2091 at 1.1510. However, rebound from 1.1822/1837 and break of 1.2029 will resume the larger up trend to next key fibonacci level at 1.2516.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall fro 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.