Sample Category Title

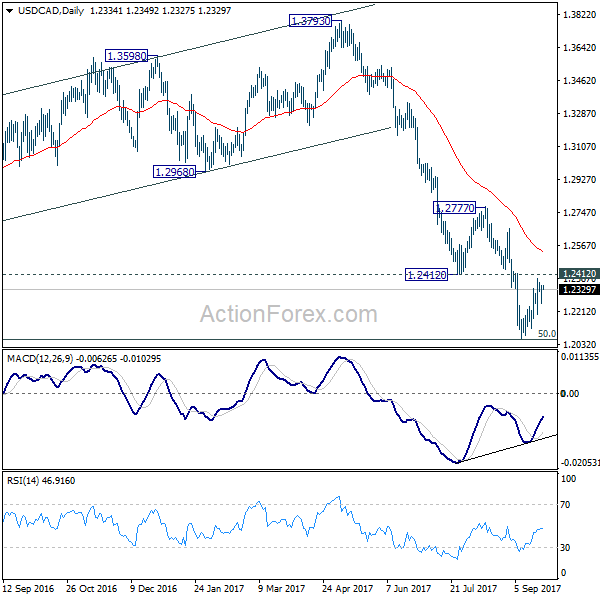

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2274; (P) 1.2313; (R1) 1.2374; More....

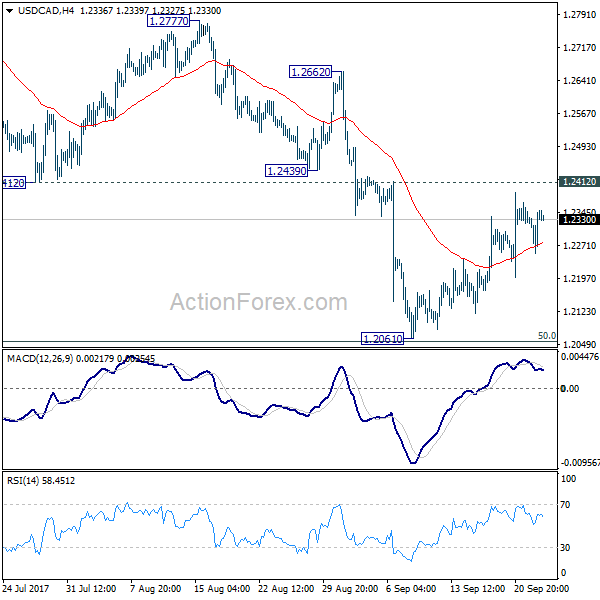

Intraday bias in USD/CAD remains neutral as consolidation from 1.2061 is still in progress. At this point, we'd remain cautious on strong support from 1.2048 to bring sustainable rebound. But still, break of 1.2439 support turned resistance is needed to be the first sign of trend reversal. Otherwise, outlook will remain bearish. Firm break of 1.2048 will pave the way to next fibonacci level at 1.1424. Break of 1.2412 will bring stronger rise back to 55 day EMA (now at 1.2531) and above.

In the bigger picture, focus remains on 50% retracement of 0.9406 to 1.4869 at 1.2048. As long as this level holds, we'd still favor that case that fall from 1.4689 is a correction. Rebound from 1.2048 could extend the larger up trend from 0.9406. However, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

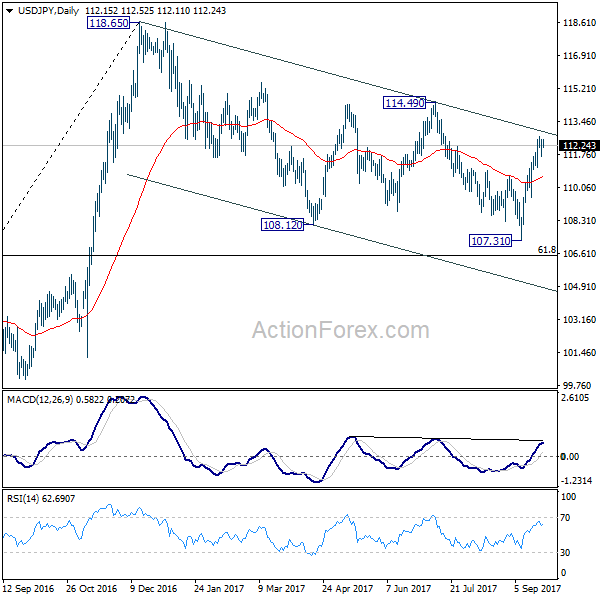

USD/JPY Daily Outlook

Daily Pivots: (S1) 111.57; (P) 112.06; (R1) 112.47; More...

Intraday bias in USD/JPY remains neutral for the moment. Further rise is in favor with 111.07 support intact. Sustained break of medium term channel resistance (now at 113.03) will argue that whole correction from 118.65 has completed. In that case, further rise should be seen to 114.49 resistance for confirmation. However, break of 111.07 minor support will raise the risk of rejection from channel resistance and turn bias back to the downside for 55 day EMA (now at 110.64) and below.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9670; (P) 0.9689; (R1) 0.9711; More....

Intraday bias in USD/CHF remains neutral for the moment. On the upside decisive break of 0.9772 resistance will suggest that whole down trend form 1.0342 has completed. In that case, near term outlook will be turned bullish for 0.9860/1.0099 resistance zone. Nonetheless, with 0.9772 resistance intact, outlook remains bearish. Below 0.9587 minor support will turn bias back to the downside for retesting 0.9420 low.

In the bigger picture, current development suggests that 0.9443 key support (2016 low) could be taken out firmly as down trend form 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

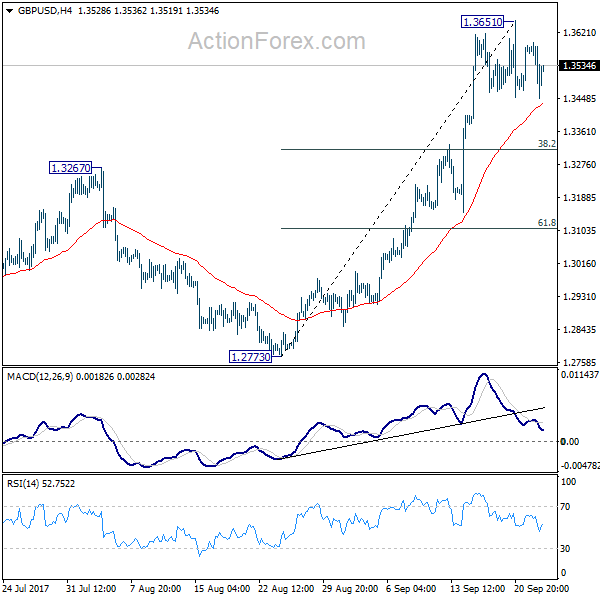

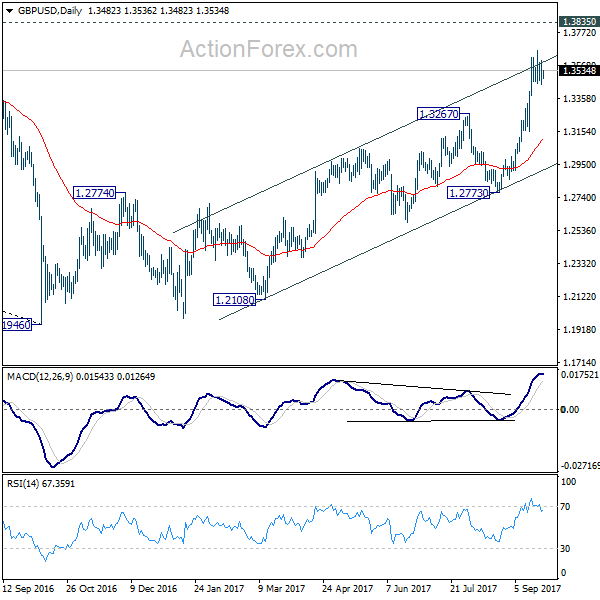

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3425; (P) 1.3510; (R1) 1.3572; More....

Intraday bias in GBP/USD remains neutral for the moment as consolidation from 1.3651 continues. In case of deeper fall, downside should be contained by 38.2% retracement of 1.2773 to 1.3651 at 1.3316 and bring rise resumption. Above 1.3651 will turn bias back to the upside for 1.3835 support turned resistance next. Break there will target 55 month EMA (now at 1.4405).

In the bigger picture, current development argues that the long term trend in GBP/USD has reversed. That is, a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

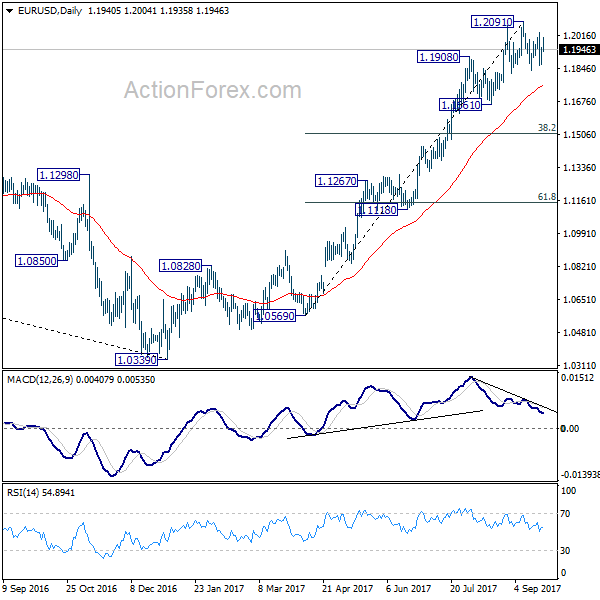

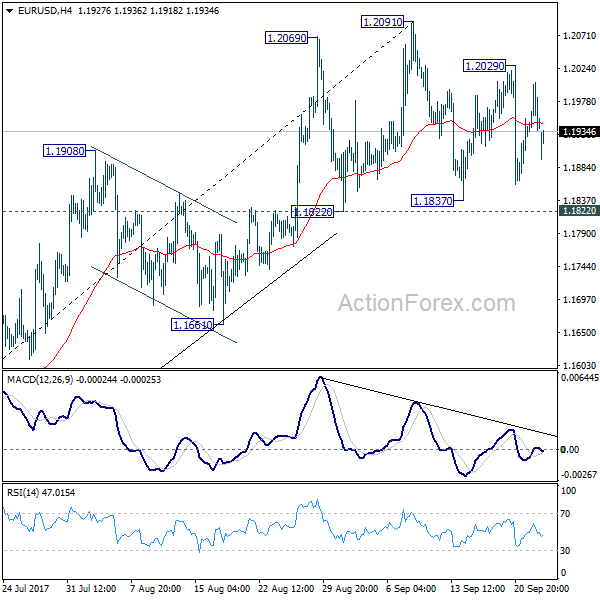

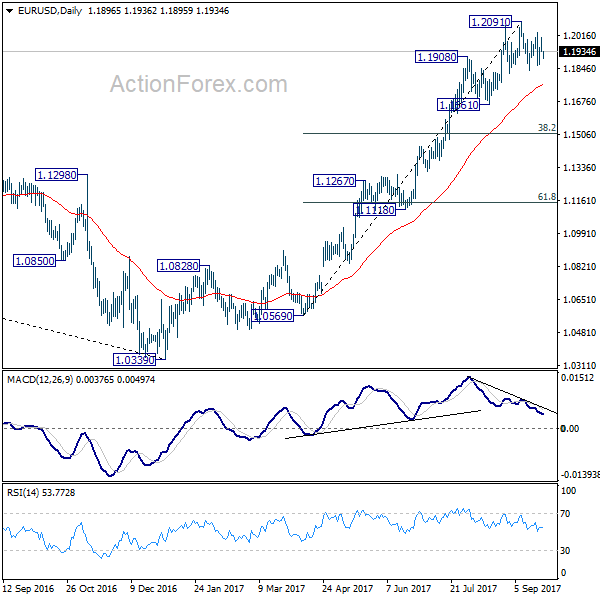

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1919; (P) 1.1961 (R1) 1.1990; More...

EUR/USD gaps lower today but it's holding well in range of 1.1822/2091. Intraday bias remains neutral for the moment. With 1.1822 support intact, near term outlook remains bullish for further rally. Break of 1.2091 will extend larger rise from 1.0339 and target next key fibonacci level at 1.2516. But considering bearish divergence condition in 4 hour MACD, break of 1.1822 will confirm short term reversal. In the case, intraday bias will be turned back to the downside through 1.1661 support. EUR/USD should then correct whole rise from 1.0569 and target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

Euro and New Zealand Dollar Mildly Lower after Elections, Brexit Negotiation to Resume

Euro gaps lower against Dollar as another week starts. Markets seem to be dissatisfied with Germany election result even though Angela Merkel won her fourth term as Chancellor. Nonetheless, loss in the common currency is limited and it quickly recovers. Meanwhile, Kiwi also trades lower after indecisive election results. Yen is mildly weaker and risk sentiments are steady even though US President Donald Trump continued his verbal exchanges with North Korea officials. Yen traders' are probably more on Japan Prime Minister Shinzo Abe's press conference for snap election, rather than the words of the two sides that are on "suicide mission". Sterling is mildly firmer as the fourth round of Brexit negotiations starts.

Euro lower on plunge of support for CDU/CSU

Angela Merkel won a fourth term as German Chancellor after Sunday's election. But vote for her CDU/CSU bloc suffered heavy decline to 32.7%, down 8.8% from 2013. That's also the worst result since 1949. Main opposition Social Democrats scored 20.2%, the worst ever result. On the other hand, the anti-immigration Alternative for Germany won 13% of vote, up 8.7% from 2013. Free Democrats got 10.5% and Greens got 9.4%. The risk now is that Merkel will need to form a coalition with at least two other parties, and that is seen as some uncertainty for the near term. Also, the better than expected results for AfD and the plunge in CDU/CSU reminded people that populism remains a threat in European Union.

Kiwi dips mildly on indecisive election

New Zealand Dollar dips mildly today, in reaction to the indecisive election held on Saturday. The ruling centrist National party won 58 seats in a 120 seat parliament. Center-left Labour won 45 seats. New Zealand First won 9 while Greens got seven. Rightwing ACT got 1 seat. Without outright majority, the National could now take a few weeks for form a coalition. But the overall results are pretty much in line with pre-election polls. So, the impact to markets should be minimal.

Fourth round of Brexit negotiation to start

The fourth round of Brexit negotiation between UK and EU will start in Brussels today. Also, there will be another round of Brexit talks between Scottish and UK governments in London. Prime Minister Theresa May called for a two year "implementation period" on Brexit, and during the time, it's almost like all status quo. UK will continue to have access to the single-market and pay into EU budgets. UK would even accept new EU regulations through to 2021. Such a proposal attracts criticism from May's own MPs. The criticism mainly center around payment to EU an European Court of Justice jurisdiction.

Japan PMI manufacturing rose to 52.6

Japan PMI manufacturing rose to 52.6 in September, up from 52.2, but missed expectation of 53.4. Nonetheless, that's the 13 straight month of expansionary reading, and the highest level since May. IHS Markit principal economist Annabel Fiddes noted that "firms signalled stronger expansions in both output and new orders amid reports of firmer demand both at home and abroad" And, "the strong end to Q3 bodes well for production in the coming months, with business confidence also perking up slightly since August." Japan Prime Minister Shinzo Abe is widely expected to announce a snap election for October today, to take advantage of the rebound in his popularity. Abe will hold a press conference at 0900GMT..

Looking ahead

German Ifo business climate in the main focus today. RBNZ rate decision is a main feature in the week and it's widely expected to stand pat. Some important economic data will be featured including Eurozone CPI, Japan CPI, Canada GDP and US durable goods and PCE. But the highlight is likely on details of US President Donald Trump's tax plan. Here are what are's expecting for the week ahead:

- Tuesday: News Zealand trade balance, NBNZ business confidence; BoJ minutes, corporate service price; German import price; US S&P Case Shiller house price, new home sales, consumer confidence

- Wednesday: Swiss UBS consumption; Eurozone M3; US durable goods, pending home sales

- Thursday: RBNZ rate decision; German Gfk consumer sentiment; Eurozone confidence indicators; German CPI; US Q2 GDP final, jobless claims; trade balance

- Friday: Japan unemployment, CPI, retail sales, industrial production, BoJ summary of opinions; China PMI manufacturing; German retail sales, unemployment; Swiss KOF; UK Q2 GDP final, mortgage approvals, M4; Eurozone CPI flash; Canada GDP; US personal income and spending, Chicago PMI

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1919; (P) 1.1961 (R1) 1.1990; More...

EUR/USD gaps lower today but it's holding well in range of 1.1822/2091. Intraday bias remains neutral for the moment. With 1.1822 support intact, near term outlook remains bullish for further rally. Break of 1.2091 will extend larger rise from 1.0339 and target next key fibonacci level at 1.2516. But considering bearish divergence condition in 4 hour MACD, break of 1.1822 will confirm short term reversal. In the case, intraday bias will be turned back to the downside through 1.1661 support. EUR/USD should then correct whole rise from 1.0569 and target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | JPY | PMI Manufacturing Sep P | 52.6 | 53.4 | 52.2 | |

| 8:00 | EUR | German IFO - Business Climate Sep | 116 | 115.9 | ||

| 8:00 | EUR | German IFO - Expectations Sep | 108 | 107.9 | ||

| 8:00 | EUR | German IFO - Current Assessment Sep | 124.7 | 124.6 | ||

| 13:00 | CNY | Conference Board Leading Index Aug | 0.90% |

Market Morning Briefing: The Dollar Index Is Trading Slightly Higher

STOCKS

Dow (22349.59,-0.04%) could be in the beginning on a small correction after the recent rally from levels near 21800 to 22400 levels. A test of 22200 or lower is possible before again resuming the long term up trend.

Dax (12592.35, -0.06%) almost went up to test the interim resistance at 12675 but came off to close at lower levels. While 12675 holds, the index may come off to 12500 or lower just now; a break above 12675 is necessary to move higher towards 12800. We prefer 12675 levels to hold just now.

Nikkei (20412.59, +0.57%) is unable to move above 20500 and could spend some time within 20200-20500 region before deciding on further direction. As mentioned earlier, 21000 and 20800 are long term resistances on the upside and there is not much scope for a potential rise in the longer term. Either the index could come off from current levels to test 20000, else it could try a re-attempt of levels above 20500.

Shanghai (3340.28, -0.37%) is moving down slowly. A test of 3320-3300 level is possible in the near term from where the index could move back to levels near 3380 again.

Nifty (9964.40, -1.56%) could test immediate support near 9900 on the daily candles from where a bounce back towards 10100 is possible. In case 9900 breaks on the downside, the next support levels would be seen near 9800 or even lower.

COMMODITIES

Gold (1292.36) could trade within 1290-1300 for a couple of sessions. Thereafter, equal chances of either moving up towards 1310-1315 or coming down to 1280 is possible.

Silver (16.89) could test decent support near 16.75 which if holds can push the index to higher levels of 17.20.

Brent (56.83) has moved up faster compared to WTI (50.57) which is almost stable near previous levels. WTI may remain below 51 for another session or two while Brent could move up to 57.45 in the near term. Crude looks positive just now but could soon enter into a corrective dip by the end of the week.

Copper (2.9415) may move up to 3.00 in the coming sessions. Trade within 3.00-2.90 is possible this week. Movements are expected to remain narrow.

FOREX

As it turns out, the Euro (1.1932) rose to 1.2005 on Friday, but was unable to sustain the rise, despite stability in the German-US 10Yr Spread (-1.81%). The overall uptrend is still intact, but the Support to watch has moved up to 1.1890, from 1.1850 earlier.

The Dollar Index (92.25) is trading slightly higher, but still remains below crucial Resistances at 92.50 and 93.00 for now. The downtrend remains intact while these hold.

Very good correlation is seen between the increase in the UK-US Yield 10Yr Spread (-0.90%) and the Pound (1.3525). The latter has found Support at 1.3438 for now and may try to move up towards 1.3630 this week, with potential for 1.38 later on.

Watch Resistance near current level on the US-Japan 10Yr Spread (2.25%). If this holds, it could limit the upside in Dollar-Yen (112.21) to the Resistance at 113.50 mentioned earlier. The Euro-Yen (133.86) looks bullish enough to try and rise towards 136.

Although a near term top seems to be in place on the Aussie (0.7953), we also note Support near 0.79, the 21-MA on the 3-day chart. A fresh bounce would need to be considered while that holds.

Dollar-Yuan (6.6020) has finally crosssed our target of 6.60 and can rise some more towards 6.61+. Dollar-Rupee (64.7950) has crucial Support at 64.70 today.

INTEREST RATES

US yields (30Yr 2.79%, 10Yr 2.26%, 5Yr 1.87%) stabilised a bit on Friday, near or just above their near term Resistance levels. This week will show whether they rise further or not. In the meanwhile, the US Yield Curve remains in a flattening mode with the US 10-5 (0.39%) and US 30-10 (0.53%) continuing to trend lower.

In contrast, the German Yield Curve is steepening, with the German 10-5 (0.7%) and German 30-10 (0.82%) looking more bullish. Yet, the German-US 10Yr Spread (-1.81%) appears to have broken its uptrend, as mentioned earlier. This is to be watched for its implication on the Euro.

UK Gilt yields (5Yr 0.76%, 10Yr 1.36%, 30Yr 1.83%) continue to rise/ trade above near term trend resistances, but could consolidate here for a while. Overall, the UK-US Yield 10Yr Spread (-0.90%) is rising, supporting the Pound.

In India, 10Yr GOI (6.6632%) is likely to remain below crucial Resistance at 6.7000-7250% with the government exerting pressure on the RBI to lower rates. The next RBI meeting is on 3rd October, next week.

EUR/USD – Mind The Gap!

Back at it for another week and markets have opened with some serious gaps all over the place. One notable gap that I wanted to high is on EUR/USD.

Take a look at the 15 minute chart below:

EUR/USD 15 Minute:

After the FOMC drop was retraced, price has gapped to the downside. But as you can see, price has done nothing but rally up toward it since the weekly open.

With what looks like some serious momentum pulling price toward closing the gap, do you see opportunity to jump on board?

I’ll include the weekly just for higher time frame context:

EUR/USD Weekly:

USDCHF – Follows Through Higher On Bull Pressure

USDCHF - With the pair following through higher on the back of previous week gains the past week, more strength should follow. On the downside, support lies at the 0.9650 level. A turn below here will open the door for more weakness towards the 0.9600 level and then the 0.9550 level. On the upside, resistance resides at the 0.9750 level where a break will clear the way for more strength to occur towards the 0.9800 level. Further out, resistance comes in at the 0.9850 level. Above here if seen will turn attention to 0.9900. All in all, USDCHF faces further upside pressure short term

EUR/USD Weekly Outlook

Much volatility was seen in EUR/USD last week. But it stayed in range of 1.1822/2091 so far. Initial bias remains neutral this week first. With 1.1822 support intact, near term outlook remains bullish for further rally. Break of 1.2091 will extend larger rise from 1.0339 and target next key fibonacci level at 1.2516. But considering bearish divergence condition in 4 hour MACD, break of 1.1822 will confirm short term reversal. In the case, intraday bias will be turned back to the downside through 1.1661 support. EUR/USD should then correct whole rise from 1.0569 and target 38.2% retracement of 1.0569 to 1.2091 at 1.1510.

In the bigger picture, rise from medium term bottom at 1.0339 is still in progress for 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside. But after all, break of 1.1661 is needed to indicate medium term topping. Otherwise, outlook will remain bullish in case of pull back.

In the long term picture, 1.0339 is now seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action form 1.0339 is developing into a corrective or impulsive move. But in either case, further rally would be seen to 38.2% retracement of 1.6039 to 1.0339 at 1.2516