Sample Category Title

Pound Soars to 1-Year High after Inflation Beat; Dollar also Up, Euro Under Pressure

The British pound surged to a one-year high in European trading on Tuesday as traders bet on a more hawkish Bank of England following stronger-than-expected UK inflation data. The US dollar extended yesterday's impressive gains against the yen but the euro struggled. The New Zealand dollar was another major gainer, while gold reversed its earlier losses following fresh threats from North Korea.

The main data in today's European session was the August inflation release out of the UK. Headline inflation rose back to May's four-year high of 2.9% year-on-year in August, beating expectations of 2.8% and up from July's 2.6% rate. Core inflation was also stronger-than-expected, rising to 2.7% y/y – its highest since November 2012. Forecasts were for core CPI to rise from 2.4% to 2.5% in August.

In a further sign that the inflation upswing from the weaker pound has yet to peak, input and output prices both came in above their top estimates. The figures will likely strengthen the argument for the Bank of England hawks that interest rates need to go up. The Bank will announce its latest policy decision on Thursday and expectations have been increasing in recent days that the MPC is heading for another split vote, with more members likely to vote for a rate hike.

The pound shot to a one-year high of $1.3287 after the data, and was last trading at $1.3265, up 0.8% on the day. It was also up sharply against the euro and the yen, jumping to a more than one-month high against both currencies. The euro breached the key 0.90 level to hit a session low of 0.8981 pounds, while against the yen, the pound hit a high of 145.94.

The euro was under pressure against the resurgent dollar for a second day, sliding to as low as $1.1924 in mid-session. A converging of views by ECB policymakers that the central bank is moving towards tighter monetary policy failed to lift the single currency. Several ECB officials spoke in favour of policy normalization yesterday, though comments that the process will be gradual, as well as the potential impact of a "persistent exchange rate shock" weighed on the euro.

However, the euro later ticked higher, rising to $1.1955, as ECB Vice President Vitor Constancio started speaking. Speaking in Frankfurt, Constancio defended the ECB's unconventional policy tools and said he was confident inflation will eventually hit the target.

The greenback continued to benefit from the improving risk-on sentiment, brought on by investor relief that the impact of Hurricane Irma was less destructive than initially feared, as well as by North Korea's inaction over the weekend. The dollar briefly broke above 110 yen before dropping slightly to around 109.85 yen. The dollar index was also unable to retain a key level, slipping below 92.0 after climbing above the level for the first time this week.

The only data out of the US today was the latest JOLTS job openings. The number of job openings rose to 6.170 million in July from a downwardly revised 6.116 million in June.

The yen's and the Swiss franc's weakness were notable against all major currencies, though gold found support from ongoing unease about tensions in the Korean peninsula. North Korea issued a new threat against the United States today following the UN's decision yesterday to adopt tougher sanctions on the hermit state. The precious metal recovered from a 1½-week low of $1322.15 an ounce to rise to around $1328 an ounce in late European trading.

In other currencies, the New Zealand dollar got a boost from the latest election polls in New Zealand that put the ruling National party ahead of the Labour party. The polls lifted the kiwi to a high of $0.7320 earlier in the session before easing to around $0.7290. The kiwi has come under pressure in recent weeks from Labour's strong performance in the polls, whose campaign pledge includes scrapping the National party's planned tax cuts.

Crude oil was on track for a second day of gains as prices were boosted after OPEC raised its forecasts for demand for 2018. The group also said it had cut output in August, giving the commodity a much-needed reprieve following the dip in demand seen as a result of the refineries closures in the US due to the hurricanes.

WTI crude was last trading up 0.4% on the day at $48.26 a barrel and Brent crude was 0.8% higher at $54.29 a barrel. The API's weekly inventory report expected later today should shed more light on the impact of the hurricanes on US stock levels.

Higher Inflation in UK May Force Bank of England to Raise Rates

The euro keeps falling against the US dollar due to increased interest in risky assets. Greenback bulls were supported by positive data from the NFIB small business index that improved to 105.3 in August against an expected decline to 104.8. At the same time, JOLTS Job openings report shows that the number of open vacancies in America in July grew to 6.17 million versus an anticipated decline to 5.96 million. Overall we are seeing positive tendencies from the labour market, which is likely to lead to wage growth and as a result to more consumer spending which remains the basis of economic expansion in the US.

Strong data from the UK pushed the GBP/USD price to the 1-year maximum. Traders reacted positively to the report on consumer price growth in August to 2.9% that is by 0.1% more than forecasted and higher than July's 2.6% rise in inflation. Sterling bulls were buoyed by the news as it increases the probability of hawkish rhetoric by Bank of England officials that will vote on interest rates on Thursday. Volatility for the pair is likely to remain high tomorrow on the background of British labour market data release.

The Australian dollar today was under pressure following the decline in the NAB business confidence index that in August dropped to 5 against 12 in July. Lower prices for commodities also have a negative impact on traders' sentiment. A slight spike in volatility is possible after the release of the Westpac report on Australia's consumer sentiment tomorrow at 00:30 GMT.

EUR/USD

The EUR/USD quotes were able to break through the inclined support line and overcoming the 1.1925 mark may become a confirmation for a sell signal with potential targets at 1.1825 and 1.1750. On the other hand, in case of the price crossing the SMA100 in the 15-minute chart, we may see growth resume with immediate goals at 1.2000 and 1.2070.

GBP/USD

The British pound demonstrated confident growth within the ascending channel and the recent break through the resistance at 1.3250 may result in a continued increase to the next target price at 1.3400. A change in trend is possible after leaving the limits of the channel and breaking through support at 1.3150. The MACD signal line is falling and that may be a signal for a continued downward correction to the lower limit of the channel.

AUD/USD

The AUD/USD resumed its decline after the recent rebound from the psychologically important 0.8000 mark. In case of breaking through this support line, the closest targets will be located at 0.7950 and 0.7870. In this case the stop should be set above the local maximum at 0.8050. It's not likely that we will see growth resuming today.

US: Small Business Confidence Remains Upbeat

The NFIB's small business optimism index rose 0.1 points to 105.3. The August headline print came in above market expectations, which called for a slight pullback to 104.9. Readings above the 105 level have been recorded only during select periods, such as in the mid-2000s and 1983, with today's print near record levels.

Movements among the sub-components were mixed with four posting a gain, five declining, and one remaining unchanged. Gains in expectations for higher sales led the way (+5 to 27 percent), followed by the belief that now is a good time to expand (+4 to 27 percent), and capital outlay plans (+4 to 32 percent). The latter marks the strongest reading since 2006. Moreover, earnings trends eased off one point but remained elevated at -11.

Most labor market indicators eased off on the month, but continued to hold up at a high level. Small businesses added jobs at a solid pace in August with the average change in employment per firm at +0.18 m/m, while plans to increase employment pulled back slightly (-1 to 18 percent). When stacked against past performance, both indicators are showing some of the best prints since the mid-2000s.

Job openings also pulled back, dropping 4 points on the month. But this followed a 5-point increase in the month prior, leaving the level of job openings at 31 percent - still one of the best showings since 2000. Over half of businesses seeking workers (52 percent) had few or no qualitied applicants, with 'quality of labor' concerns being the second most significant headwind to expansion (19 percent), right after taxes (20 percent).

Given already tight conditions, businesses continued to boost worker compensation (+1 to 28 percent). But plans to do so in the next three months pulled back for a second consecutive month, falling 1 point to 15 percent in August. The latter is still a decent reading but somewhat softer compared to the 18 percent recorded between March and June.

The net percent of owners raising average selling prices increased one point, rising to a net 9 percent - the highest level since 2014, while plans to do so in the near future fell back three points to a still-decent 20 percent.

Key Implications

Small business confidence has managed hold on to the post-election gains. While an improved view of future conditions has certainly played a part, the boost in optimism has not been solely due to a shift in the forward-looking indicators. In fact, businesses have also been reporting better nominal sales and earnings trends. This is in line with stronger demand and improved economic growth recently, particularly through the consumer spending channel.

The improvement in capital expenditure plans is particularly encouraging given that it marks the strongest reading since 2006. It appears that improved optimism is finally trickling down to investment intentions - a trend that if sustained is likely to boost business investment and lead to improved productivity.

On the other hand, the slightly softer trend in worker compensation plans is a disappointing signal for wage growth. Still, given increasingly tight labor market conditions, it is unlikely to continue. Moreover, the 'share of owners that are raising prices' that is now back at highest level since 2014 is another encouraging sign regarding inflation.

Disruptions from Hurricane Harvey do not appear to have played a large part in today's report, given that the storm made landfall in Southeast Texas late in the month. Nonetheless, we anticipate some distortions to the data ahead, with the added impact of Hurricane Irma to augment volatility. Overall, downbeat sentiment among affected businesses is likely to weigh on the headline measure in the near-term, with a subsequent boost to economic activity as reconstruction efforts and a gradual return to normalcy work in the opposite direction.

Pound Climbs to 12-Month High on Inflation Jump

The British pound has posted strong gains in the Tuesday session. In North American trade, GBP/USD is trading at 1.3264, up 0.80% on the day. On the release front, British CPI picked up speed, climbing 2.9% in August. This beat the estimate of 2.9%. In the US, JOLTS Job Openings improved to 6.17 million, easily beating the forecast of 5.96 million. On Wednesday, the UK releases wage growth, while the US will publish PPI.

The pound posted a strong gain of 1.7% last week, and the rally has resumed on Tuesday. Earlier in the Tuesday, session, the pair jumped to 1.3288, its highest level since September 2017. The pound was buoyed by strong inflation data, as CPI improved to 2.9% in August, up from 2.6% a month earlier. CPI, the primary gauge of consumer inflation, jumped on higher clothing and fuel prices. With inflation remaining above the BoE's target of 2.0%, policymakers will be under renewed pressure to raise interest rates. However, the economy has lost steam in 2017, and rate hike could hurt the economy. How will this play out at the BoE? Policymakers won't have much time to mull over the latest inflation readings, as the BoE holds its monthly policy meeting on Thursday. Whether the bank opts to raise rates or stay on the sidelines, traders should be prepared for some movement from the pound.

Bexit negotiations are grinding slowly, with plenty of major gaps between Britain and the European Union. Britain must take legislative measures to untangle itself from the continent, and the May government took a first step in that direction on Monday, as parliament voted on the EU Withdrawal Bill. The bill, which will convert all existing EU legislation into UK law, passed its second stage, with the government winning the vote by 326-290. However, the bill is far from done, with many MPs, including Conservatives, tabling amendments. Prime Minister May, still smarting from a disastrous June election, the vote is a small victory on the long journey of navigating Britain out of Brexit. The US economy has been performing well in the second quarter. Preliminary GDP came in at a sizzling 3.0%, and the labor market remains close to capacity. Still, the Achilles heel of the economy remains stubbornly low inflation levels. Wage pressure has been limited, despite the fact that many businesses cannot fill job openings. Weak inflation has hampered the Fed's plans to raise interest rates a third time this year, and the odds of a December hike have dipped to just 31%, as the markets are increasingly doubtful that the Fed will make a move before next year. Will the inflation picture improve? We could see better numbers this week for August inflation – PPI is expected to improve to 0.3% on Tuesday, and the same gain is forecast for CPI on Wednesday. Both estimates are higher than the July readings.

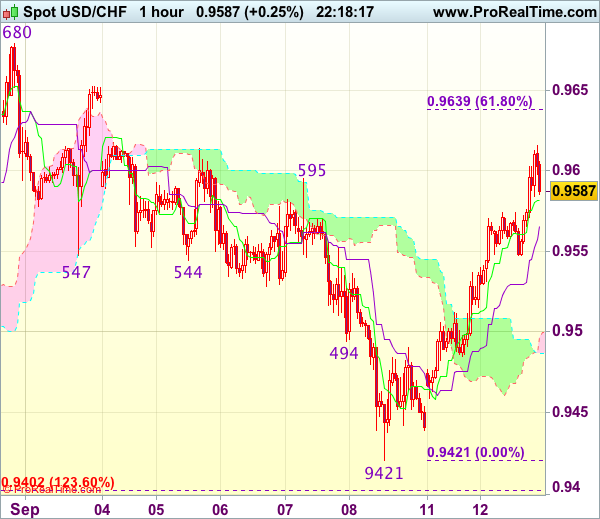

Trade Idea Wrap-up: USD/CHF – Buy at 0.9540

USD/CHF - 0.9592

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 0.9582

Kijun-Sen level : 0.9566

Ichimoku cloud top : 0.9500

Ichimoku cloud bottom : 0.9487

Original strategy :

Buy at 0.9550, Target: 0.9650, Stop: 0.9515

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9540, Target: 0.9640, Stop: 0.9505

Position : -

Target : -

Stop : -

The greenback extended the rebound from 0.9421 (last week’s low) in line with our bullish expectations, this anticipated rise together with the breach of previous resistance at 0.9595 add credence to our view that low has been formed at 0.9421 and consolidation with upside bias remains for further gain to 0.9635-40 (61.8% Fibonacci retracement of 0.9773-0.9421), however, near term overbought condition would limit upside and reckon resistance at 0.9680 would remain intact.

In view of this, we are looking to reinstate long on dips as 0.9550-55 should limit downside and bring another upmove later. Below 0.9525-30 would defer and risk correction to 0.9500 but downside should be limited and 0.9450-60 would remain intact, bring another rebound later.

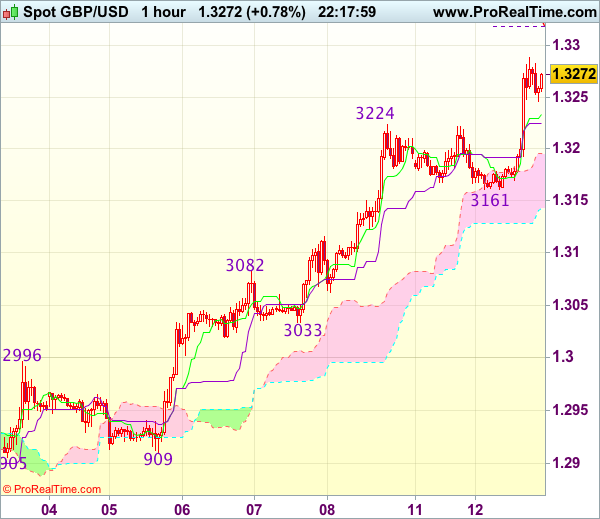

Trade Idea Wrap-up: GBP/USD – Buy at 1.3175

GBP/USD - 1.3266

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3241

Kijun-Sen level : 1.3225

Ichimoku cloud top : 1.3195

Ichimoku cloud bottom : 1.3143

Original strategy :

Buy at 1.3175, Target: 1.3275, Stop: 1.3140

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3175, Target: 1.3275, Stop: 1.3140

Position : -

Target : -

Stop : -

Cable’s intra-day breach of previous chart resistance at 1.3269 confirms medium term upmove has resumed and bullishness remains for further gain to 1.3290-00, however, loss of near term upward momentum should prevent sharp move beyond 1.3330 and reckon 1.3350-60 (61.8% projection of 1.2909-1.3224 measuring from 1.3161) would hold from here, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise at current level and would be prudent to buy cable on subsequent pullback as support at 1.3161 should contain downside and bring another upmove. Below 1.3145-50 would defer and risk correction to 1.3115-20 but downside should be limited and support at 1.3082 (previous resistance) should remain intact.

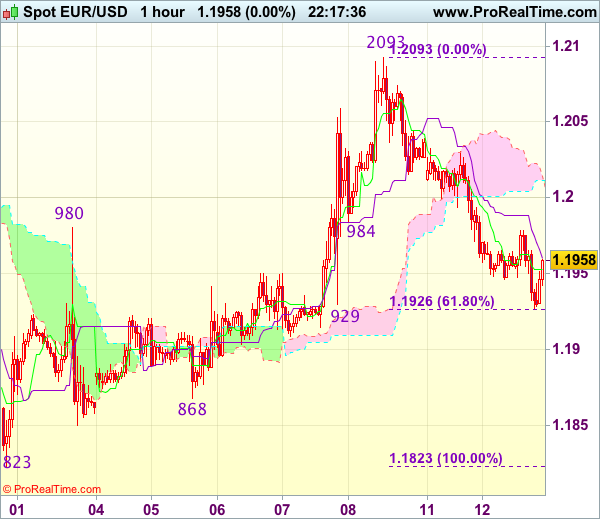

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1954

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1952

Kijun-Sen level : 1.1960

Ichimoku cloud top : 1.2011

Ichimoku cloud bottom : 1.2006

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency has fallen again after brief recovery, suggesting the decline from last week’s high of 1.2093 is still in progress for retracement of recent rise, hence weakness to 1.1900 cannot be rule out, however, loss of near term downward momentum should prevent sharp fall below previous support at 1.1868 and price should stay well above another previous support at 1.1823, bring rebound later.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above resistance at 1.1978 would bring recovery to 1.2000, however, reckon upside would be limited to resistance at 1.2030, bring another decline.

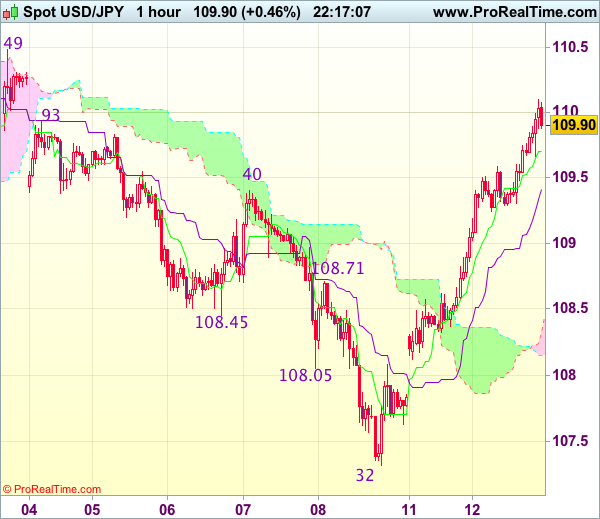

Trade Idea Wrap-up: USD/JPY – Buy at 109.00

USD/JPY - 109.85

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 109.70

Kijun-Sen level : 109.41

Ichimoku cloud top : 108.32

Ichimoku cloud bottom : 108.14

Original strategy :

Buy at 109.30, Target: 110.30, Stop: 108.95

Position : -

Target : -

Stop : -

New strategy :

Buy at 109.00, Target: 110.20, Stop: 108.65

Position : -

Target : -

Stop : -

As the greenback has surged again today after brief pullback, dampening our bearishness and suggesting the rise from 107.32 low is still in progress, hence further gain towards resistance at 110.49 would be seen, however, near term overbought condition should limit upside to resistance at 110.67, risk from there has increased for a retreat to take place soon.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as 109.00 should limit downside. Below 108.70 would defer and risk correction to 108.50 but still reckon downside would be limited to 108.30-35 and bring another rally later.

Sterling Rebound Accelerates as Inflations Jumps Higher

- European equity indices show gains of approximately 0.5% as the risk rally continues. The FTSE 100 underperforms as the strengthening of sterling weighs. US equities also start the session with modest gains.

- UK inflation is on the rise again, accelerating more than forecast in August after the biggest surge in clothes prices in almost three decades. The jump to 2.9% from 2.6% in July puts the spotlight squarely back on one of the most prominent economic repercussions of the Brexit vote in 2016.

- The 1% cap on pay rises for UK public sector workers is to be scrapped after the government agreed to a 1.7% annual pay rise for prison officers and an effective 2% rise for police officers for the current year.

- US NFIB small business optimism slightly increased from 105.2 to 105.3 in August, while consensus expected a small decline to 104.8. The outcome was too close to consensus to bother markets. The indicator remains near multiyear highs.

- OPEC crude oil production fell last month for the first time since April, in a boost to the cartel's beleaguered efforts to reduce output and rein in the global supply glut. The cartel has revised higher its global oil demand growth forecasts for this year and next as consumption in the second quarter of 2017 surpassed expectations.

- The German economy is set to grow by more than 2% this year adjusted for calendar effects, which would be the strongest rate in six years, the BDI industry association said as it lifted its growth forecast for Europe's biggest economy.

- Underlying inflation in Sweden hit the central bank's 2% target for the second straight month in August, supporting arguments that the time is right to start tightening monetary policy amid signs of an overheating economy. EUR/SEK declined from 9.59 towards 9.52.

Rates

Repositioning goes on

Global core bonds extended yesterday's decline, but the pace slowed. Risk sentiment on stock markets remained positive. Stronger than expected, but second tier, eco data (UK CPI, see FX, and US NFIB small business optimism) and EMU/US supply also weighed on core bonds. The confirmation of yesterday's technical breaks of US yields back above previous support levels (5-yr: 1.7%, 10-yr: 2.1%, 30-yr 2.68%) suggests that the downtrend since the start of the Summer is over and that we've entered a consolidation phase ahead of next week's FOMC meeting. Markets are still too dovish positioned according to us with US rate markets not even discounting a complete rate hike by the end of 2018.

At the time of writing, US yields increase by 1.2 bps (2-yr) to 2.8 bps (5-yr). Changes on the German yield curve vary between +1.7 bps (2-yr) and +3.6 bps (10-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrow up to 3 bps.

The Dutch debt agency tapped the on the run 10-yr DSL (€2.2B 0.75% Jul2027). The amount sold was below the maximum targeted €3B, but that's almost every time the case at Dutch auctions. The treasury didn't disclose the bid cover. Austria launched two new bonds via syndication. A new 5-yr RAGB (Sep2022) was priced to yield MS -36 bps, tighter than guidance in the MS -35 bps area. Austria also managed to raise €1B with a centennial bond which drew in excess of €11B demand. The 100-yr RAGB printed at MS +50 bps, at the lower end of the MS+50/55 bps guidance. The US Treasury continues its refinancing operation tonight with a $20B 10-yr Note auction. The WI trades currently around 2.16%.

Currencies

Dollar extends rebound

Today, the risk rebound continued. Core yields rose further. The dollar remained the major beneficiary among the major currencies. USD/JPY outperformed and is testing the 110 barrier. The progress of the dollar against the euro remains more modest with EUR/USD trading in the 1.1940 area. There were few data to support the move, but that might change later this week with the US price data scheduled for release tomorrow and on Thursday.

The risk rebound continued in Asia this morning. Japanese equities outperformed on yesterday's decline of the yen. The dollar maintained yesterday's gains against the euro and the yen, but there was no additional progress yet. The UN security council approved a watered-down US proposal on additional sanctions against North Korea. Markets pondered the chances on a possible reaction of North Korea.

The risk rebound was also extended in Europe. There were no important data in EMU. Core German and US bond yields rose more or less in lockstep. If anything, German yields rose slightly more than US ones, but this was probably a simple catching up move on yesterday's rise in the US. Whatever, the dollar remained well bid across the board. EUR/USD hovered toward the lower barrier of the 1.1950/80 range. USD/JPY drifted higher to the 109.75 area.

The dollar comeback gained some additional momentum going into the start of the US session. The NFIB small business confidence rose slightly from 105.2 to 105.3. A limited setback to 104.8 was expected. The report was no major factor for trading, but it helped to sustain a positive sentiment both for the dollar and for risky assets. The Trump administration preparing a new campaign to win support for a substantial tax reduction was maybe also a minor USD supportive. However, for now, we consider current move in the first place an unwinding of 'excessive' USD shorts. EUR/USD trades currently in the 1.1940 area. USD/JPY is testing the 110 mark.

To conclude: the risk-on repositioning continued and the dollar still profits slightly more than the euro (and evidently also the yen). Tomorrow and on Thursday, the focus will shift to the US price data. Interesting to see whether they are good enough to reinforce the USD positive momentum.

Sterling rebound accelerates as inflations jumps higher

Of late, sterling succeeded a gradual but sustained rebound especially against the euro. There was no obvious driver. UK eco data were mixed of late. There was also very little progress in the Brexit negotiations. Today, the eco data came again in the spotlight. UK August inflation rose much more than expected from 2.6% Y/Y to 2.9%, matching the highest level in 5 year. The consensus expected a rise to 2.8%. Core inflation was also above consensus at 2.7% Y/Y. At the August policy meeting the BoE kept a wait-and-see bias even as it was aware that inflation could reach 3.0%. Even so, the current uptick will probably force the BoE to give more weight to inflation in its policy assessment, even as growth slows and as Brexit uncertainty persists. We don't expect the BoE already to change course on Thursday, but chances on a rate hike will rise of the August upward surprise will be confirmed further down the road. The sterling rebound accelerated after the CPI release. EUR/GBP dropped temporary below the 0.90 mark and trades currently around 0.9010. Cable set a minor new top at around 1.3288, even as the dollar was well bid across the board.

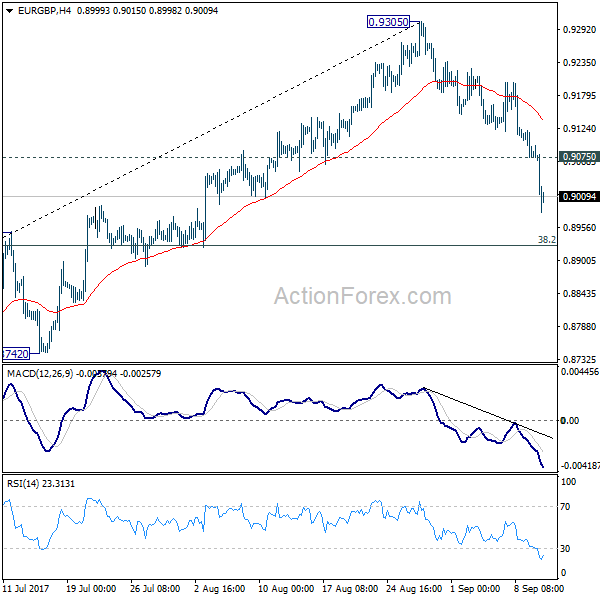

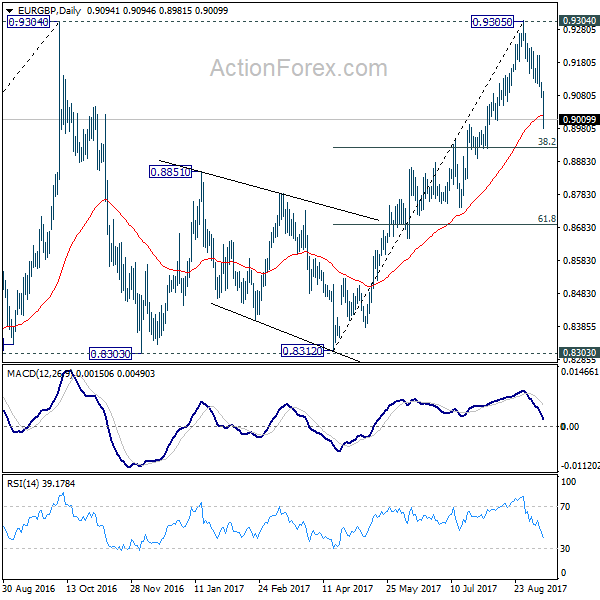

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.9062; (P) 0.9091; (R1) 0.9108; More

EUR/GBP's fall from 0.9305 short term top accelerates to as low as 0.8981 so far. Such decline is likely the third leg of the consolidation from 0.9304. Intraday bias remains on the downside for 38.2% retracement of 0.8312 to 0.9305 at 0.8926 first. Break will target 61.8% retracement at 8691 and below. On the upside, above 0.9075 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes. Firm break of 0.9799 high will target 61.8% projection of 0.5680 to 0.9799 from 0.6935 at 1.1054.