Sample Category Title

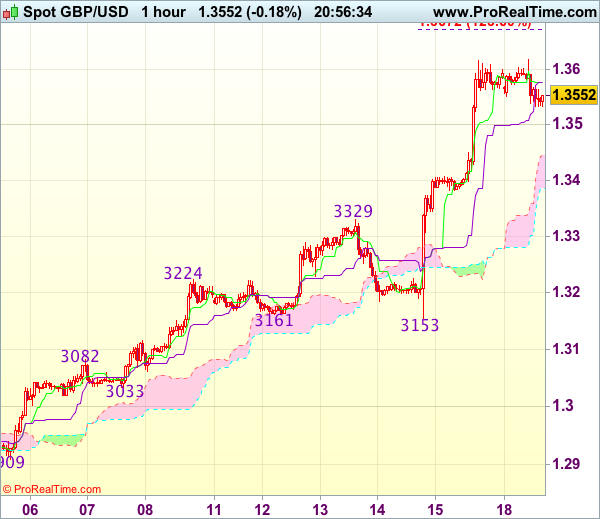

Trade Idea Update: GBP/USD – Buy at 1.3420

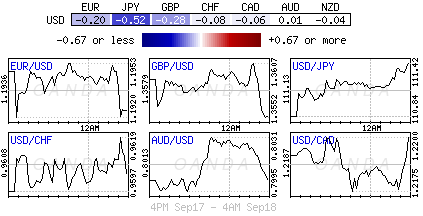

GBP/USD - 1.3555

Original strategy :

Buy at 1.3420, Target: 1.3600, Stop: 1.3385

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3420, Target: 1.3600, Stop: 1.3385

Position : -

Target : -

Stop : -

Although cable edged higher in London morning to 1.3619, lack of follow through buying on break of Friday’s high at 1.3617 and current retreat suggest consolidation with initial mild downside bias would be seen and pullback to the Kijun-Sen (now at 1.3518) cannot be ruled out, however, reckon downside would be limited to 1.3420-30 and bring another rise later, above said resistance at 1.3619 would extend recent upmove to 1.3650 and possibly towards 1.3675 but upside should be limited to 1.3700-10, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent pullback as 1.3420-30. Only below 1.3380-85 would defer and signal a temporary top is formed, bring retracement of recent rise to 1.3350, then 1.3320-25 but lower Kumo (now at 1.3302) should remain intact.

CAC Gains Ground on Strong Eurozone Inflation Report

The CAC index has started the trading week with gains. Currently, the index is at 5,226.00, up 0.26% on the day. On the release front, Eurozone Final CPI improved to 1.5%, matching the forecast. On Tuesday, the eurozone releases its current surplus and ZEW Economic Sentiment, both of which are expected to improve.

France received a thumbs-up from the OECD last week, which released a report on the French economy. The OECD is forecasting French growth of 1.7% in 2017, compared to a 1.1% gain in 2016. The report commended President Emmanuel Macron's agenda to reform the economy, but emphasized that the government needed to cut public sector spending, which is the highest in the 35-member OECD. The report also called on the French government to overhaul the country's labor laws, including cutting pension costs and raising the current retirement age of 62 years. With President Emmanuel Macron declaring he will reform France's labor laws, powerful trade unions are mobilizing to fight back. On Tuesday, some 200,000 trade unionists came out for a mass protest. The government plans to adopt new labor rules on September 22, and two large unions have threatened to respond with a massive truckers strike on September 25, which could cause chaos across the country.

French President Emmanuel Macron, a staunch supporter of a unified Europe, is hoping to continue working with German Prime Minister Angela Merkel after the German election, and focus on reforming the eurozone. Macron's proposal includes a eurozone finance minister who would be in charge of a eurozone budget. Macron's call for greater cooperation is linked to Britain's exit from the EU, which could lead to divisions among the remaining 27 members in the bloc. However, the French ambitious plan will need Germany's support before it can become a reality. Will Germany embrace the idea? Angela Merkel has indicated that she is open to the idea, but Jean-Claude Juckner, head of the European Commission, came out against the plan last week. Juckner said he favored a finance minister for the EU but was against a separate eurozone budget and finance minister. Even if the plan is not adopted, we can expect a Macron-Merkel alliance to take steps which will strengthen Franco-German ties and further unify the eurozone.

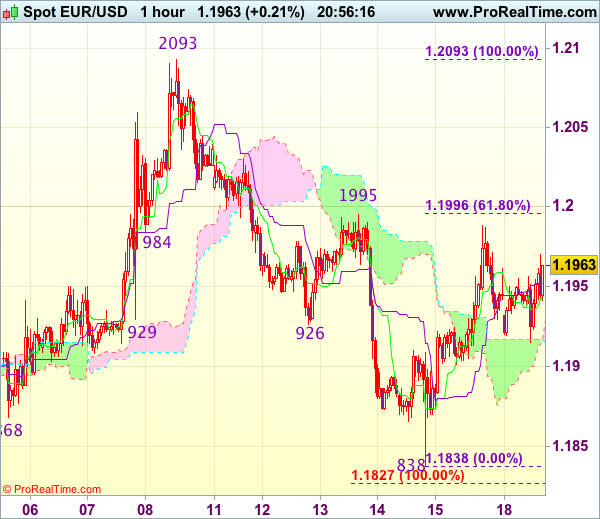

Trade Idea Update: EUR/USD – Buy at 1.1905

EUR/USD - 1.1961

Original strategy :

Buy at 1.1905, Target: 1.2005, Stop: 1.1870

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1905, Target: 1.2005, Stop: 1.1870

Position : -

Target : -

Stop : -

Although the single currency retreated after meeting resistance at 1.1988 on Friday, last week’s anticipated rebound from 1.1838 suggests low has possibly been formed there and downside should be limited to 1.1900-05, bring another rebound later to 1.1995-00 (previous resistance and 61.8% Fibonacci retracement of 1.2093-1.1838), however, break there is needed to signal the fall from 1.2093 has ended, bring subsequent rise to 1.2030-35 and then 1.2050-55.

In view of this, we are looking to buy euro again on dips as 1.1900-05 should limit downside and bring another rebound. Below 1.1865-70 would abort and suggest the rebound from 1.1838 (last week’s low) has ended, bring retest of this level first.

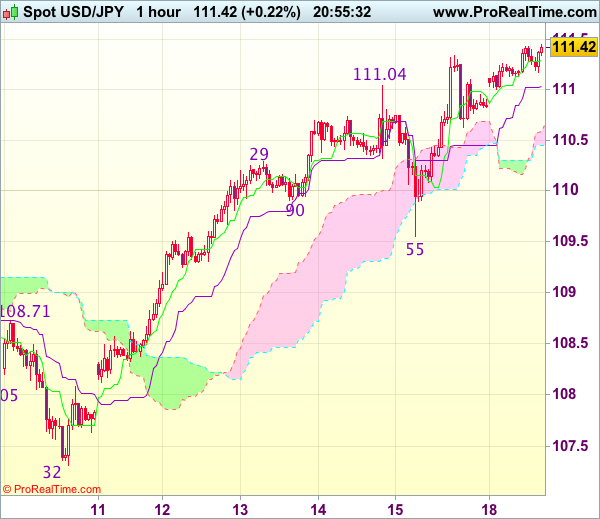

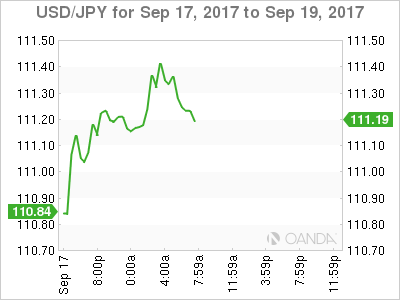

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 111.41

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the greenback has edged higher again after last week’s rally and bullishness remains or recent reversal from 107.32 low to extend gain to 111.55-60, however, reckon upside would be limited to 111.85-90 (61.8% projection of 107.32-111.04 measuring from 109.55) and price should falter below 112.00-10, risk from there has increased for a correction later.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below 111.00 would bring correction to 110.60-65 but downside should be limited to 110.30-35 and price should stay above 110.00, bring rebound later.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.79; (P) 110.56; (R1) 111.59; More...

USD/JPY's rebound from 107.31 continues today and reaches 111.44 so far. Intraday bias remains on the upside for medium term channel resistance (now at 112.91). Sustained break there will argue that whole correction from 118.65 has completed too. In that case, further rise should be seen to 114.49 resistance for confirmation. On the downside, break of 109.54 support is needed to indicate completion of the rebound. Otherwise, outlook will stay cautiously bullish in case of retreat.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

Yen Lower on Risk Appetite in Quiet Markets, Sterling Pares Gains

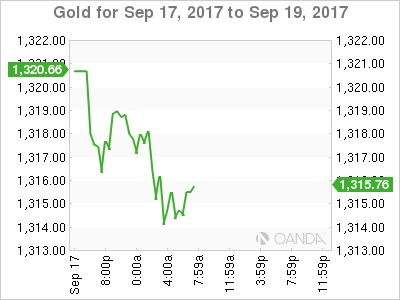

Yen trades generally lower today in otherwise quiet markets. Euro is trading firmer while Sterling is paring some of last week's sharp gains. Global markets are generally in risk seeking mode. The MSCI Asia Pacific ex Japan index surged to decade high earlier today. European indices follow with some gains, including FTSE. US futures also suggest that stocks are going to extend the record run. If other markets, gold continues with it's pull back from recent high at 1362.4 and hits as low as 1314.5 so far. It's possibly heading back to 1300 handle, which is close to 55 day EMA at 1293.4. WTI crude oil weakens mildly as it struggles to find sustainable buying to stay firm above 50 handle.

The economic calendar is rather light today. Canada international securities transactions rose CAD 23.95b in July. Eurozone CPI was finalized at 1.5% yoy in August, core CPI at 1.2% yoy. UK Rightmove house price dropped -1.2% mom in September. There are a lot of high profile events ahead in the week. BoE Governor Market Carney will speak at IMF in Washing today. RBA will release meeting minutes tomorrow. US President Trump will also address the United Nations. Fed is expected to announce the plan to unwind the balance sheet on Wednesday. UK Prime Minister Theresa will deliver a Brexit speech in Italy on Friday. And there will be general elections in New Zealand and Germany in the coming weekend.

ECB Hansson advocates broader recalibration of monetary policy

ECB Governing Council member Ardo Hansson urged not to have "inordinate focus on the asset purchase program". Instead, he advocates a "somewhat broader recalibration" of monetary policy. He noted that the central has "a range of instruments already under implementation" And, ECB could "in addition bring to the table for consideration". He pointed out that "various refinancing operations and the details of forward guidance could be more precise about interest rates". Hansson also played down the concern over Euro's strength. He noted that the exchange rate is "well within the historical range". Also, the euro area has a "current accounts surplus of some volume".

Sterling awaits BoE Carney speech

Sterling pares back some gains today as markets await BoE Governor Mark Carney's speech at IMF in Washington. Traders are rather convinced that a November hike is on the table because a known dove Gertjan Vlieghe turned his stance last Friday and said a rate hike is "approaching". The echoed the surprised BoE minutes that showed most members believe there will be a hike in coming months. Markets will look into Carney's speech today to further verify such expectations. Nonetheless, it should already be priced in well after the strong surge in Sterling last week. Therefore, any Carney triggered gains could be temporary. The Pound may turn into consolidation to digest recent gains, before getting fresh inspirations from incoming data.

Japan PM Abe will decide on parliament dissolution after September 22

In Japan, it's report over the weekend that Prime Minister Shinzo Abe will dissolve the Lower House on September 28 and call for a snap election on October. Abe responded to the rumor at Haneda airport as he was departing for United Nations Meetings in New York. Abe said that he'll "refrain from answering each and every question about a dissolution of parliament". And he will "decide when I return to Japan" on September 22. It's believed that Abe wants to ride on recent resurgence in his approval rating, for handling of the North Korea tensions. In additional, politic analysts noted that the main opposition Democratic Party is in terrible shape, leaving practically no opposition to Abe.

RBA minutes watched in upcoming Asian session

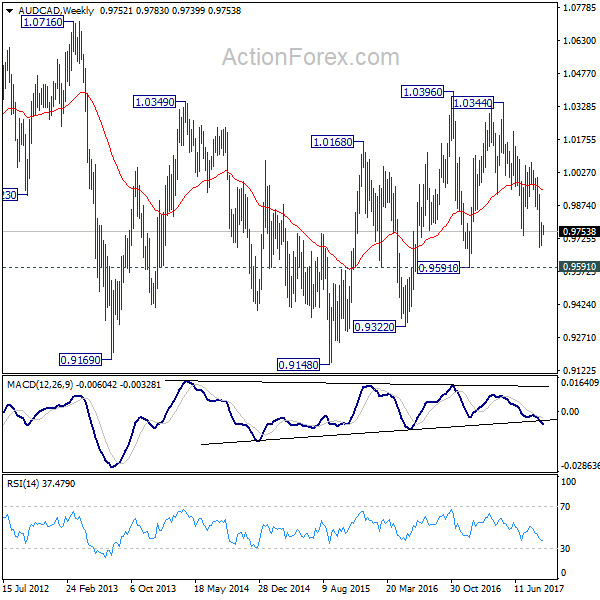

RBA minutes will be a focus in the coming Asian session. The central bank left benchmark interest rate unchanged at 1.50% on September 4 and left the markets with a relatively neutral statement. The minutes would probably just reflect that neutral stance. Nonetheless, attention will still be on any change in tone regarding monetary policies that agrees with the market expectation of a hike as next step in 2018. AUD/CAD has been softer since BoC surprised the markets by two rate hikes this year. Deeper fall is expected in the cross to 09591 key support level in short to medium term. The bearish outlook will remain until RBA becomes more explicitly in its tightening bias.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.79; (P) 110.56; (R1) 111.59; More...

USD/JPY's rebound from 107.31 continues today and reaches 111.44 so far. Intraday bias remains on the upside for medium term channel resistance (now at 112.91). Sustained break there will argue that whole correction from 118.65 has completed too. In that case, further rise should be seen to 114.49 resistance for confirmation. On the downside, break of 109.54 support is needed to indicate completion of the rebound. Otherwise, outlook will stay cautiously bullish in case of retreat.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Sep | -1.20% | -0.90% | ||

| 09:00 | EUR | Eurozone CPI M/M Aug | 0.30% | 0.30% | -0.50% | |

| 09:00 | EUR | Eurozone CPI Y/Y Aug F | 1.50% | 1.50% | 1.30% | |

| 09:00 | EUR | Eurozone CPI - Core Y/Y Aug F | 1.20% | 1.20% | 1.20% | |

| 12:30 | CAD | International Securities Transactions (CAD) Jul | 23.95B | 4.46B | -0.92B | |

| 14:00 | USD | NAHB Housing Market Index Sep | 67 | 68 | ||

| 20:00 | USD | Net Long-term TIC Flows Jul | 42.3B | 34.4B |

DAX Starts Week With Gains as Eurozone CPI Improves

The DAX index has posted slight gains in the Monday session. Currently, the DAX is trading at 12,552.00, up 0.30% on the day. On the release front, Eurozone Final CPI improved to 1.5%, matching the forecast. On Tuesday, Germany releases ZEW Economic Sentiment, which is expected to improve to 12.3 points.

With less than a week to go before the German federal election, Angela Merkel is widely expected to win her fourth term as prime minister. Merkel's CDU conservative party has a 14 percent lead over the center-left SPD, its current coalition partner. Another option for Merkel is the FDP, but the latter has insisted on receiving the finance ministry, and has also taken a hard line on immigration which Merkel may not be comfortable with. Germany's position in Europe will be even more dominant when Britain leaves the European Union, which may some members of the club uneasy.

French President Emmanuel Macron, a staunch supporter of a unified Europe, is hoping to continue working with Merkel and reform the eurozone. Macron's proposal includes a eurozone finance minister who would be in charge of a eurozone budget. Macron's call for greater cooperation is linked to Britain's exit from the EU, which could lead to divisions among the remaining 27 members in the bloc. However, the French ambitious plan will need Germany's support before it can become a reality. Will Germany embrace the idea? Angela Merkel has indicated that she is open to the idea, but Jean-Claude Juckner, head of the European Commission, came out against the plan last week. Juckner said he favored a finance minister for the EU but was against a separate eurozone budget and finance minister. Even if the plan is not adopted, we can expect a Macron-Merkel alliance to take steps which will strengthen Franco-German ties and further unify the eurozone.

Before & After the Hurricanes

Hurricanes will get the bulk of the blame but the latest data showed growth was slowing before Harvey and Irma. A big week ahead: Trump's UN speech on Tuesday; Fed decision & Yellen presser on Wednesday; PM Theresa May's EU speech on Friday and German Elections on Sunday. A new Premium note has been added to further our existing index trade.

A cascade of growth downgrades followed US retail sales and industrial production numbers on Friday. Retail sales fell 0.2% compared to +0.1% expected in August. The control group, which excludes autos, gas and building supplies was down 0.2% compared to +0.2% expected. In addition, July sales were revised lower.

It wasn't just consumers with bad news. August industrial production fell 0.9% compared to +0.1% expected in the worst monthly decline in five years. The Fed said Harvey reduced output by 0.75 pp so it's not as bad as it looks, but it's undoubtedly a poor reading. How poor? The NY Fed and Atlanta Fed GDP trackers were both lowered by 0.8 pp for Q3 while Q4 estimates were trimmed as well.

The market took the weak data in stride in a sign that it views Harvey as the culprit. That may be a hint on how buoyant the dollar will be in the week ahead as the market prepares for details of Trump's tax plan at the end of the month.

What was unambiguous was pound strength as cable finished the week just under 1.36. The OIS market is pricing in a 65% chance of a BOE hike on Nov 2 and 73% before year-end. What makes that probability even higher is that Carney's credibility can't afford another misstep.

CFTC Commitments of Traders

Speculative net futures trader positions as of the close on Tuesday. Net short denoted by - long by +.

- EUR +86K vs +96K prior

- GBP -46K vs -54K prior

- JPY -57K vs -74K prior

- CHF -2K vs -2K prior

- CAD +50K vs +54K prior

- AUD +60K vs +65K prior

- NZD +12K vs +15K prior

Those sterling shorts are suddenly rather vulnerable and no doubt many covered since the Bank of England decision. Watch out for Carney's speech today at 11 am EST (4 pm London). Euro shorts were pared after last week hitting the most-extreme since May 2011.

Market Update – Asian Session: Quiet Start To Week

Notes/Observations

ECB sees inflation rate below 1% in early 2018 citing a statistical quirk

Overnight

Asia:

Japan PM Abe: To decide on dissolving Diet and election after current US visit (**Note: Earlier reports circulated that PM Abe was considering snap election as soon as Oct)

UN Sec Council statement (from Friday) condemned 'highly provocative' North Korean missile launch

US Ambassador to UN Haley: UN Security Council may run out of options with regard to North Korea. Iran, Syria and North Korea will be major focus at UN Gen Assembly next week

US Sec of State Tillerson: increasingly aggressive North Korean threatens the region and endangers the world

North Korea said to be aiming to establish "military equilibrium" with US; "will make the US rulers dare not talk about military option"

Europe:

ECB's Praet (Belgium): Reiterates Council view that euro zone still needs substantial stimulus to get back to the near 2% inflation target; will also respond if inflation were to get too high

ECB reportedly estimates 2018 QE reinvestment average at €15B/month (**Reminder: current QE program of €60B/month in bond purchases is expected to be wound down during 2018)

Bank for International Settlements (BIS) Quarterly Review: Strong outlook with low inflation spurs risk-taking

Forza Italia party chief Berlusconi (former PM) lays policy priorities in marking a formal return to Italy's political stage

Foreign Sec Johnson laid out his vision for Brexit; believes it can still deliver £350M a week extra for the NHS (**Note: Various cabinet colleagues accuse Johnson of "backseat driving" on Brexit)

UK Interior Sec Rudd: Johnson was not starting a leadership bid by setting out his plans for Brexit in a newspaper article, adding that his intervention was "absolutely fine"

Sovereign rating actions from Friday:

S&P raised Portugal sovereign rating to investment grade, raises one notch to BBB- from BB+; outlook Stable

Moody's raised Ireland's sovereign rating to A2 from A3; outlook revised to Stable from Positive

S&P affirmed Cyprus sovereign rating at BB+; outlook revised to Positive from Stable

S&P affirmed Russia sovereign rating at BB+; outlook Positive

S&P affirmed Austria and Finland sovereign ratings at AA+; outlook Stable

Economic data

(AT) Austria Aug CPI M/M: -0.1% v -0.3% prior; Y/Y: 2.1% v 2.0% prior

(CZ) Czech Aug PPI Industrial M/M: 0.2% v 0.1%e; Y/Y: 1.4% v 1.3%e

(HK) Hong Kong Aug Unemployment Rate: 3.1% v 3.1%e

(EU) Euro Zone Aug CPI M/M: 0.3% v 0.3%e; Y/Y (final reading): 1.5% v 1.5%e; CPI Core (final reading) Y/Y: 1.2% v 1.2%e

Fixed Income Issuance:

(NO) Norway sold total NOK6.0B vs. NOK6.0B indicated in 12-month Bills; Avg Yield 0.39% v 0.41% prior; Bid-to-cover x v 2.42x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.5% at 382.5, FTSE +0.3% at 7235, DAX +0.6% at 12591, CAC-40 +0.4% at 5235, IBEX-35 +0.7% at 10391, FTSE MIB +0.7% at 22381, SMI +0.4% at 9061, S&P 500 Futures +0.2%]

Market Focal Points/Key Themes: European Indices start the week of on the front foot continuing the momentum from the end of last week, with the dollar reach an 8 week high against the yen ahead of the FOMC rate decision mid week. On the corporate front Fingerprint cards continue to fall after guiding Q3 Rev short of expectations, whilst Ryanair trades lower after cancelling over 150 flights after 'Messing up' Pilot holidays. Elsewhere Petra Diamonds trade sharply lower after prelim results, whilst in the healthcare space Thrombogenics trade higher after regaining rights to JETREA.

Equities

Consumer discretionary [(Ryanair [RYA.UK] -3.4% (Flight cancellations)]

Materials: [Petra diamonds [PDL.UK] -8.6% (Prelim FY17 results)]

Financials: [Esure [ESUR.UK] +6.8% (Controlling shareholder mulling sale), Hiscox [HSX.UK] -2% (Hurricane Harvey claims estimates)]

Technology: [Fingerprint Cards -22% (FINGB.SE] -21% (Q3 guidance)]

Telecom: [Nokia [NOKIA.FI] +1.2% (Received decision in patent license arbitration with LG Elec)]

Healthcare: [Thrombogenics [THR.BE] +17.5% (Regains global rights to JETREA (ocriplasmin))]

Energy: [Seabird Exploration [SBX.NO] -59% (Private placement)]

Speakers

ECB noted that base effect seen affecting inflation in coming quarters. Combined impact of base effects from the energy and unprocessed food HICP components will lower headline inflation in the first quarter of 2018, but raise it in the following quarter. September staff projections foresaw a V-shaped path for headline inflation

ECB's Hansson (Estonia): ECB steps could involve new refinancing operations, reworked guidance and more details on reinvestments

France Budget Min Darmanin: 2017 GDP growth seen at 1.7% vs. 1.5% official govt target

Spain Fin Min de Guindos: No market impact from any instability resulting in Catalonia region. Companies were leaving Catalonia due to high taxes. Unemployment is falling faster than govt projections as domestic economy was growing over 3%

Italy Fin Min Podoan: Domestic banks efficiency has improved due to govt measures; NPLs were falling at a faster rate. Pubic backstop and deposit insurance is needed for EU banking union

Greece PM Tsipras: Optimistic to see above target primary surplus in 2017. Country needed to complete 3rd bailout review asap despite technical and political difficulties. Aiming to complete prior actions by November

China PBOC Adviser Sheng Songcheng: Now is not the time to change the CNY currency (Yuan) regime

China PBoC said to be working on draft proposal for foreign access to financial sector

China FX Regulator SAFE reiterated view that CNY currency (Yuan) exchange rate was stable even with recent FX appreciation

Currencies

USD/JPY was at a 2-month high with the pair above 111.30 ahead of the NY Morning. Dealers were eyeing the upcoming FOMC policy meeting mid-week meeting for clues on whether interest rates could rise again by year-end

EUR/USD was little changed at 1.1940 area with dealers seeing little impetus for movement before Wednesday's Fed policy meeting

Yields on 10-year Portuguese government bonds drop faster than their euro zone counterparts early Monday after the sovereign's upgrade to BBB-, an investment-grade rating, by S&P after the close Friday

Fixed Income

Bund futures trade little changed at 161.37 as investors await a number of speeches by European and U.K. central bankers this week, as well as the US Federal Reserve's meeting. Continued downside targets 161.03 while upside resistance stands initially at 162.07, followed by 163.27.

Gilt futures trade at 125.42 up 12 ticks with little in the way of UK economic data, Gilts will take their lead from the performance of core European government bonds.. Continued downside eyeing 124.91. Upside targets 127.90 then 128.24.

Monday's liquidity report showed Friday's excess liquidity fell to €1.7655T from €1.7660T and use of the marginal lending facility fell to €109M from €115M.

Corporate issuance saw $42.8B last week via 66 tranches, bringing YTD issuance to above $1.03T. For the week ahead analysts forecast around $25B to come to market. In Euro denominated issuance ~€35B came to market via 39 issuers and 49 tranches

Looking Ahead

(UR) Ukraine Q2 Final GDP Q/Q: 0.6%e v 0.6%prelim; Y/Y: 2.4%e v 2.4%

05:30 (BE) Belgium Debt Agency (BDA) to sell €3.5B in 2024, 2027 and 2034 OLO Bonds

05:30 (NL) Netherlands Debt Agency (DSTA) to sell €2.0-4.0B in 3-Month and 6-month Bills

06:00 (PT) Portugal Aug PPI M/M: No est v -0.3% prior; Y/Y: No est v 2.2% prior

06:45 (US) Daily Libor Fixing - 07:00 (IN) India announces details of upcoming bond sale (held on Fridays)

07:00 (BR) Brazil Sept IGP-M Inflation (2nd Preview): 0.4%e v 0.3% prior

07:25 (BR) Brazil Central Bank Weekly Economists Survey

08:00 (PL) Poland Aug Employment M/M: 0.1%e v 0.3% prior; Y/Y: 4.6%e v 4.5% prior

08:00 (PL) Poland Aug Average Gross Wages M/M: -1.1%e v -0.1% prior; Y/Y: 5.7%e v 4.9% prior

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada July Int'l Securities Transactions (CAD): No est v -0.9B prior

08:30 (CH) Swiss Government question time in Parliament

09:00 (FR) France Debt Agency (AFT) to sell combined €4.0-5.2B in 3-month, 6-month and 12-month Bills

09:30 (EU) ECB announces Covered-Bond Purchases - 09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

09:50 (UK) BOE to buy £1.125B in in APF Gilt purchase operation (3-7 years)

10:00 (US) Sept NAHB Housing Market Index: 67e v 68 prior

10:30 (DE) ECB's Lautenschlaeger (Germany) in Basel

11:00 (UK) BOE Gov Carney at IMF in Washington DC

11:00 (CO) Colombia July Trade Balance: -$0.6Be v -$0.1B prior

11:30 (US) Treasury to sell 3-month and 6-month bills

14:15 (DE) SPD's Schulz takes questions at Televised Town-Hall Event in Luebeck

14:15 (CA) Bank of Canada (BOC) Dep Gov Lane

16:00 (US) July Total Net TIC flows: No est v $7.7B prior; Net Long-Term Tic Flows: No est v $34.4B prior

16:00 (US) Weekly Crop Progress Report

Dollar To Remain Contained Ahead Of Fed Decision

September 18: Five things the markets are talking about

This is a busy week both on the central bank and parliamentary election front.

Among the G7, the Bank of Japan (Thursday) and the Fed (Wednesday) hold policy meetings this week, as to does Norway’s Norges Bank (Thursday).

The BoJ is expected to leave its policy unchanged and probably will not reveal when it will unwind stimulus, but could signal determination to keep the yield curve under control.

However, for the Fed, expectations are uncertain. Recent hurricane activity is expected to cloud the outlook for the Fed – intensifying the problem is the delay in the collection and publication of official data. Expectations are for revisions going forward. Interest rates are expected to remain on hold, while the market assigns a +50% probability of a December rate increase. Many anticipate the FOMC to begin reducing the Fed’s balance sheet.

In the U.K, Brexit strategy is in focus as PM May prepares to outline her revised approach this Friday, while in Germany, the final days of the federal parliamentary campaign will play out before next Sunday’s vote (Sept. 24). Down-under, New Zealand goes to the polls this Saturday (Sept. 23).

1. Stocks given the green light

The bullish sentiment that stoked more records stateside on Friday has carried through into the new week, with both European and Asian rallying across the board.

In Japan capital markets were shut for respect-for-the-aged day.

In Hong Kong, equities jumped to the highest a 27-month overnight, as regional bourses hit decade highs, while stronger-than-expected Chinese loan data aided sentiment. The Hang Seng index rose +1.3%, while the China Enterprises Index gained +1.2%.

Down-under, and Australia’s S&P 200 was up +0.5% at the close, while in S. Korea, the Kospi index climbed +1.4%.

In China, equities were boosted by stronger domestic data that added to views that economic growth is holding up and by the loosening of margin requirements on stock index futures trading. The blue-chip CSI300 index rose +0.3%, while the Shanghai Composite Index also added +0.3%.

In Europe, regional bourses all start the week on the front foot, continuing Friday’s momentum as the U.S dollar reaches a two-month high outright against the yen (¥111.40).

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx600 +0.5% at 382.5, FTSE +0.3% at 7235, DAX +0.6% at 12591, CAC-40 +0.4% at 5235, IBEX-35 +0.7% at 10391, FTSE MIB +0.7% at 22381, SMI +0.4% at 9061, S&P 500 Futures +0.2%

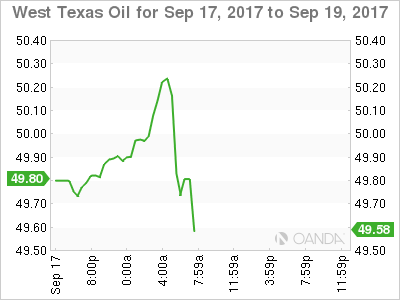

2. Oil bid on rising refinery demand, falling rig count, and gold lower

Ahead of the U.S open, crude oil prices remain better bid, trading atop of multi-month highs as the number of U.S rigs drilling for new production fell and refineries continued to restart after getting knocked out by Hurricane Harvey.

Brent crude futures are at +$55.91 a barrel, up +29c, straddling their five-month high print touched last Thursday, while U.S West Texas Intermediate (WTI) crude is trading up +41c, or +0.8%, at +$50.30, near their three-month high print also reached last Thursday.

Note: Oil refineries across the Gulf of Mexico and the Caribbean are also restarting after being shut due to hurricanes Harvey and Irma.

Also supporting crude prices is the number of rigs drilling for oil in the U.S fell sharply last week. Friday’s Baker Hughes report revealed that U.S energy firms cut seven oilrigs in the week to Sept. 15, bringing the total to 749, the fewest since June.

In the Euro session, gold has slipped to its lowest level in a fortnight as the dollar and stocks rally, while prospects of U.S monetary policy tightening ahead of a Fed meeting is also weighing on the metal. The ‘yellow’ metal is down -0.3% at +$1,315.36 an ounce.

3. Sovereign yields rise

This week, the main event will be the Federal Open Market Committee (FOMC) meeting, starting tomorrow and concluding with Wednesday’s press conference (02:30 pm EDT).

U.S policy makers are expected to take another step towards policy “normalisation,” but will it be this week? It’s not a slam-dunk, as persistently subdued global inflation, despite a pick-up in growth, remains somewhat of an impediment to tightening monetary policy. As such, the market is not wholly convinced that the Fed will move on rates again this year, with a December change put at less than a +50% probability.

The yield on 10-year Treasuries has backed up +1 bps to +2.21%, the highest yield in almost four-weeks. In Germany, the 10-year Bund yield has gained less than +1 bps to +0.44%, the highest in more than a month, while Britain’s 10-year Gilt yield has climbed less than +1 bps to +1.31% – the highest print in more than 10-weeks.

4. Dollar to remain contained ahead of Fed decision

Last week’s positive U.S inflation surprise was not sufficient to convince the market of a noteworthy continuation of the Fed rate hike cycle. Investor focus now shifts to the Fed directly.

The U.S dollar is unlikely to move much before Wednesday’s Fed announcement as is usual in the run-up to these meetings. With rates expected to remain on hold should not mean much for the dollar unless there is a ‘hawkish’ signal from this week’s Fed meet.

Ahead of the open, the dollar is a tad firmer across the board. EUR/USD at €1.1931 is down -0.16%, USD/JPY is up +0.5% at ¥111.40, while GBP/USD down 0.3% at £1.3554.

Note: Sterling is down after rallying on Thursday and Friday as caution sets in before a speech by BoE Governor Mark Carney at 10:00 am EDT.

Note: JPY outright is trading atop of its two-month lows as investors are shaking off risk fears of political threats, but also because there is a public holiday in Japan, which means less liquidity in the market.

5. Euro annual inflation up to +1.5%

Data this morning from Eurostat showed that Euro area (monetary union of 19 members) annual inflation was +1.5% in August 2017, up from +1.3% in July 2017. In August 2016 the rate was +0.2%.

European Union (28 member states) annual inflation was +1.7% in August 2017, up from +1.5% in July. A year earlier the rate was +0.3%.

Note: ECB President Draghi indicated earlier this month that the bank would outline plans next month to scale down its +€2.3T bond-buying program (QE).