Sample Category Title

Weekly Market Outlook: Elections in Germany & New Zealand, RBNZ Meeting, Key Data in Focus

Next week's market movers

- In Germany, voters will elect their new Chancellor. On the vote, we see the case for a relief bounce in European assets if Merkel is the winner as anticipated, though any major reaction may only occur towards the end of October, when the coalition-making process begins.

- New Zealand will hold its General Election as well. A victory by the incumbent National Party could support the Kiwi, whereas a potential Labor win could weigh on the currency, we think.

- The RBNZ is expected to stand pat. We don't expect any major change in language, given the lack of developments since the latest meeting.

- We also get key economic data from Germany, the Eurozone, Japan, and the US.

Important events start earlier next week, as on Saturday, New Zealand will hold its General election. Most opinion polls suggest a very tight race between the incumbent National Party and the Labor party. Judging from how the Kiwi has reacted to opinion polls so far, a victory by the National Party would probably prove beneficial for the currency, whereas a potential win for the Labor Party could weigh on NZD. We believe this is the case mainly to the different stances these two main parties hold on trade policy. The Nationals largely represent the status quo and advocate continued free trade. On the other hand, Labor officials have noted in the past that they are open to renegotiating trade deals such as the Trans-Pacific Partnership (TPP). Considering how heavily reliant New Zealand is on international trade, such a renegotiation could potentially hurt exporting firms and thereby, slow down the economy.

Subsequently on Sunday, Germany will hold its own Federal Election. Unlike the bloc's recent elections in the Netherlands and France, this battle appears to be more traditional in nature, with the two main parties holding very similar views on key issues. According to almost every opinion poll, another victory by incumbent Chancellor Merkel is perceived as certain. As such, we believe that the market reaction on the actual vote may be relatively limited, with risks tilted towards a small relief bounce in the euro and European stocks in case Merkel wins as expected.

We believe that any major market reaction in the aforementioned asset classes may result from who Merkel chooses to align herself with, something that will become clearer towards the end of October. The political alliance she forms could determine whether much-needed EU reforms will materialize, such as the creation of a position for an EU Finance Minister, a shared euro-budget, and further banking sector integration. All of these would likely be seen as steps towards the creation of a fiscal union in Europe that would accommodate the monetary one. In our view, any signs that such positive reforms may be looming could lead investors to fundamentally re-evaluate European assets, and by extension, the euro itself.

Turning back to Germany, a continuation of the "Grand coalition" between Merkel's CDU with the SPD, Germany's second largest party, is likely to be the most market-friendly outcome, considering the SPD's pro-EU stance. This could spell further good news for the common currency, and quite possibly for major European equity indices. On the other hand, a coalition that does not include the SPD, but for example includes the FDP that is against the aforementioned EU reforms, could be perceived as a negative for European markets and the euro, we think.

On Monday and Tuesday, we have no major events or indicators on the economic agenda. Market participants may still be digesting the outcomes of the aforementioned elections.

On Wednesday, during the early Asian morning, the RBNZ will announce its policy decision. At its latest gathering, the Bank acknowledged that CPI inflation softened in Q2, but noted that it is still within the target range. Importantly, officials kept the timing of their first planned rate hike unchanged for Q1 2020, while they expressed discomfort about the up-until- then strength of the Kiwi. On top of that, in the aftermath of the decision, Governor Wheeler said that the option of FX intervention is always open. Since that gathering, we did not get much in terms of economic developments. The only point worth mentioning is that the Bank's 2-year inflation expectations for Q3 slid somewhat. This combined with the fact that the Kiwi is trading more or less at the same levels it was trading back then make us believe that the Bank is likely to remain on hold once again and make very few changes to its language.

As for the Bank's first rate increase, according to New Zealand's OIS, the market continues to anticipate that to happen in Q3 2018, much earlier than the Bank's own forecasts. Another round of concerns over the exchange rate, especially more intervention warnings, could convince the market to push back its hike expectations. Having said all these, the gathering is scheduled just a few days after the nation's elections. Given that the forthcoming direction of the Kiwi may be primarily determined by the election outcome, we think the Bank's gathering may attract less attention than otherwise.

Turning to the economic indicators, in the US, durable goods orders for August are coming out. The consensus is for the headline orders to have rebounded after falling sharply in July, while the core rate is forecast to have declined. The core forecast is supported by the nation's ISM manufacturing PMI for the month, where the New Orders sub-index ticked down. The strong rebound in US civilian aircraft orders, on the other hand, supports the case for a rise in the headline rate. On balance, the market may place more emphasis on a potential decline in the core rate.

On Thursday, Germany's preliminary CPI for September is due out, one day ahead of Eurozone's print. The forecast is for the CPI rate to have ticked up, and to be exactly in line with the ECB's mandate of below, but close to 2%. The forecast is supported by the nation's preliminary Markit composite PMI for the month, which showed another strong rise in prices charged for goods and services. An acceleration in German inflation could raise speculation for a similar reaction in the bloc's overall print.

Finally on Friday, during the Asian day, Japan's CPIs for August are due for release. Without a forecast available, we see the case for both the headline rate and the core rates to have risen. We base our view on the nation's forward-looking Tokyo CPIs for August, where both the headline and the core rates rose. Even though something like that would probably be further encouraging news for BoJ policymakers, we maintain our view that as long as inflation remains so far away from the 2% inflation target, the Bank is unlikely to alter its QQE with yield-curve control framework. Under this framework, the BoJ has committed not only to achieving 2%, but to actually overshoot it.

During the European morning, Eurozone's preliminary CPI data for September are coming out, though no forecast is available yet for either the headline or core rates. We see the case for both rates to have risen somewhat further, something that we base on the bloc's preliminary composite PMI for September, which showed selling price inflation reaching its highest rate since April. Further uptick in these rates would probably be pleasant news for ECB policymakers, who are set to provide some clear details about the future of QE at their upcoming October meeting. Moving forward, we think that market focus will be on whether the Bank will proceed with a "dovish tapering", whereby it begins to reduce its monthly purchases without setting a clear roadmap for ending the programme completely.

From the US, we get personal income and spending, as well as the core PCE price index, all for August. Getting the ball rolling with income and spending, both of these rates are forecast to have declined from the previous month. The income forecast is supported by the slowdown in the nation's average hourly earnings for the month, while the decline in retail sales suggests that the spending rate may even turn negative. Turning to the core PCE index, in the absence of a forecast, we see the case for the rate to have remained unchanged. We base our view on the core CPI rate for the month, which held steady at +1.7% yoy.

Week Ahead – US Data and Fed Speakers to Dominate; Limited Risk Seen from German Elections

Election results from Germany and New Zealand will occupy market headlines at the start of the trading week, assuming there is no fresh escalation of geopolitical tensions by North Korea. US economic indicators will dominate much of the week, but Japanese and Eurozone inflation data and the Reserve Bank of New Zealand's monetary policy meeting will also be in focus. The Federal Reserve will also be attracting headlines as several policymakers hit the podium.

Few surprises expected from German election

Germany will likely elect Angela Merkel as Chancellor for a fourth term on Sunday as the nation heads to the polls. Some upsets should not be totally discounted however as far-right parties might still make significant gains and Merkel might need to seek new partners to form a government if the SPD party pull out of the current grand coalition with the CDU/CSU.

Investors have so far shown little concern about Sunday's outcome and will probably focus more on next Friday's flash inflation readings for the Eurozone. Inflation is forecast to remain at 1.5% year-on-year in September, with core inflation expected to slip to 1.2% from 1.3%. Other Eurozone data next week will include the Ifo business survey out of Germany on Monday and the Eurozone economic sentiment index on Thursday. Both the Ifo business climate index and the economic sentiment gauge are forecast to edge marginally lower in September. A slight drop in business sentiment is unlikely to alter expectations that the Eurozone economy is on track to have another strong quarter in the three months ending September, especially after this week's stronger-than-expected IHS Markit PMIs. However, a weaker inflation figure could weigh on the euro.

Japan inflation to inch higher amid dovish dissent at BoJ

Data out of Japan next week is unlikely to see much of a reaction in forex markets, but will nevertheless be important as inflation is expected to edge further up to reach a more than two-year high. Starting the week though will be the Nikkei flash manufacturing PMI for September, due on Monday, with the rest following on Friday. Friday's data will include household spending, retail sales, industrial output and jobs numbers, along with the latest CPI figures. Household spending is expected to decline for the second straight month in August, but retail sales are forecast to show a 2.6% annual gain during the period, up from 1.9% in July. The unemployment rate is expected to hold steady at 2.8% in August, while industrial output is seen rebounding 1.9% month-on-month in August's preliminary reading. The more closely watched indicator will be inflation. Core CPI, which excludes fresh foods, is forecast to rise from 0.5% to 0.7% y/y, moving further away from zero but still some distance from the Bank of Japan's 2% target.

Also grabbing attention will be the BoJ's summary of opinions of the September policy meeting on Friday. The September meeting this week saw one of the two new board members dissenting in favour of looser policy. With the Bank's remaining two hawkish policymakers now having departed, a dovish tilt shouldn't be too surprising. However, any sign of other members becoming more concerned about the delay in hitting the inflation target could push the yen lower.

Election risk for New Zealand dollar

After an unexpectedly tight election race, the outcome of New Zealand's general election on September 23 has become a highly anticipated event. The prospect of a win for the opposition Labour party dragged the New Zealand dollar to multi-week lows at the beginning of September due to the uncertainty posed by Labour's economic policies. However, a recent recovery by the ruling National party, which are now narrowly ahead in the polls, has helped the kiwi recoup some of its losses. Another risk for the kiwi next week is the policy meeting by the Reserve Bank of New Zealand.

Thursday's meeting will be the last for the Governor, Graeme Wheeler, whose replacement has not been decided yet due to the timing of the elections. The RBNZ is expected to hold rates unchanged at a record low of 1.75% and will likely maintain its neutral bias, especially after this week's somewhat disappointing second quarter GDP data. In terms of data, August trade figures will be watched on Monday.

Round four of Brexit talks eyed

British prime minister, Theresa May, is hoping to break the deadlocked Brexit talks with her speech in Florence, Italy today. Expectations will therefore be high that more substantial progress will be made on key issues when the fourth round of negotiations resume on Monday. The pound could lose some momentum if the negotiations fail to produce any concrete results.

In the meantime, investors will be looking for a possible upward revision to the second quarter GDP data, due on Wednesday, while mortgage and consumer lending figures on Friday may also attract some attention given the Bank of England's concerns about rising household debt and with a looming rate hike in November.

Fed speakers under the spotlight after hawkish FOMC meeting

It will be a busy week for the US economic calendar with a number of key data releases. First up is housing data on Tuesday, consisting of the S&P CoreLogic Case-Shiller 20-city house price index (July) and new homes sales (August). Also on Tuesday is the Conference Board's consumer confidence index, which is forecast to fall from 123 to 120.6 in September. There will be more housing data on Wednesday with pending home sales, while August's durable goods orders are also released the same day. Durable goods orders are expected to rebound by 1.5% m/m in August after plummeting by 6.8% in the prior month. On Thursday, the final estimate of second quarter GDP growth is forecast to remain unrevised at 3%. On Friday, the personal consumption expenditure (PCE) data will be watched closely, and the Chicago PMI is also released. Personal income is expected to rise by 0.2% m/min August, half the rate of July, and personal consumption is forecast to increase by just 0.1%, also down on the prior month's rate. The Fed's preferred measure of inflation, the core PCE price index will likely remain unchanged at 1.4% y/y in August.

The Fed is so far maintaining its view that this soft patch in inflation is temporary and still foresees one more rate hike by year end despite increased concerns by some FOMC members. The renewed expectations of a third rate rise following this week's FOMC meeting have lifted the US dollar, though many market participants remain unconvinced by the Fed's optimistic rate hike path. Fed officials will get the chance to clarify their latest quarterly economic projections in a series of public appearances over the coming week, the most important of which will be Chair Janet Yellen's address at an economic conference in Cleveland on September 26.

Dollar Under Pressure after Trump’s Tweet on N. Korea; Pound Weaker Despite May Rejecting Options of Leaving EU Earlier

The latest war of words between Trump and the North Korean leader Kim Jong Un kept markets nervous during the European session, with the dollar being unable to restore Wednesday's gains when the FOMC statement signaled the start of the balance sheet reduction in October and more strongly put on the table an additional rate hike later in the year. However, the Brexit speech by the UK Prime Minister Theresa May was in the spotlight during the European session with the pound sinking during the first minutes of the speech as sources reported that May would raise the odds for Britain leaving the EU before the determined date.

After the North Korean leader, Kim Jong Un, expressed his intention early on Friday to use "the highest level of hard-line countermeasure in history against the US", Trump responded with a strong language through social media, commenting that the North Korean leader "would be tested like never before". This escalated geopolitical tensions even further, with investors turning to safer-perceived investments.

Despite the dollar index being pressured during the day, it managed to edge up to 91.84 from an intra-day low of 91.54 touched earlier in the session after the San Francisco Fed President John Williams (a non-voting FOMC member) said that the economy is in a strong shape as it is close to its unemployment and inflation goals as has never been before. Though he added that interest rates would be easily reduced in case of negative economic shocks.

Dollar/yen was down by 0.54% on the day at 111.88 amid heightened geopolitical uncertainties while dollar/swissie fell by 0.24% to 0.9683.

Gold gained 0.50% on Friday, jumping to $1,297.40 per ounce.

The September Markit flash estimate of US manufacturing PMI was released in line with expectations at the two-month high of 53.0. The figure for August stood at 52.8. The respective number for the services sector came in at the two-month low of 55.1, below analysts' forecasts for a reading of 55.9, as well as below August's 56.0. Both readings remained in expansion territory above 50.0, showing "encouraging resilience in a month of hurricane disruption" according to IHS Markit Chief economist Chris Williamson. He added that "the surveys point to the economy growing at an annualized rate of just over 2% in the third quarter". The September flash composite PMI, which blends both the services and manufacturing sectors retreated to 54.6 in September from August's 55.3. Dollar/yen declined, though not by much, as the data went public.

The euro jumped to $1.2002 following Eurozone's upbeat flash PMI readings for the month of September but tumbled back to $1.1960 after the dovish remarks by the ECB Chief Mario Draghi.

The Eurozone IHS Markit composite PMI surprisingly bounced back to a multi-year high of 56.7, surpassing the 55.5 that was expected. The manufacturing PMI improved by 0.8 points to 58.2 which was the highest level seen since February 2011, while the services PMI increased by 0.9 points to 55.6.

The ECB Chief Mario Draghi said that real economic activity could complicate price monitoring. Visiting Dublin Trinity College, he admitted that price stability in the Eurozone has not been achieved yet as inflation remains subdued below the central bank's 2% target. Other ECB speakers could not provide support to the euro either, with the ECB Vice President Benoit Coeure claiming that the increasing usage of the euro by the Balkan countries may "put the economy at risk due to exchange rate shifts". A few hours later, Vitor Constancio, an executive member at the ECB said that the weak correlation between inflation and real economic activity would complicate price monitoring.

Next up, the markets will focus on the outcome of the German federal elections on Sunday where traders anticipate a victory for the Chancellor Angela Merkel. If results follow expectations, then Merkel will be in power for the fourth consecutive term.

Meanwhile, in Florence, the UK Prime Minister, Theresa May was delivering her landmark speech on her plans for the country's exit from the EU. During her public appearance, May proposed a two-year transition period while she also said that the UK will respect its budget commitments made throughout its EU membership. Moreover, she argued that Britain would do better if an agreement similar to that of the European Economic Area membership or to the free trade deal made recently with Canada would emerge.

Nevertheless, the pound failed to find support on May's remarks as the currency slumped by 0.70% to a session low of $1.3487 after a report from the Telegraph newspaper spread fears that May would raise the potential of leaving the block before March 2019. Though, in a QA session, May said that Britain would exit the EU at the end of March 2019.

In Canada, headline inflation missed expectations in August with the CPI rising by 1.4% y/y (0.1% m/m), below the 1.5% forecasted (0.2% m/m) after it rose by 1.2% in July. The core equivalent measure remained steady at 0.9% y/y (0.0% m/m vs -0.1% m/m in July). Regarding July's retail sales, those came in higher than projected, increasing by 0.4% m/m, while analysts anticipated the figure to stay flat at June's reading of 0.1%. However, excluding automobiles, household spending fell short of expectations, growing by 0.2% m/m, below the forecast of 0.4%.

In response to the data, the loonie posted moderate gains, with dollar/loonie edging down to 1.2307. Rising oil prices during the session also gave some support to the currency.

Dollar/kiwi was up by 0.34% on the day ahead of the general elections in New Zealand on Saturday.

Looking at energy markets, oil prices moved up while OPEC members Kuwait, Venezuela and Algeria as well as Russia and Oman who are not members of the organization were gathering in Vienna to discuss on possible supply reductions beyond March of next year. While in Vienna, oil ministers signaled the potential to extend the agreement well into 2018 with the Kuwait Minister who was chairing saying that since July's meeting the oil market has "markedly improved". Moreover, the Russian Minister mentioned that exports, which are not restricted so far, would also gather attention but the focus would be mostly on production levels. Though, some OPEC sources claimed that any suggestions on extensions are less likely to be made at the end of the meeting with the committee probably making recommendations in November when a wider group of OPEC and non-OPEC oil producers will meet.

The US Baker Hughes Oil Rig Count will be released at 1700 GMT. Also, Dallas Fed President and FOMC voting member Robert Kaplan is scheduled to participate in a Q&A session at the Conference titled "Global Oil Supply & Demand: Prospects for Greater Balance" in Dallas at 1730 GMT.

Australia & New Zealand Weekly: New Zealand Goes to the Polls

Week beginning 25 September 2017

- RBA on hold in 2017, 2018 and 2019.

- RBA: Deputy Governor Debelle and Assistant Governor Bullock speak.

- Australia: private sector credit.

- NZ: RBNZ policy decision, building consents, business confidence.

- China: national & Caixin PMIs.

- US: Fed chair Yellen speaks, PCE inflation, GDP 3rd estimate.

- Central banks: ECB's Draghi, BOE's Carney, BoC's Poloz speak.

- Key economic & financial forecasts.

Information contained in this report was current as at 22 September 2017.

RBA on hold in 2017, 2018 and 2019

Markets have moved to price in three hikes for the RBA's cash rate by end 2019. Other major banks concur broadly with that view.

Recall that in mid-August last year, these same players (markets and most other banks) were forecasting rate cuts over the course of the remainder of 2016 and 2017. Westpac's view at that time was "rates on hold" in 2016 and 2017.

Readers of the Westpac Market Outlook publication for September will be aware that Westpac continues to forecast the cash rate to remain on hold out to mid-2019.

Indeed we are not convinced that the cash rate will need to rise any time throughout the course of 2017, 2018 or 2019.

This approach is clearly different to the thinking of the Reserve Bank Governor himself who expects to be tightening over that period (note his speech on "the next chapter" which was delivered yesterday).

However, we continue to point out that the RBA has a very different growth outlook for the Australian economy and Australia's trading partners to our own.

The RBA expects growth in Australia to be 3.25% in 2018 and 3.5% in 2019 (above trend of 2.75%). Westpac expects a below trend pace of 2.5% in both years.

The RBA is also forecasting 2% underlying inflation in 2017 and 2018 (bottom of target band) to be followed by 2.5% in 2019. Underlying inflation is currently running at 1.8% (to June) and the upcoming revised weights are likely to reduce annual underlying inflation by 0.2-0.3%.

Going forward, the RBA's inflation forecasts also look to be overly optimistic and are likely to be subject to downward revision. Recall that in 2016 when the RBA was forced to revise its inflation forecasts below 2% it believed it had little choice but to cut rates.

While the RBA does not provide detailed forecasts outside growth and inflation, comments from the RBA Governor and written reports point to a much more confident outlook for wages growth; incomes; employment; consumption; non-mining investment and the residential construction cycle.

The Reserve Bank expects wages growth to increase over the forecast period. A major puzzle for central banks globally has been the limited response of wages to stimulatory monetary policies since the GFC. Despite these policies in the US; Germany; the UK and Japan driving labour markets to near or full employment, wages have failed to respond. Explanations for this phenomenon have been structural: globalisation; technology; retiring higher paid baby boomers; low productivity growth; absence of pricing power for employers; low inflationary and wage expectations; high risk aversion following the GFC and job insecurity.

Consistent with that global theme, wages growth in Australia has also been weak. Australia's wage price index has increased by 1.9% over the last year compared to average growth of 3.5%. The unemployment rate has held in the 5.5%-6.0% range compared to a generally accepted full employment rate in Australia of 5%.

Further, underemployment in Australia has been high at around 8.8% making total excess capacity around 14.5%. Given the global lessons on the structural wages outlook, it seems unlikely that wages in Australia (where spare capacity is higher than in these other developed economies) will lift significantly even in the medium term.

This weak wages performance has lowered annual real income growth to 0.6% while real consumption growth has held around 2.5%. The shortfall has been funded by a falling savings rate, particularly in the highly stressed mining states. Overall Australia's household savings rate has fallen from 9% to 4.6% over the last three years.

Households will need to protect that fragile savings rate and pressures will emerge on consumer spending. Of course, other pressures are impacting households - rising energy prices; record high debt levels and political uncertainty. The latter effect will work through the business sector as businesses restrain employment and investment until political clarity is achieved following the 2019 election.

Markets may be underestimating the impact on the interest rate sensitive housing market of developments which are unfolding without official rate hikes.

The four majors (90% of the mortgage market) have been raising investor and interest only mortgage rates while applying tighter lending guidelines. House price inflation is slowing and regulators are unlikely to have any patience with a reversal of this trend.

To that point, six month annualised house price inflation (CoreLogic data) in Sydney has slowed from 22.4% in January to 4.8% in August. We observed a similar response to macroprudential policies in 2015/16 when six month annualised house price inflation slowed from 25% (July 2015) to -4.4% (April 2016).

Housing activity is also slowing despite a steady cash rate. Other factors, specifically relating to foreign investors, have turned the cycle. High rise building approvals have tumbled by 40% in the last year. This has been particularly due to investment restrictions in China; lending constraints by banks; and sharp increases in state government stamp duties for foreign investors. This downturn is likely to continue for at least a further two years.

While markets are currently captivated by expectations of a coordinated lift in global growth, we are more circumspect particularly around Australia's trading partners.

With Chairman Xi likely to cement power following the National Congress in October, we expect that he will have little choice but to adopt policies to gradually deal with the excessive build up in corporate debt in China (now 166% of GDP), largely driven by the circa 30% compound growth rate of small and medium sized banks and non-banks over the last six years. These small banks now represent comparable asset bases to the heavily regulated policy banks which have only been growing at around 12% over the same period. It will be incumbent on the administration to arrest the growth rate of these small banks; off balance sheet vehicles; and non-bank institutions. Asset quality for these institutions must be suffering while reliance on overnight funding has lifted sharply.

Tighter credit conditions will slow China's growth rate - we forecast a growth slowdown from 6.7% in 2017 to 6.2% in 2018.

Finally, the ongoing legacy of elevated risk aversion, which continues ten years after the Global Financial Crisis, is contributing to unusually steady interest rates around the world. Under our figuring, on the basis that this risk aversion persists for a few more years, a 40 month stretch of steady rates in Australia would not be out of place.

Bill Evans, Chief Economist

Data wrap

Aug Westpac-MI Leading Index

- The six month annualised growth rate in the Westpac- Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, slipped from -0.04% in July to -0.19% in August.

- The growth rate remains negative for a third consecutive month pointing to below trend momentum and a sharp turnaround from strong positive, above trend reads at the start of the year.

- While the Index only gives us a glimpse of the likely momentum in the first few months of 2018 it currently seems to be more consistent with our view of the likely growth environment next year than the Reserve Bank's forecast for growth comfortably above trend. Westpac is currently forecasting growth of 2.5% in 2018 compared to the RBA's 3.25%. Trend growth is generally assessed as 2.75%.

- The Leading Index growth rate has slowed from 1.13% above trend in March to 0.19% below trend in August, a deterioration of 1.32ppts. Two components account for almost all of the reversal: commodity prices (-1.31ppts) and the yield spread (-0.43ppts). After surging nearly 40% over the second half of 2016, the RBA's AUD commodity price index has retraced nearly 12% in 2017 to date. Similarly, after widening by over 100bps in 2016, the yield gap - the difference between the 90day bill rate and the 10yr bond rate - has narrowed by about 12bps, pointing to more subdued market outlook for economic conditions.

- The contribution from other index components has been more mixed. On the positive side, the index growth rate has been boosted by: dwelling approvals (+0.27ppts); aggregate monthly hours worked (+0.26ppts); and the Westpac-MI Unemployment Expectations index (+0.09ppts). However, these improvements have been partially offset by a bigger drag from the S&P/ASX 200 (-0.22ppts) while other components have been largely unchanged.

New Zealand: Week ahead & Data Wrap

New Zealand goes to the polls

New Zealand's general election will be held on Saturday 23 September. It's looking like a close race between the two major parties - the incumbent centre-right National party and the main centre-left opposition Labour party. And even after the votes are counted on Saturday night, it could be some time before we know the final make-up of the next government. Neither of the two major parties looks likely to win an outright majority of votes. As a result, they are both likely to need the support of at least one of the minor parties to form a government. Negotiating the necessary support agreements could take some time, potentially several weeks. On top of this, counting of special votes (such as those votes cast outside a voter's usual electorate) could take another couple of weeks. We've seen in the past that this can have an important impact on the distribution of seats in Parliament, especially for the smaller parties. We'll provide more colour on the outcome of the election next week.

A temporary pop higher in GDP growth...

Turning to economic developments, recently released GDP figures showed that economic activity expanded by 0.8% through the June quarter, to be up 2.7% over the past year. That was in line with our forecast, but slightly below the 0.9% rise that the Treasury and the Reserve Bank expected.

On the face of it, 0.8% isn't a bad rate of expansion. But there are couple of things to keep in mind. Growth in the quarter was boosted by the recovery from earlier disruptions in the dairying and transport sectors. We also had a one-off boost to spending from very strong tourist inflows during the quarter related to some high profile sporting events. Against this backdrop, the pop higher in GDP growth through the June quarter actually looks fairly modest.

..but slowdown is underway...

Notably, with the above temporary boosts now abating, it looks like June will be the high point for GDP growth for a while. As we've been highlighting in recent weeks, momentum in economic activity has been fading. The slowdown in the housing market will likely dampen household spending over the coming months. In addition, growing headwinds in the construction sector are providing a brake on building activity. In fact, nationwide construction activity has fallen in both of the past two quarters, including softness in Auckland home building.

...with softening migration set to be a drag over the coming years

A further factor that leads us to expect softer GDP growth over the coming years is migration. For the past few years, record levels of net migration have seen population growth in New Zealand climbing to a little over 2% per annum. That's a rapid pace for any developed economy, and some of the fastest population growth we've seen in New Zealand since the 1970s. The resulting increase in the size of the economy has masked what has actually been quite muted economic growth on a per capita basis in recent years. In fact, taking out population increases, GDP growth over the past year was only 0.6% on a per capita basis - a far cry from the headline figures.

The strength in net migration has been due to a couple of big trends. First is that for several years now, relatively few New Zealanders have been departing, and large numbers have been returning home, particularly from Australia. At the same time, we've seen a sharp rise in new arrivals from areas like China, India and the UK.

The above trends have resulted in a large and protracted migration cycle. However, we are now starting to see some changes. First, while we're continuing to see firmness in new arrivals and the net outflow of New Zealanders remains low, these have both levelled off in recent months. At the same time, we've seen departures of non-New Zealand citizens steadily rising since mid-2016. In fact, departures of non-New Zealand citizens are nearly 20% higher than this time last year.

Many of the new arrivals to the country in recent years came over on temporary work and student visas, with numbers in these categories rising rapidly from around 2013. Typically those who come over on these programs stay for around three to four years. We're now seeing the normal corresponding outflow, which we expect to continue over the coming months.

Our forecasts have long incorporated a slowdown in net migration. That slowdown may have been a little late in arriving, but now that is has, it looks like it could be coming through even faster than we had expected. This reinforces our expectations for softer GDP growth over the coming years.

Growth to under-perform the RBNZ's forecasts, reinforcing the case for continued low interest rates

The above trends don't mean the economy is heading for a crash. But a slowdown in growth is on the cards. And that will be a challenge for the Reserve Bank. In its August Monetary Policy Statement, the RBNZ forecast annual GDP growth to accelerate to 3.8%, from its current pace of 2.5%. And even then, it only expected inflation to be back around its 2% target mid-point by 2019. However, the kind of GDP acceleration the RBNZ is looking for appears increasingly out of reach, particularly as it relies partly on a strong pickup in construction, a sector that has been going backwards recently.

With this in mind, we expect that the RBNZ will keep the OCR on hold on at its next meeting (this coming Thursday), with the policy paragraph of the statement likely to remain largely unchanged from August.

Interest rates will need to remain low for a long time in order to get inflation back up to 2% on a sustained basis. We expect the OCR to remain on hold until late 2019. In contrast, market pricing continues to suggest a hike by September next year.

Data previews

Aus Aug private credit

Sep 29, Last: 0.5%, WBC f/c: 0.4%

Mkt f/c: 0.5%, Range: 0.4% to 0.6%

- Private credit is expected to expand by 0.4% in August to be 5.4% higher than a year ago. This follows a 0.46% gain in July and a 0.4% monthly average for the year to date. This reflects the balance of two countervailing forces at present.

- Housing credit is expected to increase by 0.5%, 6.5%yr. There is an emerging gradual slowing after a tightening of lending conditions. The 3 month annualised pace eases to 6.0%, down from 6.8% in March. Notably, the total value of housing finance grew by 15% in the year to January, but has stalled since.

- Business credit has emerged from a soft spot to record robust growth of late. We expect a gain of around 0.4%, bringing the 6 month annualised pace to 5.3%, while annual growth will be around 4.5%. Commercial finance has rebounded since February, up a trend 15%, and business investment has turned around from declines to modest gains.

NZ Aug business confidence

Sep 26, Last: 18.3

- Business confidence eased a bit in August, and we expect this to continue into September. With the General Election just around the corner, uncertainty is likely to weigh on businesses' views of the economic outlook. In addition, the economy continues to face challenges regarding capacity constraints, especially in the construction sector. Nevertheless, the economy has been growing at a decent pace and confidence is expected to remain at firm levels.

- Inflation expectations dropped below 2% in the previous survey, in line with the most recent CPI outturn. We expect little change in the September survey.

NZ Reserve Bank Official Cash Rate Review

Sep 28, Last: 1.75%, WBC f/c: 1.75%, Mkt: 1.75%

- The RBNZ is highly unlikely to alter the stance of monetary policy next week, due to election uncertainty.

- Fortunately, the economic situation is such that the RBNZ can afford to sit on its hands.

- We expect no change in the OCR next week, and a repeat of previous monetary policy guidance.

- Beneath this placid surface, there is a lot going on with monetary policy.

- In time, we expect the RBNZ will have to reduce its GDP and house price forecasts, which will affect the stance of monetary policy.

NZ Aug building consents

Sep 29, Last: -0.7%, WBC f/c: flat

- Residential building consent issuance fell 0.7% in July, following a 1.3% decline in June. We expect that issuance will remain flat in August.

- Looking through recent volatility, consent issuance has lost momentum though mid-2017. In part this reflects the structural (but expected) downtrend in Canterbury, as post-earthquake reconstruction continues to gradually wind down. More notable, however, issuance in Auckland has failed to materially accelerate over the past year, and remains below the levels needed to keep up with population growth. Constraining the rise in building activity are capacity constraints, rising costs pressures and tighter credit conditions. Pre-election uncertainty may also be having some dampening impact. While we expect Auckland issuance to rise over time, it looks like this will occur gradually.

Weekly Focus: Calm Markets in a Volatile World

Market Movers ahead

- We expect good news for the ECB in the form of higher inflation and money supply growth. However, inflation is likely to decline again in coming months.

- Germany is due to hold a general election on Sunday and is likely to publish upbeat Ifo numbers on Monday.

- In the US, the August reading of the Fed's preferred inflation measure, PCE, is due out as well as news on consumer sentiment.

- The fourth round of Brexit negotiations is scheduled to begin on Monday, after Theresa May's speech today and the Labour Party conference on Sunday.

- Chinese PMIs are due for a weakening after being sustained over the summer by high steel production before pollution curbs in the winter.

- We expect the pace of decline in unemployment in Norway to have eased but if it has not, this will put pressure on Norges Bank.

Global macro and market themes

- Risk premia across asset classes are currently at pre-Lehman lows.

- High GDP growth relative to funding costs supports low risk premia.

- As US interest rates rise towards the natural rate, financial volatility and risk premia should rise

- We expect this to play out in Q4.

GBPUSD Stutters and Fails to Continue Upward Impulse

The EUR/USD price was showing a confident upward movement on the background of rising geopolitical tensions after the North-Korean minister of foreign affairs declared the possibility of a new hydrogen bomb test in the Pacific Ocean in response to the speech by Donald Trump at the UN. The common currency also received some support from the Eurozone's flash manufacturing PMI in September which increased to 58.2 against the 57.2 forecasted and from the flash services PMI which came in above expectations at 55.6.

German Chancellor Angela Merkel asked voters to come to the elections over fears of low attendances which may lead to significant changes in the result. This Sunday, parliamentary elections in Germany will be held and Merkel is likely to remain as the head of state.

The sterling was not able to keep rising and currently is falling partly due to price fixing following the previous rally and ahead of the weekend. GBP/USD also came under pressure from the CBI industrial order expectation index in the UK that reduced to 7 in September against the 13 forecasted.

The Canadian dollar weakened on the background of the disappointing core retail sales report in the country that showed growth of only 0.2% which is twice worse than the average prediction. Consumer inflation data also missed expectations and showed that the CPI increased by only 0.1% in August. Earlier the Bank of Canada increased interest rates, but the Canadian dollar has already lost part of those previously gained positions.

EUR/USD

The single currency quotes tested the 1.2000 resistance but was not able to break through it. In case of breaking through this line, the pair is likely to reach 1.2070. On the other hand, the closest objectives in case of a trend change may be 1.1925, 1.1825 and 1.1700. The chance of volatility growing till the end of the trading session is low.

GBP/USD

The GBP/USD rolled back after a couple of unsuccessful attempts to break through the strong resistance at 1.3600. Currently the price is trying to move beyond the limits of the rising channel and in case of fixing below its lower boundary we may see massive selling with potential targets at 1.3400 and 1.3250. The growth potential today is most likely to be restrained by 1.3600 line.

USD/CAD

The USD/CAD is moving within the 1.2235-1.2365 range. In case of gaining a foothold above 1.2365, the price is likely to reach the next goal at 1.2475. The MACD signal line crossed the zero mark which points to a possible price growth in the near term. Despite more chances for further growth, we do not exclude a price drop to the inclined support line.

EUR/GBP Lifted By Euro-zone Data

EUR/GBP is trading in the green and tries to stay above dynamic support despite the yesterday's breakdown. It has managed to erase the yesterday's losses and is struggling to stay much above the 0.8773 previous low. Technically, it is expected to drop further on the short term because is located under some important dynamic support levels.

The Euro remains strong on the short term, has managed to increase also versus the USD and versus the CHF. The Cable has lost ground versus the Euro as the Euro-zone data have impressed in the European session. The Flash Manufacturing PMI increased from 57.4 points to 58.2 points, signaling that the expansion continues in the manufacturing sector, while the Flash Services PMI is expected to increase from 54.7 to 55.6 points, beating the 54.7 estimate.

The German and French Flash Manufacturing PMI and the Flash Services PMI have come in better than expected as well.

Price rallies aggressively and tries to stay above the 100% Fibonacci level. A false breakdown below the mentioned level will signal an increase at least till the third warning line (wl3) of the former descending pitchfork. We may have a minor sideways movement here before will decide where to go. A drop towards the lower median line (LML) was expected, but it could come to retest the median line (ML) as well before will drop again.

GBP/USD Minor Retreat Still In Cards

Price has decreased sharply and is almost to erase the yesterday's gains. It has failed to resume the upside movement and now is located under the 150% Fibonacci line (ascending dotted line). I've drawn a minor red descending pitchfork, a retest of the upper median line (uml) could signal another leg lower on the short term. Only a breakout above the upper median line (uml) will invalidate another drop.

EUR/CHF Poised For More Gains

The currency pair has extended the upside momentum and seems determined to climb much higher on the short term. The next upside target will be at the second warning line (wl1) of the minor ascending pitchfork. Only a failure to reach the mentioned line will signal an exhaustion and a potential drop.

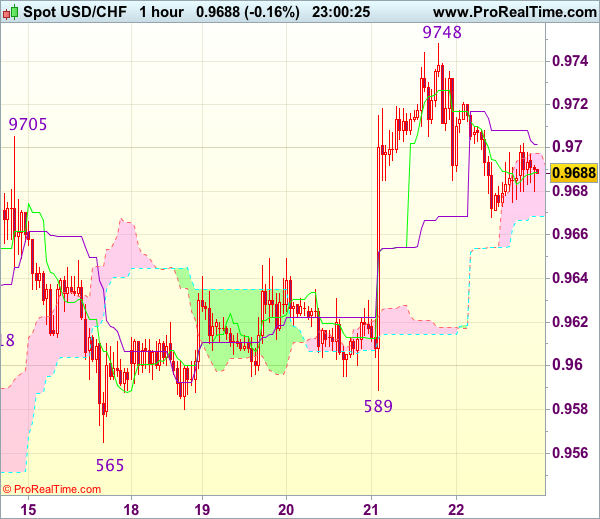

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9692

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9689

Kijun-Sen level : 0.9702

Ichimoku cloud top : 0.9698

Ichimoku cloud bottom : 0.9669

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The greenback retreated after rising to 0.9748 earlier this week and consolidation below this level would be seen and pullback towards the lower Kumo (now at 0.9654) cannot be ruled out, however, reckon previous minor resistance at 0.9630 would limit downside and price should stay well above indicated support at 0.9589, bring rebound later.

On the upside, whilst recovery to the Kijun-Sen (now at 0.9702) cannot be ruled out, reckon upside would be limited to 0.9720-25 and said resistance at 0.9748 should hold, bring retreat later. In the event dollar is able to penetrate said resistance at 0.9748, this would revive bullishness and extend recent rise from 0.9421 low to 0.9761-66 (50% Fibonacci retracement of 1.0100-0.9421 and previous resistance), then another previous resistance at 0.9773. As near term outlook is still mixed, would be prudent to stand aside for now.